Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

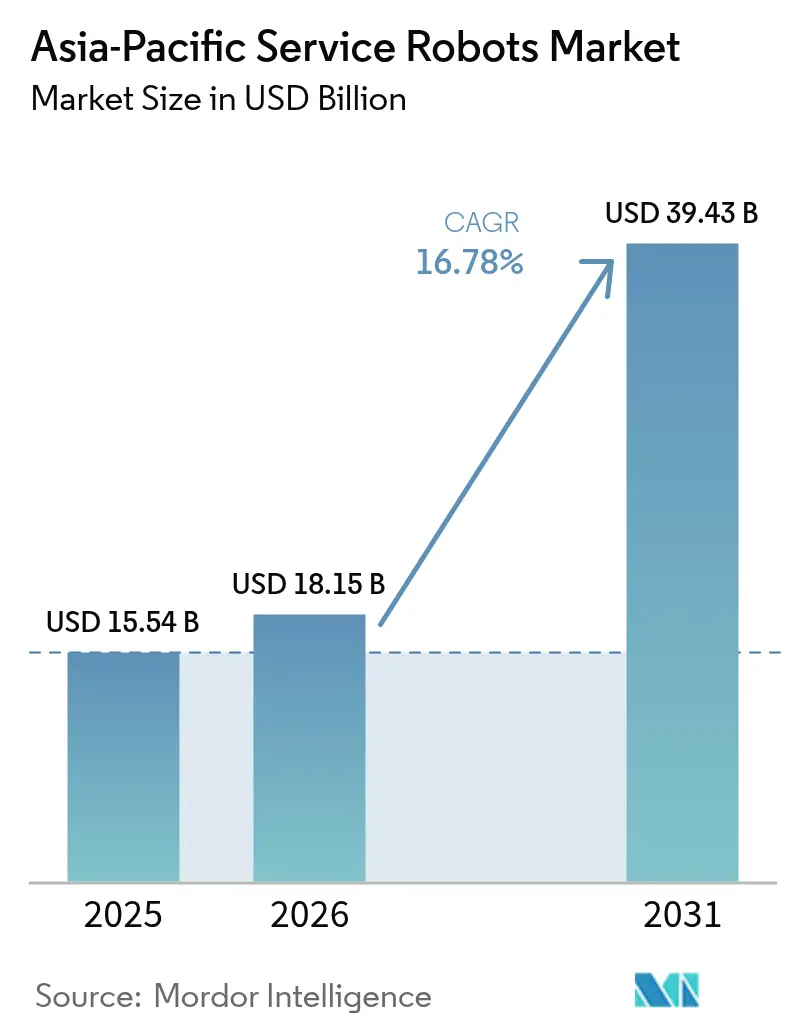

| Base Year Market Size (2025) | USD 15.54 Billion |

| Market Size (2026) | USD 18.15 Billion |

| Market Size (2031) | USD 39.43 Billion |

| Growth Rate (2026 - 2031) | 16.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Service Robots Market Analysis by Mordor Intelligence

Asia Pacific Service Robots Market size market size in 2026 is estimated at USD 18.15 billion, growing from 2025 value of USD 15.54 billion with 2031 projections showing USD 39.43 billion, growing at 16.78% CAGR over 2026-2031. A surge in automation programs across China, Japan and South Korea is redefining workforce strategies, while e-commerce, healthcare modernization and government-backed digital agendas accelerate adoption. Logistics automation is no longer an efficiency playit has become an operational necessity as tight labor markets and last-mile delivery pressures intensify. Healthcare providers now treat robots as core clinical assets that improve patient outcomes and relieve staff shortages. Convergence of 5G and on-board AI is enabling real-time remote control and data analytics, broadening deployment options into public services and critical infrastructure inspection. Although high integration costs and fragmented safety standards still temper uptake among SMEs, Robotics-as-a-Service models are starting to close the affordability gap.

Key Report Takeaways

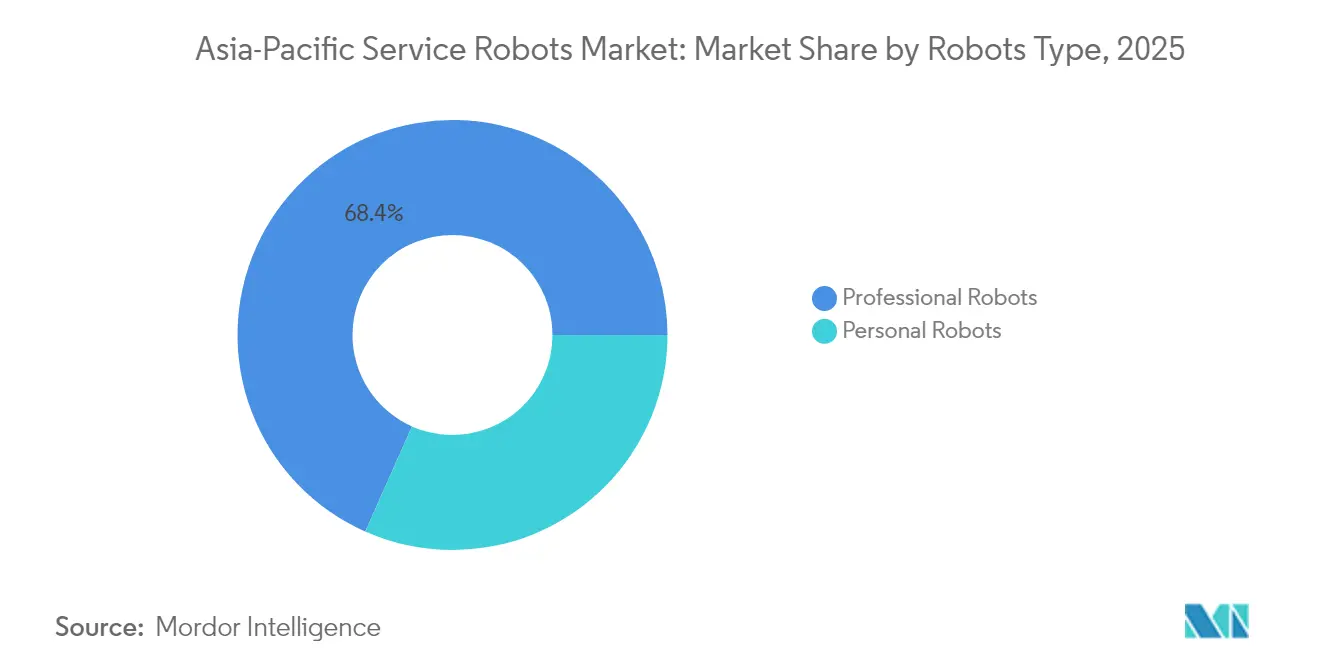

- By robots type, professional robots led with 68.35% of Asia Pacific Service Robots market share in 2025, while personal robots are projected to rise at a 18.02% CAGR through 2031.

- By application, transportation and logistics held 37.40% revenue share in 2025; healthcare is expected to grow at a 22.10% CAGR to 2031.

- By component, hardware accounted for 63.20% share of the Asia Pacific Service Robots market size in 2025, but software is poised to expand at 18.70% CAGR through 2031.

- By operating environment, ground robots dominated with 71.30% share in 2025, whereas aerial platforms are set to register 18.95% CAGR to 2031.

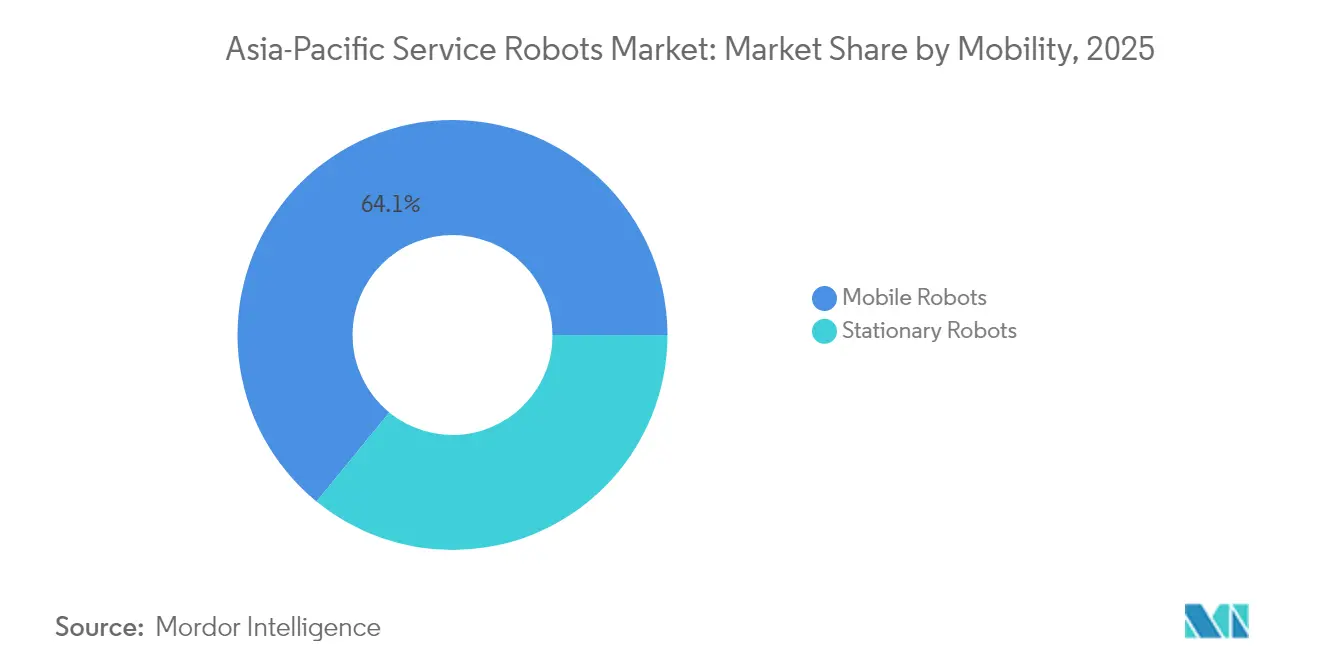

- By mobility, mobile robots captured 64.10% share of the Asia Pacific Service Robots market size in 2025 and remain the fastest-growing mobility class at 16.95% CAGR to 2031.

- By geography, China contributed 53.40% share in 2025; India is forecast to grow at 18.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Service Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom driving logistics AMRs | +3.2% | China, Japan, South Korea with spillover to Southeast Asia | Short term (≤ 2 years) |

| Aging-population healthcare demand | +2.8% | Japan, South Korea, China, with emerging impact in Singapore | Medium term (2-4 years) |

| Government incentives and Made-in-APAC programs | +1.9% | China, South Korea, Japan with policy coordination across APAC | Medium term (2-4 years) |

| 5G/AI convergence enabling remote autonomy | +1.5% | South Korea, China, Japan with infrastructure-dependent rollout | Long term (≥ 4 years) |

| Humanoid robots for EV-battery lines | +1.2% | China, South Korea with automotive manufacturing concentration | Medium term (2-4 years) |

| Infrastructure-inspection robots for aging assets | +0.8% | Japan, South Korea with expansion to mature APAC economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce boom driving logistics AMRs

Rising online retail volumes across Asia have pushed warehouse operators toward autonomous mobile robots (AMRs) that shrink fulfillment times and mitigate labor shortages. Chinese vendor Syrius Robotics plans to ship 3,000 AMRs annually to Japanese sites—10 times its current run-rate—as local overtime caps restrict driver availability.[1]Technology desk, “Warehouse Robot Maker Syrius Targets Japan,” Nikkei Asia, asia.nikkei.com Localized manufacturing by Libiao Robotics further illustrates how near-shore production sidesteps supply-chain friction and import duties. Payback periods now average under 2.5 years, making AMRs a viable option for mid-sized distributors. Regulatory changes therefore act as a demand catalyst, turning AMRs into essential infrastructure within the Asia Pacific Service Robots Market.

Aging-population healthcare demand

Japan’s share of citizens aged 65+ reached 27.3% in 2025, prompting hospitals and care homes to deploy robots for patient lifting, diaper changing and medication logistics. The AIREC caregiving robot from Waseda University showcases advanced physical assistance that surpasses basic monitoring.[2]Editorial board, “China’s Trillion-Yuan Robotics Fund,” South China Morning Post, scmp.com Robot integration has cut staff turnover and freed personnel for empathy-intensive tasks, while automated meal transport yields EUR 9,596 (USD 10,356) in annual savings per clinic.[3]Research team, “Meal-Transport Robots Cut Costs,” MDPI, mdpi.com China’s new international standard for elderly-care robots positions domestic suppliers for leadership in global applications, accelerating the Asia-Pacific service robots market toward healthcare value creation.

Government incentives and Made-in-Asia Pacific programs

Beijing’s CNY 1 trillion (USD 138 billion) state fund and MIIT’s humanoid-robot guidelines target mass production by 2025. Parallel initiatives in South Korea, such as the USD 2.53 billion Super Gap Industry Program, offer low-interest financing to robotics start-ups. These capital injections shorten development cycles, encourage local sourcing and expand the overall Asia-Pacific Service Robots Market.

5G/AI convergence enabling remote autonomy

China Mobile and Huawei’s Kuafu humanoid leverages 5G-Advanced for centimeter-level positioning and edge AI, illustrating how ultra-low latency unlocks true tele-operation. NTT DATA’s factory-inspection trials using the IOWN All-Photonics Network showed real-time video analytics without degradation, achieving latency targets impossible on legacy Wi-Fi. As networks mature, remote inspection, maintenance and public-service deployments are expected to proliferate across the Asia Pacific Service Robots Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and integration cost | -2.1% | APAC-wide with acute impact on SMEs in emerging markets | Short term (≤ 2 years) |

| Fragmented safety/certification regimes | -1.4% | Cross-border operations across APAC regulatory jurisdictions | Medium term (2-4 years) |

| Data-privacy and cyber-security concerns | -0.9% | China, South Korea, Japan with consumer-facing applications | Medium term (2-4 years) |

| Import dependence on precision actuators and sensors | -0.7% | China, India, Southeast Asia with supply chain vulnerabilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High installation and integration cost

Although hardware prices keep falling—the average humanoid is projected to reach USD 20,000-30,000 in 2025—total integration outlays often run two to three times the purchase cost due to site retrofits and staff training. For many SMEs, capital constraints delay adoption in the Asia Pacific Service Robots market. RaaS vendors now offer subscription models covering maintenance and updates, helping customers bypass large upfront expense.

Fragmented safety/certification regimes

Inconsistent rules raise compliance costs and time-to-market. South Korea’s privacy probe into Roborock vacuums points to divergent data-protection standards that force manufacturers into country-by-country redesigns. Shanghai’s humanoid-robot emergency-response guidelines may conflict with Japan’s ISO draft revisions, complicating cross-border scaling in the Asia Pacific Service Robots Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robots Type: Professional Robots Drive Industrial Transformation

Professional robots generated the bulk of 2025 revenues, holding 68.35% of Asia Pacific Service Robots market share. Their leadership rests on tangible ROI: AMR fleets cut picking time by 50% while powered exoskeletons reduce workplace injuries. Logistics systems remain the highest-revenue subsegment, propelled by omnichannel retail and same-day delivery obligations. Medical robots command premium prices for surgical precision and hospital logistics, whereas exoskeletons address lifting and fatigue issues on assembly lines. Public-relation robots offer concierge services in hospitality but adoption is moderated by cultural acceptance and language nuance.

Personal robots are scaling quickly, posting a 18.02% CAGR forecast through 2031. Domestic cleaning units lead shipments, illustrated by Ecovacs hitting RMB 16.54 billion (USD 2.3 billion) in 2024 revenue despite margin pressure. Elderly-care companions and wearable assistance devices promise the next leg of growth as aging societies drive demand. Entertainment models—pet-inspired bots and STEM education kits—round out the segment, enhancing long-tail sales across the Asia Pacific Service Robots Market.

By Component: Software Drives Intelligence Revolution

Hardware captured 63.20% of 2025 revenue. Actuators remain the costliest element as torque density advances, and sensor fusion raises ASPs for LiDAR and depth cameras. Johnson Electric reported double-digit Asian growth in motion systems linked to robotics demand.

Software is cementing its role as the value engine, set to post 18.70% CAGR to 2031. Cloud-connected orchestration, perception algorithms and fleet-management dashboards convert raw hardware into adaptable solutions. OMRON intends to surpass JPY 100 billion (USD 682 million) in data-solution sales by 2027, symbolizing the transition from product vendor to platform orchestrator. Services—maintenance, analytics, training—unlock recurring revenue in the Asia Pacific Service Robots market.

By Operating Environment: Ground Operations Dominate

Ground robots held 71.30% of 2025 revenue, buoyed by decades-old navigation algorithms and safety frameworks that assure reliable indoor mobility. Factories, hospitals and malls offer structured terrain, and battery swaps can be integrated into workflow.

Aerial robots are climbing at 18.95% CAGR. Drones equipped with AI vision survey aging bridges, reducing manual inspections by up to 60%. Delivery pilots in dense urban corridors are gaining regulatory backing as civil-aviation bodies issue flight corridors. Marine robots, though smaller in value, show promise for offshore wind inspection and aquaculture monitoring, expanding the scope of the Asia Pacific Service Robots Market.

By Mobility: Mobile Robots Enable Flexible Operations

Mobile systems accounted for 64.10% of 2025 sales, reflecting growing customer preference for flexible automation. UBTech’s 500-unit Walker S1 order highlights demand for humanoids that can traverse multiple stations, thereby boosting utilization. Mobile fleets help SMB factories amortize costs across varied tasks.

Stationary robots remain critical for micro-precision or high-payload tasks such as lab processing or semiconductor handling. Nevertheless, mobile platforms are forecast to grow at a 16.95% CAGR, aided by improved energy density and swappable batteries that extend duty cycles in the Asia Pacific Service Robots Market.

By Application: Healthcare Leads Growth Transformation

Transportation and logistics retained a 37.40% share of the 2025 Asia Pacific Service Robots market size, supported by rising e-commerce parcels and stricter delivery windows. Warehouse AMRs improve throughput and mitigate overtime restrictions, while cross-docking robots streamline pallet movement. Defense, agriculture, and mining uses remain steady but specialized.

Healthcare is set to expand at a 22.10% CAGR to 2031. Robots now assist with surgical procedures, manage ward logistics, and interact with patients. Singapore’s Changi General Hospital operates a national lab that explores precision-medicine robots and autonomous pharmacy dispensing. Payback is measurable: one hospital saved EUR 9,596 (USD 10,356) annually on meal logistics alone. As reimbursement models shift toward outcome-based metrics, stakeholders view robots as strategic levers for quality and efficiency within the Asia Pacific Service Robots Market.

Geography Analysis

China secured 53.40% of 2025 revenues in the Asia Pacific Service Robots Market, underpinned by more than 190,000 valid patents and vertically integrated supply chains. The 14th Five-Year Plan and a nearly CNY 1 trillion (USD 138 billion) investment pool assure sustained leadership to 2030. City-level clusters in Shenzhen and Hangzhou offer subsidies for AI algorithms and sensor fabs, thereby keeping BOM costs low and speeding up the time-to-market.

India is projected to be the fastest-growing geography at 18.20% CAGR. Smart-factory incentives, healthcare modernization, and digital-public-infrastructure roll-outs create greenfield opportunities for service robots. Strong software talent allows local firms to specialize in autonomy stacks while importing hardware, accelerating time-to-deployment within the Asia Pacific Service Robots Market.

Japan and South Korea maintain robust positions. Japan’s USD 300 million care-robot program ensures continuous demand, as its rapidly aging society prioritizes eldercare solutions. South Korea’s Fourth Intelligent Robot Basic Plan allocates USD 2.24 billion to push service-robot adoption in manufacturing and daily life. Elsewhere, Singapore’s smart-hospital pilots and Southeast Asia’s manufacturing diversification offer incremental volume growth as cost curves fall.

Competitive Landscape

Competition is moderating yet gradually concentrating around end-to-end platforms. Chinese leaders such as UBTech, Ecovacs and SIASUN exploit supply-chain depth to release frequent model updates at competitive price points. Japanese and South Korean incumbents focus on precision mechatronics and human-robot interaction, while multinationals such as Panasonic and Omron bundle robots with legacy factory automation suites.

Strategically, vendors pursue vertical integration—combining hardware, AI software and cloud services—to lock users into ecosystems and capture lifecycle revenue. Robotics-as-a-Service subscriptions are widening addressable markets by converting capex to opex, particularly appealing to SMEs wary of high upfront costs in the Asia Pacific Service Robots Market.

Patent activity centers on vision-based grasping and edge-AI optimization. UBTech filed 59 U.S. patents over a five-year period, mapping out intellectual property defenses for its Walker platform. Companies without deep IP portfolios partner for sensor or AI modules, accelerating time-to-market but risking margin erosion.

Asia-Pacific Service Robots Industry Leaders

LG Electronics Inc.

UBTECH Robotics Inc.

Milagrow HumanTech

Hyundai Robotics Co. Ltd.

Hanwha Robotics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Foxconn and Kawasaki began trials of a medical-service robot in Taiwan hospitals, combining Foxconn’s manufacturing prowess with Kawasaki’s robotics IP for healthcare entry.

- June 2025: Samsung Electro-Mechanics and LG Innotek advanced robotics camera modules, with LG negotiating supply for Figure AI, signaling component-maker migration into robotic value chains.

- June 2025: H-Robotics secured KRW 5.2 billion (USD 3.8 million) from the Korean MOTIE Bio-industry Project to build an AI rehab platform, anchoring public-health applications.

- April 2025: Dongfeng Motor partnered with UBTech to use Walker S for seat-belt inspection and door-lock testing, layering robots into final-quality checks and tightening traceability.

Asia-Pacific Service Robots Market Report Scope

The Asia-Pacific Service Robots Market Report is Segmented by Robots Type (Professional Robots, and Personal Robots), Application (Military and Defense, Agriculture, Construction and Mining, Transportation and Logistics, Healthcare, Government, and Other Applications), Component (Hardware, Software, and Services), Operating Environment (Ground, Aerial, and Marine), Mobility (Mobile Robots, and Stationary Robots), and Country (China, India, Japan, South Korea, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Robots Type

| Professional Robots | Logistic Systems |

| Medical Robots | |

| Powered Human Exoskeletons | |

| Public-Relation Robots | |

| Personal Robots | Domestic |

| Entertainment | |

| Elderly and Handicap Assistance |

By Application

| Military and Defense |

| Agriculture, Construction and Mining |

| Transportation and Logistics |

| Healthcare |

| Government |

| Other Applications |

By Component

| Hardware | Actuators |

| Sensors | |

| Controllers | |

| Software | |

| Services |

By Operating Environment

| Ground |

| Aerial |

| Marine |

By Mobility

| Mobile Robots |

| Stationary Robots |

By Country

| China |

| India |

| Japan |

| South Korea |

| Rest of Asia-Pacific |

| By Robots Type | Professional Robots | Logistic Systems |

| Medical Robots | ||

| Powered Human Exoskeletons | ||

| Public-Relation Robots | ||

| Personal Robots | Domestic | |

| Entertainment | ||

| Elderly and Handicap Assistance | ||

| By Application | Military and Defense | |

| Agriculture, Construction and Mining | ||

| Transportation and Logistics | ||

| Healthcare | ||

| Government | ||

| Other Applications | ||

| By Component | Hardware | Actuators |

| Sensors | ||

| Controllers | ||

| Software | ||

| Services | ||

| By Operating Environment | Ground | |

| Aerial | ||

| Marine | ||

| By Mobility | Mobile Robots | |

| Stationary Robots | ||

| By Country | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the APAC Service Robots Market?

It stands at USD 18.15 billion in 2026 with a forecast to reach USD 39.43 billion by 2031.

Which segment grows fastest within the market?

Healthcare applications are projected to expand at a 22.10% CAGR during 2026-2031.

How significant are mobile robots?

Mobile platforms hold 64.10% of 2025 revenue and are expected to grow 16.95% CAGR during 2026-2031 as factories seek flexible automation.

Why is India a focus geography?

India’s 18.20% CAGR stems from smart-factory incentives, healthcare modernization and strong software capabilities during 2026-2031.

What is driving software revenues?

Fleet-management, perception AI and cloud orchestration are pushing software growth at 18.70% CAGR during 2026-2031, overtaking hardware as the key value layer.

How do 5G networks affect robot deployment?

5G-Advanced provides ultra-low latency, enabling real-time remote operation and expanding use cases in inspection and public services.

Page last updated on: