Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

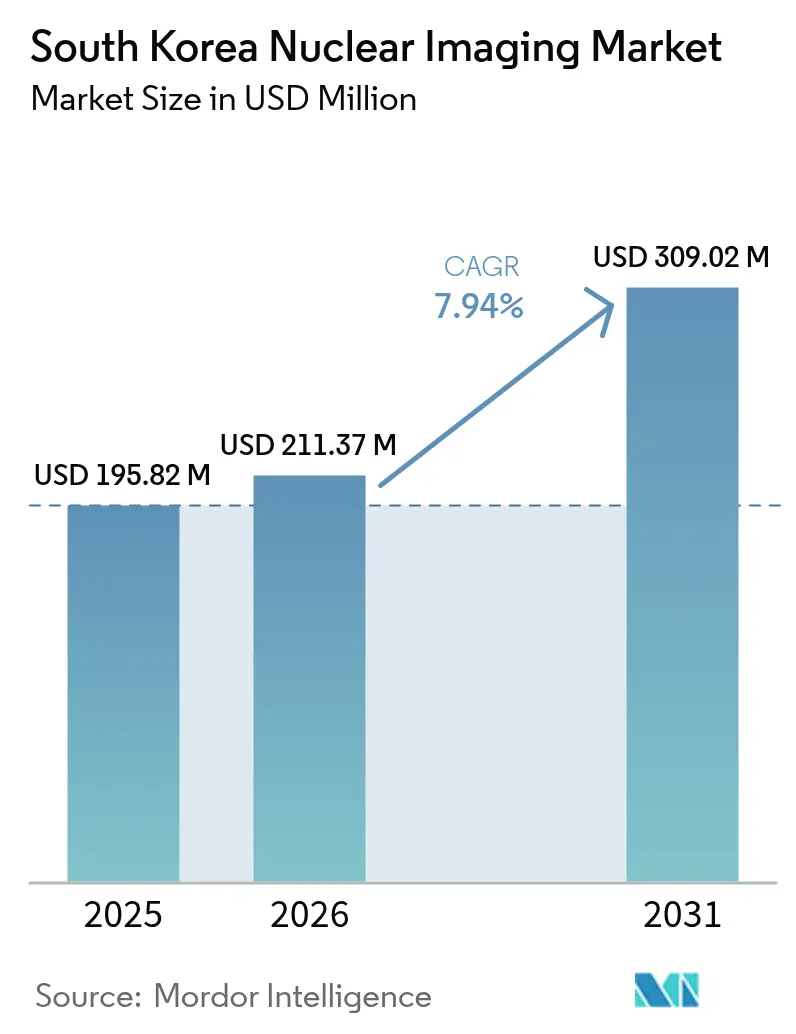

| Base Year Market Size (2025) | USD 195.82 Million |

| Market Size (2026) | USD 211.37 Million |

| Market Size (2031) | USD 309.02 Million |

| Growth Rate (2026 - 2031) | 7.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Nuclear Imaging Market Analysis by Mordor Intelligence

South Korea nuclear imaging market size in 2026 is estimated at USD 211.37 million, growing from 2025 value of USD 195.82 million with 2031 projections showing USD 309.02 million, growing at 7.94% CAGR over 2026-2031. Robust demand for precision oncology diagnostics, expanding domestic radioisotope production, and rapid integration of artificial intelligence (AI) into imaging workflows collectively underpin this trajectory[1]Source: Ministry of Health and Welfare, “보건복지부 2025년 예산, 125조 4,909억 원 확정,” mohw.go.kr . Continued build-out of cyclotron capacity, coupled with favorable reimbursement for neurology PET tracers, is widening clinical adoption beyond the Seoul–Busan corridor. Private-sector hospital investment is shortening equipment refresh cycles, while international medical-tourism inflows stimulate premium diagnostic services. Persistent supply-chain fragility for imported isotopes and workforce shortages in nuclear-medicine technologists remain structural headwinds.

Key Report Takeaways

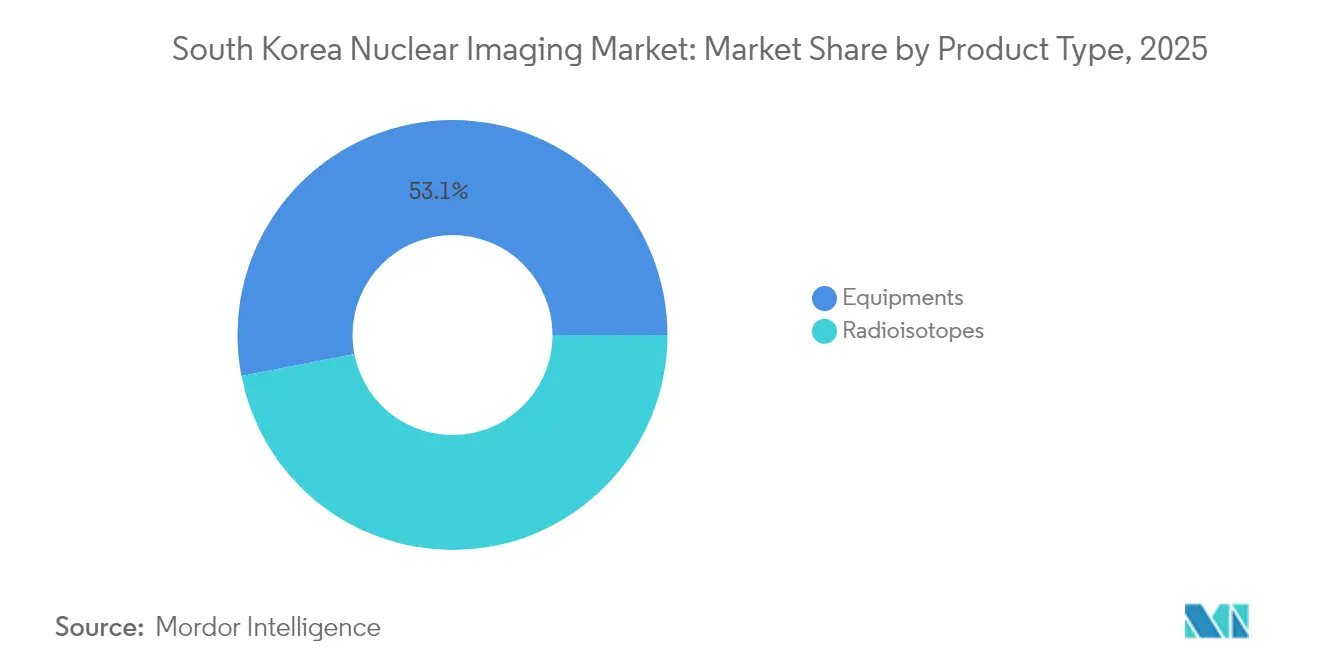

- Equipment captured 53.05% of the South Korea nuclear imaging market in 2025, reflecting provider preference for high-resolution molecular imaging, Radiosiotopes outpaced all other equipment segments with an 8.01% CAGR forecast through 2031, aided by lower capital costs and broader provincial rollout.

- Oncology applications accounted for 64.19% of the South Korea nuclear imaging market in 2025 as aging demographics accelerated demand for cancer staging and therapy monitoring, Neurology is projected to record the fastest growth, expanding at an 8.17% CAGR to 2031 on the back of dementia-care reimbursement expansion.

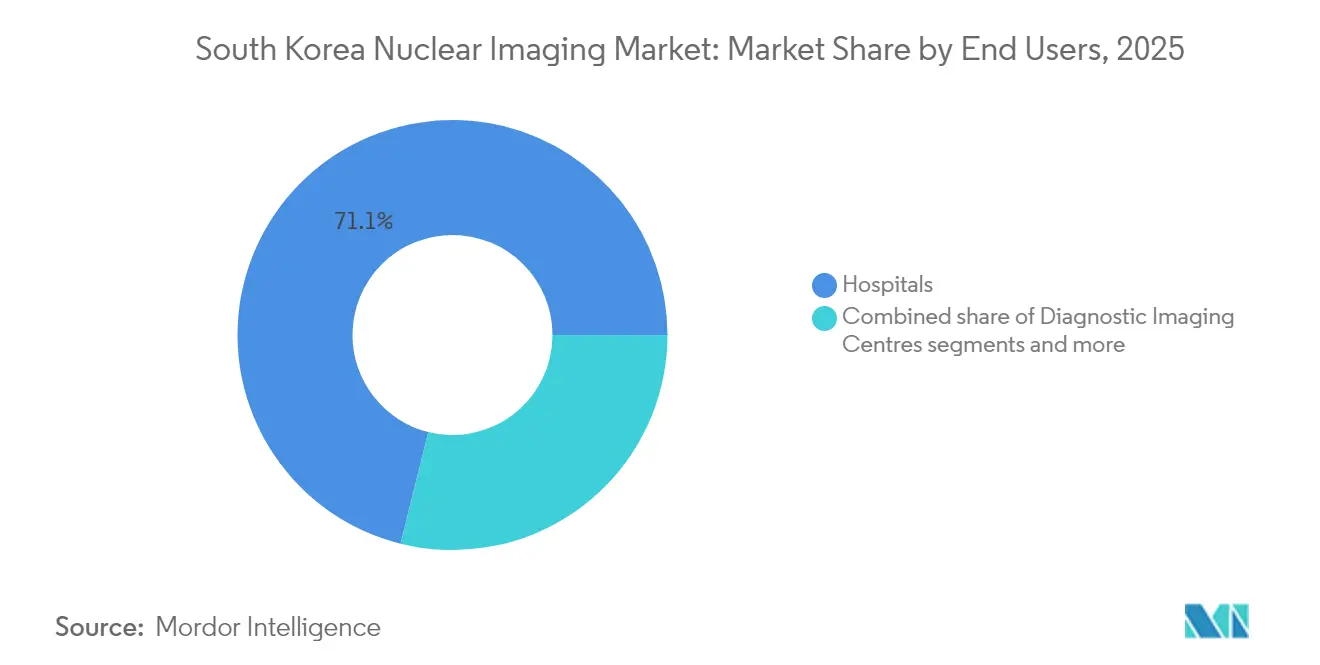

- Hospitals dominated end-user uptake with a 71.12% revenue share in 2025, leveraging integrated diagnostic-treatment pathways, Academic and research institutes are forecast to grow at 8.03% CAGR through 2031, driven by theranostics clinical-trial pipelines and government R&D grants.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Nuclear Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing oncology PET/CT demand driven by aging population | +1.8% | National, concentrated in Seoul-Busan corridor | Long term (≥ 4 years) |

| Government reimbursement expansion for dementia PET tracers | +1.2% | National, with priority in underserved regions | Medium term (2-4 years) |

| Roll-out of domestic Ga-68 generator manufacturing capacity | +1.5% | National, centered on KAERI facilities | Medium term (2-4 years) |

| Hospital privatisation accelerating equipment refresh cycles | +0.9% | Urban centers, particularly Seoul metropolitan area | Short term (≤ 2 years) |

| AI-based image-reconstruction lowering dose & scan-time | +1.1% | Major hospital networks nationwide | Short term (≤ 2 years) |

| Cyclotron build-out linked to theranostics clinical trials | +1.0% | Academic medical centers and research institutes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Oncology PET/CT Demand Driven by an Aging Population

Korea’s population aged 65 plus will reach 20.3% in 2025, placing sustained pressure on oncology imaging capacity. High-sensitivity PET/CT scanners deployed at the National Cancer Center show markedly improved lesion detection in prostate cancer, achieving 86.9% accuracy with 68Ga-NGUL tracers. Hospitals are accelerating procurement schedules, with Yonsei Cancer Center adding a carbon-ion facility that began treating patients in 2023. Parallel clinical-trial data demonstrate 49.5% objective response rates for targeted alpha therapy in neuroendocrine tumors. These factors combine to keep the South Korea nuclear imaging market firmly anchored in oncology leadership.

Government Reimbursement Expansion for Dementia PET Tracers

The Health Insurance Review and Assessment Service widened coverage for amyloid and tau PET imaging in January 2025, cutting patient co-payments by 18%. The policy supports a projected trebling of dementia prevalence by 2050, intensifying demand for early PET-based diagnosis. Seoul-based tertiary centers report 92% diagnostic accuracy when pairing AI analytics with PET for mild cognitive impairment screening. Expanded insurance coverage thereby sustains medium-term volume growth for the South Korea nuclear imaging market.

Roll-out of Domestic Ga-68 Generator Manufacturing Capacity

KAERI commenced commercial actinium-225 output in mid-2025 and is scaling gallium-68 generator lines to mitigate European reactor supply risk[2]Source: The Korea Times, “Korea to produce cancer treatment actinium-225 domestically by mid-2025,” koreatimes.co.kr . Cyclotron-produced Ga-68 shows 491 GBq/µmol apparent molar activity, markedly outclassing generator-derived alternatives. Domestic isotopes are priced nearly 14% below imported equivalents, freeing budget for equipment upgrades. Localized supply thereby strengthens resilience and underpins the South Korea nuclear imaging market.

Hospital Privatization Accelerates Equipment Refresh Cycles

Approval of Greenland International Hospital as Korea’s first for-profit facility signals broader privatization momentum. Government infrastructure packages allocate KRW 10 trillion for hospital expansion through 2028, amplifying private capital flows. Equipment vendors note reduced sales-cycle times, reflecting aggressive procurement by urban private centers. The trend elevates unit shipments and lifts near-term revenue for the South Korea nuclear imaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiopharmaceutical supply chain intermittency | -1.3% | Global impact, affecting Korean imports | Short term (≤ 2 years) |

| High capital cost of PET/MR limiting provincial access | -0.8% | Rural and secondary cities outside Seoul-Busan | Medium term (2-4 years) |

| Shortage of certified nuclear-medicine technologists | -1.1% | National, acute in rural areas | Long term (≥ 4 years) |

| Stringent MOHW radio-isotope transport regulations | -0.6% | National, affecting inter-facility transfers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Radiopharmaceutical Supply-Chain Intermittency

The October 2024 European reactor outage slashed Mo-99 output by 50%, forcing Korean clinics to ration 99mTc doses. Cardiology centers extended imaging windows and curtailed elective studies, undercutting procedure volumes. Reliance on aged foreign reactors exposes Korea to geopolitical and maintenance shocks, pressuring procurement budgets. Accelerated domestic actinium-225 and Ga-68 programs mitigate but do not yet eliminate risk. Supply instability remains the largest drag on the South Korea nuclear imaging market.

High Capital Cost of PET/MR Limiting Provincial Access

Integrated PET/MR systems exceed USD 5 million per unit, constraining adoption outside academic flagships. Provincial hospitals face longer payback horizons amid lower patient throughput. Government grants focus on PET/CT expansion, leaving PET/MR largely unfunded. The cost gap sustains modality imbalance, limiting comprehensive oncologic imaging in rural areas. Uneven equipment distribution restrains equal growth across the South Korea nuclear imaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Equipment Dominance Strengthens High-Resolution Imaging Adoption

The Equipment segment captured 53.05% of the South Korea nuclear imaging market share in 2025, underscoring provider commitment to high-resolution molecular imaging. Rapid rollout of digital detector technology improves sensitivity, letting hospitals justify premium pricing. Domestic Ga-68 production lowers tracer overhead, raising PET utilization rates across oncology and neurology. SPECT retains a strong installed base, yet faces competitive displacement in capital budgets. Equipment vendors increasingly bundle AI reconstruction to differentiate offerings, supporting higher average-selling prices.

Radioisotopes is projected to expand at an 8.01% CAGR on a value basis through 2031 as provincial hospitals favor its lower entry cost. Hybrid SPECT/CT upgrades extend the modality’s lifespan by improving anatomical localization in cardiology and thyroid imaging. The radioisotope sub-segment benefits from steady technetium-99m demand despite global supply volatility. Cyclotron-enabled copper-64 and gallium-68 pipelines diversify tracer options, reinforcing resilience. Overall, the South Korea nuclear imaging market continues to tilt toward PET while sustaining niche opportunities in SPECT and emerging therapeutic isotopes.

By Application: Oncology Leads While Neurology Gains Momentum

Oncology maintained a commanding 64.19% revenue share in 2025, reflecting Korea’s advanced multi-modality cancer care pathways. Proton and carbon-ion centers integrate diagnostic PET/CT into treatment planning, deepening procedure frequency per patient. Targeted alpha therapies guided by theranostic imaging expand addressable spend per case. Cardiology remains stable but secondary, awaiting broader tracer diversification.

Neurology shows the fastest acceleration with an 8.17% CAGR to 2031 as dementia screening becomes policy-backed. New amyloid and tau tracers coupled with AI analytics advance early diagnosis, pressing hospitals to add neuro-focused PET capacity. Thyroid imaging and therapy continue as steady-state niches supported by HANARO reactor-supplied I-131. The South Korea nuclear imaging market thus balances entrenched oncology leadership with rising neurological demand.

By End User: Academic Centers Propel Theranostics Research

Hospitals command 71.12% of the South Korea nuclear imaging market, leveraging integrated inpatient, outpatient, and surgical services. Flagship university hospitals serve as national referral hubs, operating multi-scanner suites that feed high daily throughput. Private facilities invest aggressively to retain high-acuity oncology and neurology cases in competitive urban corridors.

Academic and research institutes post an 8.03% CAGR through 2031, driven by translational theranostics programs and government R&D grants. Their proximity to cyclotrons and GMP radiochemistry labs positions them to pioneer actinium-225 and copper-64 trials. Dedicated diagnostic imaging centers fill urban scheduling gaps, particularly for PET/CT overflow. Collectively, these end-user dynamics reinforce sustained demand within the South Korea nuclear imaging market.

Geography Analysis

The Seoul metropolitan area hosts the highest density of PET/CT and cyclotron assets, anchoring more than two-thirds of national procedure volume. Flagship institutions—including Seoul National University Hospital and Korea University Medical Center—align clinical services with in-house tracer production, further cementing regional dominance. Concentration in Seoul accelerates innovation cycles, but also magnifies disparities with provincial hospitals.

Busan and surrounding Southeastern provinces represent the second growth pole, catalyzed by National University Hospital’s planned proton center and industrial links to isotope-production supply chains. Regional policy incentives, including corporate tax relief for medical-tourism facilities, spur private-sector imaging investments. However, capital intensity limits PET/MR penetration, and technologist scarcity persists outside major cities.

Rural districts remain underserved owing to long travel distances and limited equipment budgets. The Act on Integrated Support for Community Care encourages tertiary centers to deploy mobile imaging units and tele-nuclear-medicine platforms, yet execution lags due to transport-permit constraints. Addressing geographic imbalances will be crucial for equitable expansion of the South Korea nuclear imaging market.

Competitive Landscape

Global OEMs tightly hold modality leadership by combining equipment sales with structured service contracts and tracer-distribution alliances. GE HealthCare’s USD 183 million purchase of Nihon Medi-Physics secures regional radiopharmaceutical supply, reinforcing its PET/CT installed-base strategy. Siemens Healthineers fields the Biograph Trinion PET/CT with air-cooled architecture, aiming to lower facility retro-fit costs for private clinics. Philips embeds SmartSpeed AI into MRI to improve scan efficiency, positioning for cross-modal upsell .

Domestic firms seize white-space opportunities in therapeutics. SK Biopharmaceuticals’ actinium-225 pipeline with KIRAMS exemplifies synergistic research-to-manufacture capability . Korea Hydro & Nuclear Power and Framatome evaluate lutetium-177 production at Wolsong, leveraging existing reactor infrastructure . Smaller venture-backed players focus on AI workflow orchestration, addressing staffing bottlenecks rather than hardware.

Regulatory compliance under the Nuclear Safety Act imposes high entry barriers, favoring players with established quality systems. Service differentiation shifts toward end-to-end solutions—hardware, tracers, AI, and maintenance bundles—rather than price competition. Collectively, the top five companies capture roughly 55% of revenue, indicating a moderate concentration in the South Korea nuclear imaging market.

South Korea Nuclear Imaging Industry Leaders

Samyoung Unitech

GE Healthcare

FutureChem

IBA Radiopharma Solutions

NuCare Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Korea Atomic Energy Research Institute announced domestic production of actinium-225 cancer-treatment isotope beginning mid-2025, a strategic step toward radioisotope self-reliance

- December 2024: SK Biopharmaceuticals entered a collaborative research agreement with Proen Therapeutics to develop two pre-clinical small protein-based radiopharmaceuticals by 2027, advancing national theranostics capabilities

South Korea Nuclear Imaging Market Report Scope

As per the scope of the report, nuclear imaging encompasses gamma, SPECT, and PET imaging techniques. Nuclear medicine imaging procedures are non-invasive and, except for intravenous injections, are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. The South Korea Nuclear Imaging Market is segmented by Product (Equipment (Single Photon Emission Computed Tomography (SPECT), Positron-emission Tomography (PET)) and Radioisotope (SPECT Radioiso topes and PET Radioisotopes)) and Application (Orthopedics, Thyroid, Cardiology, Oncology, and Others). The report offers the value (in USD million) for the above segments.

By Product (Value)

| Equipment | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) |

| Thallium-201 (Tl-201) | ||

| Gallium-67 (Ga-67) | ||

| Iodine-123 (I-123) | ||

| Other SPECT Isotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (Rb-82) | ||

| Other PET Isotopes | ||

By Application (Value)

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other Applications |

By End User (Value)

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product (Value) | Equipment | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) | |

| Thallium-201 (Tl-201) | |||

| Gallium-67 (Ga-67) | |||

| Iodine-123 (I-123) | |||

| Other SPECT Isotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (Rb-82) | |||

| Other PET Isotopes | |||

| By Application (Value) | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other Applications | |||

| By End User (Value) | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the projected value of the South Korea nuclear imaging market in 2031?

The market is forecast to reach USD 309.02 million by 2031, expanding at a 7.94% CAGR over 2026-2031.

Which imaging modality currently leads unit revenue in Korea?

Forecasts place the market at USD 309.02 million by 2031, reflecting an 7.94% CAGR over 2026-2031.

Which imaging modality currently leads unit revenue in Korea?

PET holds leadership, capturing 53.05% share of 2025 sales thanks to oncology demand and domestic Ga-68 supply.

Why is neurology considered a high-growth application area?

Expanded reimbursement for dementia tracers and AI-enabled image analysis support an 8.17% CAGR for neurology procedures to 2031.

How are domestic isotope programs affecting supply stability?

KAERIs production of actinium-225 and gallium-68 reduces reliance on European reactors, mitigating recent Mo-99 shortages.

What challenges limit market expansion in rural provinces?

High PET/MR capital costs, technologist shortages, and stringent isotope-transport rules slow equipment deployment outside metro areas.

Which end-user group is expected to record the fastest growth?

Academic and research institutes lead with an 8.03% CAGR as they scale theranostics trials and cyclotron partnerships.

Page last updated on: