Europe Polycarbonate (PC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

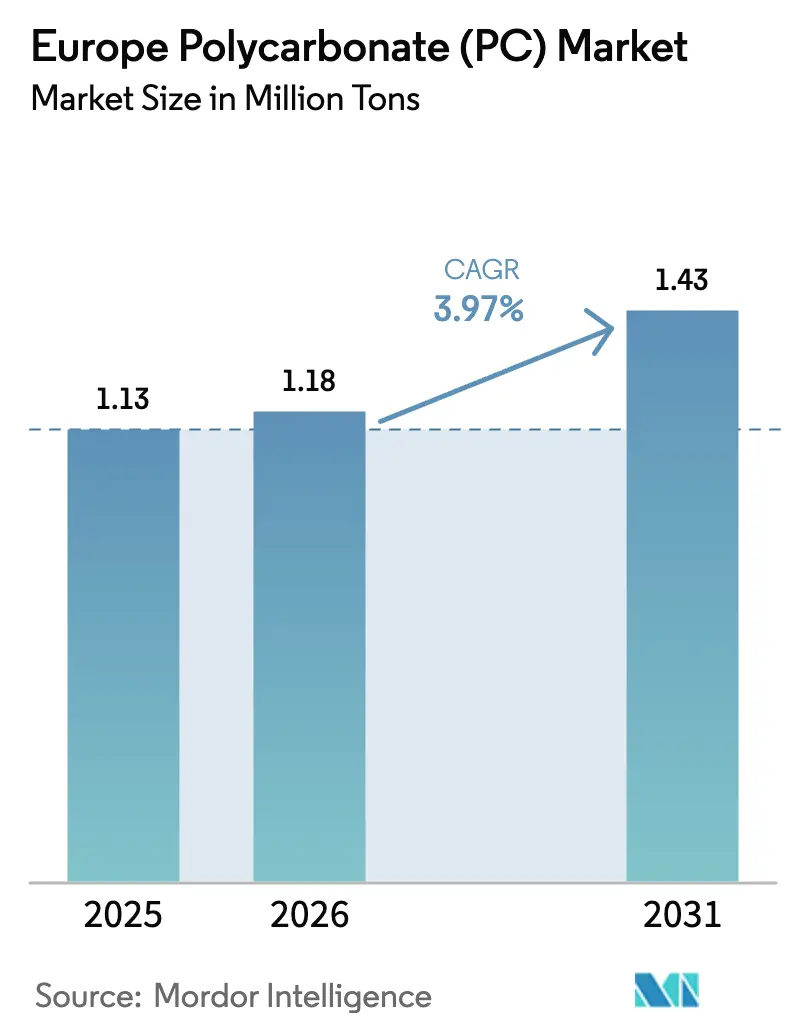

| Base Year Market Size (2025) | 1.13 Million tons |

| Market Volume (2026) | 1.18 Million tons |

| Market Volume (2031) | 1.43 Million tons |

| Growth Rate (2026 - 2031) | 3.97% CAGR |

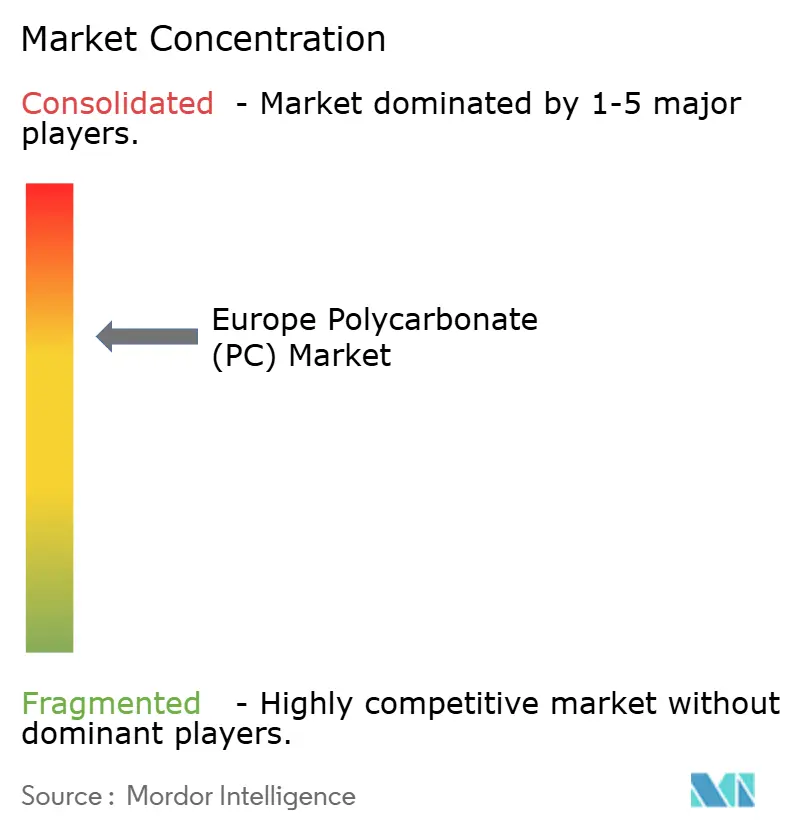

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Polycarbonate (PC) Market Analysis by Mordor Intelligence

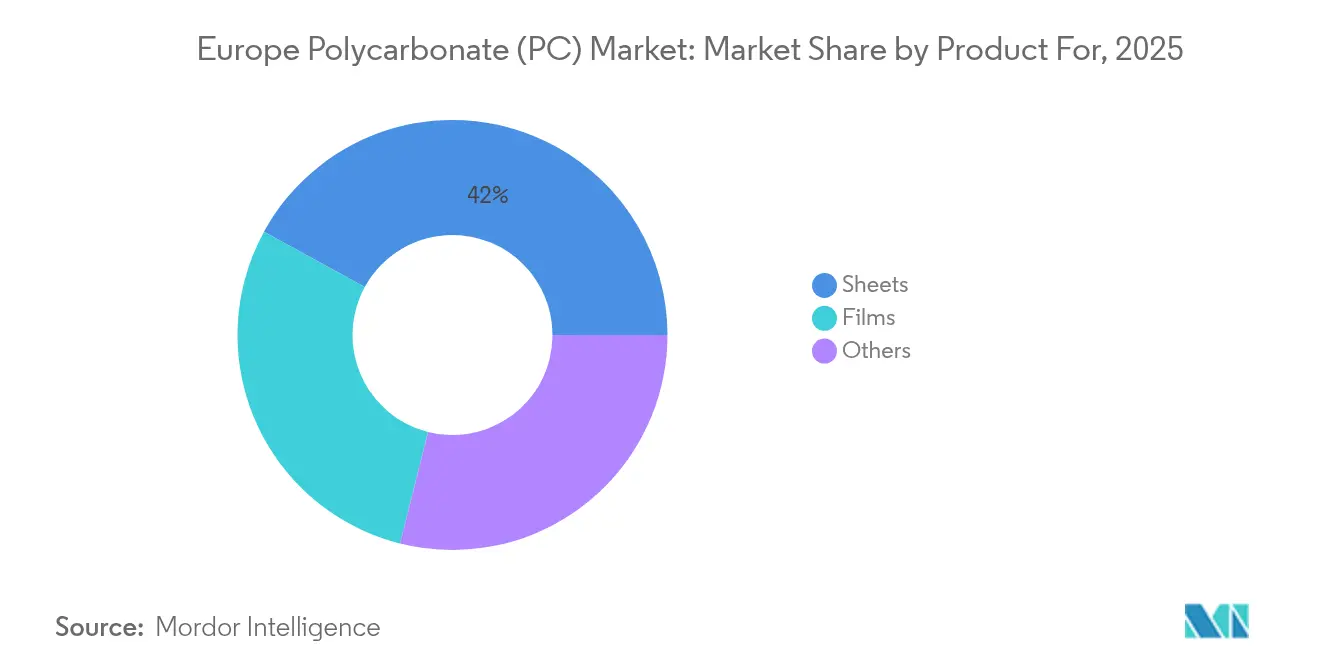

The Europe Polycarbonate (PC) market size was valued at 1.13 million tons in 2025 and estimated to grow from 1.18 million tons in 2026 to reach 1.43 million tons by 2031, at a CAGR of 3.97% during the forecast period (2026-2031). This outlook captures a market caught between regulatory disruption, structurally high energy costs, and capacity rationalization that is already removing commodity volumes from the regional supply base. Sheets retain a commanding 42.51% share of overall consumption, underpinned by glazing, construction, and large‐format automotive parts. Films, propelled by 5G devices and advanced driver-assistance systems, deliver the fastest 4.83% CAGR, demonstrating that thin-gauge, value-added formats absorb demand even as bulk grades decline. Meanwhile, persistent energy price premiums in the United States and the Middle East Gulf hamper European cost competitiveness, forcing producers to pivot toward higher-margin copolymers and circular content offerings that help defend prices. Trinseo’s shuttering of 160,000 t/y in Germany and Covestro’s Antwerp specialty line reveal the twin playbook of trimming surplus capacity and upgrading the mix to sustain the European polycarbonate market.

Key Report Takeaways

- By product form, sheets led with 42.02% of the Europe Polycarbonate (PC) market share in 2025, while films are projected to post the strongest 4.74% CAGR through 2031.

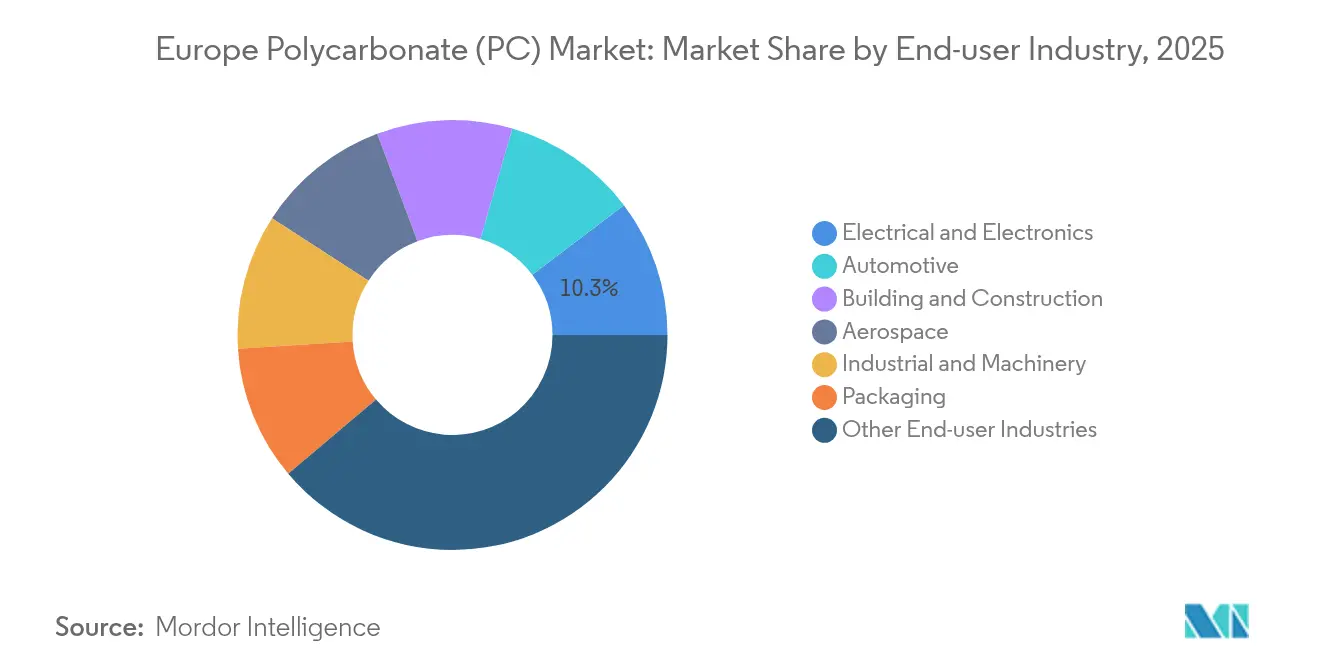

- By end-user industry, the Other End-user Industries segment accounted for a 38.84% share of the Europe Polycarbonate (PC) market size in 2025; the electrical & electronics segment recorded the highest CAGR of 5.72% from 2025 to 2031.

- By geography, the Rest of Europe commanded a 49.85% share of the Europe Ppolycarbonate (PC) market in 2025, whereas the United Kingdom is set to expand at a leading 4.49% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Polycarbonate (PC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-ready lightweighting push from EU Fit-for-55 package | +1.1% | EU core markets, spillover to UK | Medium term (2-4 years) |

| Rapid scale-up of advanced recycling via chemical depolymerization pilots | +0.9% | Germany, Netherlands, Belgium | Long term (≥ 4 years) |

| Electrification of buildings surges low-smoke, flame-retardant PC cabling components | +0.8% | EU-wide, strongest in Germany, France | Short term (≤ 2 years) |

| Re-shoring of medical device molding after COVID-19 supply shocks | +0.7% | Germany, Ireland, Switzerland | Medium term (2-4 years) |

| Solar-agrivoltaics glazing incentives in CAP reform | +0.6% | Southern Europe, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-ready lightweighting push from EU Fit-for-55 package

The EU Fit-for-55 rules drive automakers to reduce emissions by 55% by 2030, compelling aggressive mass reduction strategies that favor high-modulus polycarbonate over steel or glass. Covestro’s APEC XT launch targets sensor housings that must remain dimensionally stable at elevated EV power-train temperatures, translating regulatory pressure into real resin demand. Electric-vehicle charging stations also specify flame-retardant, UV-stable housings, further lifting volumes. Although 2024 passenger-car builds softened, OEM material engineers continue to pre-qualify copolymer grades ahead of model-year 2026 programs, ensuring the driver remains active through mid-term cycles. Competitive imports from Asia intensify in commodity grades, yet Europe Polycarbonate (PC) market participants that offer validated lightweighting data sheets maintain a pricing edge.

Rapid scale-up of advanced recycling via chemical depolymerization pilots

Chemical depolymerization, now being piloted in Germany, the Netherlands, and Belgium, breaks down post-consumer polycarbonate into BPA and DPC monomers, allowing for the production of virgin-quality re-polymerization. SABIC’s first circular grade demonstrates proof of concept, while Covestro pledges full circularity by 2050, placing early adopters at a reputational advantage in sustainability-driven tenders[1]European Union, “Construction Products Regulation 2024/3110,” europa.eu. Scaling factors—such as feedstock aggregation, solvent recovery economics, and offtake agreements—determine cost parity; however, EU product-passport rules, starting in 2026, guarantee a regulatory pull. As mechanical-recycling limitations surface in optical applications, chemical routes widen the addressable market, giving the Europe Polycarbonate (PC) market a new secondary raw-material pool that tempers virgin demand growth but extends value capture for integrated producers.

Electrification of buildings surges low-smoke, flame-retardant PC cabling components

EU directives on energy-efficient retrofits generate elevated cabling densities in confined shafts, thereby escalating fire safety standards. Halogen-free, low-smoke polycarbonate conduits satisfy EN 50575 CPR Class B-s1-d0 requirements without heavy additive packages, providing installers with lighter, recyclable systems. Retrofit programs in Germany and France prioritize rapid installation, where sheet-based trunking solutions shorten labor times. Demand links directly to public-sector renovation grant disbursement, making the driver most potent in 2025-2027. Commodity conduit suppliers attempt polypropylene alternatives; however, warpage at 110°C service undermines bids, keeping flame-retardant polycarbonate as the reference substrate.

Re-shoring of medical device molding after COVID-19 supply shocks

OEM audits following 2020 disruptions revealed regional redundancy gaps, prompting global device majors to pair existing U.S. tooling with EU molds. High-clarity, medical-grade polycarbonate secures the housings of diagnostic analyzers now manufactured in Ireland and the German Rhineland, thereby embedding local polymer consumption throughout the full product lifecycle[2]British Plastics Federation, “Engineering Thermoplastics Market Update,” bpf.co.uk. Regulatory filings lock material specifications for up to 10 years, creating stickiness that resists imported substitution. Although device capital spending follows protracted validation cycles, approved projects ensure a steady mid-term uplift to the Europe Polycarbonate (PC) market that partially offsets cyclical softness in automotive resin offtake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BPA Authorisation review tightening & potential sunset for food-contact PC | -0.80% | EU-wide, particularly Germany, France | Short term (≤ 2 years) |

| Structural energy-price premium versus US & ME Gulf | -0.50% | EU core manufacturing regions | Medium term (2-4 years) |

| Slow roll-out of ELV dismantling tech for coated PC glazing | -0.40% | Germany, France, Italy, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BPA authorization review tightening & potential sunset for food-contact PC

ECHA’s re-evaluation of BPA shifts from hazard identification to potential market authorizations, indicating that water-cooler bottles and baby-feeding products may be removed from the commerce channel by 2026. Converters hesitate to retool lines due to an uncertain payback horizon, which freezes procurement and erases volumes equivalent to nearly 1% of 2024 consumption. Producers explore BPA-free copolyesters, yet qualification costs limit near-term substitution. Brand owners pre-emptively delist BPA-based polycarbonate articles, accelerating demand attrition before a legal cut-off.

Structural energy-price premium versus US & ME Gulf

Natural-gas costs, averaging EUR 31/MWh in 2024, sat roughly three times the US Henry Hub equivalents, while grid electricity remained twice the Middle East benchmarks. For phosgene-based polymerization, energy costs can account for up to 17% of total operating expenses, making European commodity output structurally loss-making when Asian imports flood the docks of Antwerp and Hamburg. Spot-market quotes in September 2024 undercut local offers by USD 250/t, resulting in asset underutilization across three major sites. Integrated players are now accelerating a shift towards specialty copolymers and recycled content resin, where price premiums exceed the energy penalty; however, the restraint lingers until EU energy reforms or long-term LNG contracts narrow the gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Sheets anchor legacy volumes while films unlock high-growth optics

Sheets captured the largest 42.02% share of the Europe Polycarbonate (PC) market in 2025. Roofing, sound-barrier, and protective-glazing systems consumed the bulk of these volumes, leveraging the material’s 250 times impact resistance over glass and inherent UV stability. Projects under Germany’s building-renovation wave specify multiwall sheets to satisfy thermal-transmittance limits while minimizing structural retrofit costs. Nonetheless, energy-driven cost inflation prompted contractors to substitute lower-priced acrylic in non-load-bearing awnings, tempering growth. Sheet processors maintain differentiation through co-extruded hard-coat layers that meet EN 356 P8B security glazing grades, securing orders for rail station refurbishments that extend into 2027.

Films represent the fastest-growing contributor to the Europe Polycarbonate (PC) market size, with a 4.74% CAGR through 2031. Touch-panel substrates, high-definition holographic security foils, and flexible printed circuits increasingly rely on optical-grade films with thicknesses of 50–125 µm. 5G mmWave antenna windows require low-loss-tangent dielectrics; polycarbonate films outclass PET and PMMA, commanding USD 30–38/kg contract prices. Automotive HUD systems fuel additional demand: Tier-1s adopt birefringence-controlled film stacks that maintain display readability at -30°C. Covestro’s launch of flame-retardant film grades rated V-0 at 50 µm thickness positions European film extruders to defend their share against Asian imports. Alignment of film properties with stringent IEC 62031 LED substrate norms establishes a premium niche, shielding this sub-segment from commodity price fluctuations in bulk sheet.

By End-User Industry: Diversified pull reduces cyclicality

Other End-user Industries led with 38.84% of the Europe Polycarbonate (PC) market share in 2025, spanning aerospace canopies, medical diagnostic housings, and industrial sight-glass panels. Aerospace demand concentrates in France and Germany, where POLYVANTIS markets glass-fiber-reinforced sheet that meets FAR 25.853. Industrial machinery uses clear guarding to comply with the EU Machinery Regulation 2023/1230, sustaining baseline demand even during automotive downturns.

Electrical & Electronics posts the highest 5.72% CAGR through 2031 for the Europe Polycarbonate (PC) market. Consumer electronics miniaturization necessitates thin-wall flame-retardant enclosures that withstand 125°C reflow cycles. 5G antenna radomes adopt low-dk polycarbonate to enhance signal transparency versus ABS. The shift to silicon-carbide power modules in EV chargers increases operating temperatures, prompting OEMs to use high-heat copolymers. SABIC’s December 2024 LNP ELCRES CXL launch, certified ISCC PLUS, captures this premium. Electrical builders’ hardware—junction boxes, DIN-rail components—further widens the demand base as residential PV installations are expected to double by 2028 in Spain and Italy.

Geography Analysis

The Rest of Europe commanded 49.85% of the Europe Polycarbonate (PC) market in 2025, reflecting the aggregated pull from Switzerland’s medical cluster, Austria’s sheet extrusion hubs, and the Nordic region’s renewable-energy hardware. Switzerland alone consumes a substantial amount annually for in-vitro diagnostics and surgical tools, benefiting specialty-grade import flows through Basel’s logistics corridor. Nordic markets, leveraging government incentives, specify multiwall sheets in agricultural PV roofs, translating climate policy into resin offtake.

The United Kingdom (UK) records the quickest 4.49% CAGR as Brexit realigns supply chains. Domestic converters expand their sourcing beyond continental Europe, and the UKCA conformity scheme offers a semi-autonomous regulatory route that large OEMs utilize to expedite product launches. EV battery-plant investments in the West Midlands funnel incremental demand for 120°C-rated cell brackets and pack covers, keeping the UK’s share of the Europe Polycarbonate (PC) market size on a rising trajectory despite macroeconomic headwinds.

Germany, France, and Italy exhibit mature yet stabilizing demand. German OEMs’ slow recovery from 2024 vehicle output lows caps immediate volume upside, but Fit-for-55 timelines guarantee renewed raw-material calls from 2027 model years. France’s aerospace and nuclear industries generate steady, specification-driven resin demand, while Italy’s packaging machinery exports secure specialty sheet orders resilient to fluctuations in domestic GDP. Russia remains a self-contained node: sanctions curb EU exports, but SIBUR projects a 10-20% expansion in polymer demand within its captive automotive sector. The bifurcated trade environment limits direct volumes in the Europe Polycarbonate (PC) market yet reminds EU suppliers of the importance of multi-geography risk balancing.

Competitive Landscape

The Europe Polycarbonate (PC) market is concentrated. Capacity rationalization and specialization coexist in a market where surplus commodity capacity collides with structurally high energy costs. Imports from Asia remain structurally lower in cost, but European OEMs value proximity, regulatory expertise, and just-in-time delivery. Consequently, the market tilts toward a barbell structure, with large multinationals supplying high-specification resins and local compounders tailoring niche batches. Digital product-passport requirements from 2026 intensify the technology arms race; companies with robust data-management architectures will outpace smaller rivals that are unable to substantiate their cradle-to-gate footprints.

Europe Polycarbonate (PC) Industry Leaders

Covestro AG

SABIC

Trinseo

LG Chem

LOTTE Chemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Avient Corporation announced the addition of new grades to its portfolio of recycled-content polycarbonate (PC) and PC blends, developed to meet the growing demand for materials that support sustainability in the electrical and electronics (E&E) industry in the Europe, Middle East, and Africa (EMEA) regions.

- July 2025: Exolon Group SpA announced to acquire the AkyVer polycarbonate sheet business from Corplex (Kaysersberg, France). The acquired product portfolio comprises a range of polycarbonate multiwall sheets, panel products, and sheet systems. Production of these items will be integrated into the manufacturing facility of Exolon Group S.p.A. in Nera Montoro, Italy.

Europe Polycarbonate (PC) Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. France, Germany, Italy, Russia, United Kingdom are covered as segments by Country.

| Sheets |

| Films |

| Others (Fibers, etc.) |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| France |

| Germany |

| Italy |

| Russia |

| United Kingdom |

| Rest of Europe |

| By Product Form | Sheets |

| Films | |

| Others (Fibers, etc.) | |

| By End User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | France |

| Germany | |

| Italy | |

| Russia | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polycarbonate market.

- Resin - Under the scope of the study, virgin polycarbonate resin in its primary forms such as powder, granule, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms