Space-based C4ISR Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 4.61 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

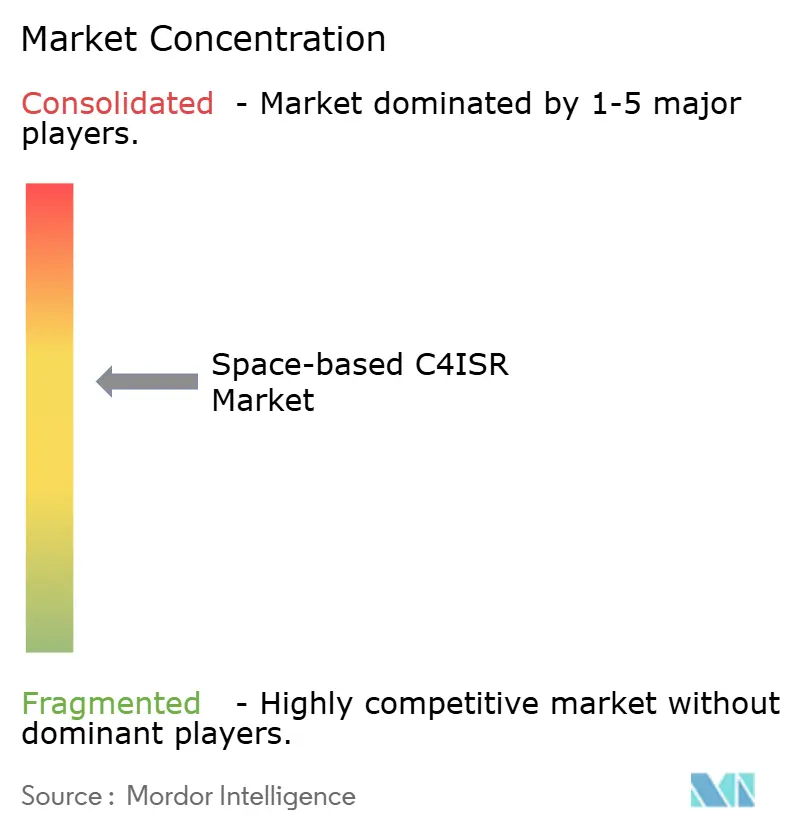

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Space-based C4ISR Market Analysis by Mordor Intelligence

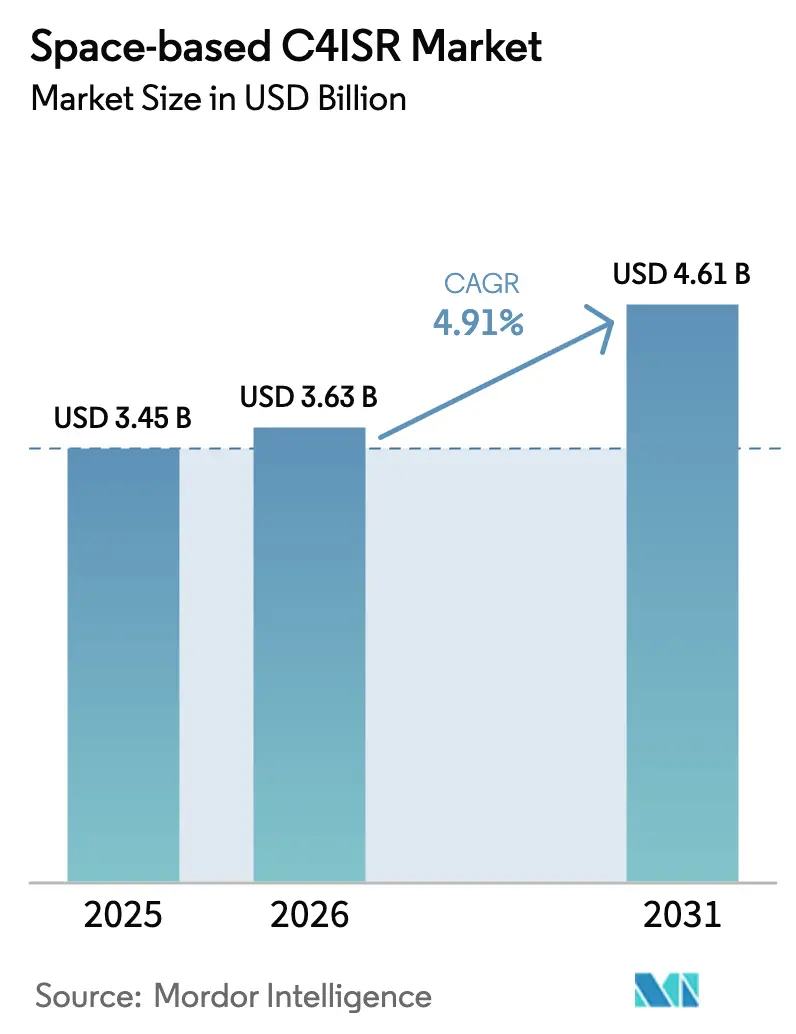

The space-based C4ISR market size is expected to grow from USD 3.45 billion in 2025 to USD 3.63 billion in 2026 and is forecasted to reach USD 4.61 billion by 2031 at a 4.91% CAGR over 2026-2031. Rising defense demand for resilient, low-latency constellations, the proliferation of commercial off-the-shelf (COTS) payloads, and the steady migration from monolithic geostationary buses to proliferated low-Earth orbit (LEO) architectures are reshaping competitive dynamics. Tactical users now expect sub-20 millisecond latency for real-time fire-control, driving interest in multi-orbit networks that fuse optical, infrared, and radar data for hypersonic threat tracking. Vertically integrated entrants such as SpaceX exploit high-volume production to undercut legacy suppliers, while primes pivot to software-defined payloads that can be re-tasked in orbit. Meanwhile, civil agencies are adopting commercial imagery for disaster response and border security, thereby expanding the non-defense revenue pool within the space-based C4ISR market.

Key Report Takeaways

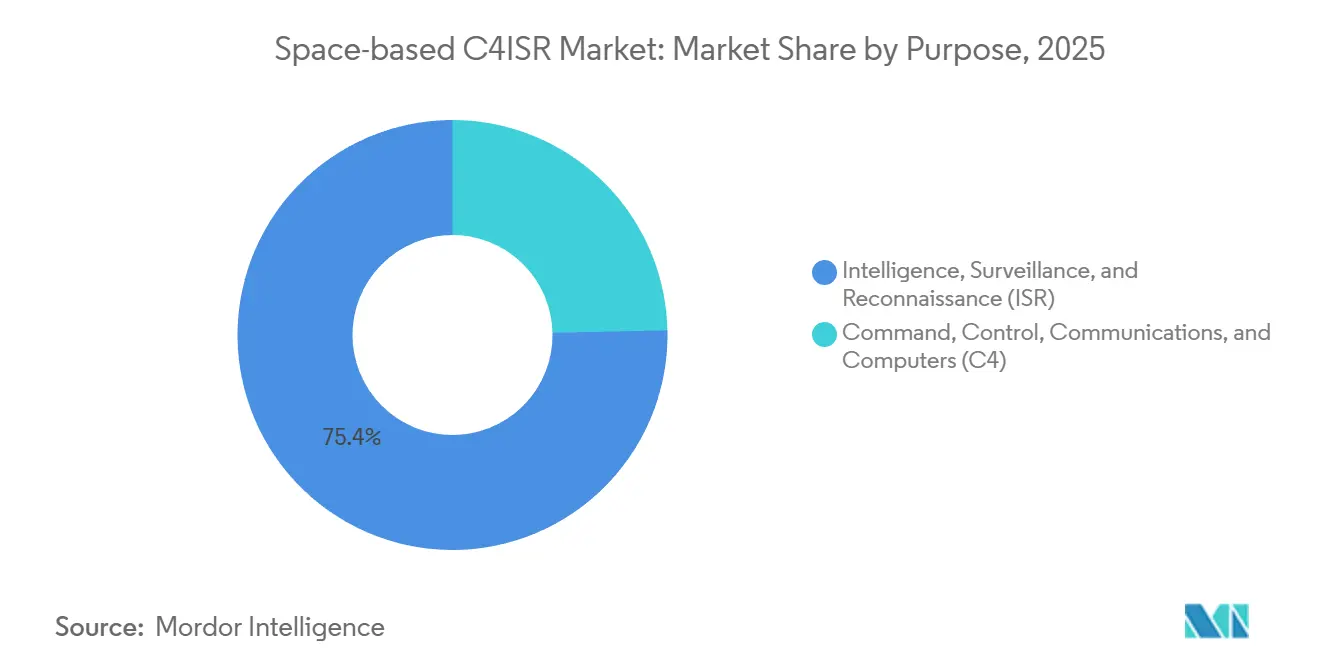

- By purpose, ISR applications accounted for 75.35% of the space-based C4ISR market revenue in 2025; the C4 segment is projected to expand at a 5.29% CAGR through 2031.

- By orbit, LEO accounted for 70.12% of the space-based C4ISR market size in 2025 and is projected to advance at a 5.63% CAGR through 2031.

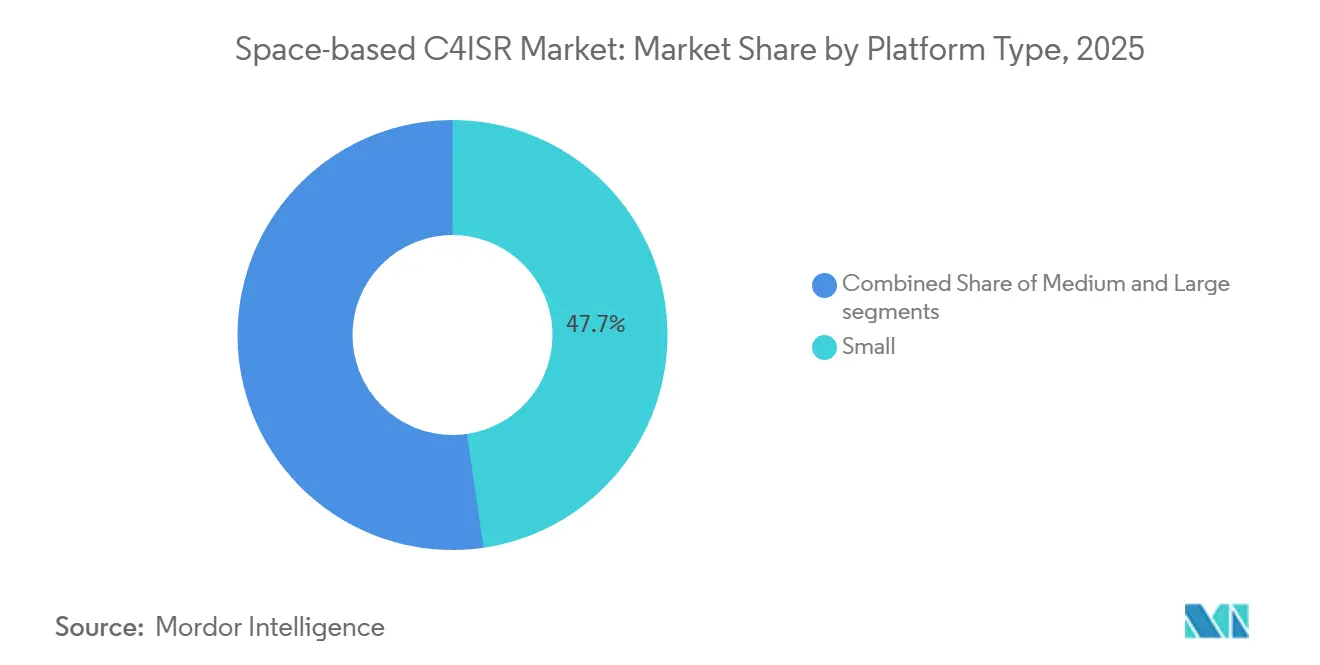

- By platform, satellites weighing less than 500 kg captured 47.69% of the space-based C4ISR market size in 2025 and are forecasted to grow at a 5.29% CAGR.

- By end user, defense forces accounted for 59.88% of revenue in 2025, while civil government and space agencies are growing at the fastest rate, with a 5.11% CAGR.

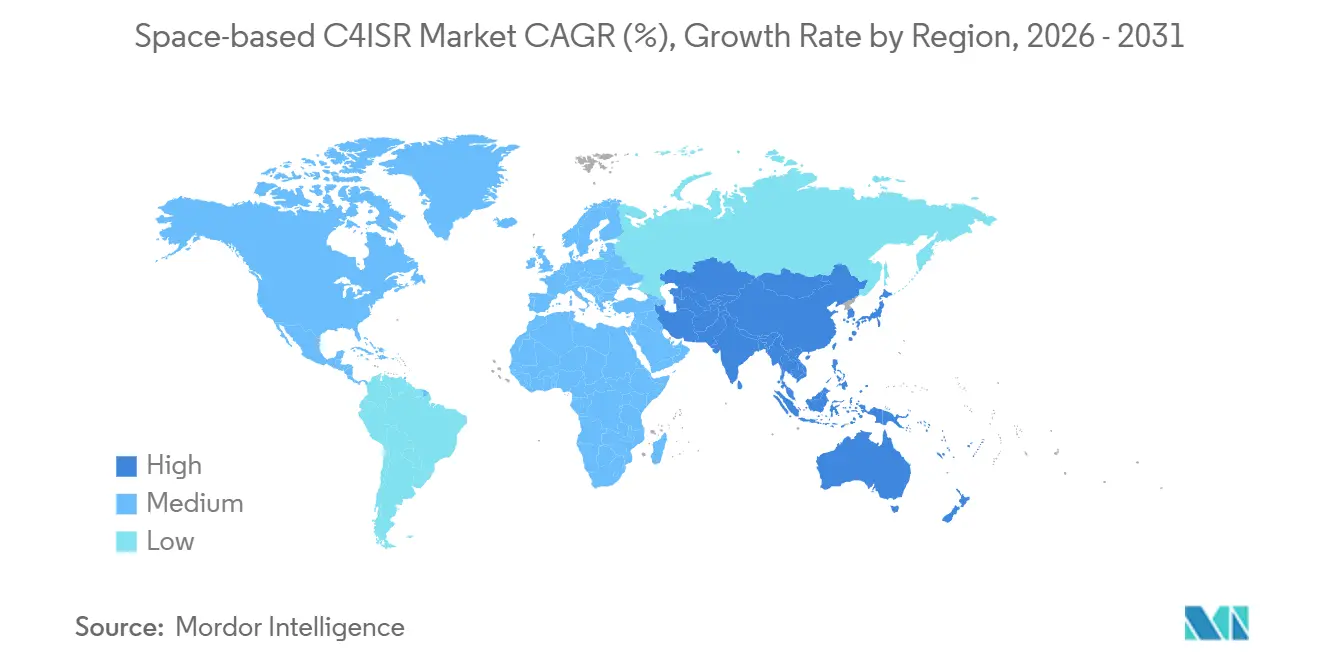

- By geography, North America led the space-based C4ISR market share with 46.72% in 2025; the Asia-Pacific region is projected to post the highest CAGR of 5.89% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Space-based C4ISR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for real-time situational awareness | +1.2% | Global, Indo-Pacific, Eastern Europe | Medium term (2-4 years) |

| Proliferation of low-cost small-sat constellations | +1.0% | North America, Asia-Pacific, Europe | Short term (≤ 2 years) |

| Higher defense spending dedicated to space domain awareness | +0.9% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Integration of C4ISR constellations with autonomous UAV swarms | +0.7% | North America, Asia-Pacific | Medium term (2-4 years) |

| COTS software-defined payloads enabling rapid re-tasking | +0.6% | Global | Short term (≤ 2 years) |

| Multi-orbit network architectures optimizing tactical latency | +0.5% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Situational Awareness

Commanders now require sub-minute decision cycles to counter maneuvering threats, prompting investment in transport-layer satellites able to push sensor data to shooters within 10 seconds.[1]Space Development Agency, “Transport Layer,” sda.mil L3Harris delivered 10 Tranche 1 platforms in 2024, featuring 10 Gbps optical crosslinks, which eliminate ground-station latency. Israel Aerospace Industries launched Ofek 19 in 2025, adding 0.5 m all-weather imaging that commanders in the Eastern Mediterranean integrate into theater command systems. Constellations of 100-plus satellites now guarantee sub-15-minute revisit times, satisfying the tempo required for hypersonic defense. Growth in the space-based C4ISR market is therefore anchored in latency-driven procurement that favors proliferated LEO designs.

Proliferation of Low-Cost Small-Sat Constellations

Rideshare missions priced near USD 1 million per 200 kg payload democratize access to orbit. Hanwha Systems is investing KRW 100 billion (USD 68.86 million) in additional small-satellite production, enabling South Korea to field radar payloads without relying on foreign primes. India’s DRDO plans 50 satellites by 2030, leveraging indigenous launchers for autonomy. These developments compress refresh cycles to three-year intervals, stimulating recurring demand and enlarging the addressable space-based C4ISR market.

Higher Defense Spending Dedicated to Space Domain Awareness

The US Space Force allocated USD 4.1 billion of its USD 29.4 billion FY-2025 budget to space domain awareness.[2]US Space Force, “FY 2025 Budget,” spaceforce.mil NATO opened its Space Centre of Excellence in Toulouse in 2024 to synchronize allied surveillance assets. Japan approved JPY 120 billion (USD 765.15 million) for relay satellites that link Aegis destroyers with US missile-warning networks. Middle-East nations, led by the UAE’s USD 500 million satellite plan, are following suit. Elevated budget allocations assure a multi-year funding stream for new platforms, stabilizing long-term demand across the space-based C4ISR market.

Integration of C4ISR Constellations with Autonomous UAV Swarms

Collaborative combat aircraft programs rely on resilient satellite links to push mission updates beyond line of sight. Kratos is developing the MACH-TB hypersonic testbed with in-flight satellite telemetry for real-time trajectory correction. BAE Systems and Hanwha collaborate on payloads that merge satellite imagery with UAV signals intelligence, enabling precision strike in contested airspace. Seamless hand-overs between satellites every few minutes require software-defined radios that auto-switch Ku-, Ka-, and optical links, embedding new capability layers within the space-based C4ISR market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Orbital congestion and space-debris collision risk | −0.8% | Global, LEO sun-synchronous | Long term (≥ 4 years) |

| High upfront capex and long development cycles | −0.6% | Emerging Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Spectrum clashes with emerging 5G/6G terrestrial services | −0.4% | North America, Europe, Asia-Pacific corridors | Short term (≤ 2 years) |

| Cyber-vulnerabilities in software-defined satellites | −0.3% | Global, contested domains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Orbital Congestion and Space-Debris Collision Risk

ESA tracks 33,290 debris objects larger than 10 cm, yielding a 1-in-1,000 annual collision probability for satellites in busy sun-synchronous bands.[3]European Space Agency, “Space Debris by the Numbers,” esa.int The February 2024 breakup of a Russian satellite forced 47 conjunction warnings within three days, raising insurance premiums by up to 20% for spacecraft lacking propulsion. Active debris removal remains experimental, with Astroscale’s ADRAS-J only proving rendezvous capability so far. Until regulators mandate end-of-life deorbiting, congestion will inflate costs and moderate growth in the space-based C4ISR market.

High Upfront Capex and Long Development Cycles

South Korea’s five-satellite 425 Project costs KRW 1.2 trillion (USD 826.34 million), crowding out other modernization priorities. India’s 50-satellite ISR goal competes with naval and air programs for budget share. Although COTS buses reduce build times to 24 months, classified payload integration and accreditation add another year, slowing the pace at which new capabilities enter the space-based C4ISR market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Purpose: ISR Dominance Funds C4 Acceleration

ISR applications produced 75.35% of 2025 revenue, underpinning the space-based C4ISR market size leadership as governments relied on electro-optical (EO), radar, and signals payloads for strategic warning. Maxar’s WorldView Legion achieved full operations in 2025, offering 30 cm imagery with daily revisit for the National Geospatial-Intelligence Agency.[4]Maxar Technologies, “WorldView Legion,” maxar.com Israel’s Ofek 19 added 0.5 m radar imaging in adverse weather, bolstering Eastern Mediterranean surveillance.

The C4 segment is projected to grow at a 5.29% CAGR through 2031, as tactical mesh networks link Patriot batteries, collaborative combat aircraft, and maneuver brigades in near real-time. L3Harris’s optical cross-links exemplify this shift, merging communications and ISR on a single bus and expanding functional overlap across the space-based C4ISR industry.

By Orbit Type: LEO Proliferation Redefines Resilience

LEO held 70.12% of 2025 revenue and is forecasted to rise at a 5.63% CAGR, reflecting the preference for sub-20 millisecond latency missions central to the space-based C4ISR market. L3Harris won USD 919 million for Tranche 2 and USD 843 million for Tranche 3, including missile-tracking satellites that integrate optical and IR sensors.

MEO supports wide-area coverage, as illustrated by the GPS III spacecraft, which also hosts nuclear-detonation detectors. Geostationary remains vital for persistent surveillance; Northrop Grumman’s polar OPIR satellites, in highly elliptical orbits, complement GEO vantage points over the Arctic.

By Platform Type: Small Satellites Unlock Rapid Refresh

Satellites under 500 kg generated 47.69% of 2025 revenue, anchoring the space-based C4ISR market size at the segment level and expanding at a 5.29% CAGR. Lockheed Martin’s SmartSat software stack on Maxar-built SDA platforms enables OTA algorithm updates, shrinking capability insertion timelines.

Medium-class satellites fill signals-intelligence roles, while large platforms remain essential for high-power GEO missions such as Boeing’s 6,000 kg WGS-12 communications craft due into service by 2028. The swing toward small satellites is reinforced by SpaceX’s ability to mass-produce sub-300 kg Starshield surveillance spacecraft for intelligence customers.

By End-User: Civil Agencies Converge with Defense

Defense users accounted for 59.88% of 2025 spending, with the US Space Force alone investing USD 4.1 billion in space domain awareness. NATO’s Space Centre of Excellence coordinates allied assets to improve resilience and interoperability.

Civil agencies, however, are expected to grow at a 5.11% CAGR as organizations like the UAE Space Agency fund multi-mission satellites for regional ISR and environmental monitoring. The EU's IRIS² constellation blends governmental communications with defense surge capacity, illustrating the blurred line between civil and military domains.

Geography Analysis

North America accounted for 46.72% of 2025 revenue thanks to the US Space Development Agency's (SDA's) prolific Tranche architecture and Canada's RADARSAT maritime surveillance fleet. L3Harris's USD 919 million Tranche 2 award and Northrop Grumman's USD 1.8 billion polar OPIR contract signal continued dominance. Vertically integrated suppliers control manufacturing, launch, and ground infrastructure, reinforcing regional leadership within the space-based C4ISR market.

The Asia-Pacific region is projected to grow at the fastest rate, with a 5.89% CAGR. China expanded its Yaogan constellation with 12 launches across 2024-2025 for coverage of the South China Sea. India plans to launch 50 defense satellites by 2030 using indigenous PSLV vehicles. South Korea's 425 Project and Hanwha's Jeju expansion highlight the country's growing domestic production capacity.[5]Hanwha Systems, “Jeju Space Center Expansion,” hanwhasystems.com Australia hosts Transport Layer ground stations, creating an Indo-Pacific relay backbone for allied forces.

Europe and the Middle East invest in sovereign capability to curb reliance on US assets. The EU committed EUR 10.60 billion (USD 12.36 billion) for IRIS², deploying 290 satellites across multiple orbits. NATO's Toulouse center sets doctrine for collective orbital defense. The UAE's USD 500 million ISR satellite plan positions Abu Dhabi as a regional hub for data. Saudi Arabia partners with Thales on radar satellites for infrastructure security. South America and Africa remain nascent, with Brazil exploring environmental partnerships and South Africa hosting foreign ground nodes, resulting in a modest near-term impact on global space-based C4ISR market growth.

Regulatory Landscape

Space-based C4ISR programs operate under a tightening set of national security and communications rules that increasingly extend to commercial suppliers. In the United States, CNSSI 1200 (August 2025) establishes mandatory cybersecurity policy and minimum criteria for space-based National Security Systems used in C4ISR missions. That raises the compliance bar for software-defined satellites, ground systems, and managed services that handle mission data.

Spectrum and space operations regulation is also shifting in ways that affect proliferated LEO architectures. In May 2026, the FCC adopted a performance-based approach for GSO/NGSO spectrum sharing, replacing legacy EPFD limits. In April 2026, it advanced a proposal to expand Space Operation Service allocations to support telemetry, tracking, and command for emergent spacecraft. Separately, Executive Order 14369 (December 18, 2025) directs development of national standards for PNT and for space traffic management and orbital debris mitigation, reinforcing debris-aware mission planning and end-of-life disposal across large constellations.

Value Chain Analysis

The space-based C4ISR value chain covers mission definition and funding (defense ministries, space agencies), satellite buses and payloads (EO/IR, SAR, SIGINT, and communications), launch and rideshare, ground segment and gateways, and data exploitation and dissemination into command-and-control networks. Proliferated LEO increases the importance of productized spacecraft platforms and industrialized integration, and it puts more weight on high-throughput optical crosslinks and encrypted terminals to keep sensor-to-shooter timelines short while reducing dependence on vulnerable ground nodes.

On the supply side, vertical integration and prime-commercial teaming are reshaping how value is captured from payload-to-data delivery. Partnerships such as Apex and Anduril (announced October 2024) point to standardized satellite buses paired with mission software for mission sets including missile tracking and space situational awareness. On the demand and distribution side, US Space Force contracting for government-owned, contractor-operated networks reinforces a services-and-backbone layer between constellations and tactical users. MILNET contracting began in June 2025 and evolved into the Space Data Network (SDN), supported by dedicated funding and major awards in 2026. This shift elevates network orchestration, terminals, and cross-domain integration as key value-chain nodes alongside spacecraft manufacturing.

Competitive Landscape

Five legacy primes, Lockheed Martin, Northrop Grumman, L3Harris, Boeing, and Maxar, controlled roughly 60% of 2025 defense revenue, indicating moderate concentration in the space-based C4ISR market. SpaceX disrupted pricing by leveraging Starlink lines to win a USD 1.8 billion reconnaissance award, compelling incumbents to accelerate their small-satellite programs. Maxar launched WorldView Legion and secured a USD 290 million NGA build contract, evidencing agile vertical integration.

Strategic differentiation centers on proliferated constellations, software-defined payloads, and multi-orbit resilience. L3Harris’s 10 Gbps optical links bypass vulnerable ground nodes, while Rocket Lab’s USD 515 million classified contract introduces a new hardware supplier for defense constellations. Hanwha’s KRW 100 billion (USD 68.86 million) investment aims for regional prime status in the Asia-Pacific.

Cybersecurity remains a weak flank: GAO flagged incomplete encryption in most US military programs. The absence of binding international regulation, beyond spectrum management, leaves risk mitigation to individual operators. Consequently, white-space opportunities emerge in debris removal, cyber-resilient architectures, and signals intelligence services for mid-tier nations, broadening the competitive canvas of the space-based C4ISR market.

Space-based C4ISR Industry Leaders

Northrop Grumman Corporation

Lockheed Martin Corporation

CACI International Inc.

L3Harris Technologies, Inc.

Elbit Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace is forming around resilient, low-latency military data transport and sensor tasking at scale, where governments increasingly purchase capability as an integrated network rather than as isolated satellites. The US Space Force consolidation of transport efforts into the Space Data Network (SDN) and the May 2026 awards to SpaceX (USD 2.29 billion for the SDN backbone and USD 4.16 billion for space-based air moving target indicator) provide demand signals for multi-orbit data movement, networking payloads, gateways, and user terminals that can support continuous targeting and time-sensitive operations.

Opportunities are also expanding in enabling layers that reduce constellation risk and accelerate refresh, including interoperable optical communications terminals, cyber-compliant ground software aligned to CNSSI 1200, and spectrum-efficient designs aligned with the FCC's May 2026 performance-based sharing framework. The market is creating room for suppliers that can integrate commercial imagery and communications with defense mission assurance, reflecting the DoD Commercial Space Integration Strategy (2024) emphasis on aligning commercial capabilities to national security architectures without relying on bespoke, one-off regulation for every provider.

Recent Industry Developments

- June 2026: Lockheed Martin received a USD 514 million contract modification from the US Space Force to produce two additional GPS IIIF satellites. The award reinforces resilient PNT capacity and sustains demand for secure payload integration and modernized space-to-ground interfaces that feed joint C4ISR networks.

- December 2025: L3Harris won a USD 843 million Space Development Agency Tranche 3 missile-tracking satellite contract. The program extends proliferated LEO sensing and reinforces the shift toward multi-satellite architectures that combine rapid revisit with data transport into tactical command-and-control.

- December 2024: The European Commission awarded the IRIS2 network contract to the SpaceRISE consortium (SES, Eutelsat, and Hispasat). The decision formalized a major European multi-orbit communications program with government and defense utility, widening the supplier base for secure connectivity, ground infrastructure, and managed services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues earned from space-enabled command, control, communications, computers, intelligence, surveillance, and reconnaissance capabilities, where satellites and their mission-ground links are necessary to deliver the intended operational outcome.

Scope exclusions: Purely terrestrial C4ISR systems, and stand-alone launch services that are not bundled into a space-based C4ISR program, are excluded.

Segmentation Overview

- By Purpose

- Command, Control, Communications, and Computers (C4)

- Intelligence, Surveillance, and Reconnaissance (ISR)

- By Orbit Type

- Low-Earth Orbit (LEO)

- Medium-Earth Orbit (MEO)

- Geostationary Orbit (GEO)

- By Platform Type

- Small (Less than 500 kg)

- Medium (500 kg to 1,500 kg)

- Large (Greater than 1,500 kg)

- By End-User

- Defense Forces

- Civil, Government, and Space Agencies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build a dependable fact base around budgets, mission plans, and procurement timing, before any sizing assumptions were finalized. We referred to public sources such as US government budget documents and contracting releases, NATO and national defense publications where available, UN registers on launched objects, ITU satellite filings, and OECD or World Bank macro series to normalize multi-year spending patterns.

To understand what is being funded and when it is likely to be delivered, we also reviewed company annual reports, investor presentations, and credible defense and space press coverage of program awards and payload roadmaps. For additional confirmation on company financial direction and program signals, we selectively used paid subscriptions covering company financials and intelligence, news and financials, patent databases, and global contracts and tenders. These desk sources are illustrative, and we also used other public references for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were completed with stakeholders across defense and civil space procurement, mission operations, payload and ground specialists, and integrators who support secure communications and ISR missions. Because the market is global, we tested inputs across major regions so procurement cycles, orbit preferences, and modernization pace could be captured, then we adjusted the dataset when multiple interviews described the same procurement pattern.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 41% |

| Mid tier: 56% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 14% | Managers: 48% | Americas: 25% |

Market-Sizing & Forecasting

The sizing model starts with a top-down build of the addressable demand pool. Public defense and civil space budgets, procurement schedules, and modernization plans are translated into annual spend tied to space-linked C4ISR capability delivery. Those totals are then corroborated through selective bottom-up approximations, such as sampled program values, typical payload and ground-system pricing ranges, and limited supplier roll-ups, which are used to validate and fine-tune the overall number.

Key inputs used include space and defense budget direction, satellite and payload procurement cadence, the split of missions by orbit (LEO versus GEO patterns), refresh cycles for ISR payloads, and the share of spend that sits in ground and mission operations versus space hardware. Where visibility is limited (for example, where awards are bundled or partially undisclosed), gaps are handled using conservative allocation rules that are rechecked during interviews and only scaled when independent signals support a change.

Forecasting is run using scenario analysis supported by trend smoothing on the main drivers. Contract awards and launch schedules can create uneven year-to-year steps, so assumptions for procurement pace, orbit mix, and price progression are aligned to what primary respondents see in the near-term pipeline, then stress-tested under slower and faster budget conditions.

Data Validation & Update Cycle

Outputs are triangulated against independent signals such as major contract announcements, publicly stated satellite procurement quantities, and budget totals, then variance checks are run across regions and end-use demand pools. When an outlier appears, we recheck the underlying drivers, verify currency timing, and re-contact sources if a program looks re-phased, re-scoped, or delayed.

Before sign-off, the model goes through multiple analyst reviews so unit logic, assumptions, and growth steps remain consistent across the full time series. Reports are refreshed annually, with interim updates for material events, and a final check is completed right before delivery so clients receive the latest view.

Mordor Intelligence's Space Based C4isr Market Size Versus Other Published Estimates

Published market values for space-based C4ISR often differ because different publishers define what is counted as space-based revenue, and they also time multi-year defense awards into annual market values in different ways. Differences in currency conversion timing, treatment of modernization versus new procurement, and how quickly assumptions are refreshed after major awards can also move the reported totals.

The benchmark table shows that the spread largely comes from what is counted as space-based C4ISR versus adjacent satellite services. In the Mordor Intelligence approach, the value is tied to development, procurement, and modernization of space-platform C4ISR systems, with stand-alone satellite operations and unrelated analytics kept out when they are not part of a C4ISR program.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.63 B (2026) | |

| Industry Publisher A | USD 3.30 B (2025) | Uses a different base year and can bundle a wider solution set, which may pull in adjacent satellite-related revenues and makes year-to-year comparison less like-for-like. |

| Global Publisher B | USD 3.40 B (2026) | Applies a broader revenue capture around space programs in some cases, which can shift value between core C4ISR program spend and surrounding support activities and equipment. |

Overall, the comparison suggests that scope choices and timing of contract recognition explain most of the gap, more than a single growth assumption. By keeping the model tied to observable budgets, procurement cadence, orbit mix, and modernization timing, the final number stays transparent and easier to update when new awards or mission changes occur.

Key Questions Answered in the Report

What is the current value of the space-based C4ISR market?

The space-based C4ISR market is valued at USD 3.63 billion in 2026, and is projected to reach USD 4.61 billion by 2031 at a 4.91% CAGR.

Which segment leads revenue within space-based C4ISR?

ISR applications hold 75.35% of 2025 revenue, driven by optical, radar, and signals payload demand.

Why are low-Earth orbit constellations preferred for defense missions?

LEO delivers sub-20 millisecond latency, enabling real-time fire-control and resilience through proliferated fleets.

Which region is growing fastest in space-based C4ISR?

Asia-Pacific is projected to record a 5.89% CAGR through 2031 on the back of Chinese, Indian, and Korean programs.

How are software-defined payloads changing satellite operations?

They allow OTA waveform and algorithm updates, letting operators re-task satellites within hours instead of years.

What is a key emerging risk for space-based C4ISR assets?

Cyber-vulnerabilities in software-defined satellites present new attack surfaces that adversaries can exploit.

Page last updated on: