South Korea Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

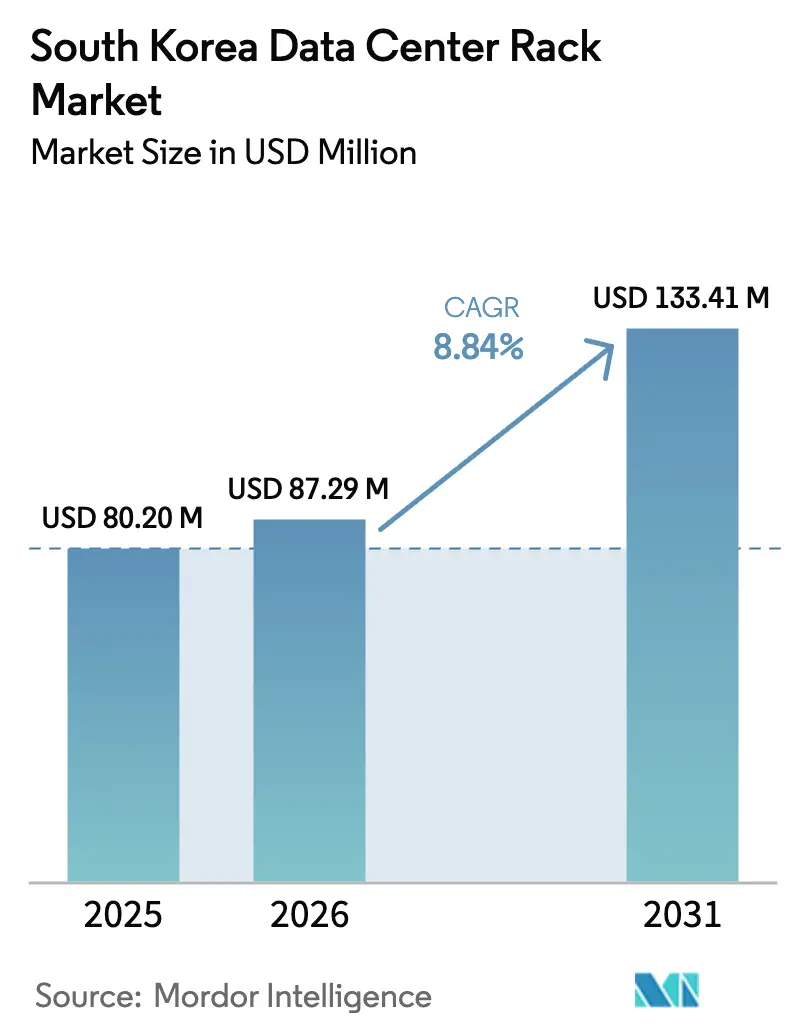

| Base Year Market Size (2025) | USD 80.20 Million |

| Market Size (2026) | USD 87.29 Million |

| Market Size (2031) | USD 133.41 Million |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

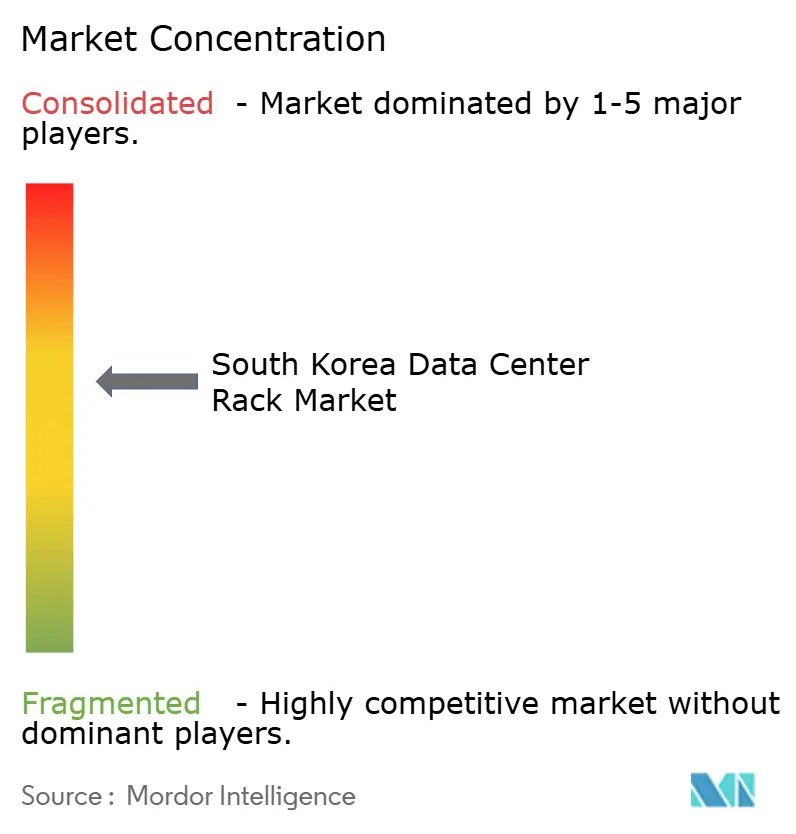

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Data Center Rack Market Analysis by Mordor Intelligence

South Korea Data Center Rack Market size in 2026 is estimated at USD 87.29 million, growing from 2025 value of USD 80.20 million with 2031 projections showing USD 133.41 million, growing at 8.84% CAGR over 2026-2031.

The South Korea data center rack market size stands at USD 62.4 million in 2025 and is projected to advance to USD 128.4 million by 2030, reflecting an 11.24% compound annual growth rate. Investors view the nation as a core Tier 1 location under the AI Diffusion Framework, which grants unrestricted access to advanced AI infrastructure and drives demand for high-density rack solutions csis. Capacity in the Seoul Metropolitan Area alone is forecast to reach 3.2 GW by 2027, a 2.4-fold jump over 2023 and a clear signal that operators need standardized, scalable rack formats.[1]Center for Strategic and International Studies, “Global AI Diffusion Framework,” csis.org Favorable Digital New Deal capital-expenditure incentives, nationwide 5G edge coverage, and strong enterprise adoption of semiconductor and gaming-related AI workloads accelerate rack uptake. Yet headwinds remain from rising industrial power tariffs that range between KRW 97.0 and KRW 234.3 per kWh and from volatility in rack-grade steel prices, both of which compress margins for operators.[2]Korea Electric Power Corporation, “Monthly Electric Tariff Schedule,” kepco.co.kr Competitive intensity is moderate, with Schneider Electric, Rittal, and Delta Electronics battling domestic specialists such as Olabs Technology and Daou Technology for hyperscale, colocation, and emerging edge deployments.

Key Report Takeaways

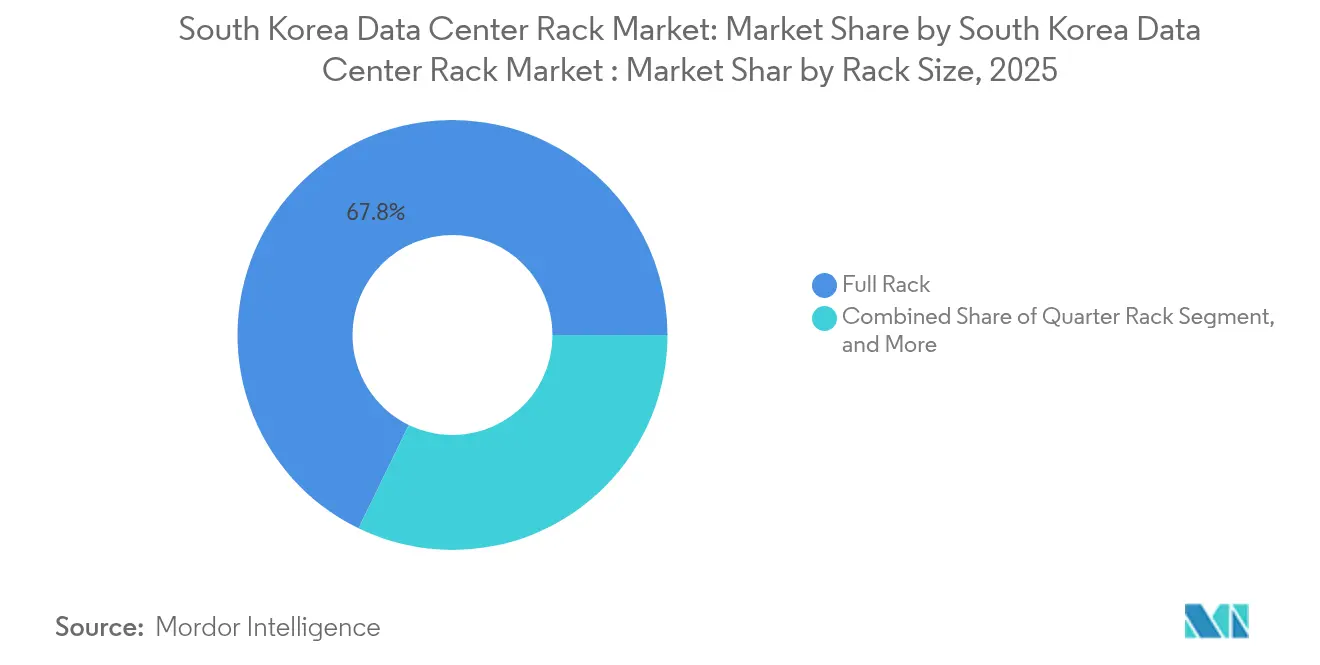

- By rack size, full racks led with 67.80% of South Korea data center rack market share in 2025, while quarter racks recorded the fastest 14.38% CAGR through 2031.

- By rack height, 42U captured 55.05% share of the South Korea data center rack market size in 2025; 48U is expanding at a 12.55% CAGR to 2031.

- By rack type, cabinet (closed) formats accounted for 71.70% revenue share in 2025; wall-mount racks are projected to grow at a 14.05% CAGR by 2031.

- By material, steel held 73.45% share of the South Korea data center rack market size in 2025, whereas aluminum is advancing at a 13.52% CAGR through 2031.

- By data-center type, colocation facilities commanded 53.90% of South Korea data center rack market share in 2025, yet hyperscale builds are rising at a 14.72% CAGR to the end of the decade.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide industry scale is not derived from any single country or region but from the combination of national and regional inputs. The data center rack market size of Mordor Intelligence integrates these into one global valuation.

South Korea Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale and Colocation Build-outs | +2.8% | National, concentrated in Seoul-Gyeonggi corridor | Medium term (2-4 years) |

| Nationwide 5G–Edge Roll-out | +1.9% | National, with early gains in Seoul, Busan, Incheon | Short term (≤ 2 years) |

| Digital New-Deal CAPEX Incentives | +1.5% | National, government-backed initiatives | Medium term (2-4 years) |

| AI/ML Workload Density Surge | +2.1% | National, semiconductor and gaming hubs | Long term (≥ 4 years) |

| New Submarine Cable Landings | +0.8% | Coastal regions, Busan and Incheon priority | Long term (≥ 4 years) |

| Liquid-cooling-ready rack designs | +1.2% | National, sustainability-focused facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscale and colocation build-outs

Financial investors back 90% of the planned 1.9 GW of new capacity scheduled for 2024–2027 in Seoul, reshaping rack demand toward units that support liquid cooling up to 132 kW per rack. Large projects such as Koscom’s KRW 1.4 trillion facility in Anyang due in 2026 exemplify the scale and ESG focus of forthcoming campuses. Power-supply constraints imposed by regulators inside the capital region push operators to adopt distributed architectures, boosting demand for edge-ready and modular racks. Bulk procurement lowers per-unit costs yet locks buyers into standardized footprints, sharpening competition among rack vendors that can pre-integrate intelligent power distribution and in-row cooling.

Nationwide 5G–edge roll-out

Since commercial launch in 2019, more than 162,000 5G base stations now blanket the country, creating low-latency use-cases that require compact, ruggedized rack designs for roadside shelters and micro-cells. KT’s demonstration of terabit-speed backhaul between major cities validates the bandwidth assumptions behind ultra-dense edge nodes kdc. Industrial 5G initiatives in smart manufacturing introduce harsh-environment requirements, pushing rack vendors to adopt corrosion-resistant materials and enhanced cable-management. Edge data-center deployments are forecast to grow at 25% annually across Asia-Pacific, with Korea often positioned as the proving ground due to its urban density and early-adopter culture.

Digital New Deal CAPEX incentives

The Digital New Deal program reimburses qualifying data-center investments that meet energy-efficiency thresholds, enabling projects such as KT Cloud’s 10 MW AI cloud site in Gyeongbuk with plans to scale past 320 MW by 2030. Incentives prioritize racks that integrate intelligent PDUs, airflow containment, and sensor-driven thermal management. Procurement guidelines favour suppliers that certify low embodied carbon, which is driving rapid adoption of aluminum and green-steel options. The framework also funds 6G testbeds, stimulating early demand for racks capable of hosting next-generation radios and terabit switching fabrics.

AI/ML workload density surge

Samsung’s USD 55 billion R&D pledge and USD 45 billion infrastructure commitment toward a 7.7-million-wafer mega-cluster intensify the need for AI training capacity. Gaming studios adopting AI-powered graphics generate 26-36% annual rises in server power draw, prompting rack designs that pair liquid cooling plates with front-serviceable manifold blocks. Schneider Electric’s joint reference designs with Nvidia illustrate how 132 kW per rack becomes the new norm in flagship facilities. ESG reporting rules effective 2026 add further pressure to prove measurable gains in power-usage effectiveness, making high-density yet efficient racks a competitive necessity.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Electricity Tariffs | -1.8% | National, industrial rate increases | Short term (≤ 2 years) |

| Rack-grade Steel Supply Volatility | -1.2% | National, import dependency | Medium term (2-4 years) |

| Stringent Seismic-Proof Design Codes | -0.9% | National, enhanced safety standards | Long term (≥ 4 years) |

| Limited Availability of RE-100 PPAs | -0.7% | National, renewable energy constraints | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating electricity tariffs

Korea Electric Power Corporation’s debt of KRW 202.5 trillion forces regular tariff hikes, raising industrial rates to as high as KRW 234.3 per kWh. Fossil fuels still produce 58.5% of electricity, leaving operators exposed to LNG volatility. Builders now specify racks with granular branch-circuit monitoring and airflow containment to squeeze every watt from cooling budgets. Examples include Digital Realty’s ICN10 site, which records a PUE of 1.3-1.4 via chilled-water rear-door heat exchangers integrated directly into locked cabinets. The slower progress toward renewable energy targets further tightens margins, making energy-efficient racks a procurement prerequisite.

Rack-grade steel supply volatility

World steel prices remain unstable amid trade tensions, with forecasters warning of 20% spikes in construction inputs under renewed tariffs. Rack builders relying on imported coil must hedge against both currency swings and freight delays. Iron-ore benchmarks are expected to drop in 2025 and 2026, encouraging cautious inventory planning ttiinc. Green-steel offerings commanded 15% of supply in 2023 and carry a premium that many Korean buyers will bear to satisfy ESG mandates. Aluminum and composite frames gain appeal despite higher upfront cost because they insulate buyers from steel volatility while boosting thermal performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full rack dominance drives standardization

Full racks generated 67.80% of revenue in 2025, a position that underscores hyperscale preferences for uniform, high-density aisles in Seoul’s multistory campuses. This leadership equates to the largest slice of South Korea data center rack market share and reinforces the economies of bulk procurement. Demand accelerates as operators adopt liquid cooling manifolds rated beyond 100 kW. In contrast, quarter racks log the fastest 14.38% CAGR as edge colocation and enterprise branches value modular capacity expansions. Retail colocation suites and distributed telco huts often default to two quarter racks instead of one full unit to optimize power feeds. The South Korea data center rack market continues to split along these form factors, yet vendors increasingly design chassis that let customers bolt quarter racks into unified frames when density demands shift.

Edge growth is particularly evident in Busan and Incheon, where submarine cable landings necessitate micro-data centers within port facilities. Operators there favor quarter racks fitted with side-mounted heat pipes because floor space commands a premium. Meanwhile, bespoke research labs in Gyeonggi retain specialized half-rack footprints that allow rapid hardware swaps during chip-validation cycles. As Korea regulates power additions inside Seoul, many landlords retrofit existing facilities with shorter rows of quarter and half racks to meet electrical quotas without structural upgrades. Such trends embed flexibility into the roadmap of the South Korea data center rack market.

By Rack Height: 42U standard meets emerging 48U demand

The 42U format held 55.05% revenue in 2025, reflecting decades of entrenched compatibility with enterprise gear. Many colocation providers continue to bundle 42U cabinets with fixed cross-connect packages, securing predictable lead times. Yet AI training clusters now require extra vertical space for rear-door heat exchangers and GPU sleds, propelling the 48U category at a 12.55% CAGR. That uplift means the 48U slice of South Korea data center rack market size could challenge 42U dominance by the decade’s end as operators retrofit white space for taller doors and higher cable ducts. Facilities with raised floors taller than one meter are the earliest adopters because they already budget for heavier loads.

Higher racks also offset power-delivery constraints by allowing more SMR batteries and busbars per cabinet, spreading heat across a longer chimney. Vendors therefore reinforce frames with seismic bracing to pass Korea’s upgraded structural codes, which add 50% extra load factors for facilities over 1,000 ㎡. Liquid cooling innovators integrate sliding manifolds that remain serviceable even at 48U heights, ensuring field engineers can replace cold plates without mechanical lifts. These innovations keep the South Korea data center rack market from fragmenting by height, instead encouraging interoperability between 42U and 48U rails and blanking panels.

By Rack Type: Cabinet racks lead security-focused market

Cabinet enclosures captured 71.70% revenue in 2025 because Korean corporate policy prioritizes physical security and acoustic containment in densely populated buildings. Standard cabinets simplify airflow containment solutions such as hot-aisle chimneys mandated by many colocation SLAs. Wall-mount units, however, accelerate at 14.05% CAGR due to rapid edge deployment in retail and transportation hubs. Their shallow depth suits shallow service corridors, while lockable front doors deter vandalism in publicly accessible areas. Open-frame racks persist in test labs and staging zones where technicians value unrestricted access, yet they seldom make it into production halls.

Cabinets increasingly ship with factory-installed high-density busbars and DC rectifiers, enabling brownfield halls to accommodate up to 30 kW without rewiring. Wall-mount designs adopt swing-out hinges for quick fiber management when technicians shoulder cramped equipment closets. Korean telcos specify wall-mounts for 5G edge pods located on building rooftops because enclosed sides resist weather ingress. Those patterns drive steady diversification inside the South Korea data center rack market, though cabinets remain the default solution wherever building codes and landlord insurance clauses demand locked enclosures.

By Data Center Type: Colocation stability versus hyperscale growth

Colocation operators delivered 53.90% of rack demand in 2025 and continue to offer predictable baseline volume. These providers bundle rack, power, and interconnection on multiyear contracts that attract domestic content-delivery, fintech, and gaming tenants. Yet hyperscale investment rises at a 14.72% CAGR as cloud majors and AI start-ups secure entire build-to-suit halls. Hyperscalers prefer pre-certified reference designs, allowing vendors to lock in thousands of identical cabinets before slab pour. Such volume tilts the South Korea data center rack market toward vendors with capital to hold inventory and absorb foreign-exchange swings.

Enterprises constrained by capital budgets still opt for colocation suites, preserving a diversified buyer base. Meanwhile, government decentralization policies encourage regional municipalities to invite midsize colocation builds, which indirectly stimulate local rack assembly plants. Edge data centers attached to 5G macro towers represent a smaller but quickly growing customer tier, typically ordering wall-mount or quarter-rack formats to fit shipping-container envelopes. Each data-center archetype therefore injects varied but complementary demand streams that collectively stabilize revenue for manufacturers.

By Material: Steel dominance faces aluminum challenge

Steel frames remain the bedrock of the South Korea data center rack market, accounting for 73.45% revenue in 2025 thanks to their load-bearing strength and competitive cost. Domestic fabricators source welded sheet and angle profiles from Pohang and Gwangyang mills, keeping lead times short. However, aluminum posts a 13.52% CAGR as buyers value its 205 W m·K thermal conductivity which dissipates heat faster in high-density AI enclosures. Aluminum also reduces per-cabinet weight by up to 40%, easing installation on raised floors with seismic bracing.

Price volatility in steel imports, amplified by trade frictions, nudges some buyers toward aluminum despite its higher sticker price. Green-steel premiums further narrow the cost gap, making lightweight alloys financially viable under ESG procurement mandates. Composite racks that sandwich carbon fiber between aluminum skins appear in semiconductor research labs where electromagnetic cleanliness matters. These shifts diversify the procurement palette but steel’s entrenched supply chains and lower material costs ensure it retains the majority share for the foreseeable future.

Geography Analysis

Seoul and its satellite cities command roughly 60% of operational white space and 70% of data-center power draw, making the capital region the gravitational center of the South Korea data center rack market. Planned additions could lift installed capacity to 3.2 GW by 2027, more than doubling the 2023 baseline. The concentration of campuses allows operators to negotiate bulk rack discounts and rely on established logistics lanes from Incheon port. Yet the government’s moratorium on new heavy-load power permits inside Seoul imposes a hard ceiling, compelling builders to maximize compute per kW through taller and denser cabinets. Seismic building codes force 50% higher structural allowances on white space over 1,000 m, prompting rack makers to reinforce frames and anchor kits for multi-story sites.

Coastal hubs such as Busan and Incheon capitalize on submarine cable landings that shorten round-trip latency to Japan, Singapore, and the United States. Edge-oriented micro-facilities in these ports specify wall-mount or quarter-rack solutions that fit within converted warehouse footprints. Nationwide 5G coverage funnels traffic to these coastal nodes first, making them early beneficiaries of AI-driven content distribution. Aluminum racks gain traction here because lower weight expedites crane lifts during rapid build-outs on pier infrastructure.

Interior provinces like Gyeonggi and Gyeongbuk are emerging beneficiaries of decentralization incentives embedded in the Digital New Deal. KT Cloud’s 10 MW anchor facility in Gyeongbuk, expandable to 320 MW, signals a pivot toward cheaper land and abundant renewable-energy potential. Samsung’s semiconductor mega-cluster in Gyeonggi injects localized demand for AI training labs that favor 48U high-density racks with liquid cooling manifolds. These inland builds diversify revenue streams for rack assemblers and temper geographic concentration risk within the South Korea data center rack market.

Mordor Intelligence tracks the data center rack market across other major regions such as Africa, Middle East, and South America, with additional country-level coverage spanning Japan, New Zealand, South Africa, Saudi Arabia, Brazil, and Spain, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

International conglomerates and agile domestic specialists share a moderately concentrated playing field. Schneider Electric deploys global R&D resources to pre-engineer cabinet ecosystems that integrate 132 kW liquid cooling coils, capturing early mindshare among hyperscalers. Rittal tailors its VX series with seismic-grade frames suited to Korean building codes, while Delta Electronics integrates high-efficiency rectifiers that align with tariff-driven energy-savings targets. These brands bundle racks with power and cooling, leveraging economies of scope.

Local manufacturers such as Olabs Technology, Dobe Computing, and Daou Technology exploit short order-to-delivery cycles and fluent understanding of regulatory paperwork. Their proximity to Seoul logistics corridors allows rapid customization, for instance adding Korean-language smart-PDU firmware ahead of factory site acceptance tests. Domestic firms also adapt more quickly to evolving ESG disclosure formats required by the Financial Supervisory Service, offering green-steel or recycled-aluminum options certified by local labs.

Strategic partnerships dominate recent announcements. Schneider Electric and Nvidia produce turnkey rack references that embed AI network fabrics, while Vertiv’s 360AI platform offers modular cooling skids that slot directly into existing aisles datacenterfrontier.[3]Data Center Frontier, “Vertiv 360AI Platform Debuts,” datacenterfrontier.com NTT DATA pairs private-5G service bundles with Schneider’s EcoStruxure modular data centers to capture edge business. Over the next five years, suppliers able to certify racks for liquid cooling, seismic resilience, and energy-usage transparency are expected to gain share inside the South Korea data center rack market.

South Korea Data Center Rack Industry Leaders

Schneider Electric

Rittal

Delta Electronics

Eaton

Huawei

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Schneider Electric opened new data-center and microgrid testing laboratories at its Global R&D Center in Massachusetts, investing €2.26 billion in R&D infrastructure.

- December 2024: Schneider Electric partnered with Nvidia to develop AI data-center reference designs supporting liquid cooling up to 132 kW per rack

- May 2024: Vertiv launched the 360AI platform to streamline AI infrastructure deployment with modular cooling strategies.

- March 2024: NTT DATA and Schneider Electric initiated a co-innovation partnership to integrate edge, private 5G, IoT, and modular-data-center offerings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korean data-center rack market as factory-built enclosures (principally 19-inch steel or aluminum frames) that house servers, networking gear, power distribution, and related cable management inside purpose-built data centers. The valuation captures new rack hardware revenue booked by OEMs and system integrators when racks are shipped into colocation, hyperscale, enterprise, and edge facilities during the calendar year.

Scope exclusion: second-hand racks, rail-kit accessories, integrated PDUs, cooling doors, and any revenue from installation labor fall outside this coverage.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights (?52U and Custom)

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed rack engineers, colocation capacity planners, hyperscale procurement managers, and local installers across Seoul, Busan, and Incheon. These conversations validated density road maps, typical ASP erosion, adoption of 48U formats, and the shift toward liquid-ready cabinets, helping us refine assumptions that literature alone cannot surface.

Desk Research

We began by assembling time-series indicators from open sources such as the Korean Statistical Information Service on ICT building completions, Ministry of Science & ICT data on hyperscale power permits, Korea Customs Service import codes for HS-940320, and trade association briefs from the Korea Data Center Council. Company 10-Ks, investor decks, and selected news archives inside Dow Jones Factiva supplemented facility-level CAPEX and rack mix disclosures. To benchmark pricing and material shifts, analysts pulled steel coil indices from Korea Iron & Steel Association, patent trends through Questel, and public procurement notices listing rack specifications. These diverse records give a factual spine, yet they are illustrative only; many further publications were reviewed for corroboration and gap filling.

Market-Sizing & Forecasting

A top-down construct converts installed and planned IT power (MW) into rack counts by applying primary-validated density ratios, which are then multiplied by annual average selling prices to obtain value. Bottom-up checks sampled supplier shipments and channel price lists are overlaid to reconcile totals. Key variables include hyperscale CAPEX pipelines, rack-height mix, domestic steel cost index, 5G traffic growth, and RE-100 PPA availability; each feeds a multivariate regression that projects demand through 2030. Where bottom-up evidence is thin, utilization curves from comparable facilities are imputed before final convergence.

Data Validation & Update Cycle

Mordor analysts run deviation scans against customs tallies and power-on-site trackers, rerouting oddities for peer review. Reports refresh every twelve months, with rapid interim updates if a material event, such as a 300 MW campus announcement, alters the baseline.

Why Mordor's South Korea Data Center Rack Baseline Commands Confidence

Published numbers often diverge because firms pick dissimilar rack definitions, pricing pools, or refresh cadences. According to Mordor Intelligence, variation also stems from whether analysts net out accessories, how they treat hyperscale internal transfers, and the year chosen as "current."

Key gap drivers include some publishers bundling integrated PDUs and containment, others applying global ASPs to local volumes, and a few projecting forward from 2021 data without updating for the 2024 power-tariff jump.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 80.2 mn (2025) | Mordor Intelligence | - |

| USD 66.5 mn (2023) | Global Consultancy A | Older base year and narrower Seoul-only scope |

| USD 152.0 mn (2024) | Regional Consultancy B | Bundles rack PDUs and cold-aisle containment |

| USD 680.0 mn (2024) | Trade Journal C | Aggregates all mechanical infrastructure, not stand-alone racks |

The comparison shows that once accessory revenue and non-rack hardware are stripped out, and 2025 demand is applied, Mordor's disciplined, annually refreshed approach yields a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the South Korea data center rack market?

The market is valued at USD 87.29 million in 2026 and is set to reach USD 133.41 million by 2031 at an 8.84% CAGR.

Which rack format holds the largest share?

Full racks dominate with a 67.80% share in 2025 owing to hyperscale and colocation standardization.

Why are 48U racks gaining popularity?

AI and high-performance workloads need extra space for liquid-cooling hardware and power distribution, driving a 12.55% CAGR for 48U cabinets.

How are rising electricity tariffs affecting rack design?

Higher power costs push operators toward cabinets with intelligent PDUs, airflow containment, and materials that dissipate heat more efficiently.

Page last updated on: