Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

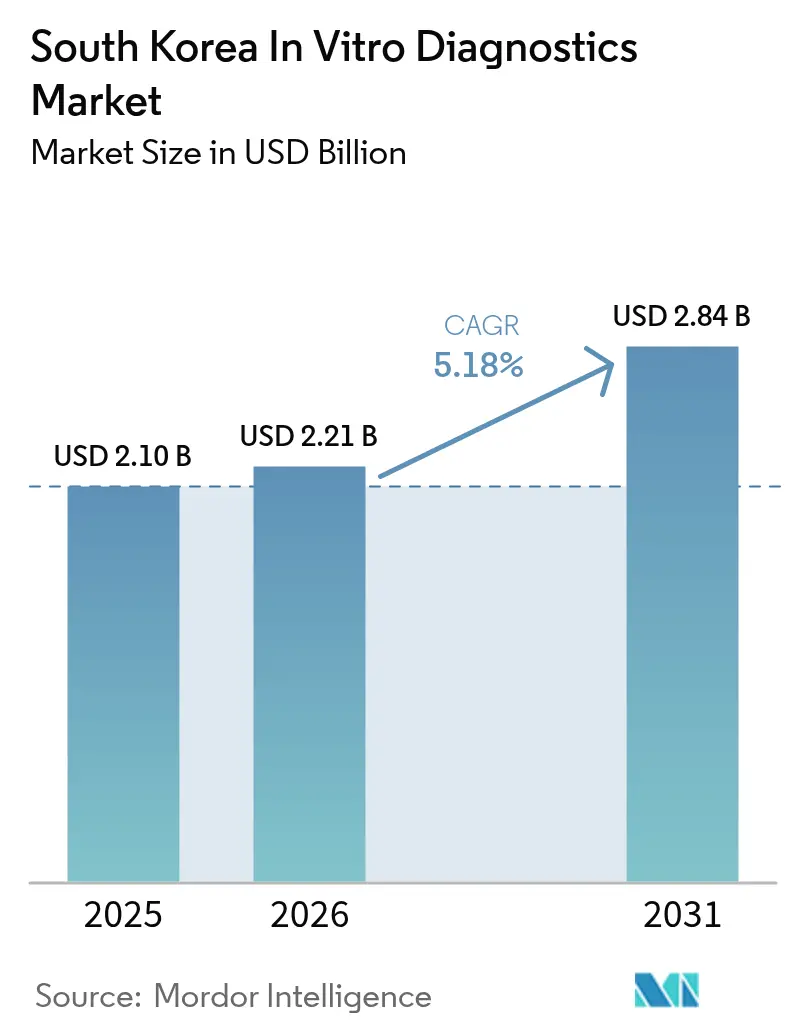

| Base Year Market Size (2025) | USD 2.10 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 2.84 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

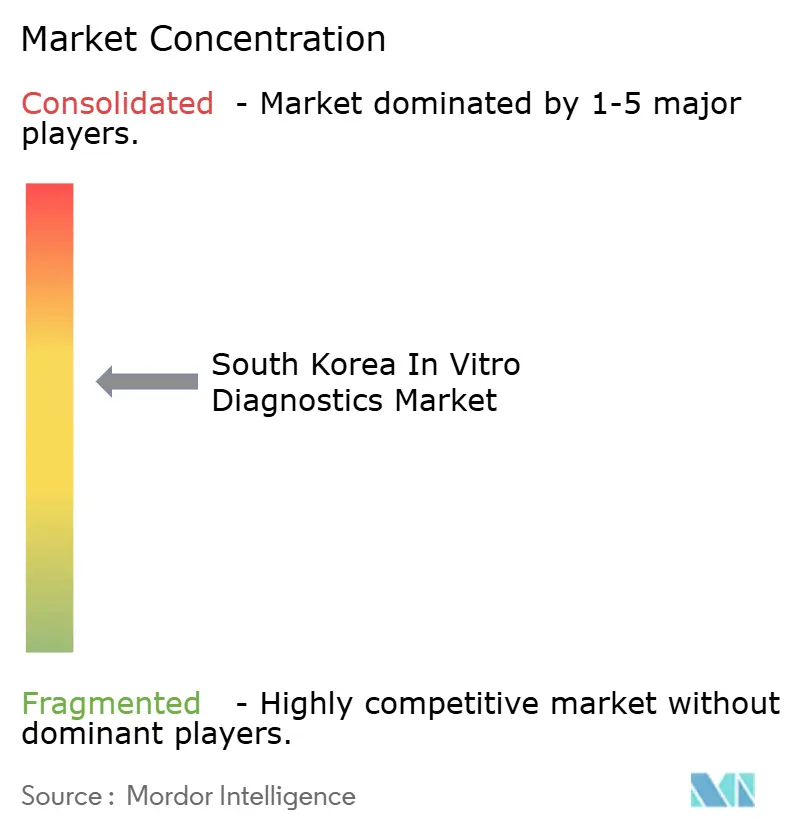

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea In Vitro Diagnostics Market Analysis by Mordor Intelligence

The South Korea in-vitro diagnostics market size is expected to grow from USD 2.10 billion in 2025 to USD 2.21 billion in 2026 and is forecast to reach USD 2.84 billion by 2031 at 5.18% CAGR over 2026-2031. The post-pandemic reset is moderating headline growth, yet rising chronic-disease prevalence, an expanding geriatric base, and ongoing universal coverage under the National Health Insurance System (NHIS) are securing a dependable demand baseline. Companies are shifting portfolios from COVID-19 kits toward oncology and metabolic panels, while domestic reagent makers benefit from the industry’s recurring-revenue model. Consolidation of independent reference laboratories, steady venture-capital inflows into biotech clusters, and AI-enabled home-testing pilots are amplifying scale advantages. Regulatory clarity from the Digital Medical Products Act, effective January 2025, is encouraging investment in software-driven diagnostics even as stringent Ministry of Food and Drug Safety (MFDS) reviews keep quality standards high.

Key Report Takeaways

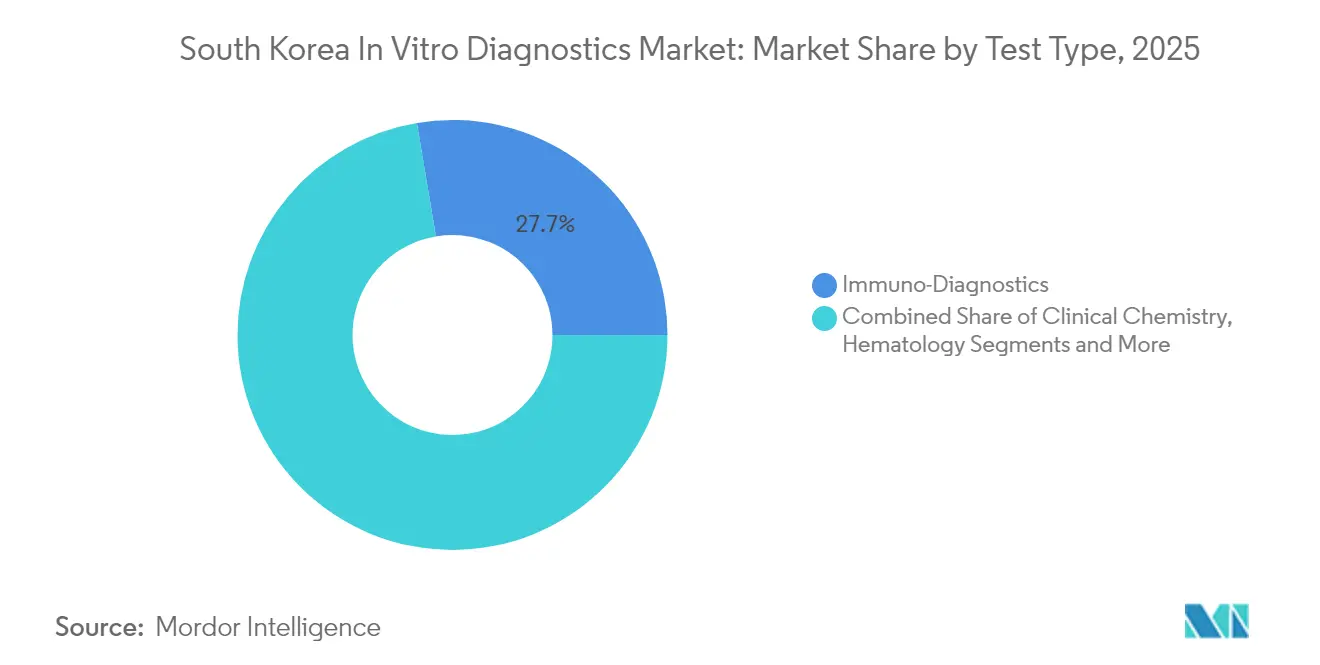

- By test type, immuno-diagnostics led with 27.65% of South Korea in-vitro diagnostics market share in 2025, while molecular diagnostics is projected to advance at 8.85% CAGR through 2031.

- By product, reagents and consumables accounted for 74.05% share of the South Korea in-vitro diagnostics market size in 2025; instruments are forecast to grow at 6.78% CAGR from 2026 to 2031.

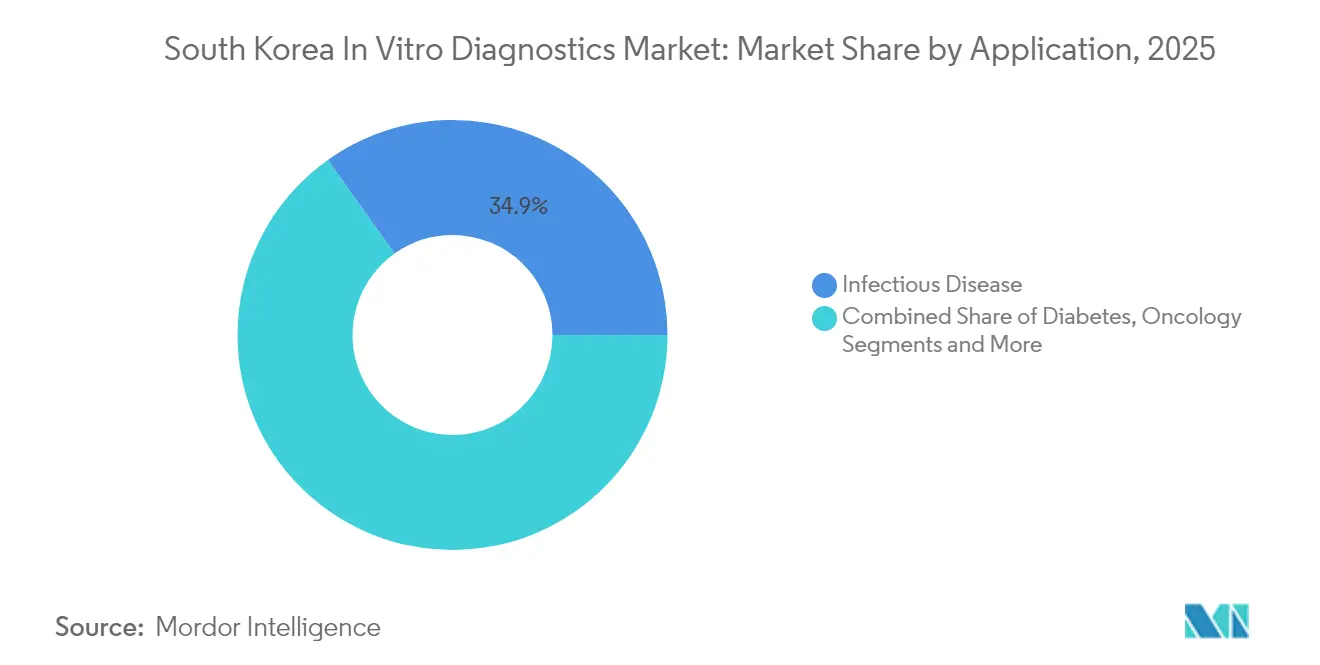

- By application, infectious disease testing commanded 34.85% revenue in 2025 and oncology diagnostics is slated to expand at 8.18% CAGR to 2031.

- By end-user, independent laboratories captured 54.55% revenue share in 2025, whereas hospital-based labs are set to post 6.86% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea In Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Geriatric Population & Chronic-Disease Burden Elevating Test Volumes | +1.8% | National, with higher impact in urban centers | Long term (≥ 4 years) |

| Universal NHIS Coverage & Screening Mandates Sustaining High Utilisation Rates | +1.2% | National | Medium term (2-4 years) |

| Expansion of Private Reference Labs & Consolidated Testing Driving Central-Lab Demand | +0.9% | Urban centers, with limited rural impact | Medium term (2-4 years) |

| Robust Government & VC Funding for Domestic Biotech/IVD Innovation Clusters | +0.7% | Major innovation hubs (Seoul, Daejeon, Incheon) | Medium term (2-4 years) |

| Growth of Digital Health & Home-Testing Ecosystems Increasing Self-Monitoring Kits | +0.5% | National, with early adoption in metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population & Chronic-Disease Burden Elevating Test Volumes

One in five Koreans will be at least 65 years old by late 2025, a demographic turning point that is swelling demand for routine metabolic, cardiovascular, and cancer panels. Diabetes alone represented 11.8% of the national disease burden for men and 8.3% for women in 2024, translating into frequent HbA1c and renal-function monitoring. Hospitals and independent labs are installing high-throughput chemiluminescence and multiplex PCR systems to keep pace with screening volumes. Instrument vendors are bundling reagent contracts that stabilize cash flows for both parties. The South Korea in-vitro diagnostics market therefore links population aging directly to predictable consumable revenue streams.

Universal NHIS Coverage & Screening Mandates Sustaining High Utilisation Rates

NHIS financing shields patients from out-of-pocket shock and supports broad adoption of diagnostic tests across income groups[1]Health Insurance Review & Assessment Service, “Healthcare System in Korea,” hira.or.kr. National screening programs for five major cancers oblige providers to test eligible adults at prescribed intervals, ensuring base-line volumes even during economic downturns. Claims and examination data consolidated within the NHIS database underpin epidemiological studies that guide reimbursement updates and test-menu revisions. Digital health pilots that integrate wearables with insured services are expected to lift uptake of home-based analyzers. As a result, the South Korea in-vitro diagnostics market continues to post stable unit growth irrespective of macro cycles.

Expansion of Private Reference Labs & Consolidated Testing Driving Central-Lab Demand

Independent laboratories process 55% of national test volume, a share built on economies of scale, 24-hour operations, and automated sample logistics. Surveys show two-thirds of facilities maintain biosafety level-2 suites and a median of four PCR platforms, proving readiness for complex panels. Consolidation accelerated during COVID-19 when single sites ran up to 50,000 molecular assays daily. Central labs now channel capital toward digital pathology servers and cloud-native laboratory information systems. Consequently the South Korea in-vitro diagnostics market benefits from lower per-test costs that increase accessibility without eroding margins.

Government & VC Funding for Domestic Biotech/IVD Innovation Clusters

The High-Tech Bio Initiative and parallel local tax incentives channel funding to Seoul, Daejeon, and Incheon, where startups co-locate with research hospitals. Venture rounds target syndromic PCR, lab-on-a-chip, and AI decision-support software. Seegene’s Open Innovation Program granted up to USD 600,000 per project to 26 global teams, accelerating collaborative platform development[2]Seegene Inc., “Open Innovation Program Awardees,” seegene.com. Investors favor business models that pair reagent subscriptions with cloud analytics. Such policy and capital alignment sustains the innovation pipeline feeding the South Korea in-vitro diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement Caps & Price-Volume Agreements Exerting Margin Pressure | -0.6% | National | Medium term (2-4 years) |

| Stringent MFDS Approval Requirements Prolonging Time-to-Market | -0.4% | National | Short term (≤ 2 years) |

| Shortage of Skilled Laboratory Professionals Outside Major Metro Areas | -0.3% | Rural and secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Caps & Price-Volume Agreements Exerting Margin Pressure

HIRA reviews couple fee schedules with quality metrics, while the New Diagnosis-Related Group scheme bundles payments, nudging labs to curb test menus and negotiate volume rebates. Fee-for-service rules still dominate chronic-care pathways, but ceiling prices for popular assays compress supplier margins. As a defence, manufacturers lock in reagent contracts and prioritize high-specificity panels that justify premiums. Sustained cost pressure nonetheless moderates unit revenue growth within the South Korea in-vitro diagnostics market.

Stringent MFDS Approval Requirements Prolonging Time-to-Market

Class III and IV devices require direct MFDS file review, often extending submission cycles beyond 18 months[3]MFDS, “Approval Process – Medical Devices,” mfds.go.kr. The Digital Medical Products Act introduces extra software-validation checkpoints that can delay AI-based analyzers. September 2024 approvals fell to 109, barely 56% of the prior-year monthly average, signalling backlog risk. Smaller innovators divert resources to regulatory consultants, potentially slowing product launches. These requirements, while safeguarding patient safety, dampen the near-term growth trajectory of the South Korea in-vitro diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Reshapes Testing Paradigms

Immuno-diagnostics captured 27.65% of South Korea in-vitro diagnostics market share in 2025, reflecting broad use in hormone, infectious-disease, and auto-immune panels. Molecular diagnostics, buoyed by pandemic investments, is forecast to register 8.85% CAGR to 2031, the fastest among all categories. High multiplexing allows simultaneous detection of up to 14 pathogens, cutting turnaround times and conserving samples. The segment’s momentum is steering bulk-purchase agreements for nucleic-acid reagents that reinforce vendor–lab partnerships. Meanwhile clinical chemistry and hematology retain stable demand for routine liver, kidney, and blood-cell indices, helped by full automation that blends seamlessly with existing laboratory information systems.

Large reference laboratories now reallocate floor space to next-generation sequencers for oncology and rare-disease profiling, broadening the South Korea in-vitro diagnostics market. Cost per run is falling due to reagent-rental schemes that spread capital charges over multi-year contracts. Hospitals increasingly outsource low-margin ELISA panels to focus in-house resources on urgent molecular assays. Vendors are countering sample-to-result complexity with cartridge-based point-of-care PCR that suits emergency departments. As use cases diversify, cross-disciplinary panels blur classic modality boundaries, stimulating integrated platforms that can toggle between chemiluminescence and PCR modes within a single chassis.

By Product: Reagents Fuel Recurring Revenue Streams

Reagents and consumables delivered 74.05% of the South Korea in-vitro diagnostics market size in 2025, validating the razor-and-blade model that underwrites manufacturer profitability. Pandemic-era overstocking of viral-RNA kits has pivoted toward oncology and metabolic strips, sustaining consumable throughput. Price-volume contracts tie multisite chains to single-vendor reagent catalogs, locking predictable cash flows. In contrast, instruments posted a smaller base but are expected to advance at 6.78% CAGR through 2031 on the back of workflow automation, reduced sample volumes, and cloud connectivity.

Laboratories value middleware that funnels data from disparate analyzers into one dashboard, propelling demand for software-as-a-service and interpretation algorithms. Artificial-intelligence companions that flag outliers and suggest reflex testing add clinical value and justify subscription fees. To preserve growth margins, suppliers bundle training, maintenance, and data-security packages, turning one-off sales into annuity-style agreements that reinforce the South Korea in-vitro diagnostics market.

By Application: Oncology Diagnostics Gain Momentum

Infectious-disease assays retained top billing with 34.85% revenue in 2025 as multiplex respiratory panels and antimicrobial-resistance screens remain cornerstones of public-health strategy. Yet oncology diagnostics is slated to grow at 8.18% CAGR, catalysed by aging demographics and government-funded screening drives. Companion diagnostics for targeted therapies are infiltrating formularies, raising both ticket size and clinical significance. Diabetes and cardiology tests also expand steadily, mirroring lifestyle shifts and the rising prevalence of metabolic syndrome and heart failure.

Tumour-marker test kits integrate liquid biopsies with bioinformatics dashboards, enabling stage-zero detection that can cut downstream treatment costs. Personalized genomics panels help oncologists match regimens to mutation signatures, enhancing therapeutic efficacy. This convergence of diagnostics and therapeutics deepens provider reliance on molecular laboratories, further embedding oncology as a growth engine in the South Korea in-vitro diagnostics market.

By End-User: Independent Labs Lead Market Transformation

Independent laboratories accounted for 54.55% of assay volume in 2025, propelled by economies of scale, automated dispatch systems, and 24-hour result cycles. Many sites operate biosafety level-2 suites and maintain separate nucleic-acid extraction rooms, underscoring technical depth. This scale encourages bulk procurement and justifies investment in AI image-analysis servers. Hospital labs, while smaller today, are on track for 6.86% CAGR to 2031 as tertiary centres broaden in-house menus for critical tests and adopt modular analyzers that fit limited bench space.

Academic institutes and contract research organizations sustain biomarker discovery pipelines, often partnering with instrument firms for early-access trials that later spill into clinical menus. Point-of-care deployments and home-testing kits, reinforced by the AI-IoT senior-care project covering 45,000 elders, push diagnostics closer to patients. Such decentralization aligns with community-care legislation and reduces urban–rural disparities, opening fresh niches within the South Korea in-vitro diagnostics market.

Geography Analysis

South Korea’s advanced hospital network and NHIS funding framework guarantee baseline access to laboratory services nationwide. Still, infrastructure is densely clustered around Seoul, Incheon, and Gyeonggi Province, home to most reference labs and specialist staff. Rural counties shoulder higher per-patient expenditure for hypertension and diabetes management, signalling unmet diagnostic capacity. The government’s AI-IoT pilot distributes connected glucometers and vital-sign sensors to older adults, broadening test coverage beyond urban cores.

Domestic production dropped 80.4% in 2024 as COVID-19 kit demand normalised, yet export receipts stayed positive, sustaining a trade surplus. Korean suppliers now target neighbouring ASEAN and Middle-East markets, leveraging cost-competitiveness and rapid-regulatory approval pathways. Conversely, multinationals view Korea as a launch pad for Asia-Pacific digital-health offerings thanks to high 5G penetration and strong e-government infrastructure. Regional growth thus reinforces the South Korea in-vitro diagnostics market while dispersing production risk across broader export channels.

Nationwide community-care legislation obliges municipal clinics to coordinate home visits, transitional care, and diagnostics, pushing volume to portable analyzers. Tele-consult portals that integrate lab results with electronic medical records lessen geographical inequities. Government funding also incentivizes secondary-city bio-clusters, particularly in Daejeon, to attract startups and stem capital flight. Over the forecast period, balanced capacity expansion is expected to narrow urban–rural test-turnaround gaps, improving equity across the South Korea in-vitro diagnostics market.

Competitive Landscape

Global majors such as Abbott, Danaher, and Siemens Healthineers continue to dominate core analyzers, leveraging broad menus and service footprints. Sysmex reported record net sales and operating profit for the nine months ending March 2025, aided by stronger reagent demand in Korea. These firms bundle hardware leasing with reagent contracts, securing long-term share. Domestic champions Seegene, SD Biosensor, and Boditech Med pivoted from pandemic windfalls into multiplex PCR, immunoassay, and point-of-care niches. Seegene’s partnership with Werfen to co-develop technology underscores rising international ambitions.

The MFDS Digital Medical Products Act defines software-as-a-medical-device criteria, prompting alliances between AI startups and established kit makers. Korean reference labs pilot large language models for automated result comments, a use case guided by draft MFDS guidelines on AI devices. Venture-capital firms channel capital into cloud-native middleware vendors that offer open-API connectivity, aligning with laboratory digitization. International entrants must therefore navigate a market where domestic firms have regulatory agility and cultural proximity, yet scale advantages still rest with multinationals. This balanced mix fuels steady innovation within the South Korea in-vitro diagnostics market.

Successful strategies centre on integrated platforms that collapse sample prep, amplification, and detection into sealed cartridges, reducing contamination risk and technician workload. Vendors also differentiate through AI-assisted quality control that flags pre-analytical errors. Consumable pricing remains a battleground as NHIS negotiations compress list prices. Suppliers counter with subscription models that bundle service contracts, software updates, and reagent quotas, sustaining predictable income streams. These models help defend margins while reinforcing customer lock-in across the South Korea in-vitro diagnostics market.

South Korea In Vitro Diagnostics Industry Leaders

Abbott Laboratories

Beckton, Dickinson, and Company

Siemens Healthineers

Danaher Corporation

Thermo Fisher Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AriBio and Fujirebio completed sample acquisition for Alzheimer’s biomarker co-development, aiming to strengthen early detection capacity.

- January 2025: South Korea’s MFDS implemented the Digital Medical Products Act, establishing a formal path for AI-enhanced diagnostics.

South Korea In Vitro Diagnostics Market Report Scope

As per the scope of this report, in vitro diagnostics involves medical devices and consumables utilized to perform in vitro tests on various biological samples. Doctors use them for different medical conditions diagnosis, such as chronic diseases. South Korea's In Vitro Diagnostic Market is segmented by test type (clinical chemistry, molecular diagnostics, immune diagnostics, hematology, and other test types), product (instrument, reagent, and other products), applications (infectious disease, diabetes, cancer/oncology, cardiology, nephrology, and other applications), and end users (diagnostic laboratories, hospitals, and clinics and other end users). The report offers the value in ( USD million) for the above segments.

By Test Type

| Clinical Chemistry |

| Molecular Diagnostics |

| Immuno-Diagnostics |

| Hematology |

| Other Test Types |

By Product

| Instruments |

| Reagents & Consumables |

| Software & Services |

By Application

| Infectious Disease |

| Diabetes |

| Oncology |

| Cardiology |

| Nephrology |

| Other Applications |

By End-User

| Independent Diagnostic Laboratories |

| Hospital-Based Labs & Clinics |

| Academic & CRO Laboratories |

| Other End-Users |

| By Test Type | Clinical Chemistry |

| Molecular Diagnostics | |

| Immuno-Diagnostics | |

| Hematology | |

| Other Test Types | |

| By Product | Instruments |

| Reagents & Consumables | |

| Software & Services | |

| By Application | Infectious Disease |

| Diabetes | |

| Oncology | |

| Cardiology | |

| Nephrology | |

| Other Applications | |

| By End-User | Independent Diagnostic Laboratories |

| Hospital-Based Labs & Clinics | |

| Academic & CRO Laboratories | |

| Other End-Users |

Key Questions Answered in the Report

How large is the South Korea in-vitro diagnostics market in 2026?

It is valued at USD 2.21 billion and is projected to reach USD 2.84 billion by 2031.

Which test type is growing fastest in South Korea?

Molecular diagnostics is forecast to grow at 8.85% CAGR through 2031 on the back of multiplex PCR expansion.

Why do reagents dominate South Korean diagnostic revenues?

Reagents and consumables generate 74.05% of 2025 revenue because recurring purchases follow each instrument placement.

What role do independent labs play in Korea's diagnostic ecosystem?

They process 54.55% of test volume, leveraging automation and scale to deliver rapid, cost-efficient results nationwide.

How will the Digital Medical Products Act affect market entrants?

The Act sets clear approval criteria for AI-driven diagnostics, adding compliance steps but also offering defined pathways for innovative software solutions.

Which application area is expected to advance most quickly?

Oncology diagnostics, supported by aging demographics and precision-medicine adoption, is projected to grow at 8.18% CAGR to 2031.

Page last updated on: