Asia-Pacific Polycarbonate (PC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

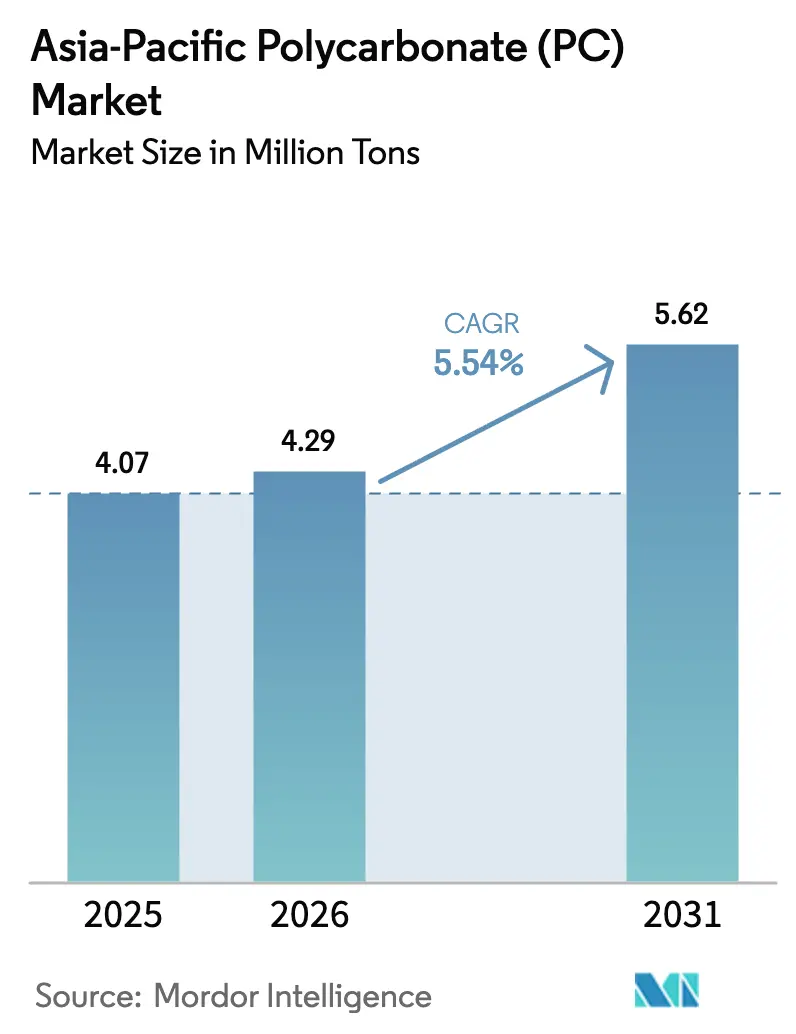

| Base Year Market Size (2025) | 4.07 Million tons |

| Market Volume (2026) | 4.29 Million tons |

| Market Volume (2031) | 5.62 Million tons |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

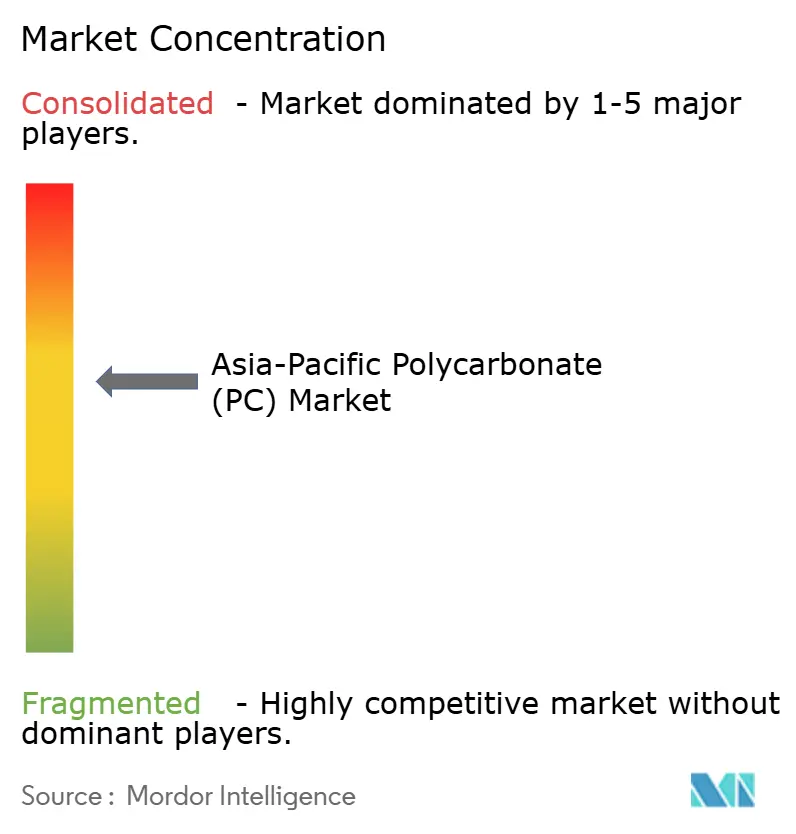

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Polycarbonate (PC) Market Analysis by Mordor Intelligence

The Asia-Pacific Polycarbonate Market size in 2026 is estimated at 4.29 million tons, growing from 2025 value of 4.07 million tons with 2031 projections showing 5.62 million tons, growing at 5.54% CAGR over 2026-2031. Robust electronics manufacturing, accelerating electric-vehicle (EV) adoption, and infrastructure upgrades across Southeast Asia collectively drive this trajectory, keeping the Asia-Pacific polycarbonate market at the center of global demand growth. The widespread use of polycarbonate in display lenses, battery cases, and building glazing leverages the material’s optical clarity, flame retardance, and lightweight profile, giving suppliers latitude to penetrate new value-added niches. China’s domestic ecosystem, policy incentives for new-energy technologies, and rapid additions of optical-grade capacity safeguard regional supply, while the adoption of chemically recycled feedstock increases circularity compliance without performance trade-offs. A simultaneous shift toward specialty films for flexible electronics highlights the Asia-Pacific polycarbonate market's transition from a commodity-driven to an application-driven approach.

Key Report Takeaways

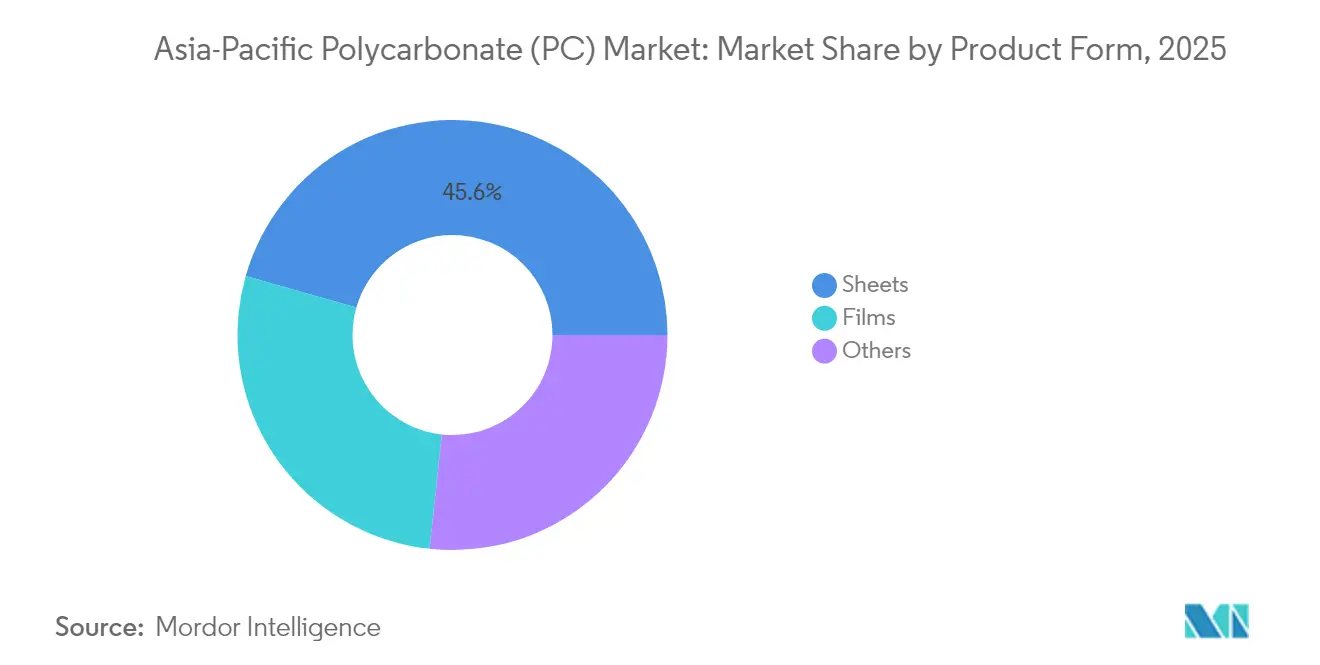

- By product form, sheets led with 45.58% of the Asia-Pacific Polycarbonate (PC) market share in 2025, whereas films are projected to register the quickest 5.83% CAGR through 2031.

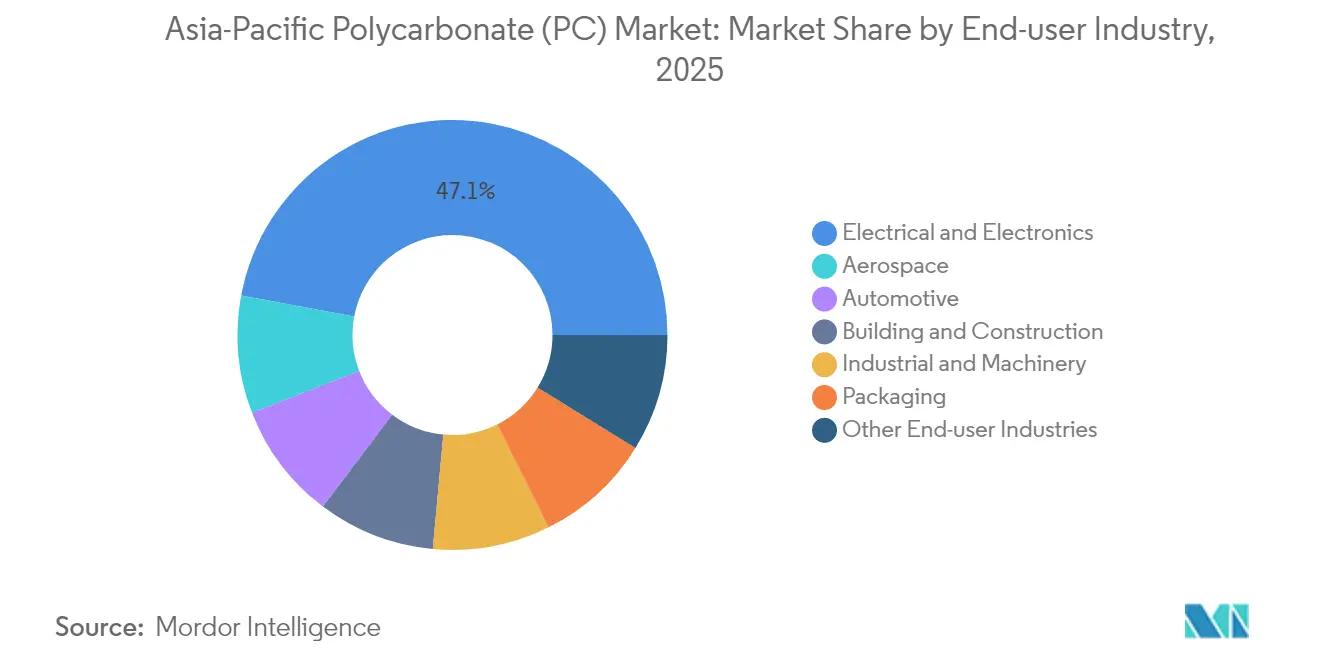

- By end-user industry, the electrical and electronics sector accounted for 47.05% of the Asia-Pacific Polycarbonate (PC) market size in 2025 and is expected to advance at a 6.19% CAGR through 2031.

- By geography, China retained a 60.12% market share in 2025, while the Rest of Asia-Pacific segment is poised to expand at a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Polycarbonate (PC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-driven demand for lightweight glazing & battery cases | +1.2% | China, Japan, South Korea, ASEAN spillover | Medium term (2-4 years) |

| Surge in Chinese optical-grade PC for advanced displays | +0.8% | China core, Southeast Asia tech transfer | Short term (≤2 years) |

| Rise of chemical-recycling routes (ISCC PLUS certified feedstock) | +1.1% | Global; early uptake in Japan, Korea | Long term (≥4 years) |

| Construction boom in ASEAN green-building projects | +0.9% | Thailand, Malaysia, Vietnam, Indonesia | Medium term (2-4 years) |

| 3-D printing adoption in prototyping & spares manufacturing | +0.7% | Japan, South Korea, Australia, ASEAN | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

EV-Driven Demand for Lightweight Glazing & Battery Cases

Automakers across the region are redesigning battery enclosures and panoramic sunroofs using polycarbonate to reduce mass, enhance impact resistance, and improve range. Covestro’s Map Ta Phut expansion adds advanced film capacity calibrated for thin-wall battery case liners, signaling a strategic shift toward EV-specific grades[1]Covestro, “Covestro Expands Film Capacity in Thailand,” covestro.com. China’s New Energy Vehicle mandate and Japan’s 2050 carbon-neutrality roadmap extend policy certainty, prompting OEMs to lock in lightweight materials across future model cycles. As solid-state battery commercialization gains momentum after 2027, demand for high-heat-resistant polycarbonate is expected to rise, rewarding suppliers who have invested early in flame-retardant chemistries. The convergence of stricter safety regulations and consumer appetite for longer driving range ensures a multi-year pull on high-performance volumes. Tier-1 component suppliers are therefore partnering with material producers to co-engineer battery enclosures, creating stickier downstream relationships that insulate against commodity price swings.

Surge in Chinese Optical-Grade PC for Advanced Displays

Domestic display panel makers in China are scaling capacity to support high-resolution smartphones, vehicle infotainment screens, and AR/VR headsets. Optical-grade polycarbonate must exhibit low birefringence and superior thermal stability, driving investments in purification technologies that reduce trace contaminants. Wanhua’s 200 ktpa expansion squarely targets this niche, enabling localization of previously imported grades while lowering lead times for electronics OEMs. AI-enabled quality control systems installed along the extrusion lines tighten dimensional tolerances, strengthening the appeal of local supply in a segment historically dominated by Japanese producers. As display makers migrate to curved and foldable form factors, demand for ultra-thin, high-clarity sheets and films is expanding faster than overall panel output, widening the premium against commodity grades. These dynamics cement optical-grade PC as a strategic pillar of China’s semiconductor supply-chain resilience program.

Rise of Chemical-Recycling Routes (ISCC PLUS Certified Feedstock)

Chemical recycling closes performance gaps that hinder mechanically recycled streams, supplying virgin-like resin to meet rising OEM sustainability commitments. SABIC’s ISCC PLUS certified portfolio demonstrates identical mechanical strength and optical properties to fossil-based equivalents while cutting cradle-to-gate carbon emissions by up to 50%[2]SABIC, “Certified Circular Polycarbonate Launched in Asia,” sabic.com. Stringent Extended Producer Responsibility rules in Japan and Korea accelerate early adoption, while China’s 2060 carbon-neutral pledge encourages public-private pilot projects to collect post-consumer polycarbonate waste. Capital intensity remains a hurdle, yet joint-venture models that blend petrochemical expertise with waste-management networks are emerging across Singapore and Malaysia. Over the long term, chemically recycled content will migrate from brand-driven niche to baseline compliance, nudging overall regional utilization rates higher as certification audits become mandatory for supplier qualification.

Construction Boom in ASEAN Green-Building Projects

Rapid urbanization across Thailand, Vietnam, and Indonesia boosts demand for energy-efficient glazing in airports, data centers, and mixed-use developments. Polycarbonate’s natural light transmittance, high impact resistance, and UV-blocking coextrusions align with green-building metrics that reward envelope performance. Thailand’s Board of Investment incentives and Malaysia’s Green Building Index credits provide clear monetary benefits for developers who adopt advanced glazing materials. Singapore’s BCA Green Mark framework also lists polycarbonate roofing as a recognized daylighting solution, seeding specification pull throughout ASEAN. Regional humidity and cyclone conditions favor lighter, more flexible sheets over brittle glass, thereby reducing structural steel requirements and overall project costs. Although supply-chain sophistication varies among emerging economies, global producers are deploying prefabricated façade kits that reduce on-site skill bottlenecks and compress construction timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BPA price volatility amid feedstock integration gaps | -0.60% | China manufacturing core with global supply chain impacts | Short term (≤ 2 years) |

| Intensifying intra-APAC overcapacity & price wars | -0.40% | China, Japan, Korea with competitive spillover effects | Medium term (2-4 years) |

| Stricter micro-plastic discharge rules in Japan & Korea | -0.30% | Japan, Korea with potential regional regulatory harmonization | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BPA Price Volatility Amid Feedstock Integration Gaps

Bisphenol A (BPA) remains the critical precursor to virgin polycarbonate, so price gyrations directly influence resin margins, especially for stand-alone extruders lacking backward integration. Chinese BPA capacity additions in 2024 temporarily depressed prices by 15%, but subsequent turnarounds and phenol supply bottlenecks generated a 20% rebound within six months, unsettling annual supply contracts. Vertically integrated leaders, such as Wanhua, are mitigating exposure through captive feedstock, whereas mid-tier converters face squeezed spreads that limit their reinvestment capacity. Environmental regulations governing acetone emissions exacerbate the risk of unplanned outages, introducing additional volatility. Over the near term, the Asia-Pacific polycarbonate market must manage raw-material hedging strategies more tightly to preserve profitability during boom-and-bust feedstock cycles.

Intensifying Intra-APAC Overcapacity & Price Wars

Regional nameplate capacity is outpacing demand, resulting in utilization rates that fall below the economic breakeven point for several commodity producers. Competitive discounting, extended credit terms, and freight-absorption tactics are eroding discipline, with spot prices expected to drift toward cash-cost parity by late 2024. Specialty product differentiation offers some insulation, yet even film and optical-grade segments are beginning to see margin compression as new entrants emulate process technology. While some producers consider mothballing older lines, high exit barriers slow coordinated rationalization, thereby prolonging oversupply. Trade tensions and tariff uncertainties complicate export relief valves, forcing players to double down on cost-efficiency programs. For the Asia-Pacific polycarbonate market, sustained price pressure could delay capital expenditure in recycling or downstream integration, potentially widening technology gaps versus global peers over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Sheets Dominate Amid Films Innovation

Sheets accounted for 45.58% of the Asia-Pacific polycarbonate market share in 2025, driven by robust demand in architectural skylights, machine guards, and automotive glazing, where mechanical rigidity and clarity are key requirements. The segment’s historical scale delivers procurement volumes that keep conversion costs low, encouraging OEM standardization. Even so, sluggish replacement rates in mature end-markets temper volume growth, leaving sheets to expand at a pace similar to that of the broader Asia-Pacific polycarbonate market. Suppliers are responding with UV-coextruded variants and abrasion-resistant grades that lengthen service life in high-traffic applications, nudging the performance envelope rather than radically altering demand dynamics.

Films represent the fastest-growing product category, recording a 5.83% CAGR through 2031 as they deliver thin-gauge benefits vital to flexible circuits, in-mold electronics, and photovoltaic backsheets. Teijin’s biomass-derived lens films demonstrate how sustainability and high refractive index can coexist without sacrificing processability. The Asia-Pacific polycarbonate market size for films is expected to grow as display manufacturers shift to foldable devices that require ultra-thin diffusion layers capable of withstanding tight bending radii. Specialty film converters are investing in plasma-enhanced surface treatments that anchor antimicrobial or anti-fog coatings, thereby adding further breadth of application in medical-device packaging.

By End User Industry: Electronics Leadership Drives Innovation

Electronics captured 47.05% of the Asia-Pacific Polycarbonate (PC) market share in 2025, driven by unrelenting demand for camera lenses, laptop housings, and 5G radio covers that require heat stability and light transmission. Component miniaturization drives down wall thicknesses, but the intrinsic toughness of polycarbonate safeguards against fracture, thereby increasing its market share compared to acrylic alternatives. As smartphones adopt multi-camera arrays with periscope lenses, high-precision molding resins—often modified for their refractive index—gain relevance, reinforcing supplier focus on narrow molecular weight distributions to minimize warpage.

Building and construction applications continue to deliver mid-single-digit growth as green-building certifications proliferate across ASEAN. Transparent roofing for logistics hubs, daylight panels in mass-transit stations, and hurricane-resistant shutters underscore new niches that anchor baseline demand. Packaging, although smaller in volume, is evolving through high-barrier medical blister packs and reheatable food trays, areas where polycarbonate’s thermoformability and sterilization tolerance add value. Industrial machinery adoption centers on guards and housings that must withstand oils, coolants, and repeated impact, while aerospace, though tiny in tonnage, commands premium prices for flame-retardant sheet used in cabin interiors.

Geography Analysis

China retained a commanding 60.12% share of the Asia-Pacific polycarbonate market in 2025, reflecting unparalleled clustering of electronics, automotive, and construction supply chains. Domestic initiatives such as the New Energy Vehicle mandate expand downstream pull, while Wanhua’s integrated BPA-PC complex adds 200 ktpa of optical-grade capacity to cut import dependence and capture higher margins.

Japan and South Korea remain technology-intensive markets where quality assurance frameworks and brand-owner requirements sustain premium pricing. Japan’s Household Appliance Recycling Law and Korea’s Extended Producer Responsibility scheme accelerate the adoption of ISCC PLUS-certified resin, underscoring the strategic importance of chemical recycling investments.

Thailand’s BOI tax holidays and Malaysia’s Green Building Index converge to pull polycarbonate sheet imports for skylight roofing and façade cladding. India’s announced 165 ktpa polycarbonate plant by Deepak Chem Tech will localize supply for domestic EVs and smartphone assembly lines, trimming logistics costs and currency exposure. Australia’s infrastructure stimulus prioritizes cyclone-resistant building materials, creating opportunities for suppliers of thick-gauge sheets that meet wind-load criteria. Across the sub-region, uneven standards make certification services a market differentiator, spurring global suppliers to establish application-development centers in Jakarta and Ho Chi Minh City to accelerate product approval cycles.

Competitive Landscape

The Asia-Pacific Polycarbonate (PC) market exhibits moderate concentration. Global majors, such as SABIC and Covestro, leverage integrated feedstock and proprietary reactor technologies, while regional champions, like Wanhua and LG Chem, exploit cost advantages and local distribution networks. Price competition, however, remains intense. Chinese state-backed entrants continue to scale nameplate capacity, forcing incumbents to adopt flexible tolling agreements and demand-responsive operating schedules. Southeast Asian converters, buoyed by favorable power tariffs, chip away at commodity-grade imports by curating agility on small-volume runs.

Asia-Pacific Polycarbonate (PC) Industry Leaders

Covestro AG

Mitsubishi Chemical Corporation

LOTTE Chemical Corporation

LG Chem

SABIC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Haldia Petrochemicals Ltd., a petrochemical producer in India, unveiled its plan to set up a polycarbonate production facility in West Bengal, backed by an investment of USD 1 billion. By opting to utilize the available land at its current Haldia site, the company underscores its strategic move to diversify deeper into the downstream chemical sector.

- June 2024: Teijin Limited announced that a new, additional production line for its polycarbonate resin Panlite sheet and film, located at its Matsuyama plant in Japan, will begin operation. The company invested in this new line to meet growing demand for high-quality automotive interior parts and in-vehicle electronic components, such as displays and touch screens.

Asia-Pacific Polycarbonate (PC) Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Australia, China, India, Japan, Malaysia, South Korea are covered as segments by Country.| Sheets |

| Films |

| Others (Fibers, etc.) |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| China |

| India |

| Japan |

| Malaysia |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Product Form | Sheets |

| Films | |

| Others (Fibers, etc.) | |

| By End User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | China |

| India | |

| Japan | |

| Malaysia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polycarbonate market.

- Resin - Under the scope of the study, virgin polycarbonate resin in its primary forms such as powder, granule, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms