Spain Digital Transformation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

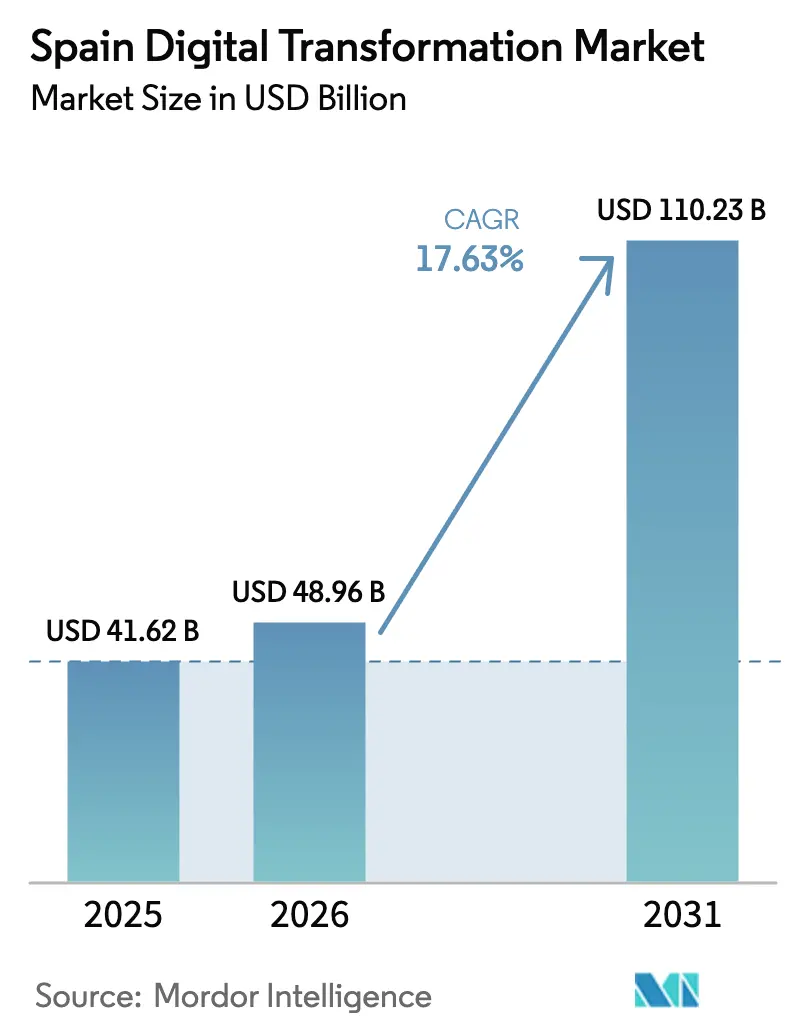

| Base Year Market Size (2025) | USD 41.62 Billion |

| Market Size (2026) | USD 48.96 Billion |

| Market Size (2031) | USD 110.23 Billion |

| Growth Rate (2026 - 2031) | 17.63% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Digital Transformation Market Analysis by Mordor Intelligence

The Spain digital transformation market size was valued at USD 41.62 billion in 2025 and estimated to grow from USD 48.96 billion in 2026 to reach USD 110.23 billion by 2031, at a CAGR of 17.63% during the forecast period (2026-2031). Strong public funding from the EU-financed Recovery & Resilience Facility, a nationwide fiber-to-the-home (FTTH) penetration above 90%, and the Digital Spain 2026 agenda position the country for sustained digital investment.[1]European Commission, "Spain’s Recovery and Resilience Plan", European Commission, commission.europa.eu Corporate demand for cloud migration, edge deployments, and AI-enabled analytics is reinforced by six-fold data-center capacity growth projected by 2026. Sector tailwinds also include mandatory e-invoicing rules that accelerate fintech adoption, while the first national Quantum Technologies Strategy underscores rising interest in advanced computing. Parallel headwinds come from a projected shortfall of senior cloud and AI specialists and tight SME budgets, yet managed-service providers are filling capability gaps.

Key Report Takeaways

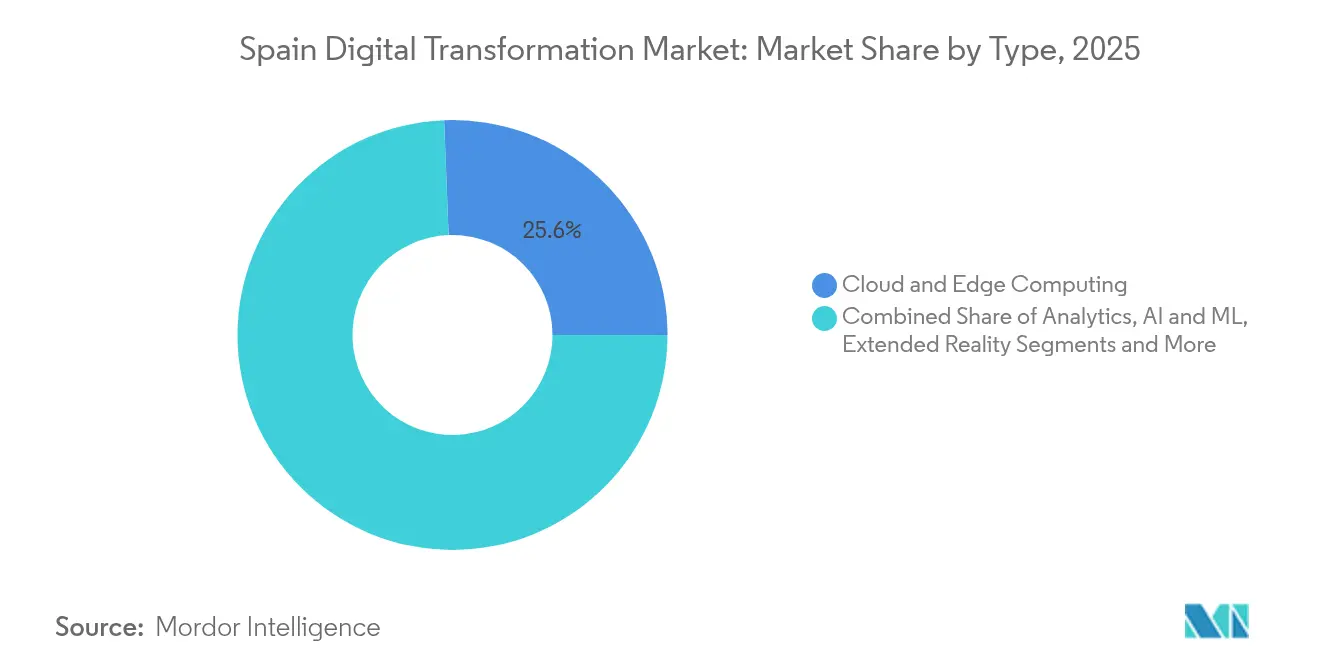

- By technology, Cloud & Edge Computing led with 25.62% of the Spain digital transformation market share in 2025, while AI/ML & Analytics is set to grow at a 19.12% CAGR to 2031.

- By service type, Consulting & Integration held 39.35% revenue share in 2025; Managed Services is projected to advance at 17.96% CAGR through 2031.

- By deployment mode, cloud models commanded 64.35% of the Spain digital transformation market size in 2025; hybrid deployment is rising at 19.03% CAGR between 2026-2031.

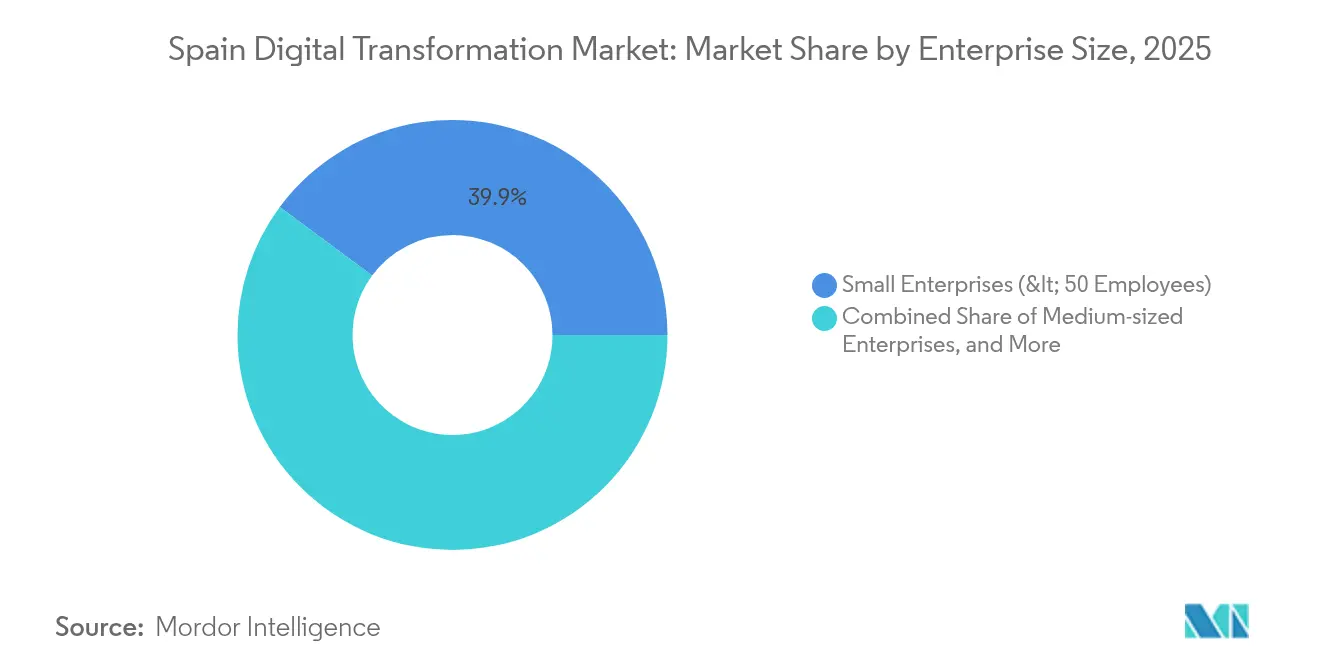

- By enterprise size, large enterprises accounted for 59.20% market share in 2025, yet SMEs are forecast to register a 19.80% CAGR through 2031.

- By end-user industry, BFSI led with 16.60% share of the Spain digital transformation market size in 2025; healthcare is expanding fastest at 19.12% CAGR to 2031.

- By region, the Community of Madrid contributed a 27.40% share in 2025, while Andalusia is the fastest-growing region at 18.07% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain participates in a competitive field that extends beyond its own borders. The market landscape in the global digital transformation (dx) industry outlined by Mordor Intelligence covers that wider structure.

Spain Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-funded Recovery & Resilience Facility Injecting EUR 70 Bn into Spanish Digitalization | +4.5% | National, with concentration in Madrid, Catalonia, and Andalusia | Medium term (2-4 years) |

| Digital Spain 2026 Agenda Targeting 100% 5G & Digital Public Services | +3.8% | National, with urban areas benefiting first | Long term (≥ 4 years) |

| Mandatory E-invoicing under Ley Crea y Crece 2022 | +3.5% | National, with stronger impact on SME-dense regions | Short term (≤ 2 years) |

| FTTH Penetration (>90%) Accelerating Cloud Migration | +2.1% | National, with higher impact in Madrid and Barcelona | Medium term (2-4 years) |

| Smart Tourism Adoption (Smart Destinations Program) | +1.8% | Coastal regions, Balearic and Canary Islands, major tourist destinations | Medium term (2-4 years) |

| Industry 4.0 PERTE Funds for Industrial Clusters | +1.5% | Basque Country, Catalonia, Valencia, industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-funded Recovery & Resilience Facility: Catalyzing cross-sector innovation

Targeted EU grants of EUR 70 billion (USD 79.1 billion) earmark 26% for digital initiatives, directing large tranches to public-sector digitalization, skills programs, and SME modernization. The scheme has already attracted a EUR 4.1 billion private battery-plant investment that leverages digital manufacturing platforms, illustrating how public incentives crowd in corporate capital.[2]Stellantis, "Stellantis and CATL to Invest Up to EUR 4.1 Billion in Joint Venture for Large-Scale LFP Battery Plant in Spain", stellantis.com Completion timelines align with 2026 milestones and underpin predictable demand for enterprise cloud, cybersecurity, and edge solutions.

Digital Spain 2026 agenda: Framework for digital leadership

Ten policy priorities aim for universal 100 Mbps coverage and a tripling of SME online sales participation by 2025. Spain already ranks third in EU connectivity and seventh in digital public services, confirming early gains.[3]Invest in Spain, "ICT. Information and communication technologies in Spain", investinspain.org Parallel workforce-upskilling targets covering 80% of citizens ensure demand-side readiness, while structured collaboration with telecom operators accelerates 5G roll-outs that underpin industrial IoT and smart-city projects.

Mandatory e-invoicing: Transforming business processes

Ley Crea y Crece obliges digital invoicing for 3.4 million firms, triggering accelerated investment in cloud accounting, payments automation, and data-driven finance platforms. Financial support through the Digital Kit grants of up to EUR 29,000 per SME further lowers adoption friction. The rule also heightens cybersecurity focus because expanded digital transaction flows amplify data-protection risk.

FTTH penetration: Enabling advanced services nationwide

Spain’s fiber network reaches more than 90% of households, enabling low-latency workloads in AI, telemedicine, and immersive media. Robust connectivity also underpins a forecast six-fold jump in domestic data-center capacity to more than 600 MW by 2026, establishing Spain as a Southern European digital gateway. [4]Silicon, "Data Center Boom Turns Spain into a Digital Hub for Southern Europe", Silicon, silicon.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Senior Cloud / AI Talent | -2.8% | National, with acute impact in Madrid and Barcelona | Medium term (2-4 years) |

| Fragmented Micro-SME Base with Limited IT Budgets | -1.9% | National, with higher impact in rural regions | Long term (≥ 4 years) |

| Rising Compliance Burden under EU AI Act & GDPR Fines | -1.2% | National, with higher impact on data-intensive sectors | Medium term (2-4 years) |

| Public-sector Legacy Mainframes Re-platforming Costs | -0.8% | National, concentrated in administrative centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Talent shortage: Bottleneck in execution

An estimated deficit of 30,000 experienced ICT specialists in 2025 inflates payroll costs by 15-20% year-on-year, prompting firms to outsource operations to managed-service providers and to recruit in secondary cities. Government grants of EUR 160 million for AI scholarships will ease junior-talent pipelines, yet senior expertise remains scarce in the medium term.

Fragmented micro-SME base: Structural adoption hurdle

Micro-enterprises represent 99% of Spanish companies but often lack the scale to justify complex platforms. Although EUR 4.7 billion in NextGenerationEU funding has been assigned to SME digitalization, limited digital awareness and restricted access to finance slow roll-outs, especially outside metropolitan areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cloud & Edge Computing dominates while AI accelerates

Cloud & Edge Computing retained a 25.62% share of the Spain digital transformation market in 2025, supported by outstanding fiber coverage and major hyperscaler investments, including Microsoft’s inaugural Spanish cloud region opened in 2024. The public-cloud segment is forecast to reach EUR 9.67 billion (USD 10.92 billion) in 2026. This contribution translates into the largest Spain digital transformation market size sub-category, and it is set to grow as edge nodes reduce latency for industrial automation and smart-city deployments.

AI/ML & Analytics shows the fastest momentum, with a 19.12% CAGR centered on the EUR 1.5 billion national AI Strategy that scales supercomputing capacity through MareNostrum 5 enhancements. Adoption is further propelled by a EUR 150 million incentive program for corporate AI deployments that could create 30,000 technology positions. Enterprises view advanced analytics as a productivity lever capable of boosting output by up to 20 % in manufacturing, logistics, and healthcare.

By Service Type: Integration services lead while managed services grow fastest

Consulting & Integration services represented 39.35% of Spain digital transformation market share in 2025, reflecting demand for complex multi-cloud migrations and ERP modernization. Large consultancies strengthened capabilities through targeted deals such as Capgemini’s acquisition of Syniti, which expands data-migration expertise.

Managed Services is projected to expand at an 17.96% CAGR as organizations offset talent shortages. Telefónica Tech increased cybersecurity and cloud-operations revenue by 7% in 2024, illustrating a rising appetite for outsourced operational stewardship.

By Deployment Mode: Hybrid models gain traction while cloud dominates

Cloud deployment captured 64.35% of Spain digital transformation market spending in 2025, thanks to cost elasticity, consumption-based pricing, and support for remote work practices accelerated by pandemic conditions. Extensive 5G and FTTH infrastructure also eases adoption in secondary cities.

Hybrid deployment is advancing at 19.03% CAGR because banks and healthcare providers need on-premise control for sensitive records while still exploiting cloud elasticity. Vodafone Spain and Kyndryl’s alliance to supply hybrid multicloud solutions illustrates how service providers bundle advisory, infrastructure, and managed operations under a single framework.

By Enterprise Size: SMEs closing the gap with large enterprises

Large enterprises contributed 59.20% of 2025 revenue in the Spain digital transformation market. Energy major Iberdrola earmarked EUR 41 billion (USD 41 billion) for 2024-2026 grid digitalization and green-hydrogen projects that combine IoT, AI, and advanced analytics.

SMEs are on a steeper 19.80% CAGR, driven by the Digital Kit program, which had distributed more than EUR 1.9 billion to over 460,000 firms by September 2024. Cloud subscriptions, low-code platforms, and cybersecurity as a service mitigate internal skill gaps and enable incremental investment without major capital outlays. The Spain digital transformation market size for the SME segment is therefore set to narrow the historic adoption gap.

By End-user Industry: Healthcare growth outpaces BFSI leadership

BFSI retained 16.60% of the Spain digital transformation market size in 2025 as large banks accelerated open-banking platforms and AI-driven compliance. BBVA added digital mortgage journeys and predictive insights for relationship managers, illustrating continuous maturity in customer experience.

Healthcare is projected to expand at a 19.12% CAGR. The government’s EUR 100 million National Health Data Space supports secure data pooling for diagnostics, while the World Health Organization named Universitat Oberta de Catalunya a collaborating center on digital health, enhancing Spain’s ecosystem credibility. Tele-consultation, remote monitoring, and AI-aided imaging drive investment, especially in regions with aging populations.

Geography Analysis

Madrid contributed 27.40% of the Spain digital transformation market in 2025, fuelled by corporate headquarters density, concentrated public-sector demand, and 61% of national data-center capacity. Microsoft’s local cloud region and sizeable telecom innovation clusters give the capital a leading installed-base advantage that attracts service providers and venture capital.

Catalonia ranks second, leveraging Barcelona’s smart-city credentials and vibrant startup environment. High-profile events like the IoT Solutions World Congress bring global firms to pilot edge and AI prototypes within the region’s urban-digital-twin program. Fiscal pressures and infrastructure underinvestment present structural challenges, yet the regional government’s AI Commission aims to sustain competitiveness in mobility, life sciences, and creative industries.

Andalusia is the fastest-growing region at an 18.07% CAGR. Research on 376 Andalusian SMEs confirms that digital transformation boosts organizational learning (β = 0.445) and innovation (β = 0.460), supporting early-stage investment cases. CGI’s acquisition of Novatec will add more than 300 IT specialists in Granada, strengthening local delivery capability for automotive and finance clients. Rural broadband subsidies through the UNICO-Banda Ancha program improve last-mile connectivity, enabling agri-tech and tourism-tech pilots that capitalize on the region’s sector mix.

Mordor Intelligence provides coverage of the digital transformation (dx) market across other key regional markets, including Europe, Asia, and North America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United Kingdom, Netherlands, China, Canada, Germany, and Japan incorporating local coverage and market participation, as required.

Competitive Landscape

The Spain digital transformation market features a blend of global hyperscalers, international consultancies, and specialized Spanish providers. Market concentration is moderate: top five suppliers collectively hold near-60% revenue share in cloud infrastructure and integration, while vertical-specific niches remain fragmented. Strategic alliances are commonplace as firms seek complementary assets. Vodafone Spain partners with Kyndryl for hybrid multicloud propositions, leveraging Vodafone’s network reach and Kyndryl’s managed-infrastructure expertise.

Technology differentiation is evident. Indra’s Minsait division recorded a 7% sales increase in 2024 by combining cybersecurity, ERP modernization, and AI solutions for the public sector and financial institutions. Telefónica Tech focuses on endpoint security and cloud operations outsourcing, supplementing traditional connectivity services to lock in enterprise clients.

White-space opportunities concentrate on digital-twin solutions, AI-enabled process automation for SMEs, and quantum-computing applications for logistics routing and pharmaceutical discovery. Government funding of EUR 808 million for quantum initiatives provides a five-year runway for domestic startups to collaborate with universities and multinationals. Competitive intensity is expected to rise as foreign vendors capitalize on improved data-sovereignty rules and robust connectivity.

Spain Digital Transformation Industry Leaders

-

Accenture PLC

-

Google LLC (Alphabet Inc.)

-

IBM Corporation

-

Microsoft Corporation

-

Cognex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Iberdrola España confirmed an economic impact above EUR 11 billion in the Basque Country and EUR 5 billion in Madrid, supported by smart-grid and green-hydrogen digital programs.

- April 2025: The Government of Spain unveiled the Quantum Technologies Strategy 2025-2030 with a EUR 808 million budget that introduces a Quantum Communications Hub.

- April 2025: A mobile-based digital National Identity Card (MiDNI) launched under the Digital Identity Plan to streamline citizen e-services.

- March 2025: The Minister for Digital Transformation announced higher cybersecurity allocations and a semiconductor research center in Malaga during the ASLAN Congress.

Spain Digital Transformation Market Report Scope

Digital transformation involves integrating technologies like analytics, artificial intelligence, machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, among others, across various end-user industry verticals.

Spain's digital transformation market is segmented by type (analytics, artificial intelligence, and machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, and other types (digital twin, mobility, and connectivity)) end-user industry (manufacturing, oil, gas, and utilities, retail & e-commerce, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, and other end-user industries (education, media & entertainment, environment, etc.)). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Analytics, Artificial Intelligence and Machine Learning |

| Extended Reality (XR) |

| Internet of Things (IoT) |

| Industrial Robotics |

| Blockchain |

| Additive Manufacturing / 3D Printing |

| Cyber-security |

| Cloud and Edge Computing |

| Digital Twin |

| Mobility and Connectivity |

| Consulting and Integration |

| Managed Services |

| Support, Training and Maintenance |

| Software Platforms |

| Hardware and Devices |

| Cloud |

| On-premise |

| Hybrid |

| Small Enterprises (< 50 Employees) |

| Medium-sized Enterprises (50-249 Employees) |

| Large Enterprises (≥ 250 Employees) |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Education, Media and Environment |

| By Type | Analytics, Artificial Intelligence and Machine Learning |

| Extended Reality (XR) | |

| Internet of Things (IoT) | |

| Industrial Robotics | |

| Blockchain | |

| Additive Manufacturing / 3D Printing | |

| Cyber-security | |

| Cloud and Edge Computing | |

| Digital Twin | |

| Mobility and Connectivity | |

| By Service Type | Consulting and Integration |

| Managed Services | |

| Support, Training and Maintenance | |

| Software Platforms | |

| Hardware and Devices | |

| By Deployment Mode | Cloud |

| On-premise | |

| Hybrid | |

| By Enterprise Size | Small Enterprises (< 50 Employees) |

| Medium-sized Enterprises (50-249 Employees) | |

| Large Enterprises (≥ 250 Employees) | |

| By End-user Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Education, Media and Environment |

Key Questions Answered in the Report

What is the current value of the Spain digital transformation market?

The market stands at USD 48.96 billion in 2026 and is projected to reach USD 110.23 billion by 2031 at an 17.63% CAGR.

Which technology segment holds the largest Spain digital transformation market share?

Cloud & Edge Computing led with a 25.62% share in 2025, supported by hyperscaler data-center expansion.

Why are managed services growing faster than traditional integration projects?

Firms use managed services to offset a shortage of senior cloud and AI talent and to secure predictable operating costs, leading to an 17.96% forecast CAGR through 2031.

Which Spanish region is expanding digital transformation spending most quickly?

Andalusia shows the highest CAGR at 18.07% thanks to targeted broadband subsidies and new delivery centers.

How is government policy shaping AI adoption in Spain?

The EUR 1.5 billion national AI Strategy funds supercomputing upgrades and offers EUR 150 million in incentives, driving a 19.12% CAGR for AI/ML & Analytics solutions.

What are the primary constraints facing Spain’s digital transformation initiatives?

A projected deficit of 30,000 senior ICT specialists and limited IT budgets among micro-SMEs temper the pace of adoption, especially outside major cities.

Page last updated on: