South America Polycarbonate (PC) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

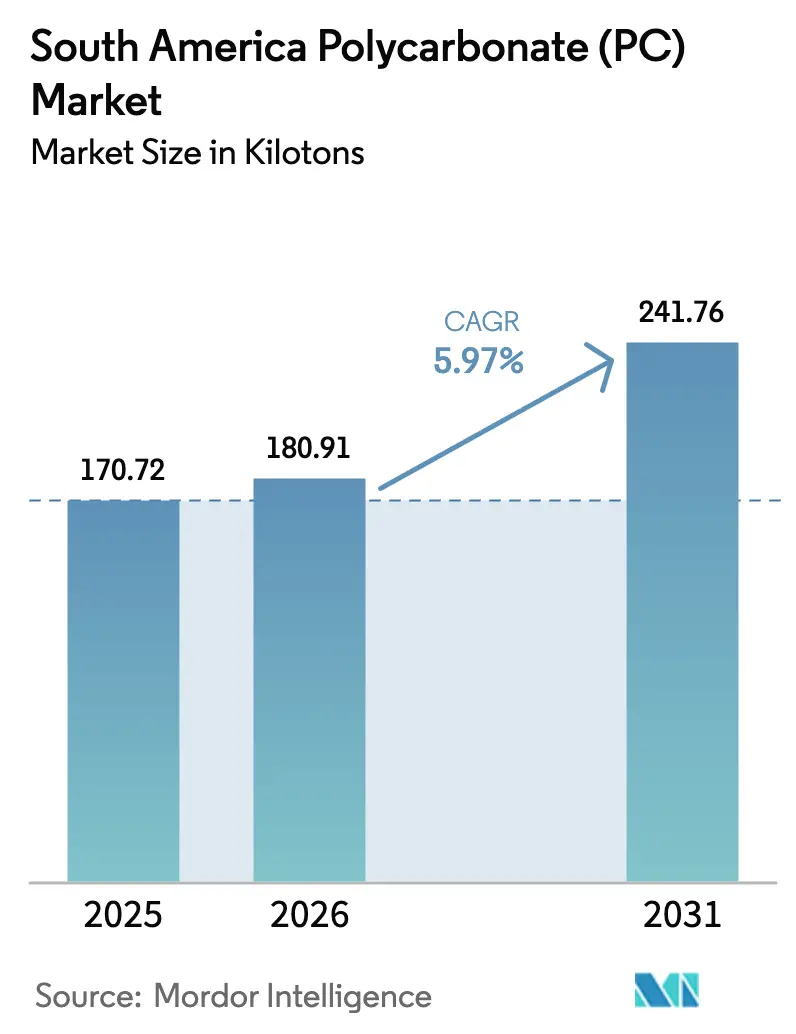

| Base Year Market Size (2025) | 170.72 kilotons |

| Market Volume (2026) | 180.91 kilotons |

| Market Volume (2031) | 241.76 kilotons |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

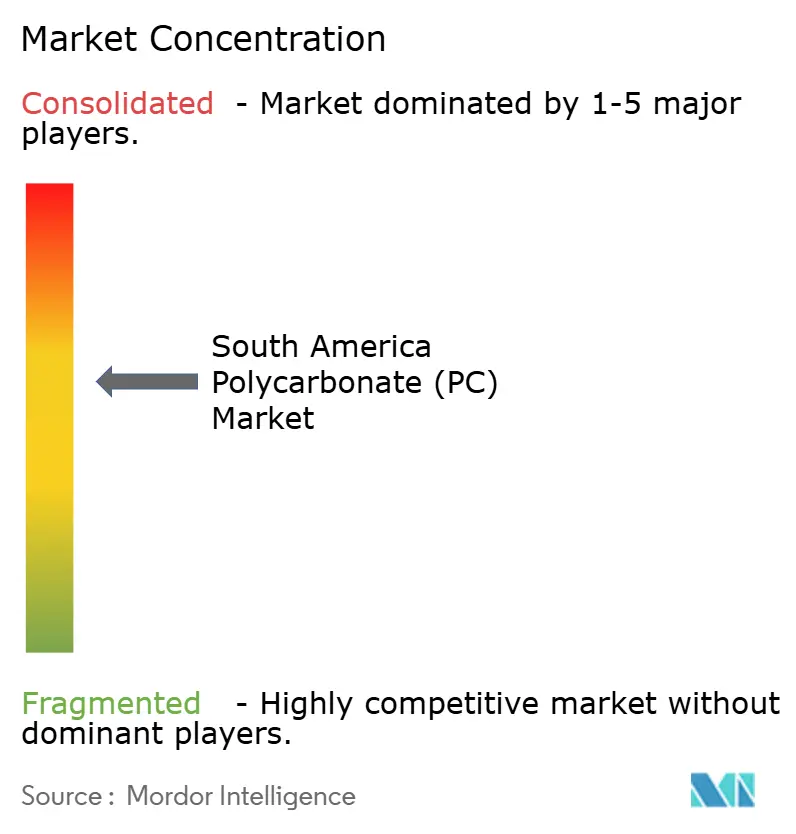

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Polycarbonate (PC) Market Analysis by Mordor Intelligence

The South America Polycarbonate Market size was valued at 170.72 kilotons in 2025 and is estimated to grow from 180.91 kilotons in 2026 to reach 241.76 kilotons by 2031, at a CAGR of 5.97% during the forecast period (2026-2031). Brazil's electronics assembly base is expanding rapidly. Construction activity is rebounding under stricter green-building codes, and automotive OEMs are transitioning to paint-free, high-gloss exterior parts. These changes reduce finishing time and lower emissions of volatile organic compounds. As manufacturers pursue Scope 3 carbon reductions, there is a notable increase in the adoption of higher recycled-content grades, with sheets continuing to dominate in glazing and roofing applications. However, a significant policy risk persists. South America accounts for only a small share of global bisphenol-A feedstock production. This limited share exposes converters to potential freight cost spikes and tariff fluctuations.

Key Report Takeaways

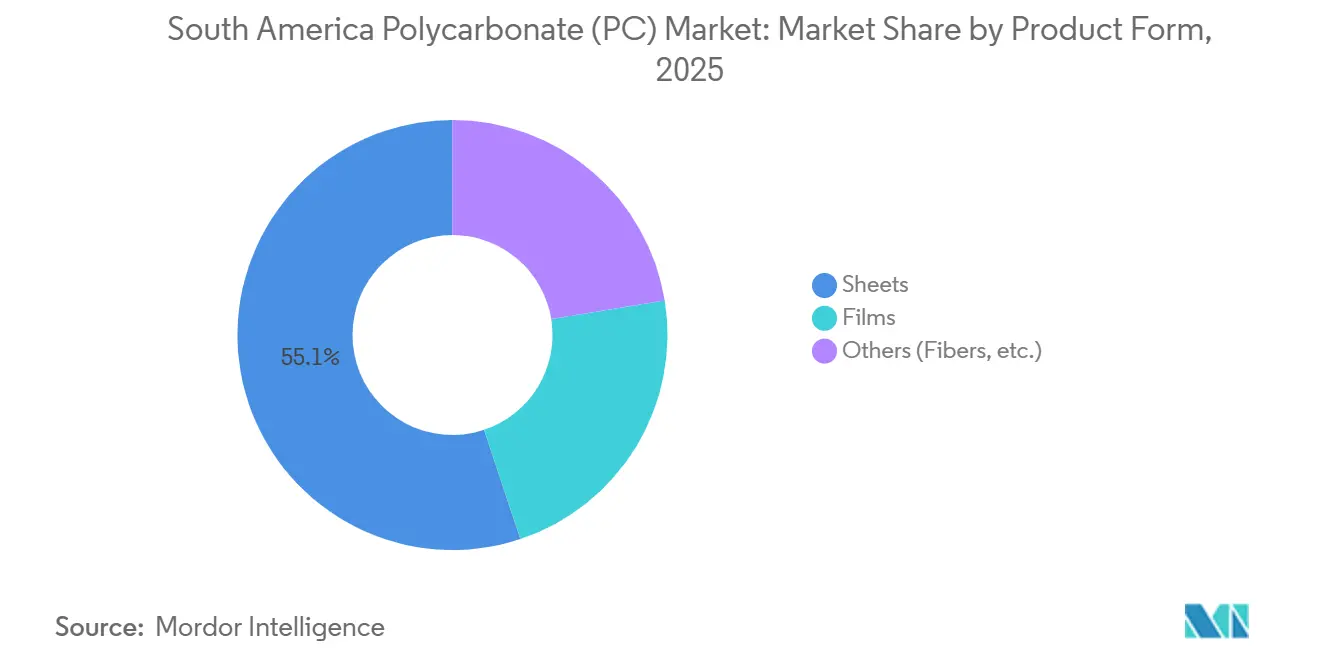

- By product form, sheets led with 55.12% of the South America polycarbonate market share in 2025, while films are projected to expand at a 6.46% CAGR to 2031.

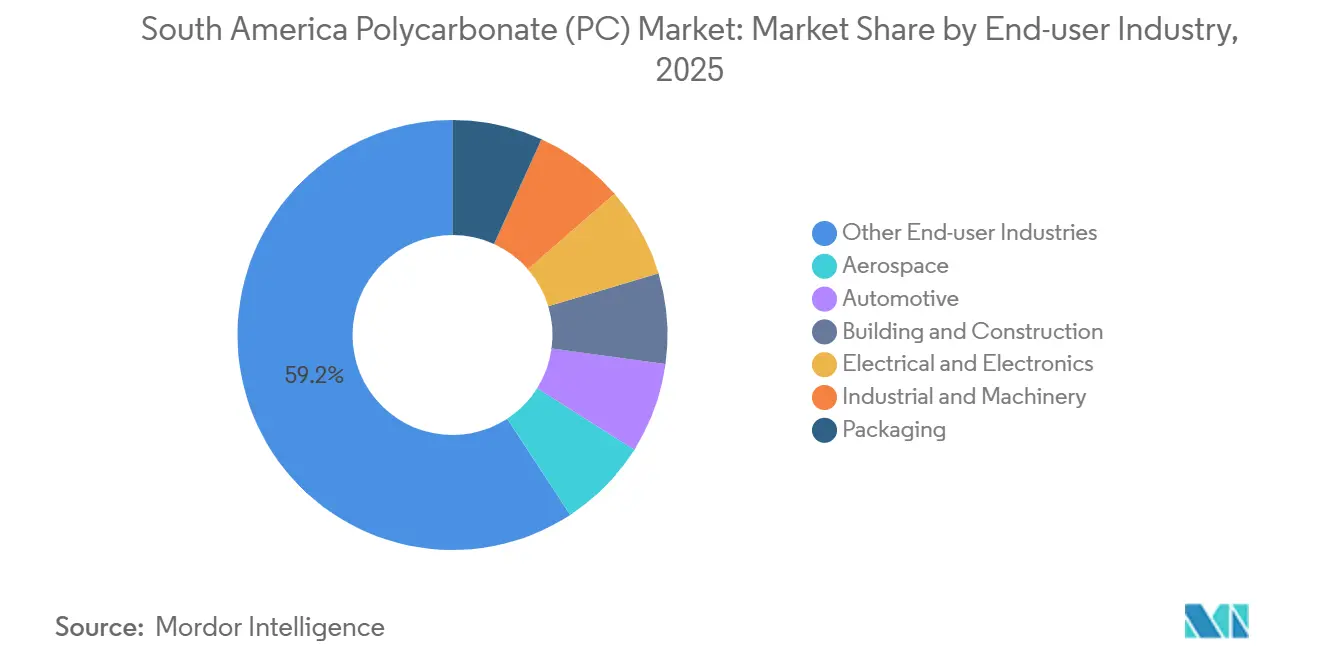

- By end-user industry, other end-user industries accounted for 59.22% share of the South America polycarbonate market size in 2025 and electrical and electronics is advancing at a 6.78% CAGR through 2031.

- By geography, Brazil captured 41.10% of the South America polycarbonate market share in 2025, whereas Argentina is forecast to grow at a 6.56% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Polycarbonate (PC) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronics manufacturing electrification | +1.20% | Brazil (São Paulo, Manaus), Argentina (Buenos Aires) | Medium term (2-4 years) |

| Construction boom and green-building codes | +1.50% | Brazil (national, São Paulo, Rio de Janeiro), Argentina (Buenos Aires, Vaca Muerta corridor) | Short term (≤ 2 years) |

| OEM shift to paint-free high-gloss PC | +0.80% | Brazil (automotive clusters: São Paulo, Paraná), Argentina | Medium term (2-4 years) |

| Local green-hydrogen BPA projects | +0.40% | Brazil (Piauí, São Paulo industrial belt), Argentina | Long term (≥ 4 years) |

| ESG-driven recycled/bio-based PC uptake | +0.70% | Global, early adoption in Brazil (São Paulo industrial belt) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electronics Manufacturing Electrification

In 2025, Brazil's electronics sector experienced significant growth, supported by increased investments. During the first half of the year, air-conditioner production increased, driving demand for polycarbonate housings, fan blades, and control panels. Meanwhile, the sales of hybrid and electric vehicles rose, spurring heightened demand for flame-retardant polycarbonate battery covers and charging-port housings[1]Organização Internacional dos Constructores de Automóveis, “2024 Production Statistics and 2025 Sales Data,” oica.net . This development expanded the South American polycarbonate market by incorporating specialty grades into compact, high-density consumer devices. However, local processors faced margin pressures due to an influx of low-cost imports from China.

Construction Boom and Green-Building Codes

In recent years, Brazil has experienced significant growth in its construction services and works. The national construction cost index has also risen, signaling robust activity in sectors such as glazing, roofing, and cladding, with polycarbonate sheets increasingly substituting traditional, heavier glass. Tax credits in São Paulo and Rio de Janeiro municipalities are incentivizing projects certified under PROCEL Edifica, LEED, or AQUA, which is driving the adoption of polycarbonate sheets in daylighting façades[2]Brazil Green Building Council, “PROCEL Edifica and Green Building Certifications in Brazil,” gbcbrasil.org.br . Meanwhile, in Argentina, the materials-demand index has rebounded, driven largely by the Vaca Muerta pipeline works. These projects require lightweight, impact-resistant glazing shields, thereby broadening the footprint of the South America polycarbonate market.

OEM Shift to Paint-Free High-Gloss PC

Brazil assembled 2.64 million vehicles in 2025, with a target of 2.74 million for 2026. Several original equipment manufacturers (OEMs) are replacing painted ABS panels with molded-in-color polycarbonate. This transition eliminates finishing steps and reduces cycle time, as reported. Covestro’s Makrolon and Formosa Idemitsu’s TARFLON IR series, recognized for their durability and gloss retention under tropical UV rays, position polycarbonate as a cost-neutral alternative when accounting for paint savings. This development expands the market opportunity for polycarbonate in South America, particularly for applications such as spoilers, mirror housings, and headlamp lenses.

ESG-Driven Recycled/Bio-Based PC Uptake

SABIC aims to produce a significant amount of circular polycarbonate by 2030, targeting a reduction in greenhouse gas emissions compared to traditional grades. Covestro RP series incorporates chemically recycled content, while Trinseo EMERGE ECO line features post-consumer scrap, both aiding electronics brands in meeting their Scope 3 targets. In 2024, Brazil's ANVISA approved chemically recycled polycarbonate for food contact, paving the way for its use in premium water bottles and cosmetics packaging. These advancements are drawing new buyers into the South America polycarbonate market, despite the region's lagging recycling infrastructure.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import dependence for specialty grades | -0.60% | Brazil, Argentina | Short term (≤ 2 years) |

| Under-developed recycling infrastructure | -0.50% | Brazil, Argentina | Medium term (2-4 years) |

| Water and energy cost spikes for producers | -0.40% | Brazil industrial hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Import Dependence for Specialty Grades

South America, producing a small share of global bisphenol-A, remains reliant on Asia and the Middle-East for sourcing optical, medical, and flame-retardant polycarbonates. This dependency has left converters highly susceptible to fluctuations in freight costs. To support its domestic market, Brazil increased polymer import tariffs in 2024. If similar measures are applied to engineering plastics, it could strain working capital across South America's polycarbonate sector. Meanwhile, Argentine processors continue to face the dual challenges of currency volatility and a lack of local resin warehousing, resulting in extended lead times and higher hedging expenses.

Water and Energy Cost Spikes for Producers

In Brazil's industrial southeast, producers facing already thin margins on commodity sheets are encountering rising input costs due to electricity tariff adjustments and seasonal water scarcity. The energy-intensive sector of chemical recycling is particularly affected, as it contends with both water treatment charges and elevated peak-hour power rates. This combination not only reduces the cost advantage over virgin resin but also discourages investments in more lucrative recycled grades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Sheets Command, Films Accelerate

Sheets accounted for 55.12% of the 2025 volume within the South America polycarbonate market. These sheets, which are favored for agricultural greenhouses, skylights, and commercial roofing, offer impact strength and UV stability at only one-sixth the weight of glass. Covestro’s Makrolon multiwall sheet, featuring warranties of up to 20 years, is well-aligned with Brazil’s green-building codes. This feature assists architects in meeting PROCEL Edifica thresholds without requiring metal supports. Films, although smaller in market share, are projected to grow at a 6.46% CAGR during the forecast period of 2026-2031. This growth is driven by their application in flexible touch-screen overlays, membrane switches, and automotive interior laminates, which are increasingly replacing heavier PMMA. Additionally, thinner gauges, particularly those under 250 microns, are reducing resin usage per unit, thereby improving converter margins. In 2024, Brazil's production of millions of air-conditioners incorporated clear polycarbonate film for digital displays. Meanwhile, Argentina’s Vaca Muerta modular housing projects have specified anti-hail co-extruded sheets. These developments are expanding the South America polycarbonate market, catering to both ends of the value spectrum.

By End-User Industry: Diversified Demand Mix

Other end-user industries, ranging from medical devices to specialty optics, captured 59.22% of volume in 2025, underscoring polycarbonate's adaptability. It is being utilized in sterilizable surgical handles, industrial machine guards, and high-precision lenses. Electrical and electronics is the fastest-growing segment, with a 6.78% CAGR during the forecast period of 2026-2031, largely driven by Brazil's burgeoning edge-AI appliance market, which demands thermally stable and electrically insulating housings. The automotive sector has seen heightened demand, spurred by OEMs' shift towards paint-free exterior parts and lightweight glazing. Notably, in 2025, Brazil ramped up vehicle exports to Argentina, solidifying the cross-border trade of headlamp lenses and panoramic roofs. Meanwhile, construction applications have been benefiting from the region's green-building initiatives, and the aerospace sector has been securing niche, high-value orders for cabin windows and diffusers in Embraer jets. These diverse streams collectively bolster the South America polycarbonate market, providing resilience against disruptions in any single sector.

Geography Analysis

Brazil remains the anchor of the South America polycarbonate market with 41.10% of 2025 consumption. Policy incentives, particularly those promoting photovoltaic installations with polycarbonate backsheets, further cement Brazil's leading position. Argentina, by contrast, is the fastest climber at a projected 6.56% CAGR during the 2026-2031 period. This surge is driven by PPP road projects and the Vaca Muerta pipeline, both of which are boosting demand for lightweight shelters and corrosion-resistant covers. In the rest of South America, demand is largely influenced by mining safety glazing in Chile and greenhouse roofing in Colombia.

In Brazil, federal and municipal green-building initiatives, such as tax incentives for achieving LEED silver ratings or higher, are propelling the adoption of polycarbonate sheets. São Paulo's commercial hubs are seeing increased sheet usage, while skyscrapers in Rio de Janeiro are turning to multiwall panels to comply with updated thermal insulation standards. However, power tariffs are rising in Minas Gerais and Espírito Santo due to transmission constraints. This has prompted processors to shift closer to hydropower sources in Paraná. Despite a significant year-over-year surge in Argentina's construction cost index as of February 2025, which has tightened margins, there is a discernible preference for long-life polycarbonate over multi-layer glass. The reason is that polycarbonate's installation demands less labor, making it a more economical choice.

Trade policies are proving pivotal. In 2024, Brazil raised its polymer import tariffs. Furthermore, if domestic production does not keep pace, Brazil might introduce more anti-dumping measures. Such moves could limit converters' access to standard-grade resin across the South American polycarbonate landscape. Meanwhile, SABIC's impending sale of its Campinas plant to Mutares, set to finalize in the second half of 2026, poses another challenge. If Mutares shifts focus to recycled or medical-grade resins, it could curtail the local supply of commodity sheet resin. This is expected to compel processors to rely on Asian spot cargoes, which come with extended lead times and currency fluctuations.

Competitive Landscape

The South America polycarbonate market is moderately consolidated. SABIC's divestiture of its Engineering Thermoplastics division, including the Campinas facility, reflects a strategic shift toward circular polymers. This move may create opportunities for Asian suppliers and regional converters to focus on commodity sheets and films.

Covestro has expanded its RP chemically recycled portfolio to meet automotive OEM Scope 3 criteria. Similarly, Trinseo's EMERGE ECO line, featuring high recycled content, is gaining traction among electronics brands, driven by Brazil's extended-producer-responsibility law. The market emphasizes technological advancements, including molded-in-color high-gloss parts that eliminate painting, advanced dissolution recycling, and initial trials with bio-based BPA.

However, South America's local production capacity remains limited. No domestic start-up has scaled polycarbonate production or chemical recycling. Braskem's new recycling lines exclude engineering plastics. Brazilian sheet extruders are collaborating with Taiwanese resin manufacturers like CHIMEI and Wanhua, reducing lead times and offering competitive pricing against European imports, especially amid the 2024 freight-rate surge. Despite these developments, the top five suppliers

South America Polycarbonate (PC) Industry Leaders

SABIC

Covestro AG

LG Chem

Mitsubishi Chemical Group Corporation

Teijin Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SABIC launched LNP ELCRES CXL copolymers offering upgraded chemical resistance for mobility, electronics, and industrial uses.

- May 2024: Covestro AG released a polycarbonate resin with 90% post-consumer recycled content that achieves UL 94 V-0 at 1.5 mm and delivers a 70% lower carbon footprint than virgin resin.

South America Polycarbonate (PC) Market Report Scope

Polycarbonate (PC), also known as "organic glass," is a durable, transparent thermoplastic polymer with exceptional impact resistance. Its properties, including heat resistance and dimensional stability, make it ideal for various applications such as optical devices (camera lenses, car headlights), home decor (room dividers, aquariums), and bullet-resistant materials.

The South America Polycarbonate (PC) Market is segmented by product form, end-user industry, and geography. By product form, the market is segmented into sheets, films, and others. By end-user industry, the market is segmented into aerospace, automotive, building and construction, electrical and electronics, industrial and machinery, packaging, and other end-user industries. The report also covers the market size and forecasts for polycarbonate in 2 countries across the South American region. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Sheets |

| Films |

| Others (Fibers, etc.) |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| Brazil |

| Argentina |

| Rest of South America |

| By Product Form | Sheets |

| Films | |

| Others (Fibers, etc.) | |

| By End User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | Brazil |

| Argentina | |

| Rest of South America |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polycarbonate market.

- Resin - Under the scope of the study, virgin polycarbonate resin in its primary forms such as powder, granule, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms