South Korea Dairy Alternatives Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

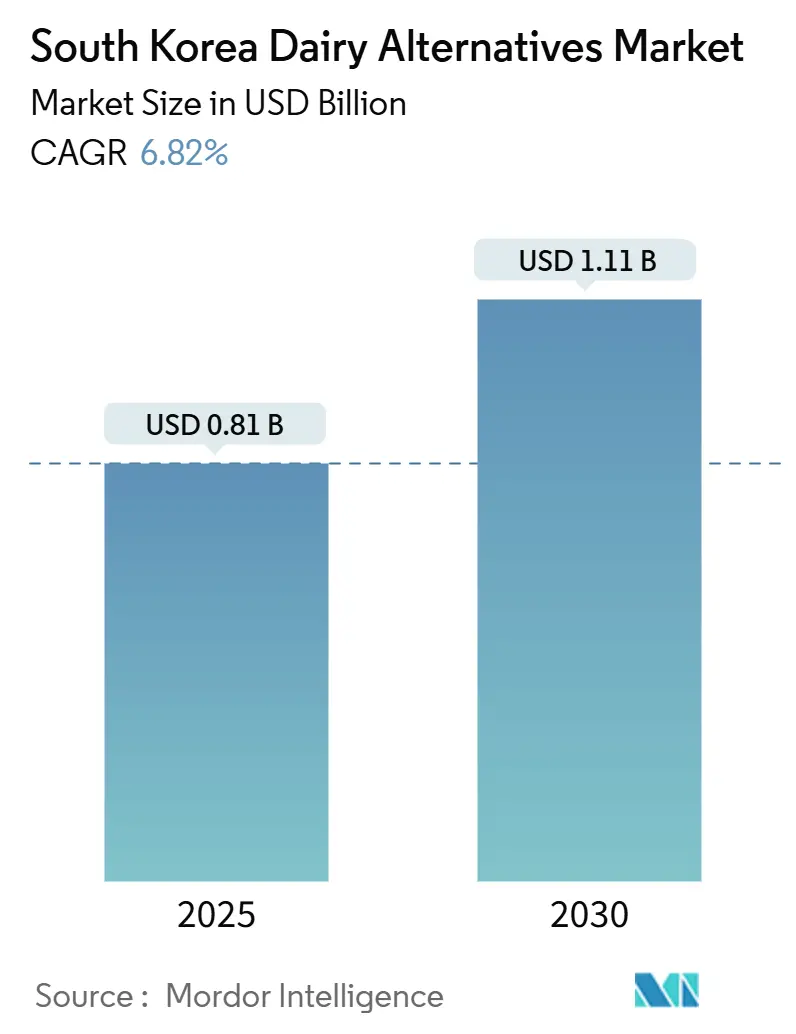

| Market Size (2025) | USD 0.81 Billion |

| Market Size (2030) | USD 1.11 Billion |

| Growth Rate (2025 - 2030) | 6.82% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Dairy Alternatives Market Analysis by Mordor Intelligence

The South Korea Dairy Alternatives Market is projected to grow from USD 0.81 billion in 2025 to USD 1.11 billion by 2030, registering a compound annual growth rate (CAGR) of 6.82%. The market's growth is driven by increasing health and wellness trends, as consumers opt for plant-based milk products due to their low-calorie, cholesterol-free profiles, and added nutritional benefits such as proteins, vitamins, and probiotics. These attributes support vitality, weight management, and align with K-beauty preferences, particularly as vegan and flexitarian diets gain popularity. The expanding café culture in South Korea has further integrated dairy alternatives into everyday beverages like lattes and smoothies, fostering acceptance and demand. Innovations such as precision fermentation are addressing texture and sensory gaps in non-dairy yogurts, cheeses, and desserts, appealing to urban millennials seeking sustainable and indulgent options.

Key Report Takeaways

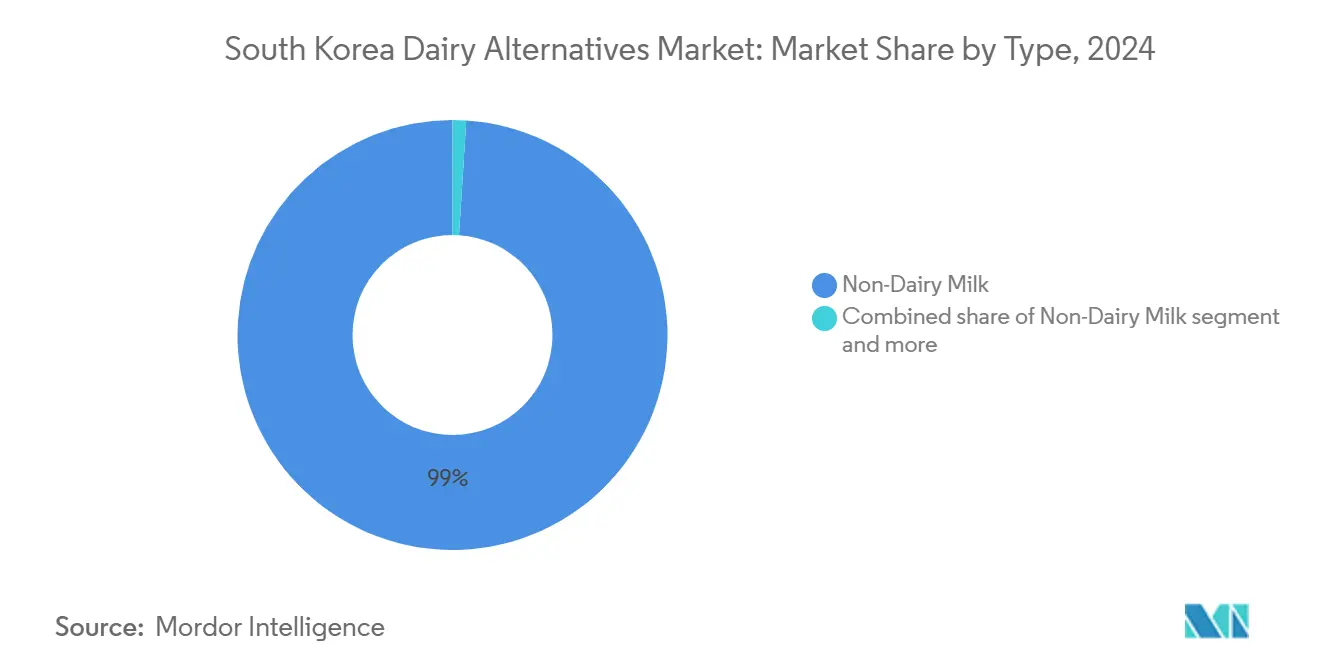

- By type, Non-Dairy Milk led with 98.98% share in 2024; the segment is projected to expand at a 6.86% CAGR through 2030.

- By flavor, Unflavored captured 40.82% in 2024, while Flavored is forecast to expand at a 7.45% CAGR through 2030.

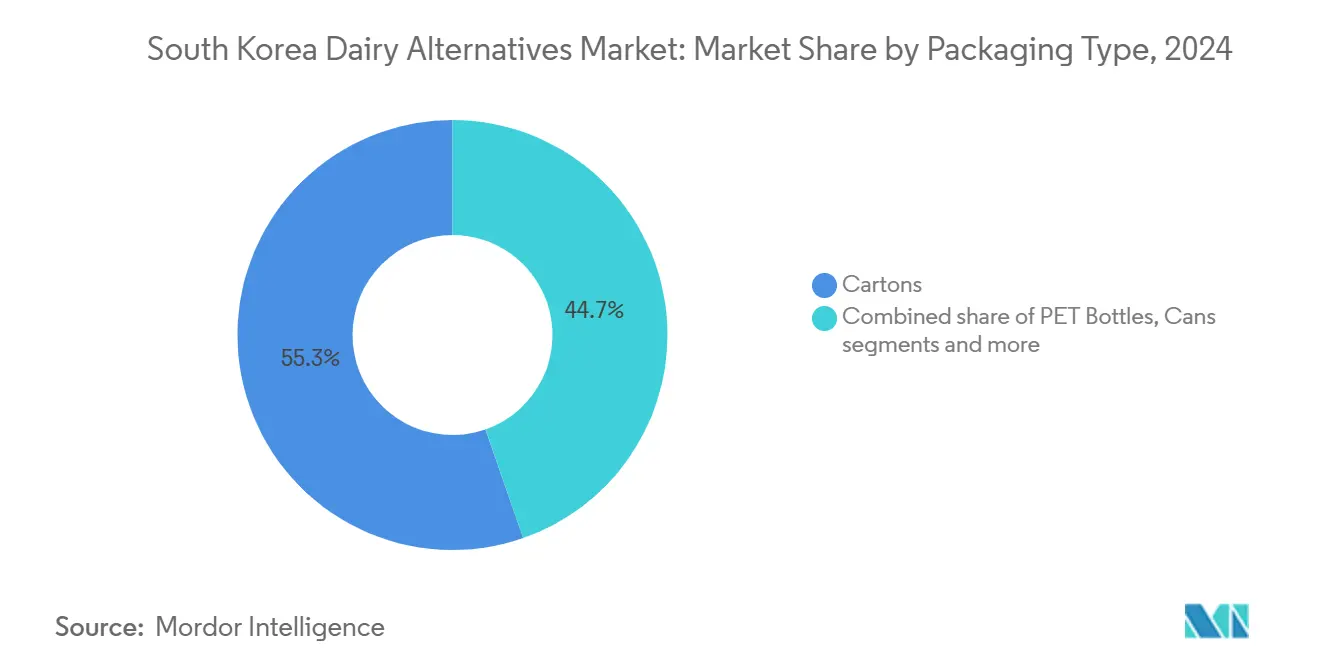

- By packaging type, Cartons held a 55.34% share in 2024, and PET Bottles are projected to grow at a 7.23% CAGR through 2030.

- By distribution channel, Off-trade accounted for 97.54% of the South Korean dairy alternatives market size in 2024, while On-trade is advancing at a 6.87% CAGR to 2030.

South Korea Dairy Alternatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing interest in health and wellness | +1.5% | National, concentrated in Seoul, Gyeonggi, and major urban centers | Medium term (2-4 years) |

| Shift toward plant-forward diets | +1.2% | National, with higher adoption among MZ generation in metropolitan areas | Long term (≥ 4 years) |

| Government and industry support for plant-based innovation | +0.9% | National, with research and development hubs in North Gyeongsang Province and Seoul | Medium term (2-4 years) |

| Strong cafe and coffee culture | +1.0% | National, especially Seoul, Busan, and urban café-dense districts | Short term (≤ 2 years) |

| Advancements in food technology | +0.7% | National, with innovation centers in Seoul and Gyeonggi-do | Long term (≥ 4 years) |

| Rising concerns over animal welfare | +0.5% | National, driven by urban millennials and Gen Z consumers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing interest in health and wellness

The growing focus on health and wellness is driving the South Korean dairy alternatives market, as consumers prioritize nutrient-rich, low-calorie plant-based options that provide high protein, vitamins, potassium, and heart-healthy fats while reducing cholesterol and calorie intake compared to traditional dairy products. This trend is largely attributed to the high prevalence of lactose intolerance in the population, leading to a shift toward digestible substitutes that minimize bloating, gas, and discomfort without compromising nutritional value. Additionally, the rise in milk allergies and the demand for functional foods that support diabetes prevention and overall health are further fueling this growth. Urban millennials and Gen Z are increasingly adopting these alternatives, influenced by wellness trends that emphasize clean-label, fortified beverages containing probiotics and superfoods. Products such as nut butters and plant-based milks are perceived as beneficial for sustained energy and skin health. Food innovation labs are responding by developing localized formulations that combine traditional Korean flavors with health benefits, making these products a regular part of daily diets in smoothies, lattes, and cereals.

Shift toward plant-forward diets

The shift toward plant-forward diets is driving the growth of the dairy alternatives market in South Korea, supported by the adoption of flexitarian and vegan lifestyles. Consumers are increasingly prioritizing ethical and sustainable eating habits, replacing traditional dairy products with plant-based alternatives. This trend is particularly prominent among urban millennials, who are reducing animal product consumption for improved digestion, a lower environmental footprint, and animal welfare considerations. Cultural shifts are further accelerating this trend, with influencers and K-beauty movements promoting the benefits of fortified plant-based milks for skin health, weight management, and overall vitality. These products are increasingly outpacing traditional dairy, as vegan restaurants and e-commerce platforms drive trials among digitally savvy youth who value clean labels and product traceability. According to the Korea Vegan Society, the number of vegans in South Korea reached 2.5 million in 2025, highlighting significant growth and positioning dairy alternatives as essential components of daily diets.

Government and industry support for plant-based innovation

Government and industry support for plant-based innovation is driving the growth of the South Korean dairy alternatives market. This is achieved through strategic investments in research and development, regulatory frameworks, and export incentives that promote advancements in soy, almond, oat, and coconut-based formulations, as well as non-dairy cheeses and yogurts. These efforts aim to address sensory challenges, such as replicating the creaminess and meltability of traditional dairy products. This supportive ecosystem enables companies to build consumer trust, particularly among individuals with lactose intolerance and flexitarian preferences. For example, in October 2023, South Korea’s Ministry of Agriculture, Food and Rural Affairs announced plans to advance the country’s plant-based industry. These plans include establishing research centers for alternative proteins, promoting the use of local ingredients in dairy substitutes, and implementing export strategies targeting the global market, valued at trillions of won. These policy-driven initiatives are directly contributing to the growth of the dairy alternatives market through innovation and strategic support.

Strong café and coffee culture

The strong café and coffee culture in South Korea significantly drives the dairy alternatives market, with plant-based milks such as oat, almond, and soy being widely integrated into beverages like lattes, americano, and iced drinks at urban cafes and chains, including Starbucks Korea. These alternatives provide creamy textures and neutral flavors that complement coffee without overpowering its taste. This daily consumption pattern has normalized non-dairy options, particularly among millennials and Gen Z, encouraging menu diversification with flavored variants. Visible barista preparations further promote these products by highlighting health benefits such as low-calorie content and being cholesterol-free. Additionally, quick-service restaurant (QSR) innovations incorporating plant-based options into meals enhance the versatility of the category. The high density of cafes in South Korea supports the premium positioning of plant-based milks, while e-commerce platforms enable consumers to replicate café-style beverages at home. For example, according to the Ministry of Food and Drug Safety, as of 2023, over 966,200 restaurants were operating in South Korea [1]Source: Ministry of Food and Drug Safety, "Number of restaurants operating in South Korea", mfds.go.kr. This extensive foodservice ecosystem, particularly the prevalence of cafes, plays a critical role in driving demand for dairy alternatives through high-volume beverage service and plant-based menu adaptations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste and texture limitations | -0.8% | National, particularly affecting repeat purchase among flexitarians | Short term (≤ 2 years) |

| Perception of plant-based products as highly processed | -0.6% | National, concentrated among older consumers and health purists | Medium term (2-4 years) |

| Limited availability of certain varieties | -0.4% | Regional, more acute outside Seoul and Gyeonggi-do | Short term (≤ 2 years) |

| Supply chain vulnerabilities | -0.5% | National, with exposure to global commodity price volatility | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Taste and texture limitations

Taste and texture challenges hinder the growth of the South Korean dairy alternatives market. Plant-based milks often exhibit beany aftertastes, gritty textures, or watery consistencies, which fail to replicate the creamy richness and smooth meltability of traditional dairy products. This deters consumers accustomed to the indulgent experience of dairy-based lattes, yogurts, and cheeses. Soy-based alternatives, in particular, face issues such as off-flavors and separation, despite advancements in processing techniques like enzyme treatments and homogenization. Similarly, nut-based options struggle with inconsistent foam stability, which affects their appeal in café settings, limiting their adoption among lactose-intolerant but flavor-conscious urban consumers. These sensory limitations also heighten price sensitivity, as premium innovations often fail to appeal to flexitarians who prioritize taste over health benefits. As a result, growth remains concentrated within niche vegan segments rather than achieving widespread household acceptance. Non-dairy cheeses and desserts face additional challenges, including poor stretchability, inadequate browning, and chalky textures caused by pea or coconut proteins.

Perception of plant-based products as highly processed

The perception of plant-based products as highly processed is a limiting factor for the South Korean dairy alternatives market. Consumers express concerns about additives, stabilizers, emulsifiers, and fortificants in products such as soy, almond, and oat milk, often viewing them as artificial despite clean-label claims. Many prefer natural, traditional dairy products or unprocessed ferments like doenjang, driven by health-conscious skepticism toward ultra-processed foods associated with metabolic risks. This perception is particularly strong among older demographics and rural populations, such as those in Jeolla, who value minimal processing. As a result, the adoption of non-dairy yogurts and cheeses, which rely on gums for texture, remains limited. However, urban millennials are increasingly driving demand for transparency, favoring products with shorter ingredient lists and enhanced natural formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Non-Dairy Milk Dominates, Niche Segments Lag

Non-dairy milk accounted for 98.98% of the South Korean dairy alternatives market in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 6.86% through 2030. Its appeal is driven by improved sensory profiles that closely replicate the creaminess and mouthfeel of traditional dairy products. Oat and almond variants, in particular, are noted for their smooth texture, subtle nuttiness, and roasted soybean notes, which are free from overpowering beany flavors or bitterness. These improvements are achieved through advancements in sprouting techniques and processing methods that enhance stability and palatability. Nutritionally, non-dairy milk offers high protein content, enriched vitamins and minerals, probiotics, and lower fat levels while being cholesterol-free. This makes it attractive to health-conscious consumers seeking functional benefits such as improved digestibility for lactose-intolerant individuals and sustainable sourcing that aligns with environmentally conscious preferences.

Non-dairy cheese, yogurt, and desserts are emerging as significant growth segments within South Korea's dairy alternatives market. This growth is driven by increasing lactose intolerance, the rise of veganism, and a shift toward flexitarian diets, particularly among urban millennials seeking sustainable options beyond non-dairy milk. Non-dairy cheese is gaining traction with nut, soy, and coconut-based formulations that replicate meltability for use in pizzas, burgers, and other Western-style snacks. Non-dairy yogurt is experiencing growth through coconut, oat, and almond-based products that appeal to health-conscious consumers with lower calorie content and improved digestibility. Non-dairy desserts, including vegan ice creams and frozen treats, are leveraging eco-friendly packaging, creamy textures derived from pea protein, and innovative flavors.

By Flavor: Unflavored Leads, Flavored Variants Accelerate

In 2024, unflavored non-dairy milk products accounted for 40.82% of the market share. These products dominate due to their versatile and neutral profile, making them suitable for everyday uses such as coffee blending, cereal preparation, and cooking. Consumers prioritize purity and minimal additives, which appeals to health-conscious, lactose-intolerant individuals seeking straightforward, cholesterol-free alternatives. These products often feature natural nutty or oaty flavors derived from soy, almond, or oat bases, without artificial sweetness that could mask their nutritional benefits, such as high protein and vitamin content. The strong consumer trust in unflavored options as reliable dairy substitutes is further supported by dedicated shelving in stores and e-commerce platforms, which encourage impulse purchases. Millennials, in particular, value clean labels, low-calorie content, and digestibility over indulgent flavors. Additionally, foodservice chains offering plain plant-based milk options have normalized their daily use, further driving their market leadership.

The flavored non-dairy milk segment is projected to grow at a CAGR of 7.45% through 2030. This growth is driven by indulgent taste profiles such as vanilla, chocolate, strawberry, and coffee-infused options, which transform plant-based drinks into enjoyable treats. These products are particularly appealing to younger demographics who experiment with novel flavors in smoothies, lattes, and desserts while addressing lactose intolerance. Flavored variants are crafted with low-calorie, allergen-friendly bases such as oat, almond, or soy, enhanced by natural extracts and sweeteners. The segment's momentum is further supported by innovative formulations that overcome early sensory limitations, delivering creamy textures and authentic dairy-like indulgence without cholesterol or heaviness. The rising cafe culture and demand for premium, customizable beverages have also contributed to the popularity of flavored plant-based milk, with foodservice chains increasingly introducing these options.

By Packaging Type: Cartons Dominate, PET Bottles Surge

Cartons accounted for 55.34% of the South Korean dairy alternatives packaging market in 2024, driven by aseptic multilayer barriers that protect plant-based milks from light, oxygen, and contaminants, ensuring nutritional quality and fresh flavors. This segment benefits from the use of renewable paperboard, supported by regulations aimed at reducing plastic usage and growing consumer demand for sustainable packaging, particularly amid the rise in vegan preferences. Lightweight, stackable designs with no-spill grips cater to urban households by offering convenient storage and pouring solutions. Additionally, high printability allows for the effective display of health claims and branding, appealing to millennial consumers. Innovations such as biodegradable coatings and QR code traceability further enhance e-commerce adaptability and foodservice efficiency, solidifying cartons as a versatile and sustainable packaging option that outperforms rigid alternatives in both functionality and consumer appeal.

PET bottles are projected to grow at a CAGR of 7.23% through 2030, contributing significantly to the growth of dairy alternatives packaging in South Korea. Their shatterproof and lightweight properties make them ideal for urban, on-the-go lifestyles, where consumers frequently choose plant-based milk for commutes, workouts, or quick office breaks. Additionally, cost-effective scalability supports the introduction of premium flavored products, while tamper-evident features build trust among allergen-sensitive consumers. This growth aligns with South Korea's sustainability goals, driven by innovations in rPET recycling and deposit systems. These advancements support portable packaging solutions in e-commerce and foodservice grab-and-go segments. According to the Ministry of Climate, Energy and Environment, South Korea aims to reduce plastic waste generation by 50% and increase the plastic waste recycling rate from 34% to 70% by 2030 [2]Source: Ministry of Climate, Energy and Environment, "Land and Waste". eng.me.go.kr. These initiatives are expected to further drive eco-friendly adaptations of PET bottles, meeting the rising demand for vegan and plant-based products.

By Distribution Channel: Off-Trade Dominates, On-Trade Revives

In 2024, off-trade channels accounted for 97.54% of South Korea's dairy alternatives market. These channels dominate due to their convenience for household stockpiling and impulse purchases. Supermarkets and hypermarkets play a key role by offering extensive shelf space for a variety of plant-based milk options. This setup allows consumers to compare nutritional profiles, flavors, and brands at their convenience, aligning with urban lifestyles that prioritize planned grocery shopping over spontaneous dining. The dominance of off-trade channels is further supported by omnichannel integration, combining the physical accessibility of convenience stores with the growing popularity of online platforms. These platforms provide home delivery, subscription services, and personalized recommendations, catering to health-conscious, lactose-intolerant consumers seeking fortified and sustainable options without the need for immediate consumption.

On-trade channels are projected to grow at a compound annual growth rate (CAGR) of 6.87% through 2030, contributing significantly to the expansion of South Korea's dairy alternatives market. These channels offer immediate accessibility in high-traffic locations such as cafes, quick-service restaurants (QSRs), and other dining establishments. Urban consumers are increasingly exposed to vegan menu options, encouraging trial among lactose-intolerant and flexitarian diners without requiring a commitment to home consumption. Foodservice chains are innovating by incorporating dairy alternatives into beverages and baked goods, enhancing visibility and fostering repeat consumption. This trend aligns with growing health awareness, as consumers seek cholesterol-free, nutrient-fortified substitutes. Additionally, the rise of ethical veganism and sustainable dining preferences is driving per capita on-trade consumption of dairy alternatives. According to the United States Department of Agriculture (USDA), in 2023, monthly per capita spending in this sector reached USD 139.1, highlighting strong foodservice investments that are accelerating the adoption of plant-based alternatives [3]Source: United States Department of Agriculture (USDA), "Food Service - Hotel Restaurant Institutional Annual", usda.gov.

Geography Analysis

South Korea's dairy alternatives market demonstrates significant geographic concentration, with Seoul and Gyeonggi-do accounting for the majority of consumption. This is attributed to higher disposable incomes, a dense café culture, and a demographic inclined toward early adoption. Millennials and Gen Z flexitarians in these urban areas are driving demand for plant-based milks, particularly in lattes, vegan restaurants, and premium off-trade options. The prevalence of lactose intolerance and health-conscious trends further boosts the popularity of oat, almond, and soy variants, aligning with fast-paced lifestyles that prioritize convenient and sustainable choices.

Busan is emerging as a secondary market hub, supported by coastal tourism, the expansion of quick-service restaurant (QSR) menus, and increasing wellness awareness. These factors are normalizing the consumption of non-dairy yogurts and cheeses, particularly in seafood pairings and beachside cafés. Meanwhile, the Jeolla Provinces, known for their agricultural and conservative roots, are experiencing niche growth. This is driven by local soy-based innovations and flexitarian experimentation, which bridge traditional dairy preferences with growing interest in plant-based alternatives.

Additionally, the regulatory environment in South Korea is facilitating this market evolution. In November 2023, the Ministry of Food and Drug Safety (MFDS) issued labeling guidelines for plant-based products. These regulations prohibit the use of animal-derived food names, such as "milk," for plant-based alternatives to prevent consumer confusion. This initiative aims to enhance consumer education and build trust across the market, fostering greater acceptance and adoption of dairy alternatives nationwide.

Competitive Landscape

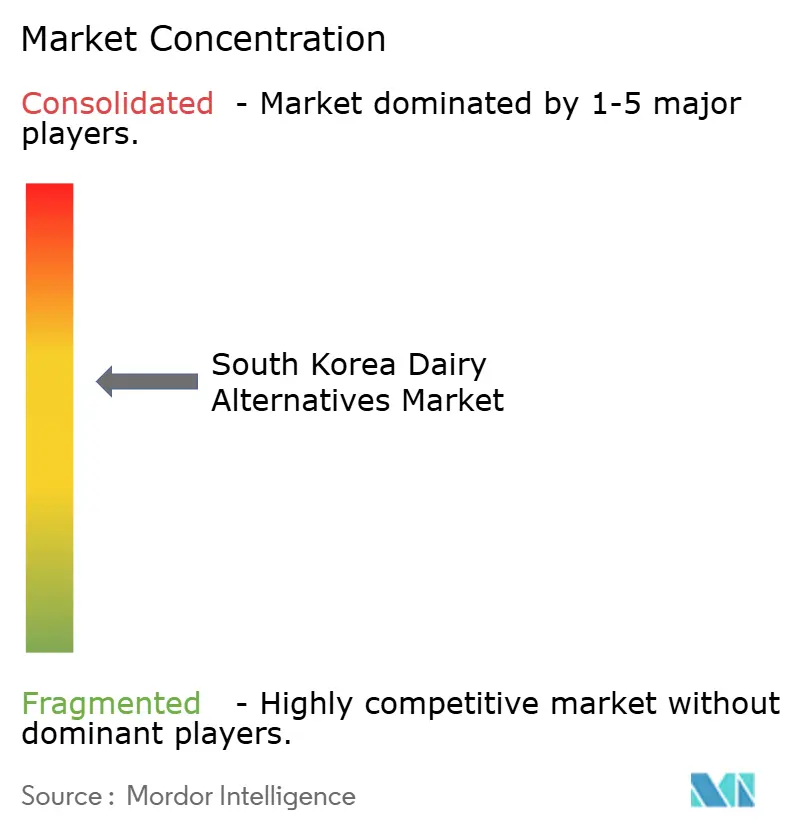

The South Korean dairy alternatives market is moderately fragmented, with key players such as Armored Fresh, Califia Farms LLC, Blue Diamond Growers, Dr. Chung’s Food Co. Ltd, and Maeil Co. Ltd leading the market. These companies offer a diverse range of soy, almond, and oat milk products tailored to local consumer preferences. They leverage extensive manufacturing capabilities, distribution networks, and partnerships with cafés to integrate plant-based options into mainstream consumption, driven by increasing lactose intolerance and the growing popularity of vegan diets. Domestic leaders like Maeil and Dr. Chung’s Food Co. Ltd dominate the non-dairy milk segment with products featuring familiar nutty flavors and fortified formulations.

There are significant opportunities in the non-dairy cheese, yogurt, and dessert segments, where current market penetration is limited due to challenges in taste, texture, and retail distribution. These gaps present innovation potential, particularly in developing products that replicate the meltability and creaminess of traditional dairy using nut bases or pea proteins. Emerging players are addressing these niches with offerings such as probiotic yogurts and coconut-based cheeses, catering to Westernized menus and health-conscious Gen Z consumers. Meanwhile, established companies face challenges in formulation, creating opportunities for startups to differentiate themselves with clean-label products and locally inspired flavors, such as sesame-infused desserts.

Precision fermentation is emerging as a transformative technology in the market, enabling startups and agile firms to produce animal-free caseins and whey proteins. These innovations enhance the sensory qualities of non-dairy products, such as melt, stretch, and browning in cheeses and yogurts, addressing key barriers to mass adoption. This technological advancement positions disruptors to compete with incumbents in premium segments. Additionally, precision fermentation supports scalable and customizable textures for products like vegan ice creams, aligning with ethical consumer demands and the expansion of urban cafés.

South Korea Dairy Alternatives Industry Leaders

-

Armored Fresh

-

Blue Diamond Growers

-

Califia Farms LLC

-

Dr. Chung’s Food Co. Ltd

-

Maeil Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Seoul Milk introduced Plant-Based Yogurt Cocogurt, a product made with 96.3% coconut milk. It offers a sweet and rich coconut flavor and is enriched with vitamins, minerals, and dietary fiber.

- March 2023: Binggrae introduced a dairy-free version of its well-known banana-flavored milk. This product is made with almond and soy, catering to vegan consumers and individuals with dairy restrictions.

South Korea Dairy Alternatives Market Report Scope

Non-Dairy Butter, Non-Dairy Milk are covered as segments by Category. Off-Trade, On-Trade are covered as segments by Distribution Channel.| Non-Dairy Milk | Oat Milk |

| Hemp Milk | |

| Hazelnut Milk | |

| Soy Milk | |

| Almond Milk | |

| Coconut Milk | |

| Cashew Milk | |

| Non-Dairy Cheese | |

| Non-Dairy Desserts | |

| Non-Dairy Yogurt | |

| Others |

| Flavored |

| Unflavored |

| PET Bottles |

| Cans |

| Cartons |

| Others |

| On-trade | |

| Off-trade | Convenience Stores |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others (Warehouse clubs, gas stations, etc.) |

| By Type | Non-Dairy Milk | Oat Milk |

| Hemp Milk | ||

| Hazelnut Milk | ||

| Soy Milk | ||

| Almond Milk | ||

| Coconut Milk | ||

| Cashew Milk | ||

| Non-Dairy Cheese | ||

| Non-Dairy Desserts | ||

| Non-Dairy Yogurt | ||

| Others | ||

| By Flavor | Flavored | |

| Unflavored | ||

| Packaging Type | PET Bottles | |

| Cans | ||

| Cartons | ||

| Others | ||

| Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Supermarkets and Hypermarkets | ||

| On-line Retail | ||

| Others (Warehouse clubs, gas stations, etc.) | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms