South America Polyamide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

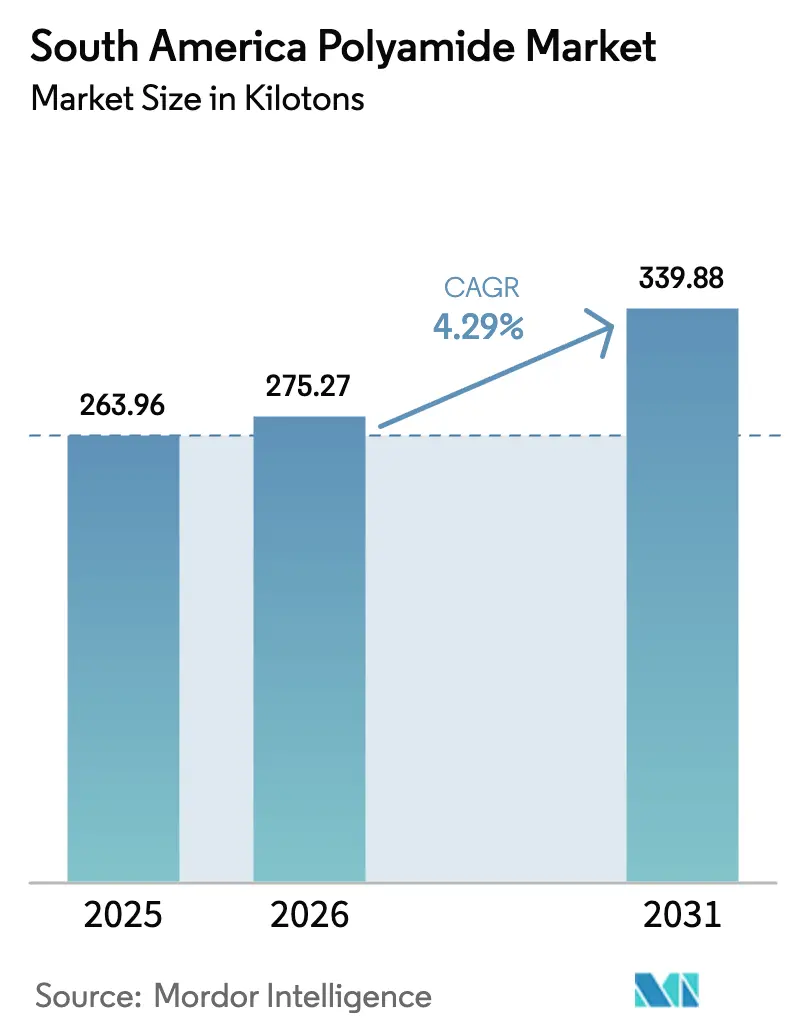

| Base Year Market Size (2025) | 263.96 kilotons |

| Market Volume (2026) | 275.27 kilotons |

| Market Volume (2031) | 339.88 kilotons |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Polyamide Market Analysis by Mordor Intelligence

The South America Polyamide Market size is expected to grow from 263.96 kilotons in 2025 to 275.27 kilotons in 2026 and is forecast to reach 339.88 kilotons by 2031 at 4.29% CAGR over 2026-2031. This steady expansion is powered by rising demand for lightweight, high-strength engineering plastics in automotive, packaging, and aerospace programs, and it benefits from regional trade frameworks that lower tariff barriers for finished components. Brazil’s integrated petrochemical network supplies competitive feedstock access, while recent antidumping measures protect domestic producers against low-cost imports, encouraging additional capacity investment. Argentina is capturing a growing share of cross-border component production as its regulatory environment aligns with Brazil’s homologation standards, stimulating unified product specifications across multiple end-user sectors. Producers that combine technical service, local compounding, and bio-based resin development are best positioned to meet sustainability targets and deliver consistent quality for high-value applications.

Key Report Takeaways

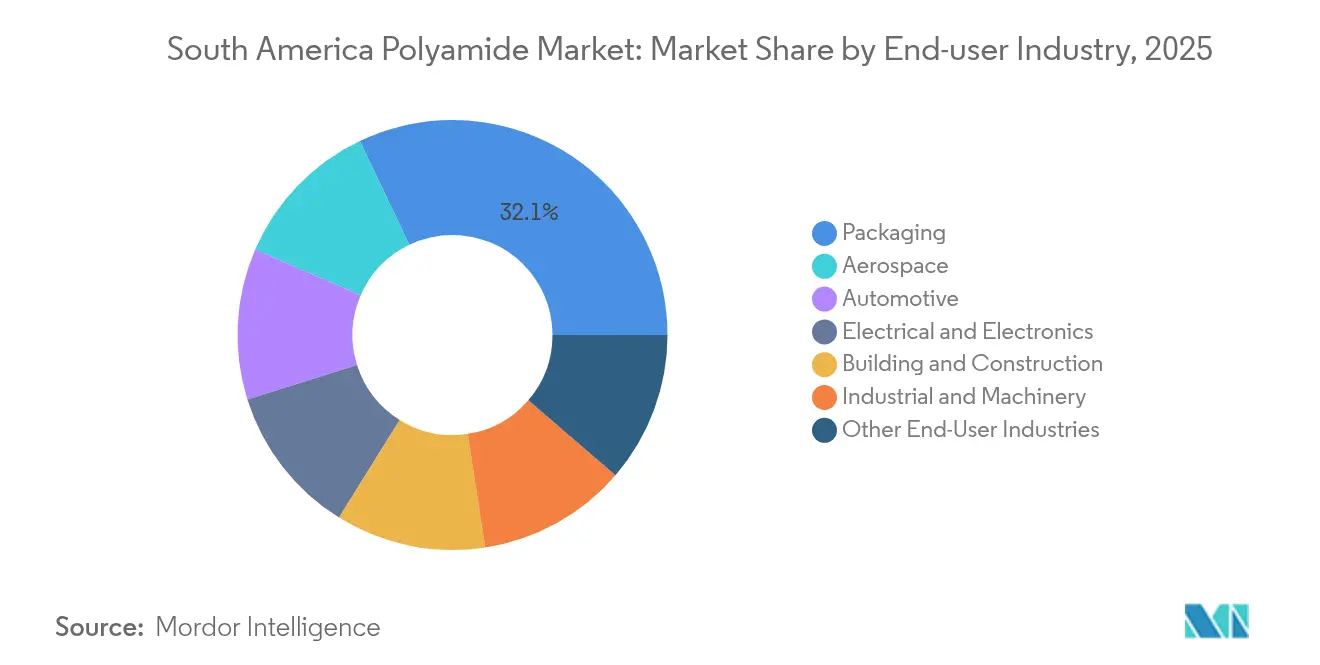

- By end-user industry, packaging led with 32.10% of the South America polyamide market share in 2025; aerospace is projected to expand at a 6.04% CAGR through 2031.

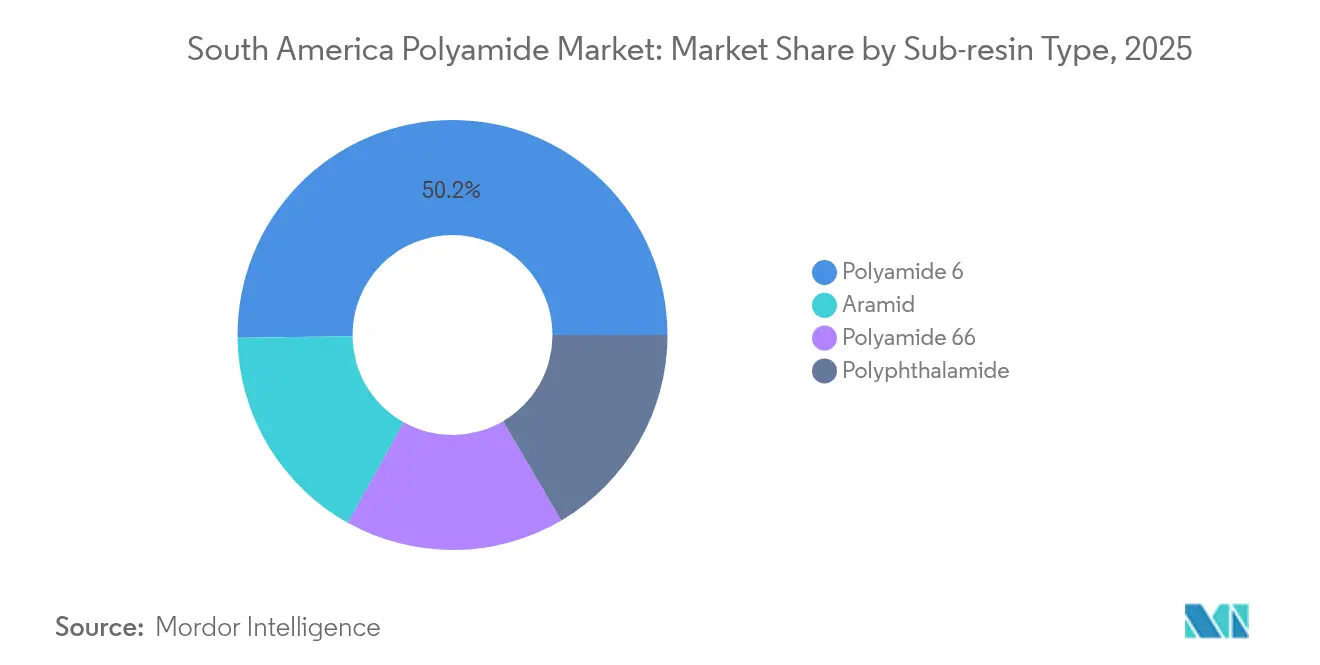

- By sub-resin type, polyamide 6 captured 50.20% share of the South America polyamide market size in 2025, while aramid fibers are advancing at a 5.18% CAGR to 2031.

- By geography, Brazil accounted for 72.70% of the South America polyamide market size in 2025; Argentina is forecast to post a 6.45% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Polyamide Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive lightweighting push post-2025 | +1.2% | Brazil core, Argentina emerging | Medium term (2-4 years) |

| Bio-based PA 6,10 capacity expansions in Brazil | +0.8% | Brazil primary, regional spillover | Long term (≥ 4 years) |

| EU-Mercosur trade deal boosting exports | +0.9% | Regional, EU export focus | Medium term (2-4 years) |

| Near-shoring of electronics assembly into Brazil | +0.7% | Brazil concentrated | Short term (≤ 2 years) |

| Lithium-ion battery separator film demand | +0.5% | Regional, mining states priority | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automotive Lightweighting Push Post-2025

Automakers in Brazil and Argentina are mandated to cut fleet emissions, which translates into vehicle weight reduction targets that elevate the role of engineering plastics. New homologation rules signed in 2024 allow components approved in either country to circulate region-wide, helping suppliers streamline part designs and validation requirements[1]Ministerio de Economía, “Resolución 114/2024,” argentina.gob.ar. Nylon components already used in air-intake manifolds, radiator end-tanks, and battery enclosures can contribute as much as 40 kg of weight savings per vehicle, and demand intensifies as electric vehicle platforms multiply. Established polymer processors have started dedicated production cells for under-the-hood polyamide 66 parts that must handle continuous temperatures above 120 °C. OEMs also specify glass-fiber-reinforced grades to meet mechanical performance thresholds, making compound formulation expertise a competitive differentiator.

Bio-based PA 6,10 Capacity Expansions in Brazil

Castor-oil and sugarcane derivatives give Brazilian producers a robust pathway toward 100% renewable polyamide 6,10, satisfying corporate carbon-neutral pledges without major performance trade-offs[2]Simanke et al., “Recent advances in biobased materials and value-added chemicals,” aiche.org. Pilot plants demonstrate 20% lower life-cycle emissions than conventional PA 6, and automotive tier suppliers have accepted moderate price premiums to secure first-mover advantages in sustainable components. Packaging converters target cosmetics and personal-care brands that require high oxygen- and aroma-barrier films yet insist on renewable content certification. Commercial viability hinges on scaling dehydration and polymerization units above 30 kilo tons per year, which requires joint ventures between resin producers and agricultural processors.

EU-Mercosur Trade Deal Boosting Exports

The agreement slashes import duties on many chemical intermediates, giving South American processors cost-effective access to European markets. Specialty film and fiber manufacturers can ship certified sustainable products under preferential tariffs, a benefit that grows as the EU enforces stricter carbon-border adjustment rules. Compliance, however, demands traceability for all bio-based inputs, and mid-tier processors are investing in blockchain-enabled supply-chain platforms to document farm-level sourcing data. Large integrated producers capitalize on their existing sustainability audits and third-party certifications to maintain a competitive edge and secure long-term offtake contracts.

Lithium-ion Battery Separator Film Demand

Battery cell makers in Chile, Brazil, and Argentina’s lithium triangle regions specify nylon-based separator films that outperform polyethylene in puncture resistance and thermal stability. Mining firms paired with cathode producers advocate local chemical value-addition, which sets the stage for regional nylon film plants. Though current volumes remain small, multi-gigawatt-hour cell factory announcements project compounded growth that underpins long-term contracts for specialty polyamide 6 grades with tight molecular-weight distribution.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile adiponitrile and caprolactam prices | -1.1% | Regional, import-dependent | Short term (≤ 2 years) |

| PP and high-performance polyester substitution | -0.7% | Regional, cost-sensitive segments | Medium term (2-4 years) |

| Weak recycling and collection infrastructure | -0.4% | Regional, urban concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PP and High-Performance Polyester Substitution

Flexible packaging converters opt for polypropylene or specialty polyester laminates when nylon prices rise sharply or when barrier requirements are moderate. In appliance housings, short-glass-fiber polypropylene can achieve comparable stiffness at 10-15% lower cost, pressuring polyamide volumes in midrange applications. Automotive interior suppliers have added high-flow PBT grades capable of passing new scratch-resistance tests, limiting polyamide acceptance in certain trim components. Nylon retains an edge in continuous temperature environments, yet its cost differential must narrow to hold share in these cost-sensitive segments.

Weak Recycling and Collection Infrastructure

Automotive OEMs demand at least 20% recycled content in non-safety critical parts, yet local compounders struggle to secure consistent bale purity. Municipal collection programs concentrate in dense urban areas and rarely segregate engineering-grade plastics. Without an extended producer responsibility mandate, infrastructure finance rests on voluntary initiatives that have yet to reach commercial scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user Industry: Packaging Drives Volume Growth

Packaging applications accounted for 32.10% of South America's polyamide market share in 2025 and remain the largest volume consumer because nylon layers extend shelf life for meat, cheese, and cooking oil pouches. The South America polyamide market size for the packaging segment is projected to climb steadily through 2031 as e-commerce food delivery accelerates cold-chain investments. Aerospace, although smaller in absolute tonnage, records the fastest 6.04% CAGR thanks to Embraer’s composite wing demonstrator that specifies carbon-fiber prepregs reinforced with PA 6 tougheners.

Polyamide suppliers serving packaging lines differentiate through cast-film flatness control and co-extrusion adhesion to EVOH, which lowers material usage without sacrificing barrier properties. Aerospace compounders must meet stringent out-gassing and flame-smoke-toxicity thresholds, reinforcing the value of tight process monitoring. Automotive customers require rapid color matching for engine-compartment components exposed to UV and under-bonnet heat; multi-layer injection with metal inserts demands precise mold-flow simulation. As a result, service capability, not just resin availability, largely dictates market capture across these varied end-user segments.

By Sub-Resin Type: Specialty Grades Command Premium Growth

Polyamide 6 represented 50.20% share of the South America polyamide market in 2025, reflecting its favorable cost-to-performance balance and well-established supply chains. The South America polyamide market size for PA 6 will continue to expand on the back of packaging and monofilament applications that capitalize on the resin’s exceptional oxygen-barrier properties. Polyamide 66 maintains relevance as vehicle powertrains evolve toward higher operating temperatures, and regional demand remains resilient even as internal-combustion engines concede share to hybrids.

Aramid fibers enjoy a 5.18% CAGR, buoyed by aerospace and defense procurement of ballistic panels, protective apparel, and reinforcement fabrics where extreme tensile strength-to-weight ratios justify premium pricing. Polyphthalamide, though small in tonnage, enables precision electronics connectors by sustaining mechanical integrity at solder-reflow temperatures, underscoring its strategic value for near-shored electronics assembly.

Geography Analysis

Brazil dominated with 72.70% of South America polyamide market share in 2025, and its position is underpinned by domestic petrochemical integration, a robust automotive cluster, and a fast-growing electronics sector. The South America polyamide market thus achieves economies of scale from shared logistics corridors that link resin producers in the Southeast to automotive plants in São Paulo and Minas Gerais. Federal tariff hikes from 12.6% to 20% on selected polymer imports lock in a cost advantage for local suppliers, while antidumping cases against Asian fiber producers shelter domestic filament spinners.

Argentina, although smaller in absolute tonnage, is the fastest-growing geography with a 6.45% CAGR forecast to 2031. Manufacturing revitalization plans prioritize automotive components, agricultural machinery, and aircraft parts, all of which lean on high-performance polyamide grades for durability and lightweighting. The Argentina-Brazil vehicle homologation accord allows components produced in either country to circulate freely, removing duplicative approval steps and reducing time to market for Argentine suppliers. Decree 1/2025 opens the door to certified non-hazardous waste imports, encouraging post-consumer nylon recycling streams that could feed local compounders targeting OEM recycled-content mandates.

The Rest of South America, comprising Colombia, Chile, Peru, and smaller Andean markets, makes up the remainder of volume and exhibits diverse demand drivers. Colombia’s ban on single-use plastics forces packaging producers to explore recyclable multi-layer films, potentially lifting nylon usage where barrier performance is critical. Mining expansion in Chile and Peru propels industrial conveyor belts and wear components molded from abrasion-resistant PA 6 compounds.

Competitive Landscape

The South American polyamide market is moderately fragmented. RadiciGroup, leveraging its expertise in high-performance fibers, scaled up glass-fiber-reinforced nylon compounding lines in São Paulo state to tackle under-the-hood and electrical connector opportunities. Braskem focuses on developing bio-based polyamides in collaboration with academic institutions, targeting consumer brands seeking renewable content certificates. Ascend Performance Materials extends its Latin American reach through distribution agreements that place engineered compounds closer to converters’ floors, emphasizing rapid technical-service turnaround.

South America Polyamide Industry Leaders

Ascend Performance Materials

BASF

Domo Chemicals

DSM-Firmenich

UBE Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Brazil’s Health Regulatory Agency opened consultation on adding polyamide-imide 2 to the authorized polymers list for food-contact plastics, setting migration limits that align with Mercosur standards.

- March 2024: Ascend Performance Materials selected Snetor as its first Latin American distribution partner for polyamide-based engineered materials, expanding regional compound availability.

South America Polyamide Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Aramid, Polyamide (PA) 6, Polyamide (PA) 66, Polyphthalamide are covered as segments by Sub Resin Type. Argentina, Brazil are covered as segments by Country.| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-User Industries |

| Aramid |

| Polyamide 6 |

| Polyamide 66 |

| Polyphthalamide |

| Argentina |

| Brazil |

| Rest of South America |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-User Industries | |

| By Sub-Resin Type | Aramid |

| Polyamide 6 | |

| Polyamide 66 | |

| Polyphthalamide | |

| By Geography | Argentina |

| Brazil | |

| Rest of South America |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyamide market.

- Resin - Under the scope of the study, virgin polyamide resins like Polyamide 6, Polyamide 66, Polyphthalamide, and Aramid in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms