Technology, Media and Telecom

5th MayAccelerating Additive Manufacturing Adoption in India

3 Min Read

South Korean Data Center Physical Security Market Report is Segmented Into Component (Solution Type, Service Type), Data-Center Tier(Tier I and II, Tier III, Tier IV), Data Center Type(Hyperscaler, Colocation, Enterprise, and Edge Data Center). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

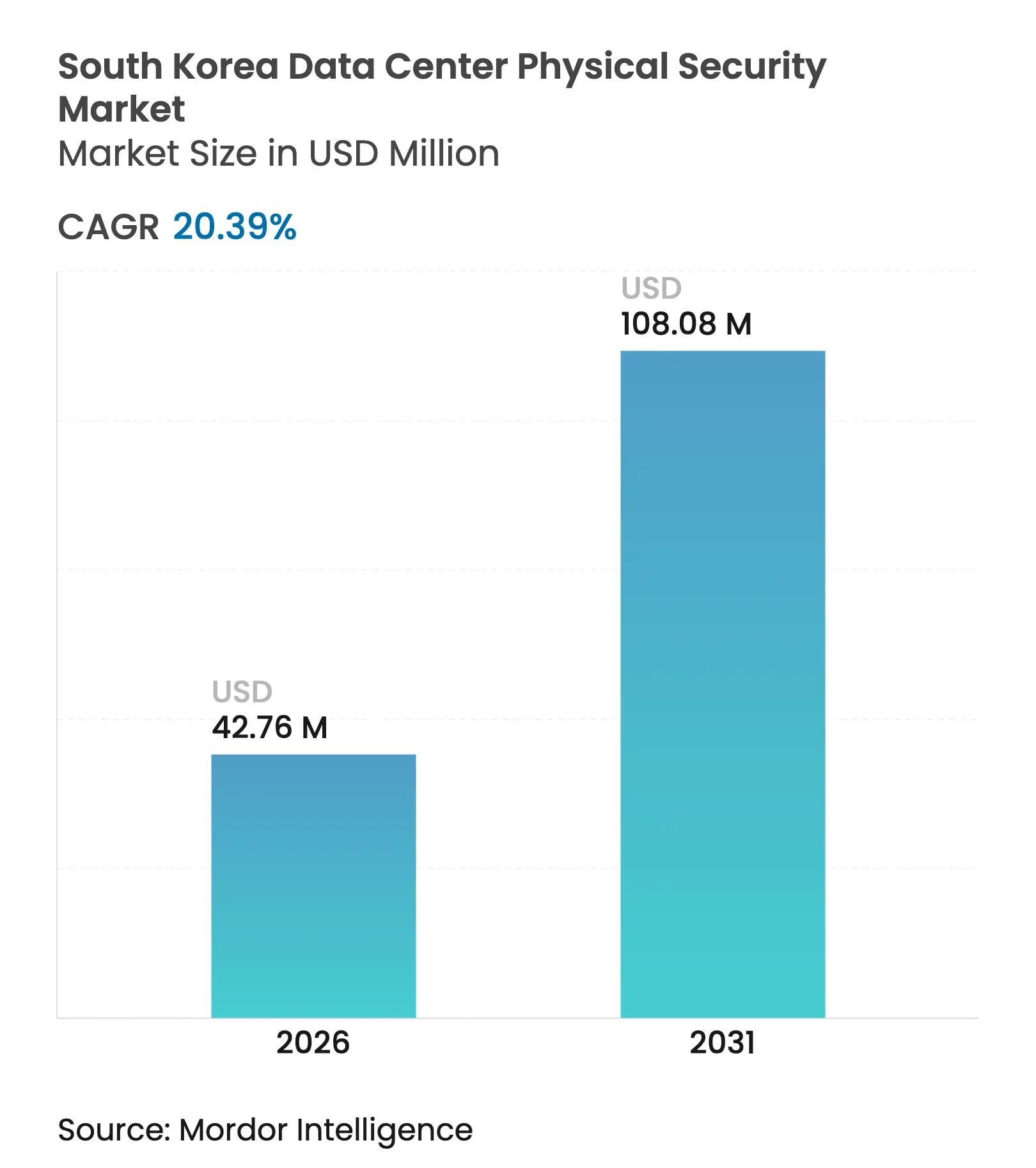

| Market Size (2026) | USD 42.76 Million |

| Market Size (2031) | USD 108.08 Million |

| Growth Rate (2026 - 2031) | 20.39 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The South Korea data center physical security market size was valued at USD 35.52 million in 2025 and estimated to grow from USD 42.76 million in 2026 to reach USD 108.08 million by 2031, at a CAGR of 20.39% during the forecast period (2026-2031). Surging hyperscale construction, stricter post-incident fire-safety mandates and the government’s multi-billion-dollar AI infrastructure push are accelerating capital outlays on biometric access control, AI-enabled surveillance and Tier IV-grade perimeter protection. Consolidation of cloud and AI workloads inside megawatt-scale campuses is widening the threat surface, motivating operators to adopt unified platforms that fuse environmental, access and video analytics into one command layer. Private 5G roll-outs and edge computing programs further amplify demand for secure micro-facilities, while ESG reporting requirements move resilient physical protection from a cost center to a board-level performance metric.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing data traffic and need for secure connectivity Increasing data traffic and need for secure connectivity | +4.2% | National, concentrated in Seoul Capital Area | Medium term (2-4 years) | % Impact on CAGR Forecast :+4.2% | Geographic Relevance :National, concentrated in Seoul Capital Area | Impact Timeline :Medium term (2-4 years) |

Rise in cyber threats Rise in cyber threats | +3.8% | National, with focus on critical infrastructure | Short term (≤ 2 years) | |||

Surge in hyperscale and colocation investments Surge in hyperscale and colocation investments | +5.1% | Regional hubs in Seoul, Busan, Ulsan | Long term (≥ 4 years) | |||

Mandatory CCTV-storage compliance under PIPA Mandatory CCTV-storage compliance under PIPA | +2.9% | National regulatory requirement | Short term (≤ 2 years) | |||

ESG-driven demand for resilient infrastructure ESG-driven demand for resilient infrastructure | +2.4% | Corporate facilities nationwide | Medium term (2-4 years) | |||

Government grants for 5G edge data-center roll-outs Government grants for 5G edge data-center roll-outs | +2.7% | Strategic locations for 5G deployment | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Data-Traffic Surge and Secure Connectivity

Daily domestic data flows reached multi-terabit levels as AI inference, video streaming and private 5G networks intersect, turning latency-sensitive workloads into mission-critical assets.[1]U.S. Department of Commerce, “Cybersecurity Snapshot for the Republic of Korea,” commerce.gov The U.S. Department of Commerce estimates South Korean systems face more than 1.2 million hacking attempts every day, a trend pushing operators to unify physical and logical defenses. Naver’s private 5G construction program shows how edge nodes now embed hardened cages, vibration-resistant racks and on-device analytics to maintain service continuity. Samsung’s announced pursuit of advanced HVAC controls underscores the linkage between environmental management and physical protection in high-density halls. Ministry of Science and ICT 5G spectrum allocations to over 30 enterprises deepen the lattice of micro-facilities that require remote-managed locks and tamper-proof enclosures. Together these elements raise baseline investment in the South Korea data center physical security market.

Rise in Hybrid Cyber Threats

Specialized cyber units targeting the peninsula increasingly pair digital exploits with on-site intrusion to bypass segmented networks, compelling facilities to harden first-layer perimeters. The Korean National Police Agency’s deepfake-detection toolkit adoption signals elevated concern around AI-driven impersonation at security checkpoints.[2]Korean National Police Agency, “AI Deepfake Detection Initiative,” police.go.kr Financial institutions’ recent blocking of foreign generative-AI services over data-sovereignty worries has accelerated biometric deployment to validate every individual entering vault areas. The National Intelligence Service continues to warn of exfiltration campaigns leveraging compromised smart-building systems, prompting operators to mandate redundant physical-layer monitoring. These dynamics infuse an additional 3.8% CAGR lift into the South Korea data center physical security market.

Surge in Hyperscale and Colocation Build-outs

More than USD 39 billion in confirmed field projects—including SK Telecom and AWS’s 103-MW Ulsan campus—are reshaping design templates toward multi-gigawatt estates that function like critical-national infrastructure.[3]SK Telecom, “Building the Nation’s Largest AI Data Center in Ulsan,” sktelecom.com Facilities crossing the 100-MW threshold now require concentric fencing, long-range thermal cameras and blast-rated access portals, raising average security spend per MW. Government clearance for a 3-GW hyperscale park in Jeollanam-do transforms a rural province into a multi-site security zone with shared emergency-response protocols. Colocation incumbents reply by elevating sites to ISO 27001 and Tier IV standards, inserting biometric portals and automated incident-response bots to retain hyperscale tenants. These build-outs add about 5.1% to projected CAGR for the South Korea data center physical security market.

Mandatory CCTV-Storage Compliance Under PIPA

Following the 2022 data-center fire, amendments to the Personal Information Protection Act (PIPA) require video evidence retention and tamper-evident storage, catalyzing upgrades to on-premises storage arrays, hardened DVR vaults and secure log-management software. Operators installing AI analytics must now provide audit trails that map every face, time stamp and entry zone, pushing demand for scalable object-storage clusters inside secure rooms. Regulatory audits levy steep fines for gaps, prompting even SME facilities to adopt enterprise-class recording and encrypted off-site replication. Large integrators report a 20% jump in compliance-driven retrofit projects since 2024, solidifying a 2.9% contribution to overall growth in the South Korea data center physical security market.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited IT budgets and low-cost substitutes Limited IT budgets and low-cost substitutes | -2.8% | SME data centers nationwide | Short term (≤ 2 years) | (~)% Impact on CAGR Forecast:-2.8% | Geographic Relevance :SME data centers nationwide | Impact Timeline :Short term (≤ 2 years) |

High upfront cost of multi-factor access control High upfront cost of multi-factor access control | -3.2% | Tier III/IV facilities | Medium term (2-4 years) | |||

Shortage of skilled physical-security integrators Shortage of skilled physical-security integrators | -2.1% | Technical integration projects | Long term (≥ 4 years) | |||

Public resistance to facial-recognition solutions Public resistance to facial-recognition solutions | -1.9% | Public-facing facilities | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited IT Budgets and Low-Cost Substitutes

Many mid-tier operators still allocate less than 10% of capital budgets to security, prompting reliance on commodity cameras and keypad locks that underperform against evolving threats. A leading national daily documented a 90 billion-won AI data center operating at half capacity because planned physical safeguards were pared back during construction. Smaller sites increasingly outsource protection through security-as-a-service models, but dependence on external monitoring firms creates onboarding delays and contract-lock risks. Influx of inexpensive hardware from overseas vendors further suppresses price ceilings, yet introduces supply-chain assurance challenges that drive up total cost of ownership. Budget tension is expected to shave 2.8% off the potential CAGR of the South Korea data center physical security market.

High Upfront Cost of Multi-Factor Access Control

Deploying mantraps, biometric scanners, and layered authentication can exceed USD 60,000 per entry point, a figure that double-counts once civil-works upgrades and redundancy requirements are included. Suprema’s flagship BioStation 3 terminals improve throughput but still need networking, power, and HVAC adjustments to maintain fingerprint and facial-matching accuracy. Integrators note that return on investment becomes compelling only for facilities at or above 10 MW, leaving legacy server rooms reliant on single-factor systems. Smartphone-based biometrics alleviate some hardware cost, yet concerns around mobile malware slow adoption among financial services tenants. These barriers trim roughly 3.2% from the attainable growth of the South Korea data center physical security market.

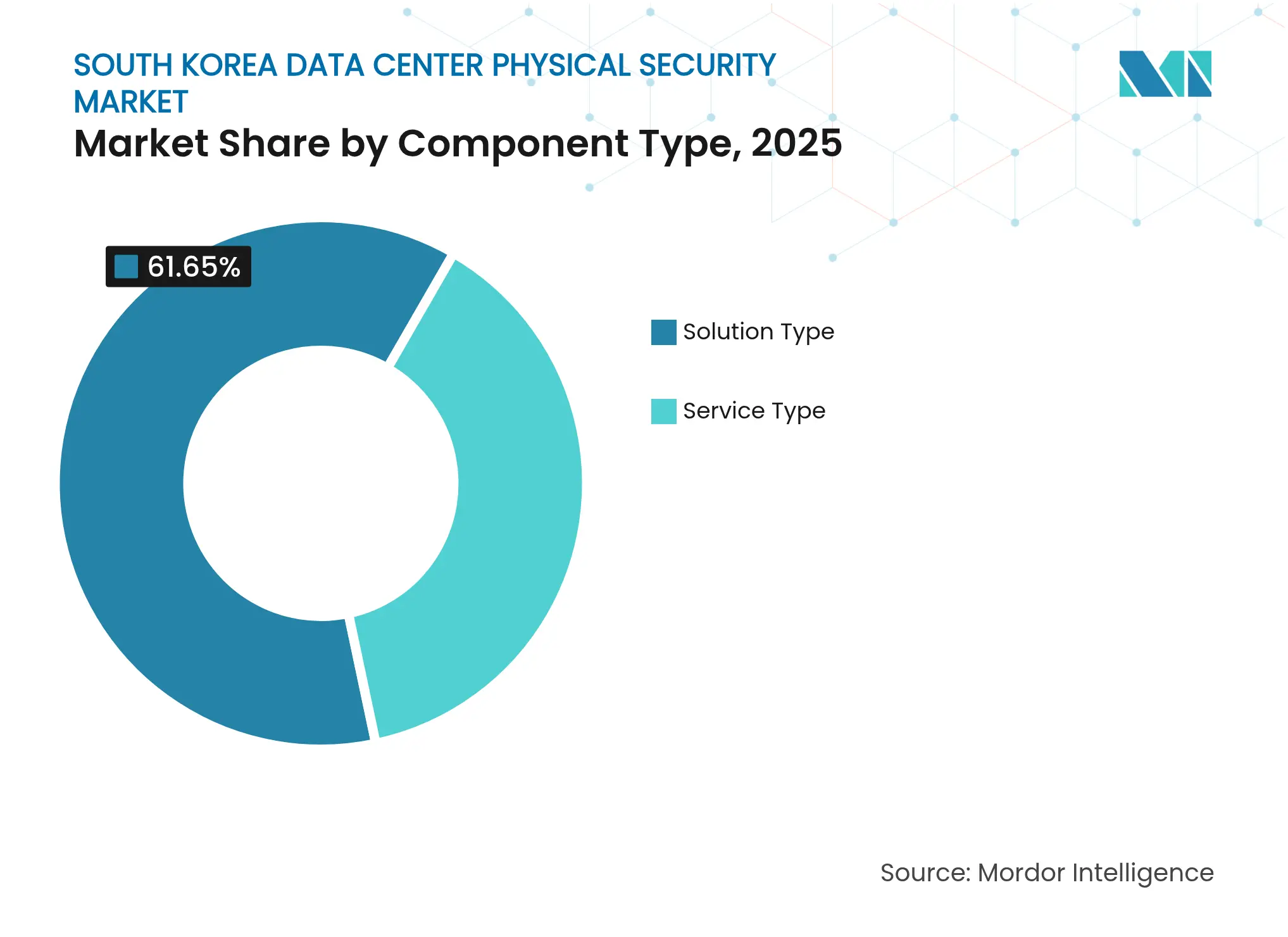

By Component: Solutions Dominate as Services Accelerate

Solution offerings held 61.65% revenue in 2025, confirming that cameras, biometric portals and fire-suppression gear are foundational purchases in every South Korea data center physical security market deployment. AI-enabled video surveillance leads volume, with Hanwha Vision’s Wisenet lineup powering real-time object classification and perimeter breach alerts inside Tier III white spaces . Access-control sub-spend is shifting toward multimodal recognition—iris, vein and facial match—at cage and cabinet level to satisfy audit requirements for multi-tenant operators. Intrusion detection sensors now integrate vibration analysis, radar and lidar to minimize false alerts during 24/7 maintenance cycles. Environmental and fire-safety solutions increasingly rely on aspirating-smoke detection that samples air in high-density aisles, halving alarm latency compared with legacy point detectors.

Service revenue is smaller today yet is forecast to rise 21.74% CAGR through 2031 as operators outsource system health checks, firmware patching and compliance reporting. Consulting teams design multi-layered defenses bridging physical and logical domains so that a badge swipe automatically triggers privilege escalation monitoring. Integration projects dominate hyperscale build-outs because proprietary camera firmware, AI analytics and building-management systems must converge under a single dashboard. Managed-security contracts bundle 24/7 monitoring, predictive maintenance and quarterly penetration testing into pay-as-you-grow models, a trajectory that adds fresh annuity streams to the South Korea data center physical security industry.

Note: Segment shares of all individual segments available upon report purchase

By Data-Center Tier: Tier IV Upgrades Drive Premium Adoption

Tier III sites represented 56.70% of the South Korea data center physical security market size in 2025 thanks to their balanced redundancy profile and favorable capital-to-revenue ratios. Operators routinely install N+1 power, chilled-water loops and dual-feed fiber, demanding concurrent maintainability from door controllers, CCTV arrays and networked fire panels. Redundant security appliances ensure badge verification, video recording and alarm signaling continue during maintenance windows, safeguarding uptime commitments.

Tier IV deployments, while numerically fewer, are set to expand at 21.22% CAGR through 2031 as AI model-training clusters require 99.995% availability. Each operational zone—generation hall, battery room, white space, carrier meet-me area—runs isolated biometric checkpoints to confine blast radius if a breach occurs. Parallel video networks stream to geographically distant command centers for disaster-recovery compliance, a mandatory feature since the Kakao outage. Operators also fit armored walls and seismic dampers to protect GPU pods valued at millions of USD per rack. As these investments accelerate, Tier IV will claim a larger slice of the South Korea data center physical security market.

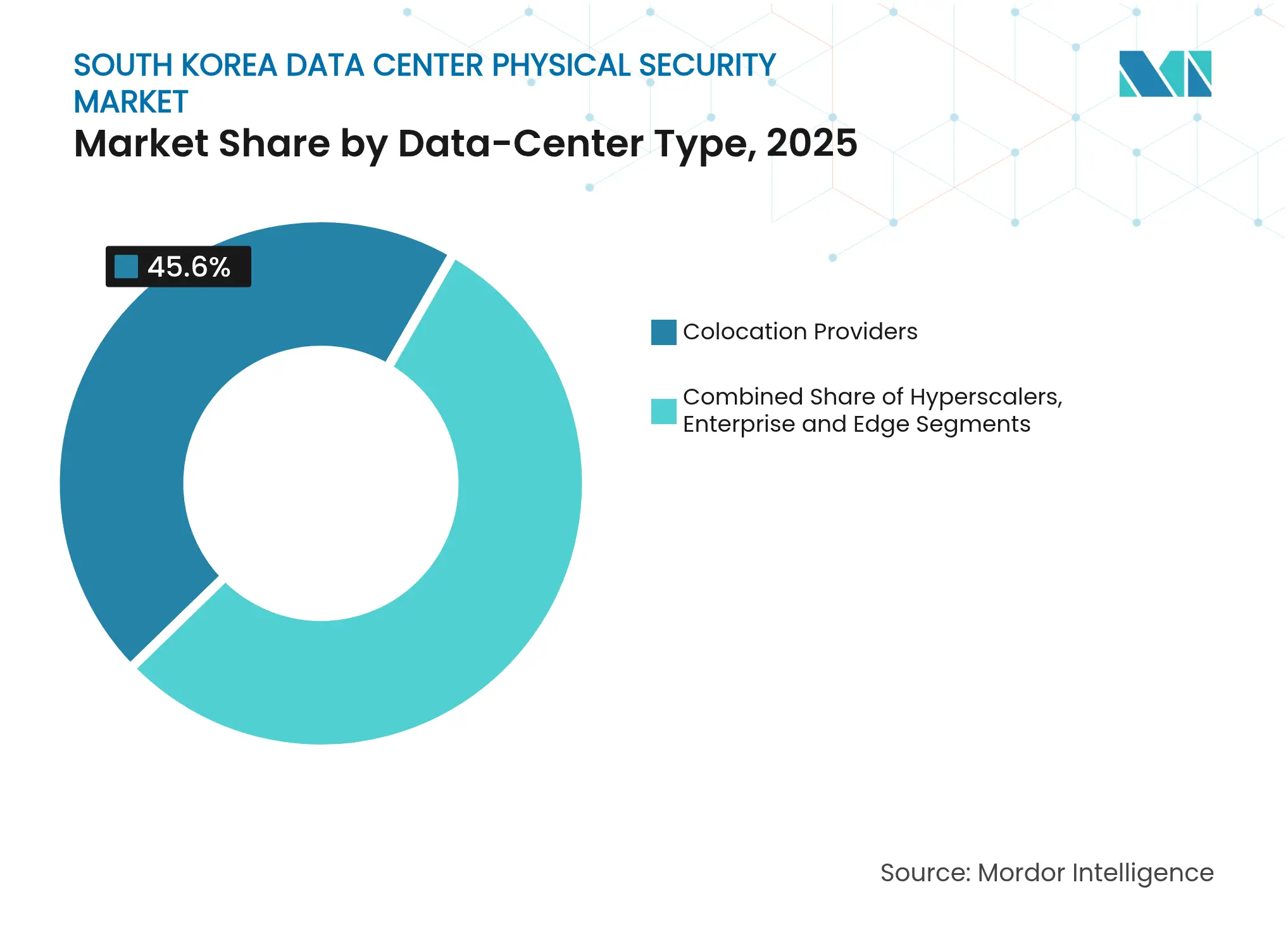

By Data-Center Type: Hyperscalers Reshape Requirements

Colocation operators captured 45.60% revenue share in 2025, leveraging shared security infrastructure to lower total cost for hundreds of tenants. Visitor management kiosks issue color-coded badges that gate access to elevator banks, cold corridors and carrier rooms, while real-time dashboards furnish audit logs for SOC 2 and ISO 27001 filings. These firms purchase high-throughput X-ray scanners and thermal cameras at dock doors to control the constant flow of customer gear, demonstrating economies of scale intrinsic to multi-tenant estates.

Hyperscalers are the fastest-growing group, advancing at 23.86% CAGR as global cloud brands localize AI training and sovereign-cloud regions. A single 100-MW campus can spend USD 25 million on physical security alone, covering drone detection, radar-augmented fences and fully redundant command centers. Cloud operators prefer proprietary standards that often exceed industry norms, compelling vendors to co-innovate on zero-trust physical access and predictive maintenance analytics. Enterprise and edge data centers remain important for latency-sensitive workloads, yet they increasingly interconnect to hyperscale hubs for resiliency, pushing uniform security benchmarks across the ecosystem.

Note: Segment shares of all individual segments available upon report purchase

South Korea’s data-center footprint concentrates around the Seoul Capital Area, where carrier density, skilled labor and enterprise proximity create a security-rich environment spanning dozens of Tier III halls. Operators apply shared threat-intelligence workflows that pool incident data, enabling faster pattern recognition and coordinated law-enforcement escalation. These inter-site synergies reinforce purchasing power for bulk-buy of biometric terminals and high-definition cameras, anchoring the largest slice of the South Korea data center physical security market.

A second growth front is forming in southeastern industrial corridors linking Ulsan and Busan, where energy-infrastructure adjacency provides cost-effective power and chilled-water access. The Ulsan AI campus integrates LNG-fed turbines with on-site security command hubs, illustrating how industrial synergies offset remote-location risks. Busan’s port connectivity invites submarine-cable landings, extending physical security requirements to cable landing stations and marine perimeters. Regional governments provide tax incentives that ease capital flows into hardened shell constructions and reinforced entrance vestibules.

Jeollanam-do’s planned 3-GW mega-campus accelerates decentralization, compelling integrators to design nationwide security fabrics that federate access management across multiple provinces. Edge nodes tied to smart-city projects in Songdo and Suwon extend protection to traffic controls and public-safety IoT devices, blurring lines between critical-infrastructure and data-center security. Maritime routes connecting South Korea to global Internet backbones introduce undersea-cable vulnerability, prompting operators to coordinate with coast-guard units and deploy vibration sensors along beach manholes. Collectively these dynamics sustain double-digit growth across all regions within the South Korea data center physical security market.

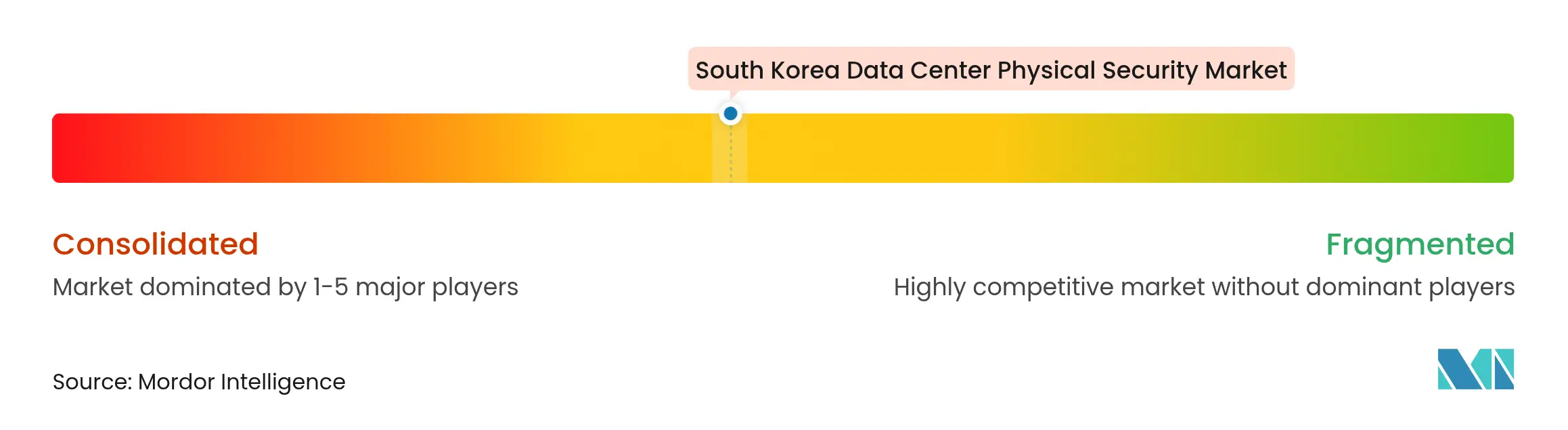

Market Concentration

Global camera giants and domestic specialists share a moderately fragmented arena where the top five vendors account for roughly 45% aggregate revenue. Hanwha Vision retains a local manufacturing advantage that accelerates firmware customization for Korean scripts, while Hikvision leverages scale economics to price high-resolution units competitively. Suprema and ASSA ABLOY compete in biometric access, focusing on multimodal credentials and privacy-by-design storage modules to align with PIPA constraints.

Strategic pivots gravitate toward AI analytics, cloud-native policy engines and ESG reporting dashboards. Johnson Controls integrated its CCURE Cloud with local data storage options to improve regulatory alignment, whereas Axis Communications released edge-compute cameras that cut uplink bandwidth by 50%, easing remote-site deployments. Domestic start-ups experiment with smartphone-based biometric keys that eliminate traditional card issuance and reduce e-waste, offering sustainability credentials alongside convenience.

Partnership momentum quickens: SK Telecom collaborates with SK Shielders to merge cyber-threat intelligence into physical-alarm correlation workflows, and Digital Realty teams with domestic telecom carriers to co-locate SOC operations next to peering rooms for faster incident mediation. Patent filings at the Korean Intellectual Property Office show rising interest in radar-enabled perimeter monitoring and AI-driven fire-risk prediction, confirming an innovation pipeline poised to enrich the South Korea data center physical security market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The data center physical security market refers to the industry focused on providing products and services to safeguard the physical infrastructure and assets of data centers. This includes measures to protect data centers from unauthorized access to premises, hardware theft, vandalism, sabotage, terrorist acts, and other physical threats. Key components of data center physical security may include video surveillance and monitoring, access control systems, physical barriers, biometric authentication, and environmental controls designed to ensure the safety and integrity of the data center environment.

The South Korean data center physical security market is segmented by solution type, service type, and end users. By type, the market is segmented into video surveillance and access control solutions. By service type, the market is segmented into consulting services and professional services. By end user, the market is segmented into IT and telecommunication, BFSI, government, media and entertainment, and other end users. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Pricing Strategy for Semiconductor Components

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.