Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

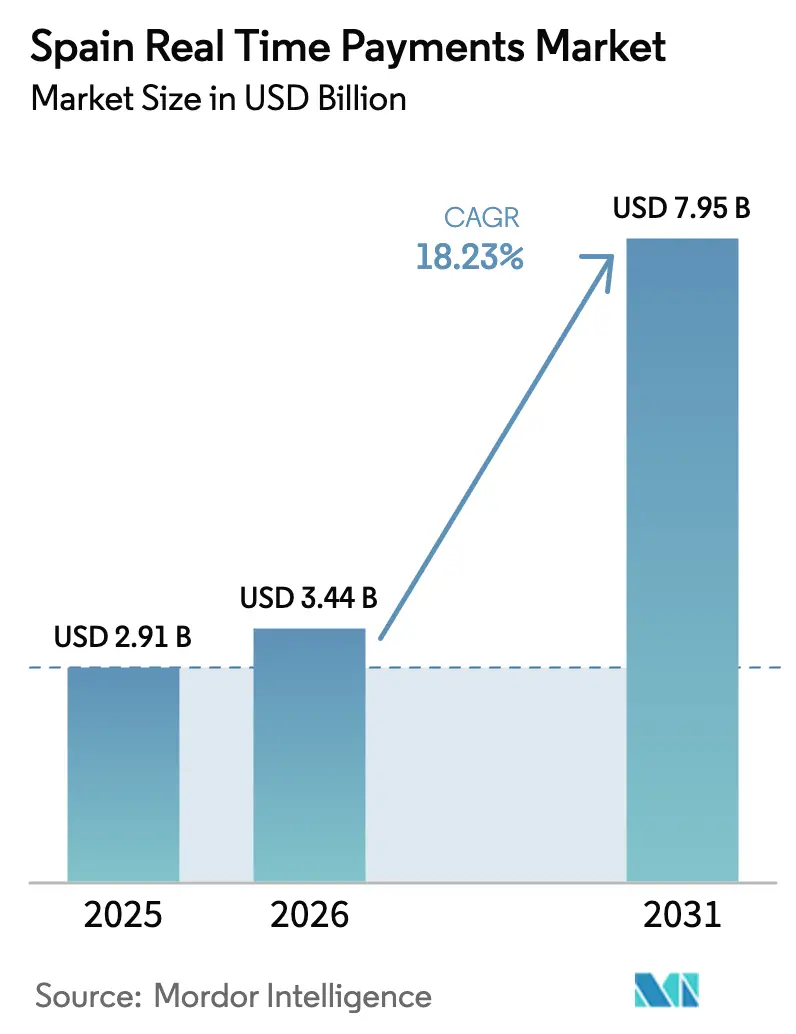

| Base Year Market Size (2025) | USD 2.91 Billion |

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 7.95 Billion |

| Growth Rate (2026 - 2031) | 18.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Real Time Payments Market Analysis by Mordor Intelligence

The Spain real time payments market size is expected to grow from USD 2.91 billion in 2025 to USD 3.44 billion in 2026 and is forecast to reach USD 7.95 billion by 2031 at 18.23% CAGR over 2026-2031. Rapid scale-up reflects Spain’s 53% instant-transfer penetration-well above the 15% European average. Mandated SEPA Instant Transfer rules effective January 2025, fee caps that equalize instant and regular credit transfers, and early ISO-20022 migration create strong compliance pressures that favor instant rails. [1]European Commission, “Regulation (EU) 2023/xxxx on Instant Payments,” ec.europa.eu Merchant demand for account-to-account (A2A) checkout, 5G-enabled mobile ubiquity, and rising fintech-bank partnerships further reinforce growth. Cloud modernization among mid-tier banks, coupled with domestic–cross-border initiatives such as EuroPA, widens addressable volumes and intensifies competition. However, fraud-as-a-service and fragmented legacy cores moderate momentum and shape risk-adjusted investment priorities.

Key Report Takeaways

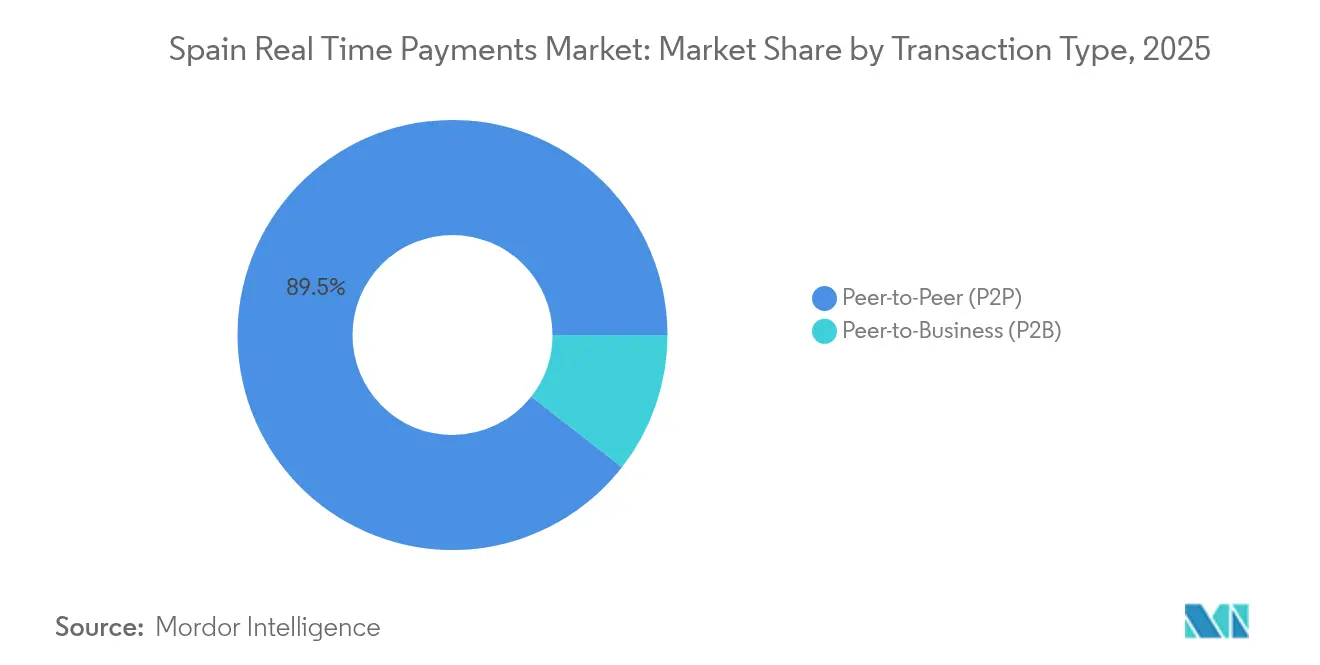

- By transaction type, peer-to-peer transfers led with 89.45% revenue share in 2025, while peer-to-business transactions are forecast to expand at a 18.87% CAGR through 2031.

- By component, platforms held 67.25% of 2025 revenue; services record the highest projected CAGR at 19.98% through 2031.

- By deployment model, cloud captured 54.70% of 2025 revenue and is rising at a 18.96% CAGR to 2031.

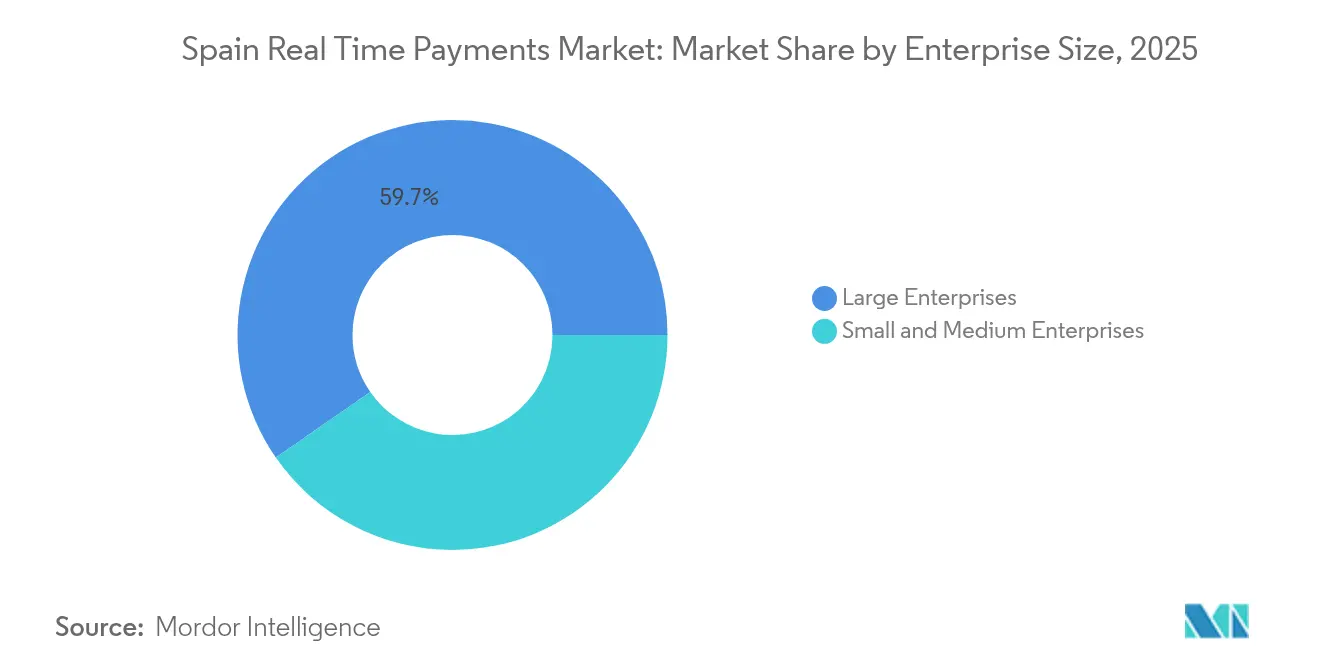

- By enterprise size, large enterprises commanded 59.65% market value in 2025, whereas SMEs show the fastest growth at a 19.74% CAGR.

- By end-user industry, retail and e-commerce accounted for 35.62% share in 2025; government and public sector is advancing at a 20.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Smartphone Penetration Coupled with 5G Roll-out | +3.2% | National, with early gains in Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Shift of Spanish Merchants to Account-to-Account Checkout at POS | +4.1% | National, concentrated in retail hubs | Short term (≤ 2 years) |

| Mandatory SEPA Instant Transfer Regulation Drives the Market | +5.8% | EU-wide, Spain early adopter | Short term (≤ 2 years) |

| ISO-20022 Migration Unlocking Data-Rich RTP Use-Cases | +2.9% | Global, Spain leading implementation | Long term (≥ 4 years) |

| Rise of FinTech–Bank Partnerships for Instant Salary and Gig-Worker Payouts | +2.4% | National, urban centers leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Smartphone Penetration Coupled with 5G Roll-out

Telefonica reached 90% 5G coverage across 1,500 municipalities by early 2025, delivering speeds up to 1,600 Mbps that enable ultra-low-latency payment processing. High smartphone usage dovetails with Bizum Pay’s NFC launch, positioning mobile-first adoption even as 66% of face-to-face payments remained cash in 2024. [2]Stripe, “2024 Spain Payments Report,” stripe.com Together, network upgrades and app innovation foster rapid retail acceptance and pave the way for wider Spain real time payments market adoption. Spain’s leadership in 5G Standalone, alongside Germany and Austria, cements the infrastructure base for future use cases.

Shift of Spanish Merchants to Account-to-Account Checkout at POS

Redsys processed EUR 505 billion (USD 545.4 billion) through 1.5 million POS terminals in 2024, illustrating immediate A2A integration potential. Amazon’s Bizum integration and 50,000+ merchants accepting the service—up 19% year-on-year—signal tipping-point dynamics. Contactless cards already comprise 67% of transactions, easing behavioral transition to instant A2A. Banco Santander’s zero-fee POS offer for new merchants removes cost friction. These developments accelerate Spain real time payments market penetration in retail environments.

Mandatory SEPA Instant Transfer Regulation Drives the Market

The EU regulation that took effect 9 January 2025 mandates sub-10-second euro transfers and fee parity with regular credits. [3]European Commission, “Regulation (EU) 2023/xxxx on Instant Payments,” ec.europa.eu CaixaBank scrapped instant-transfer fees for all clients from January 2025, highlighting compliance-driven competitive moves. Reporting deadlines were deferred to April 2026, yet infrastructure investments surged as banks raced to meet messaging and timestamp standards. Spain’s 53% instant-transfer share enables local institutions to leverage regulations for cross-border service advantage.

ISO-20022 Migration Unlocking Data-Rich RTP Use-Cases

Structured data enhances automated reconciliation and regulatory reporting, supporting e-invoicing mandates for firms over EUR 8 million (USD 8.64 million) turnover. CaixaBank’s EUR 5 billion (USD 5.4 billion) “Cosmos” plan funds compliance and analytics, underlining strategic importance. Rich messaging also supports EuroPA’s multi-country user journeys, aligning Spain real time payments market capabilities with future cross-border expectations. [4]European Payments Council, “ISO-20022 Migration Guide,” europeanpaymentscouncil.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Fraud-as-a-Service Targeting RTP Channels | -2.8% | National, urban areas most affected | Short term (≤ 2 years) |

| Fragmented Legacy Core Banking Systems among Mid-Tier Spanish Banks | -1.9% | National, regional banks concentrated | Medium term (2-4 years) |

| Processing Fee Caps Pressuring PSP Margins | -1.6% | National, affecting all PSPs | Short term (≤ 2 years) |

| Delayed Merchant On-Boarding due to KYC Bottlenecks | -1.2% | National, SME sector most impacted | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Fraud-as-a-Service Targeting RTP Channels

Eight in ten Spaniards reported scam attempts in 2024, and 7% lost at least EUR 5,000 (USD 5,400) via RTP fraud. Real-time irrevocability compresses fraud-detection windows, urging banks to adopt hybrid ML models and graph analytics. The threat heightens demand for secure services within the Spain real time payments market, where 63% of users ask for stronger bank protection.

Fragmented Legacy Core Banking Systems among Mid-Tier Spanish Banks

While major lenders fund multi-billion-euro digital programs, smaller regionals struggle to meet 10-second processing mandates, slowing overall Spain real time payments market rollout. Cloud-based managed services increasingly bridge capability gaps, yet integration and compliance costs weigh on budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: P2P Dominance Faces B2B Disruption

Peer-to-peer transfers controlled 89.45% of 2025 revenue, reflecting Bizum’s 1 billion annual transactions. However, the peer-to-business sub-segment is forecast to expand at 18.87% CAGR as merchants roll out instant A2A checkout. This shift diversifies Spain real time payments market size by broadening use cases into retail and services. Cross-border P2P via EuroPA links 50 million users in Spain, Italy, and Portugal, deepening network effects.

Strong consumer familiarity underpins resilient P2P volume; yet merchant uptake of A2A doubles Bizum online purchases to 30 million in 2024, valued at EUR 1.65 billion (USD 1.782 billion). As SMEs digitize at speed, P2B convenience and lower interchange begin eroding card dominance, reinforcing growth prospects across the Spain real time payments market.

By Component: Services Growth Outpaces Platform Investments

Platforms still represent 67.25% of 2025 spending, but services forecast a 19.98% CAGR through 2031 as banks prioritize fraud analytics and compliance assistance. Outsourced monitoring helps mid-tier banks achieve ISO-20022 readiness and manage 24/7 settlement obligations. Resultant operational expenditure elevates services share within Spain real time payments market size forecasts.

European Banking Authority deadline extensions for harmonized reporting now spur consultancy demand to retrofit systems. AI-driven fraud solutions, exemplified by CaixaBank’s Cosmos rollout, differentiate providers as fraud threats intensify. The component mix signals a shift from initial platform build-out toward value-added service layers.

By Deployment Mode: Cloud Migration Accelerates Modernization

Cloud holds 54.70% revenue and grows 18.96% CAGR, reflecting cost and scalability benefits for instant rails. Mid-tier institutions leverage cloud to bypass CapEx for core upgrades required by SEPA rules, driving Spain real time payments market share gains for cloud vendors. On-premise maintains 45.30% share among major banks prioritizing in-house security controls.

Fintech entrants such as Silbo Money use cloud-native design to scale across WhatsApp’s 35 million Spanish users swiftly. Telefonica’s extensive 5G coverage ensures connectivity resilience, reinforcing cloud adoption for latency-sensitive payment workloads.

By Enterprise Size: SME Digitalization Drives Fastest Growth

Large corporates currently generate 59.65% of market value thanks to complex treasury needs. Nevertheless, SMEs are forecast to grow 19.74% CAGR as fee caps, freemium pricing, and cloud platforms lower entry barriers. Mandatory e-invoicing for firms exceeding EUR 8 million turnover accelerates digital uptake, anchoring demand for ISO-20022-ready solutions within the Spain real time payments market.

SME adoption challenges—skills shortages and integration costs—are easing via SaaS packages and fintech partnerships. CaixaBank’s zero-fee instant transfers likewise help level cost structures for small firms.

By End-User Industry: Government Sector Leads Digital Transformation

Retail and e-commerce posted 35.62% share in 2025; yet government and public sector is set for a 20.95% CAGR through 2031. The April 2025 launch of the MiDNI digital ID app integrates payments into citizen services. Public-procurement e-invoicing volume exceeds 12 million annually, fostering instant settlement demand.

Energy and telecom utilities deploy RTP to streamline billing, as shown by Iberdrola España enabling card payments at 3,200 charging stations (40% of its network). BFSI remains a core adopter owing to regulatory imperatives, whereas healthcare is poised to follow as digital health payments mature.

Geography Analysis

Spain real time payments market leadership stems from 53% instant-transfer penetration, enabled by Bizum’s user base and nationwide 5G coverage. Redsys processes USD 545.4 billion equivalent annually across 1.5 million POS devices, illustrating ready merchant infrastructure. Telefonica’s 90% 5G footprint across 1,500 municipalities underpins ubiquitous mobile RTP usage.

European integration deepens reach: the EuroPA link connects 186 institutions and 50 million users in Spain, Italy, and Portugal, enabling phone-number-based instant transfers and positioning Spain as a regional hub. Banco Santander’s One-Leg-Out scheme further extends instant capability to non-EU destinations. Harmonized SEPA fee caps remove cost friction across borders, enhancing Spain real time payments market competitiveness.

Spain’s banks also carry significant Latin American footprints, offering optionality for future corridor expansion. With 93% of consumers comfortable sending RTP domestically and 90% receiving, Spain serves as a reference model for markets transitioning from card-centric systems.

Competitive Landscape

Collaboration defines domestic dominance: Bizum aggregates 29 million users across >30 banks, processing 1 billion transfers yearly and securing nearly 90% share of instant P2P traffic. International card schemes and fintechs contest merchant space, but regulatory fee parity erodes structural advantages.

Disruptors leverage alternative channels. Silbo Money integrates payments into WhatsApp, courting 35 million Spanish users with zero-fee messaging-based transfers. Revolut’s rollout of 50 ATM-kiosks aims to capitalize on Spain’s 60% cash POS share and upsell digital accounts. Domestic processor Iberpay and clearing house Iberpay monitor scheme interoperability and support EuroPA expansion, fortifying the Spain real time payments market.

Strategic investments highlight competitive positioning. CaixaBank’s USD 5.4 billion Cosmos program focuses on AI fraud controls and API enablement to sustain differentiation under commoditized fee structures. Banco Santander targets A2A merchant solutions to defend acquiring revenue as interchange pressure rises. Fragmentation remains moderate: top five entities—Bizum, Iberpay, Redsys, CaixaBank, and Santander—control close to 60% of transactional volume.

Spain Real Time Payments Industry Leaders

ACI Worldwide Inc.

FIS Global

Paypal Holdings Inc.

Fiserv Inc.

Matercard Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Banco Santander enabled international Bizum transfers to Italy and Portugal, deepening EuroPA interoperability; the move supports its A2A merchant expansion strategy while locking in cross-border volumes.

- June 2025: Revolut introduced 50 large-format ATMs in Madrid and Barcelona, using physical presence to acquire cash-reliant users and funnel them to app-based RTP services.

- June 2025: Silbo Money opened its WhatsApp-based payment platform to the public, aiming for 30,000 users by year-end as a low-cost alternative to Bizum.

- April 2025: Spanish government launched MiDNI digital ID, enabling in-app account opening and age verification; payments providers integrate ID rails to streamline KYC.

Spain Real Time Payments Market Report Scope

Real time payments or instant payments refer to payment rails (platforms or networks via which payments are made) that share a few characteristics, such as they are real-time and initiate, clear, and settle in a matter of seconds. Real-time payment payments are ideally available 24x7x365, meaning they are always online and available for transfer.

The Spain Real Time Payments Market is segmented by Payment Type (P2P, P2B).

By Transaction Type

| Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) |

By Component

| Platform / Solution |

| Services |

By Deployment Mode

| Cloud |

| On-Premise |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises |

By End-User Industry

| Retail and E-Commerce |

| BFSI |

| Utilities and Telecom |

| Healthcare |

| Government and Public Sector |

| Other End-user Industries |

| By Transaction Type | Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) | |

| By Component | Platform / Solution |

| Services | |

| By Deployment Mode | Cloud |

| On-Premise | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Utilities and Telecom | |

| Healthcare | |

| Government and Public Sector | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the Spain real time payments market?

It is valued at USD 3.44 billion in 2026 and is projected to reach USD 7.95 billion by 2031.

Why did instant transfers surge in Spain ahead of other EU nations?

Early compliance with SEPA Instant rules, fee parity mandates, and collaborative schemes such as Bizum drove 53% instant-transfer penetration compared with the 15% EU average.

Which segment grows fastest within the Spain real time payments market?

Peer-to-business transactions are forecast to expand at a 18.87% CAGR through 2031 as merchants adopt account-to-account checkout solutions.

How are Spanish banks addressing rising fraud in real-time payments?

Institutions invest in hybrid machine-learning and graph-based analytics; CaixaBank’s Cosmos plan dedicates significant funds to AI-driven fraud prevention.

What role does cloud deployment play?

Cloud holds 54.70% revenue share and supports 18.96% CAGR, allowing mid-tier banks to modernize quickly and comply with 10-second settlement rules without heavy CapEx.

Page last updated on: