Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Spain Data Center Physical Security Market is Segmented by Component (Solution, Services), Data Center Tier (Tier I and II, Tier III, Tier IV), Data Center Type (Hyperscaler/Cloud Service Providers, Colocation Providers, Enterprise and Edge Data Center). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

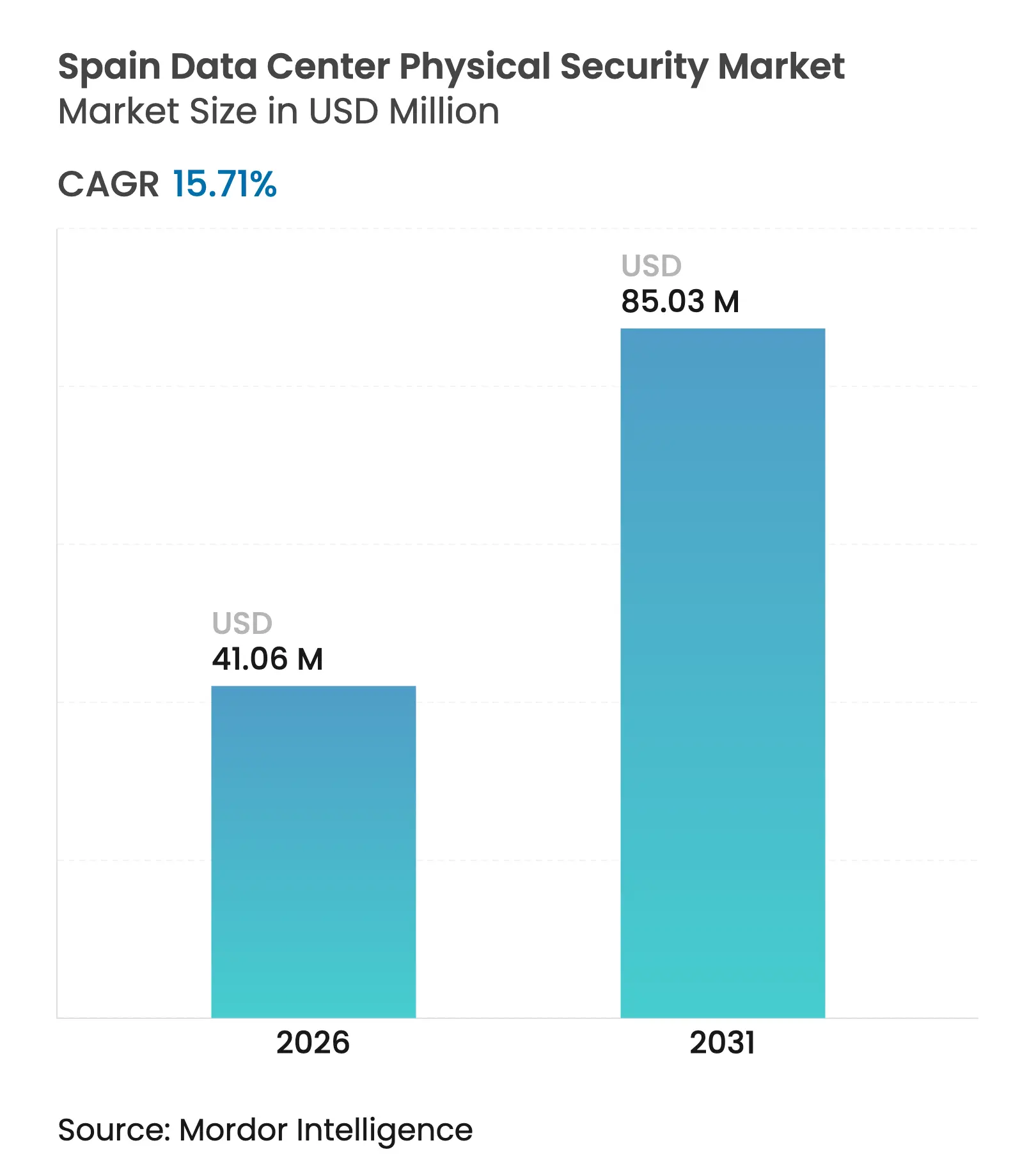

| Market Size (2026) | USD 41.06 Million |

| Market Size (2031) | USD 85.03 Million |

| Growth Rate (2026 - 2031) | 15.71 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Spain data center physical security market size in 2026 is estimated at USD 41.06 million, growing from 2025 value of USD 35.47 million with 2031 projections showing USD 85.03 million, growing at 15.71% CAGR over 2026-2031. This expansion is fueled by hyperscale capital expenditure, stringent national regulations and the country’s role as a connectivity bridge between northern Europe, Latin America and North Africa. Madrid alone is set to host more than two-thirds of national capacity, compelling operators to deploy multi-layered protection that aligns with NIS2, GDPR and Esquema Nacional de Seguridad (ENS) requirements. Investment momentum from Microsoft, Damac Group and Iron Mountain is creating reference sites that showcase AI-enabled video analytics, privacy-first biometrics and replicated data-hall compartmentalization standards. At the same time, rising material costs and a limited pool of security-cleared technicians are putting margin pressure on integrators, encouraging vendors to deliver pre-engineered solutions that shorten installation windows and reduce site-based labor.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising cloud-service capacity build-outs

Rising cloud-service capacity build-outs

| +3.2% | Madrid-Barcelona corridor, national | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+3.2%

|

Geographic Relevance

:

Madrid-Barcelona corridor, national

|

Impact Timeline

:

Medium term (2-4 years)

|

Escalating compliance needs (GDPR, NIS2, ENS)

Escalating compliance needs (GDPR, NIS2, ENS)

| +2.8% | National | Short term (≤ 2 years) | |||

Heightened threat of physical breaches

Heightened threat of physical breaches

| +2.1% | Global, high-value facilities | Short term (≤ 2 years) | |||

Rapid hyperscale and colocation expansion Rapid hyperscale and colocation expansion | +3.7% | Madrid-Barcelona corridor | Medium term (2-4 years) | |||

Convergence of physical and OT-cyber security Convergence of physical and OT-cyber security | +1.9% | National | Long term (≥ 4 years) | |||

Edge micro-data-center rollout

Edge micro-data-center rollout

| +1.4% | Urban centers, industrial zones | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Cloud-Service Capacity Build-Outs

Installed IT load is projected to grow significantly, a four-fold jump that is reshaping how operators approach perimeter, rack-level, and human-centric protection. Microsoft’s first Spanish cloud region and Google’s parallel expansions are establishing new benchmarks that colocation operators must emulate to keep enterprise clients. These sites illustrate the shift from perimeter-only guarding to AI video analytics that flag anomalous maintenance behavior in real time. Iron Mountain’s MAD-1 campus, which serves 230,000 global customers, demonstrates how multi-tenant facilities can justify biometric portals, hardened delivery docks and 24/7 SOC oversight without eroding profitability. Economies of scale are further making advanced infrared cameras and thermal analytics affordable for mid-tier providers.[1]Brad Smith, “Microsoft Expands Spanish Cloud Region,” microsoft.com

Escalating Compliance Needs for GDPR, NIS2 and ENS Regulations

Royal Decree 311/2022 aligned ENS with Europe-wide NIS2 obligations, compelling operators to implement 72 technical measures that now bind physical access, video retention and incident logging. Public-sector and BFSI workloads cannot be processed in facilities lacking ENS-High accreditation, an incentive that has already propelled Zscaler and other cloud platforms to redesign their badge systems for continuous audit output. Penalties reaching 2% of global turnover are nudging smaller colocation players to accelerate budget allocations for mantrap retrofits and dual-factor biometrics. The legal nexus also extends to supply-chain verification, forcing EPC contractors to clear enhanced background checks before entering secure zones.[2]Centro Criptológico Nacional, “ENS Guidelines 2024,” ccn-cert.cni.es

Heightened Threat of Physical Breaches and Insider Sabotage

Industry studies attribute up to 80% of data-center losses to insider activity, prompting Spanish operators to embed behavior analytics into access logs that measure door-open dwell time, equipment removal, and key-card anomalies. The arrival of AI accelerators valued at more than USD 25,000 each is creating a lucrative hardware theft target that necessitates chip-level tamper sensors and privacy-first facial authentication. Alcatraz AI’s Rock X deployment in Madrid demonstrates how GDPR-compliant biometrics can block tailgating without storing raw facial imagery.[3]Ben Wallace, “Rock X Biometric Tailgating Prevention,” alcatraz.ai

Rapid Hyperscale and Colocation Expansion in the Madrid–Barcelona Corridor

Capital spending is growing is turning the corridor into Europe’s fastest-growing edge of the FLAP-D cluster. MERLIN Properties’ Barcelona Zona-Franca campus illustrates the pace: its 15 MW hall achieved full lease-up less than six months after commissioning, compelling front-end investment in integrated fence, LIDAR and thermal detection arrays certified to ISO 27001 and PCI-DSS. Vendors are responding with modular guardhouses, fiber-linked radar units and AI-based perimeter analytics that can be mounted during construction phases, protecting sites even before façade closure

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High upfront CapEx for Tier III/IV security

High upfront CapEx for Tier III/IV security

| -1.8% | National, high-tier facilities | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-1.8%

|

Geographic Relevance

:

National, high-tier facilities

|

Impact Timeline

:

Short term (≤ 2 years)

|

Interoperability challenges with legacy gear

Interoperability challenges with legacy gear

| -1.2% | Retrofit markets | Medium term (2-4 years) | |||

Shortage of security-cleared technicians

Shortage of security-cleared technicians

| -0.9% | Madrid-Barcelona corridor | Medium term (2-4 years) | |||

Urban zoning curbs on perimeter hardening

Urban zoning curbs on perimeter hardening

| -0.7% | Madrid, Barcelona urban cores | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Upfront CapEx for Tier III/IV-Grade Security Infrastructure

Steel and aluminum tariffs that rose to 25% in 2024 lifted prices of fences, bollards and mantrap frames by 15-20%. For a 30 MW greenfield campus, physical protection can amount to 10% of total build cost, a figure that strains the capex budgets of local colocation firms. Operators are therefore phasing deployments, installing biometric cabinets only in the most critical data halls at go-live and expanding coverage as rack occupancy climbs. EPC firms such as ACS are mitigating exposure by prefabricating security rooms off-site, minimizing on-site labor and shortening commissioning windows.

Interoperability Challenges with Legacy CCTV and Access-Control Gear

Many enterprise facilities still rely on proprietary DVRs and MIFARE badge readers introduced between 2015 and 2020. These systems lack the open APIs that ENS now requires for automated incident exports, forcing operators to choose between wholesale rip-and-replace or hybrid overlays that dilute analytics accuracy. AI video engines need 4K feeds to identify tailgating or object removal, yet older cameras max out at 720 p. The resulting technical debt lengthens project timelines and erodes ROI until phased migration plans reach full coverage, a window that can stretch up to 36 months for multi-hall sites.

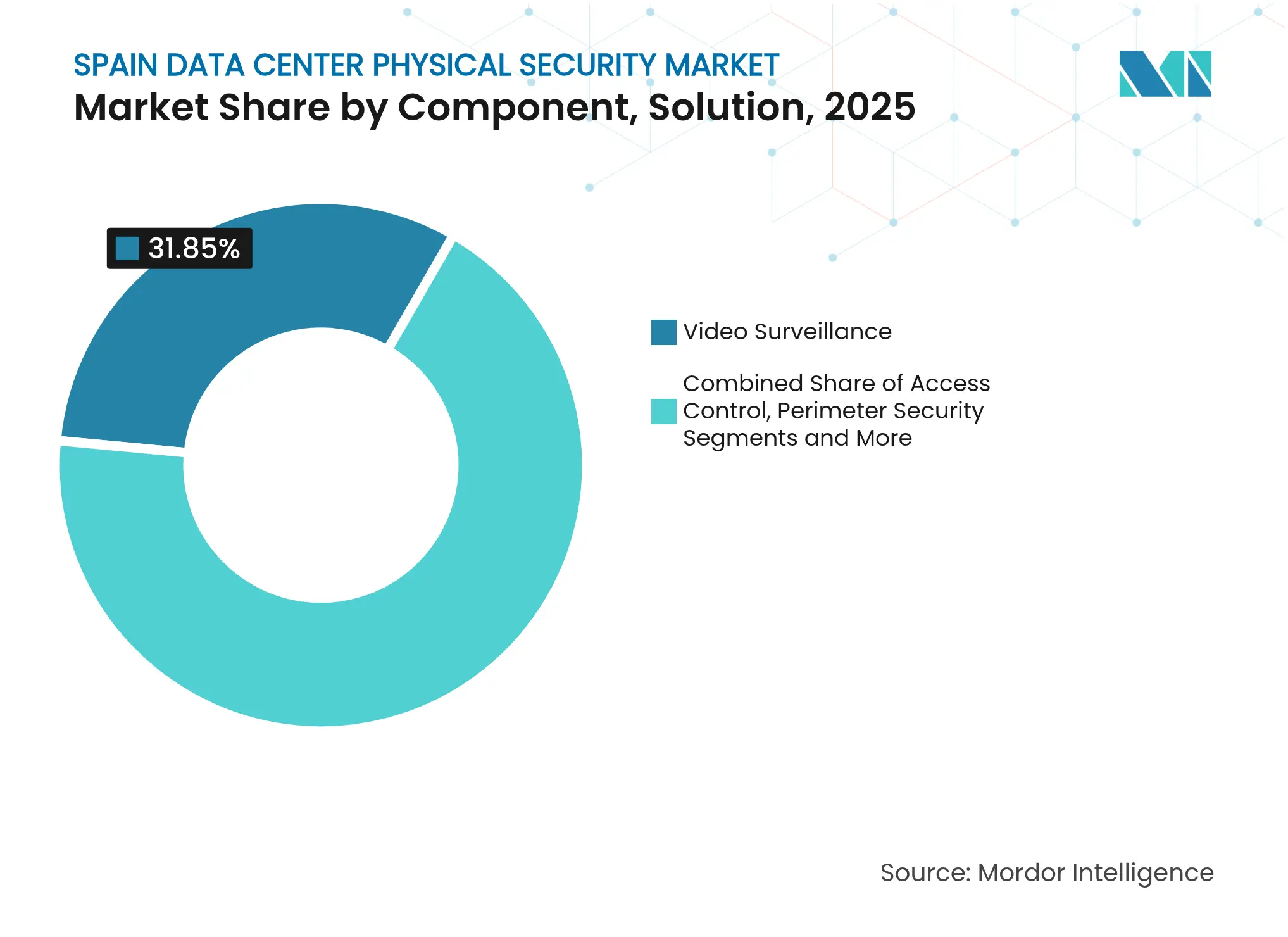

By Solution Type: Video Surveillance Dominates While Access Control Accelerates

Video surveillance accounted for 31.85% of the Spain data center physical security market in 2025, reflecting its critical role in perimeter, aisle, and rack oversight. Growth continues as hyperscale projects specify 100% camera coverage, 30-day retention, and real-time AI analytics for motion, object removal, and thermal anomalies. Access control is expanding at 15.98% CAGR as facilities upgrade from swipe cards to multimodal biometrics that integrate vein, facia,l and mobile credentials. Perimeter security components are integrating radar, LIDAR, and drone-detection sensors, enabling automated lockdown when intrusions are validated. Intrusion detection and environmental monitoring lines are converging; humidity spikes in battery rooms now auto-trigger camera presets and access restrictions. Honeywell’s Digital Video Manager exemplifies cross-domain integration that simplifies ENS reporting and shortens incident investigation cycles.

Operators view video footage as legal evidence to defend SLA penalties or insurance claims, elevating archival storage to compliance-critical status. Access control vendors are embedding privacy-by-design features such as on-device template matching to avoid storing biometric data in central repositories. Thermal-imaging fences can detect human presence at 300 m, reducing guard patrol frequency.

Note: Segment shares of all individual segments available upon report purchase

By Data-Center Tier: Tier III Retains Lead, Tier IV Gains Speed

Tier III sites captured 62.55% Spain data center physical security market share in 2025 because they balance 99.982% availability with capex restraint. Operators deploy dual power feeds, redundant badge controllers and N+1 CCTV recorders to maintain surveillance during maintenance. Tier IV builds, often exceeding 35 MW IT load, require 2N distribution, diverse mantrap paths and dual perimeter rings, pushing security capex up to USD 600 per m². The Spain data center physical security market size for Tier IV is forecast to rise fastest at 17.55% CAGR to 2031 as sovereign cloud mandates push critical workloads into fault-tolerant halls.

Tier I and II footprints continue to shrink as legacy enterprise facilities migrate to colocation or cloud, freeing budgets for camera and badge upgrades rather than full-scale rebuilds. Data-hall compartmentalization in Tier III+ expansions now mirrors Tier IV best practice, introducing zoned smoke partitions and biometric vestibules. ENS audits increasingly check that physical controls map to cybersecurity playbooks, making integrated SOCs a competitive necessity. Hyperscalers are piloting sensory lighting that changes color when zones move from normal to alert state, providing immediate visual cues for roving guards

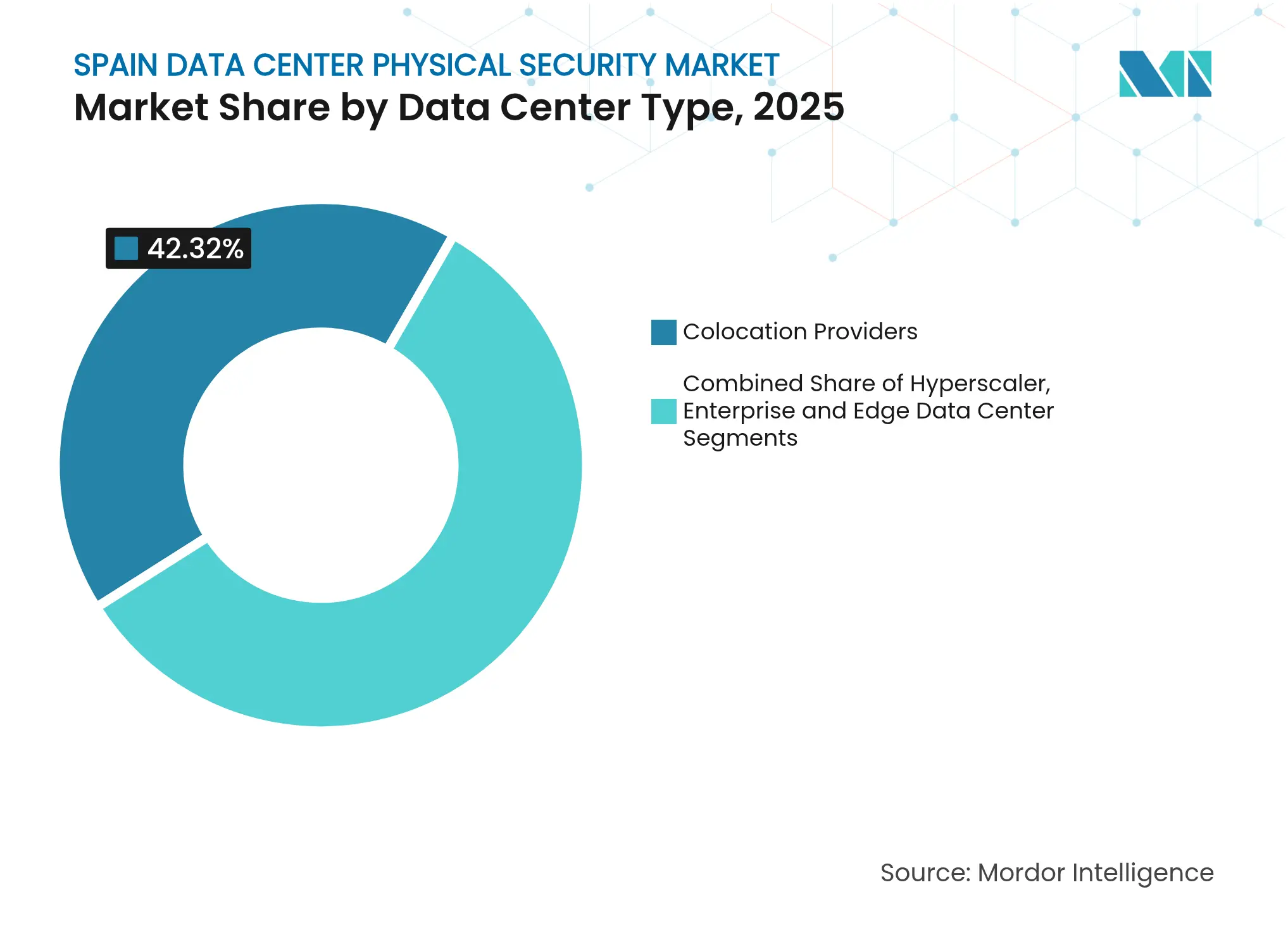

By Data-Center Type: Colocation Holds Volume, Hyperscalers Drive Growth

Colocation providers controlled 42.32% of revenue in 2025 by spreading security investment across multiple tenants, each subscribing to tiered protection bundles. Shared SOC services allow small enterprises to comply with ENS at lower cost. However, cloud platforms owned by Microsoft, Amazon and Google are scaling Spanish capacity at 17.05% CAGR, and each facility embeds proprietary biometric workflows and AI-based perimeter analytics. The Spain data center physical security market will therefore see hyperscalers exert growing influence on standards and procurement practices.

Edge and enterprise data centers are being retrofitted to support 5G-enabled low-latency applications in Seville, Málaga and Bilbao. Telefónica’s VDC-Edge program demands compact yet Tier III-equivalent security, prompting vendors to launch rack-integrated cameras and key-cabinet biometrics. The colocation segment is answering hyperscale pressure by offering “sovereign suites” with dedicated vestibules, continuous guard presence and logical-physical convergence dashboards.

Note: Segment shares of all individual segments available upon report purchase

Spain’s data-center physical security demand is highly concentrated in the Madrid-Barcelona corridor, which accounted for 66.85% of installed capacity in 2025. Madrid benefits from dense fiber, superior power redundancy and proximity to DE-CIX interconnection nodes, attracting hyperscale and fintech tenants that mandate Tier IV-equivalent security. Barcelona’s Mediterranean cable access fuels growth in AI model-training clusters, prompting investments in ISO 27001-compliant guard programs and integrated drone-detection systems.

Regional governments are incentivizing capacity diversification: Navarre’s plan to double data-center footprint introduces mid-scale sites that still require ENS-High controls, while Aragón’s low-carbon grids lure AI inference farms seeking renewable PPA guarantees. These developments expand the Spain data center physical security market beyond the core corridor, giving integrators opportunities to deploy pre-fabricated mantraps and modular SOC kits in smaller cities. Iberdrola’s renewable supply commitments ensure stable power for surveillance and access systems, aligning decarbonization goals with 24/7 security uptime expectations.

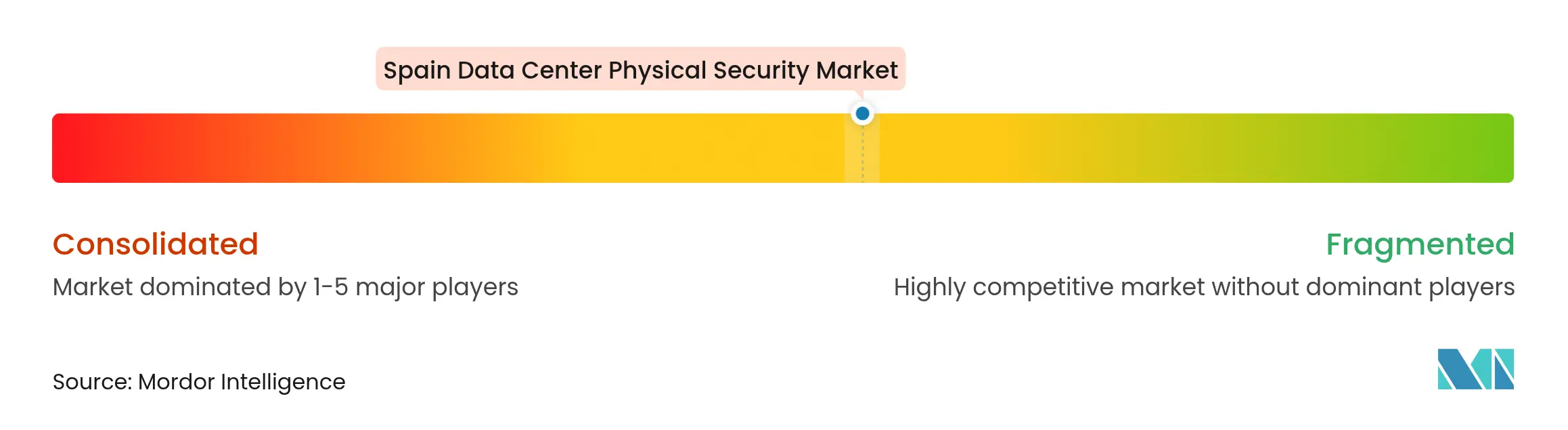

Market Concentration

The Spain data center physical security market remains moderately fragmented despite consolidation signals. Global incumbents—Johnson Controls, Honeywell and Axis Communications—leverage broad portfolios that bundle cooling, fire and badge systems into integrated proposals, capturing multi-hall greenfield projects. At the same time, specialized platforms such as Alcatraz AI, Gallagher and Genetec differentiate on AI-centric analytics, low-latency facial matching and open-API ecosystem support.

Regulatory expertise acts as a key differentiator: vendors with documented ENS and NIS2 compliance templates shorten approval cycles for public-sector contracts and win hyperscale bids that require unified cyber-physical dashboards. Local integrators Prosegur and Indra build advantage through Spanish-language SOC staffing and on-call engineering within four-hour SLAs across the corridor. Component shortages and tariff-driven cost spikes are pushing integrators toward vendor-agnostic designs that can swap cameras or badge readers without re-certification, preserving delivery timelines.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE and GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Spain Data Center Physical Security Baseline Earns Dependability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 35.47 million (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 23 million (2024) | Regional Consultancy A | Excludes integration services and newest Tier IV builds; older baseline | ||

USD 30.60 million (2022) | Industry Portal B | Uses static spend-per-rack metric; refresh cadence unclear |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.