Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

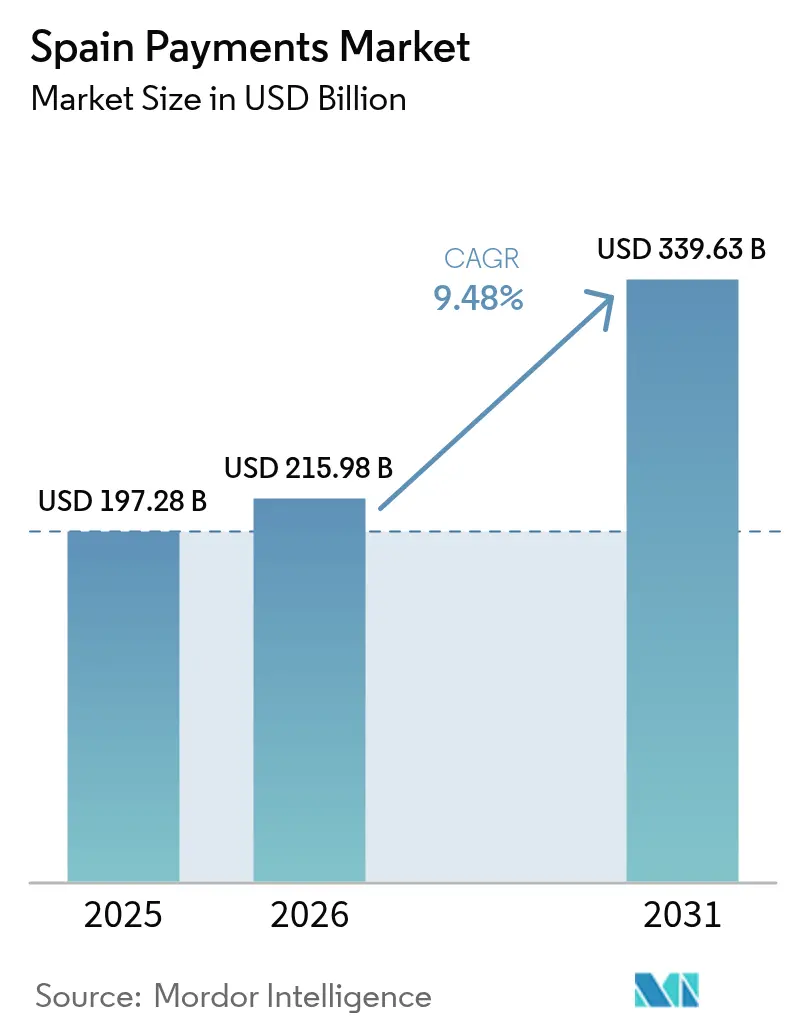

| Base Year Market Size (2025) | USD 197.28 Billion |

| Market Size (2026) | USD 215.98 Billion |

| Market Size (2031) | USD 339.63 Billion |

| Growth Rate (2026 - 2031) | 9.48% CAGR |

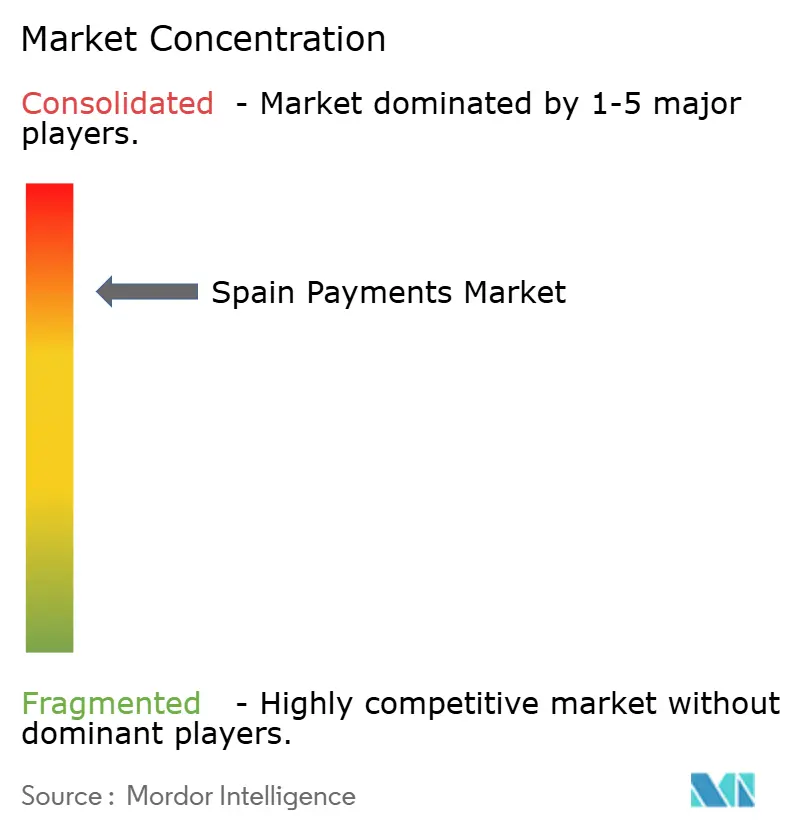

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Payments Market Analysis by Mordor Intelligence

Spain payments market size in 2026 is estimated at USD 215.98 billion, growing from 2025 value of USD 197.28 billion with 2031 projections showing USD 339.63 billion, growing at 9.48% CAGR over 2026-2031. Growth stems from a convergence of regulatory pressure, retail digitalization, and consumer appetite for real-time, contactless experiences that relegate cash to the margins. Mandatory strong customer authentication under PSD2 has pushed banks to expose data securely, fuelling an open-banking ecosystem where fintech firms orchestrate friction-free checkouts and account-to-account (A2A) transfers. The widespread rollout of SEPA Instant, now offered free of charge under EU Regulation 2024/886, removes the final cost hurdle for 10-second settlements that rival card rails.[1]Regulation (EU) 2024/886, EUR-Lex, eur-lex.europa.eu Merchant adoption of contactless point-of-sale (POS) terminals surpassed 95% at CaixaBank locations alone in 2024, underscoring infrastructure readiness.[2]CaixaBank to invest €5 bn in tech over next 3 years, FSTech, fstech.co.uk Meanwhile, mobile-first commerce is pulling even late-adopting demographics into the digital fold, translating demographic shifts into steady transaction volume growth.

Key Report Takeaways

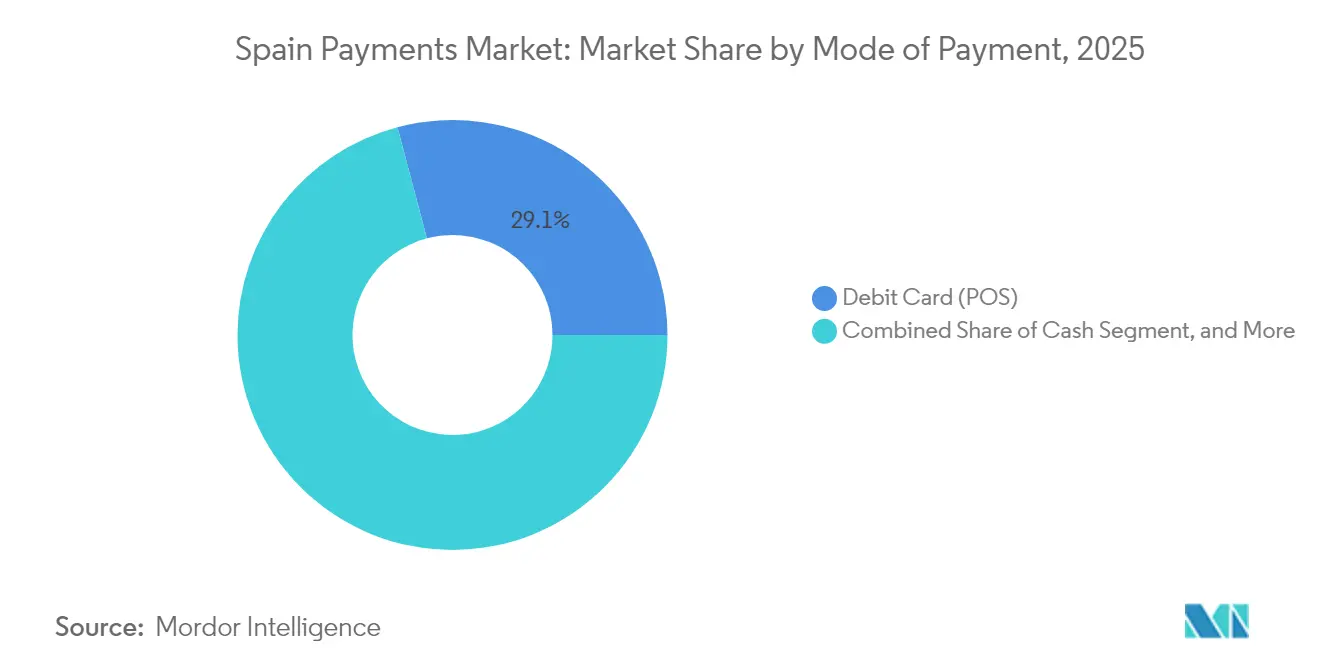

- By mode of payment, debit cards led with 29.12% of Spain payments market share in 2025; account-to-account transfers are forecast to expand at a 9.98% CAGR through 2031.

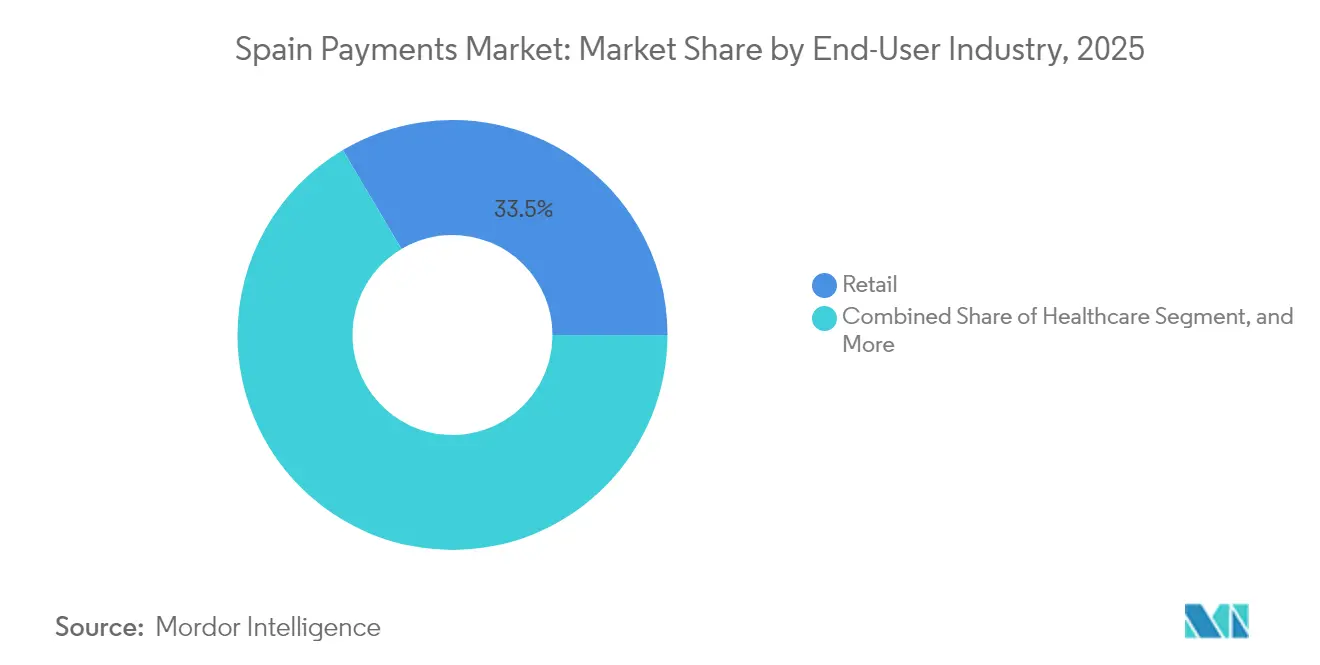

- By end-user industry, retail held 33.52% of Spain payments market size in 2025, while healthcare is advancing at a 10.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce and m-commerce boom | +2.1% | National, with concentration in Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Government digitization and PSD2 push | +1.8% | National, EU regulatory compliance | Short term (≤ 2 years) |

| Contactless POS infrastructure expansion | +1.5% | National, accelerated in urban centers | Medium term (2-4 years) |

| SEPA Instant rails adoption | +1.2% | National, EU interoperability focus | Short term (≤ 2 years) |

| BNPL-led surge in ticket size | +0.9% | National, youth demographics concentrated | Medium term (2-4 years) |

| Biometric-ID payment authentication | +0.6% | National, premium banking segments first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce and m-commerce boom

Online retail has morphed into the prime catalyst for the Spain payments market as smartphone transactions rose significantly. Merchants weave in one-click checkouts and digital wallets to keep abandonment rates low, while AI-driven recommendations subtly nudge shoppers to higher-value baskets. Social-commerce integrations let influencers embed buy buttons in live streams, broadening the revenue funnel for payment service providers. The blending of augmented-reality product trials with embedded finance makes the act of paying invisible yet indispensable. As the metaverse concept matures, virtual storefronts could extend Spain’s commerce footprint beyond physical borders, with payments handled seamlessly behind the scenes.

Government digitization and PSD2 push

The Plan de Digitalización de las AAPP 2021-2025 allocates EUR 6.5 billion (USD 7.34 billion) to modernize public-sector payments, while the Kit Digital subsidy earmarks EUR 3.067 billion (USD 3.47 billion) for SME tech adoption. These funds incentivize municipalities and small merchants to integrate real-time collections, reducing cash leakage and manual reconciliation. PSD2’s data-sharing mandate has also unlocked a wave of account-information and payment-initiation services; nearly every Tier-1 bank now offers open APIs as a baseline capability. Fintech aggregators exploit this access to craft budgeting apps, tax-filing tools, and subscription-management dashboards, all of which route payments through low-cost A2A rails. In parallel, Spain’s digital ID initiative promises biometric verification that could shrink fraud exposure for both citizens and corporates.

Contactless POS infrastructure expansion

CaixaBank’s deployment of more than 310,000 touchscreen POS devices, 95% of its estate, illustrates how thoroughly tap-to-pay has infiltrated Spanish retail. Transit operators followed suit: Madrid Region buses and Granada’s metro now accept EMV contactless cards, eliminating the friction of separate travel cards. Falling terminal prices and the ubiquity of NFC-enabled smartphones have removed cost barriers for mom-and-pop stores. Accessibility features such as voice assistance broaden inclusivity, enabling visually impaired consumers to transact independently. QR-code acceptance, popular among micro-merchants, complements the card infrastructure by offering a hardware-light alternative for event vendors and food stalls.

SEPA Instant rails adoption

As of January 2025, Spanish banks may no longer charge for instant euro transfers, aligning with Regulation 2024/886. Former fees of EUR 0.50–3.00 kept uptake modest; now, free 10-second settlements threaten to divert routine payments from card schemes. Businesses relish 24/7 liquidity, especially marketplaces that disburse funds to gig workers and artisans. Payment-service providers are scrambling to fortify their core systems to handle peak-time loads, sparking vendor consolidation among firms lacking scale. With cross-border reach to 36 SEPA countries, the rail positions Spain as a springboard for pan-European instant-payment products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Card-present and CNP fraud uptick | -1.4% | National, concentrated in tourist areas and e-commerce | Short term (≤ 2 years) |

| High SME merchant service fees | -0.8% | National, rural and small business concentration | Medium term (2-4 years) |

| Fragmented cross-border euro settlement | -0.6% | National, EU cross-border commerce focus | Medium term (2-4 years) |

| Digital exclusion of elderly and rural users | -0.4% | Regional, concentrated in rural Castilla-León, Extremadura, Galicia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Card-present and CNP fraud uptick

Card-not-present fraud accounted for 73% of total card losses in Europe during 2024, with Spain’s tourist hotspots proving especially vulnerable.[3]2024 Payment Threats and Fraud Trends Report, European Payments Council, europeanpaymentscouncil.eu E-skimming kits embedded in checkout scripts siphon customer data, while phishing lures target users of mobile P2P apps such as Bizum. Banks increasingly adopt machine-learning engines that monitor velocity, geolocation, and device fingerprints, but fraudsters are quick to test new attack vectors. The added layer of PSD2 multifactor authentication has curbed simple credential-stuffing attempts, yet social-engineering tactics remain stubbornly effective. Security spending competes with innovation budgets, slowing feature rollouts among smaller providers.

High SME merchant service fees

Although interchange caps lowered variable costs, acquirers often offset the shortfall with higher flat-rate fees, leaving many SMEs unconvinced of digital payments’ value proposition. Seasonal businesses along Spain’s coasts balk at monthly terminal rentals and opaque surcharges, defaulting to cash to preserve thin margins. Fintech acquirers tout blended rates below 0.3% but require volume commitments beyond what micro-enterprises can deliver. Regulators push transparency, yet the intricate layering of scheme, acquirer, and processor fees perpetuates confusion. Until simplified, fixed-fee structures proliferate, cash may retain a foothold in Spain’s long-tail merchant base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Debit Cards Lead, A2A Payments Surge

Debit cards commanded 29.12% of Spain payments market share in 2025, a legacy advantage built on decades of POS acceptance in grocery, fuel, and public-sector bill payments. The segment still accrues steady volume because consumers trust familiar chip-and-PIN and are rewarded through bank-linked loyalty programs. Meanwhile, the account-to-account category is on a tear, projected to register a 9.98% CAGR to 2031. The Spain payments market size for A2A transactions is poised to top USD 126.38 billion by 2031 if current growth holds, underpinned by Bizum’s network of 19.1 million users who logged 500 million transfers in 2024. Free instant transfers, newly mandated, further tilt everyday spending toward A2A, eroding low-ticket debit volumes. Digital wallets that ride on underlying card tokens, Apple Pay, Google Pay, Samsung Pay, enjoy double-digit gains as banks preload credentials, although wallet growth still ladders up to the broader card ecosystem.

Online-only payment modes tell a complementary story. Cash-on-delivery shrinks as e-commerce trust climbs, while Buy Now Pay Later (BNPL) edges toward mainstream among millennials seeking fee-free installments. BNPL’s ticket-size uplift echoes in higher cart values, yet regulators watch closely as household credit cycles lengthen. Credit-card growth settles into mid-single-digit territory, restrained by consumer wariness of revolving debt and the appeal of fee-free A2A. Ultimately, channel lines are blurring: Bizum Pay’s NFC rollout means a wallet top-up is no longer required for in-store tapping, showcasing how platform convergence will define the next phase of Spain's payments market evolution.

By End-User Industry: Healthcare Drives Digital Payment Innovation

Retail preserved its lead with 33.52% of Spain payments market size in 2025, reflecting omnichannel integrations that let shoppers hop between web storefronts and physical aisles without payment friction. Self-checkout kiosks and scan-and-go apps now dot major grocery chains, reducing queue fatigue and boosting throughput. Loyalty engines marry SKU-level data with real-time offers, turning the act of paying into a value-exchange moment. Even open-air markets in Valencia experiment with QR-code collections tied to municipal vendor registries, further embedding digital payments into daily commerce.

Healthcare, however, is the emergent star, forecast to grow at 10.15% CAGR as telemedicine, e-prescriptions, and wearable-device subscriptions proliferate. The Spain payments market share of healthcare stood below 5% in 2025 but is projected to double by 2031 as insurers reimburse teleconsultations directly into providers’ accounts via SEPA Instant, shortening cash cycles. Hospitals integrate patient-journey portals that bundle appointment booking, co-pay settlement, and post-visit financing in a single interface, reducing administrative overhead. Stringent data-protection rules nudge vendors toward tokenized storage and biometric verification, aligning with broader eIDAS 2.0 objectives. For fintech firms with compliant gateways, the vertical offers fertile ground to specialize in HIPAA-adjacent, GDPR-secured payment flows.

Geography Analysis

Madrid and Barcelona account for well over half of Spain payments market activity thanks to dense merchant networks, vibrant fintech clusters, and high tourist turnover. Local governments streamline licensing for POS installations and run city-sponsored accelerator programs, enabling rapid prototyping of wallet features and QR acceptance pilots. Bizum and CaixaBank often debut beta functions in these metros before rolling them out nationwide, reinforcing the cities’ status as digital sandboxes.

Secondary hubs such as Valencia and Seville exhibit escalating adoption driven by logistics and tourism, respectively. Valencia’s freight corridors digitize B2B settlements to shave days off the order-to-cash cycle, while Seville’s transit operator Tussam now accepts contactless fare payments across its entire fleet. The Basque Country and Catalonia, traditionally entrepreneurial, show above-average take-rates for invoice-financing fintech products that settle via instant credit transfers. Meanwhile, rural Galicia and Extremadura lag due to patchy broadband and aging populations but are explicit targets of the Kit Digital subsidy program aimed at bridging the urban-rural divide.

Spain’s role within the Single Euro Payments Area positions it as a corridor for remittances flowing to Latin America, leveraging cultural ties and shared language. Spanish banks extend white-label wallet offerings to subsidiaries in Mexico and Peru, enabling cross-border A2A at competitive FX spreads. The geography-tailored mix of retail, B2B, and remittance flows means payment providers must be adept at local nuance yet compliant with EU-wide standards. As 5G coverage expands into the Pyrenees and Balearic Islands, latency-sensitive payment use cases, such as in-car tolling and real-time gaming micro-purchases, stand to gain traction, adding further volume to the Spain payments market.

Competitive Landscape

Spain’s payments arena is moderately consolidated: the top five processors collectively handled an estimated 72% of domestic transaction value in 2024. Bizum’s consortium model makes it a quasi-utility; 35 partner banks fund the service yet compete on user experience and loyalty overlays. Redsys anchors card processing, charging between 0.3% and 1.5% depending on merchant category, and invested in tokenization to retain relevance as wallets grow. Global entrants such as Adyen, Stripe, and Craftgate target export-oriented e-commerce merchants with unified European acquiring licenses, adding international heft to a field once dominated by domestic incumbents.

Legacy banks are far from complacent. BBVA’s Horizon platform collapsed multiple legacy cores into a single cloud-native architecture, slicing development cycles by up to six months.[4]Digital Transformation Strategy Update, BBVA, bbva.com Santander experiments with earned-wage access through its partnership with CloudPay, eyeing payroll-linked credit products as an upsell path. CaixaBank earmarked EUR 5 billion for tech through 2027, ring-fencing funds for generative-AI chatbots that pre-empt payment-related customer queries.

White-space opportunities abound in healthcare, cross-border SME settlement, and municipal service payments. Fintechs that can navigate sector-specific compliance stand to carve defensible niches. Yet looming on the horizon is the European Central Bank’s exploratory digital euro, which could reroute person-to-person flows onto public infrastructure, compressing interchange economics. Providers therefore balance near-term feature sprints with contingency strategies for a potential central-bank platform that could reshape the Spain payments market.

Spain Payments Industry Leaders

Google Pay

PayPal Holdings, Inc.

Stripe, Inc.

Visa Inc.

Mastercard Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bizum expanded to Italy, Portugal, and Andorra, enabling cross-border P2P payments for Spanish users.

- January 2025: Unicaja Banco partnered with Fiserv to modernize real-time processing and fraud defenses.

- December 2024: CloudPay joined forces with Banco Santander to roll out on-demand pay for Spanish employers.

- December 2024: GMV completed contactless EMV deployments across multiple Madrid Region bus routes.

Spain Payments Market Report Scope

In Spain, the payment market encompasses the financial landscape that enables transactions between consumers and businesses, utilizing a range of payment methods. This ecosystem spans digital payments, remittances, and conventional banking transactions. The report tracks the revenue generated from providing payment services in Spain.

Spain Payment Market is Segmented by Mode of Payment (Point of Sale(Card Payments (Debit Cards, Credit Cards, Bank Financing Prepaid Cards), Digital Wallet, Cash), Online Sale(Card Payments (Debit Cards, Credit Cards, Bank Financing Prepaid Cards), Digital Wallet), and by End-User Industries (Retail, Entertainment, Healthcare, Hospitality)

The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Mode of Payment

| Point of Sale | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash | |

| Other POS Modes | |

| Online Sale | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Modes |

By End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Transportation |

| Other Industries |

| By Mode of Payment | Point of Sale | Debit Card Payments |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other POS Modes | ||

| Online Sale | Debit Card Payments | |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Modes | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Transportation | ||

| Other Industries | ||

Key Questions Answered in the Report

What is the current value of Spain’s payments transactions?

Spain payments market size stands at USD 215.98 billion in 2026 and is expected to grow rapidly through 2031.

How fast are instant transfers growing?

Account-to-account instant payments are poised for a 9.98% CAGR through 2031, bolstered by fee-free SEPA Instant rails.

Which payment mode dominates in-store spending?

Debit cards hold the largest share at 29.12% of 2025 point-of-sale volume.

Which vertical is seeing the quickest digital-payment uptake?

Healthcare leads with a projected 10.15% CAGR to 2031 as telemedicine and e-prescription services scale.

What are the main risks to growth?

Rising card-not-present fraud and high SME acquiring fees collectively shave almost 2.2 percentage points off forecast CAGR.

Page last updated on: