South America IT Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

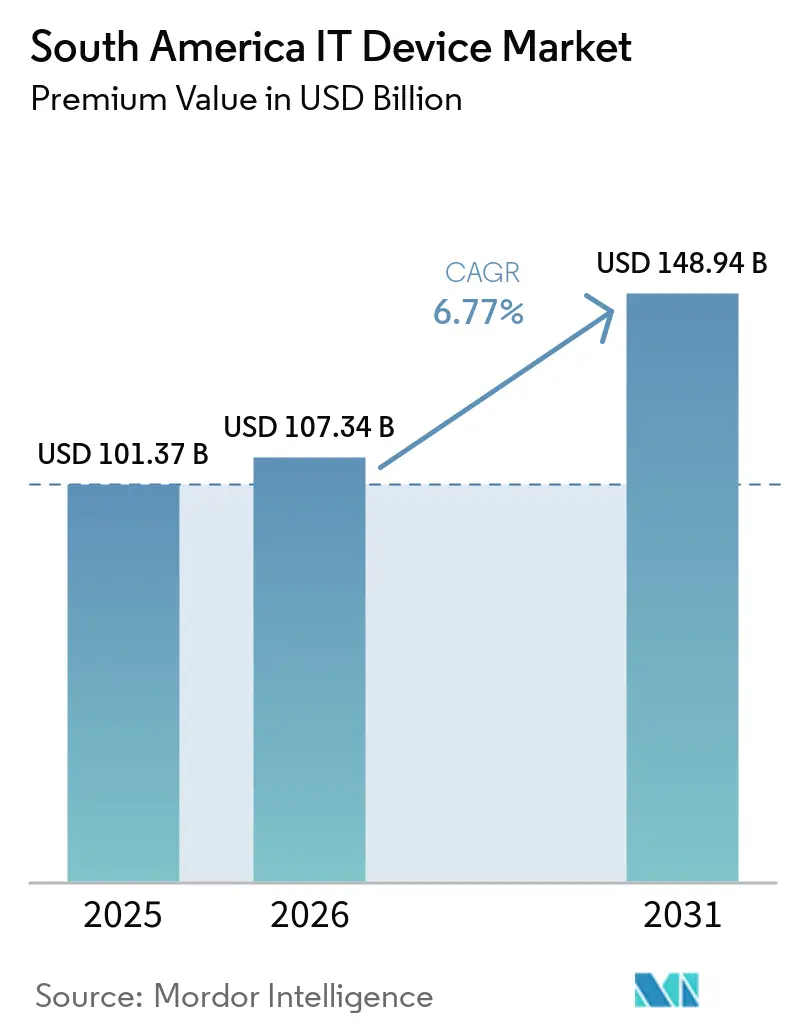

| Base Year Market Size (2025) | USD 101.37 Billion |

| Market Size (2026) | USD 107.34 Billion |

| Market Size (2031) | USD 148.94 Billion |

| Growth Rate (2026 - 2031) | 6.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America IT Device Market Analysis by Mordor Intelligence

The South America IT device market size was valued at USD 101.37 billion in 2025 and estimated to grow from USD 107.34 billion in 2026 to reach USD 148.94 billion by 2031, at a CAGR of 6.77% during the forecast period (2026-2031). Demand is shifting away from purely cyclical replacement toward structurally higher volumes as Brazil’s PIX instant-payment platform spreads installment financing, the Manaus Free Trade Zone attracts assembly lines that shorten lead times, and enterprises prioritize cloud-ready endpoints over on-premises hardware. Smartphones continued to anchor spending, yet fitness-centric wearables and 2-in-1 notebooks are climbing fastest as insurers and hybrid-work mandates reshape buying priorities. Online retail is eclipsing physical stores in tier-2 cities, and premium devices are gaining share because financing programs distribute the upfront outlay over 12-18 months. Currency fluctuations and memory-component shortages temper the outlook, but diversified semiconductor sourcing and local manufacturing cushion some price shocks for the South America IT device market.

Key Report Takeaways

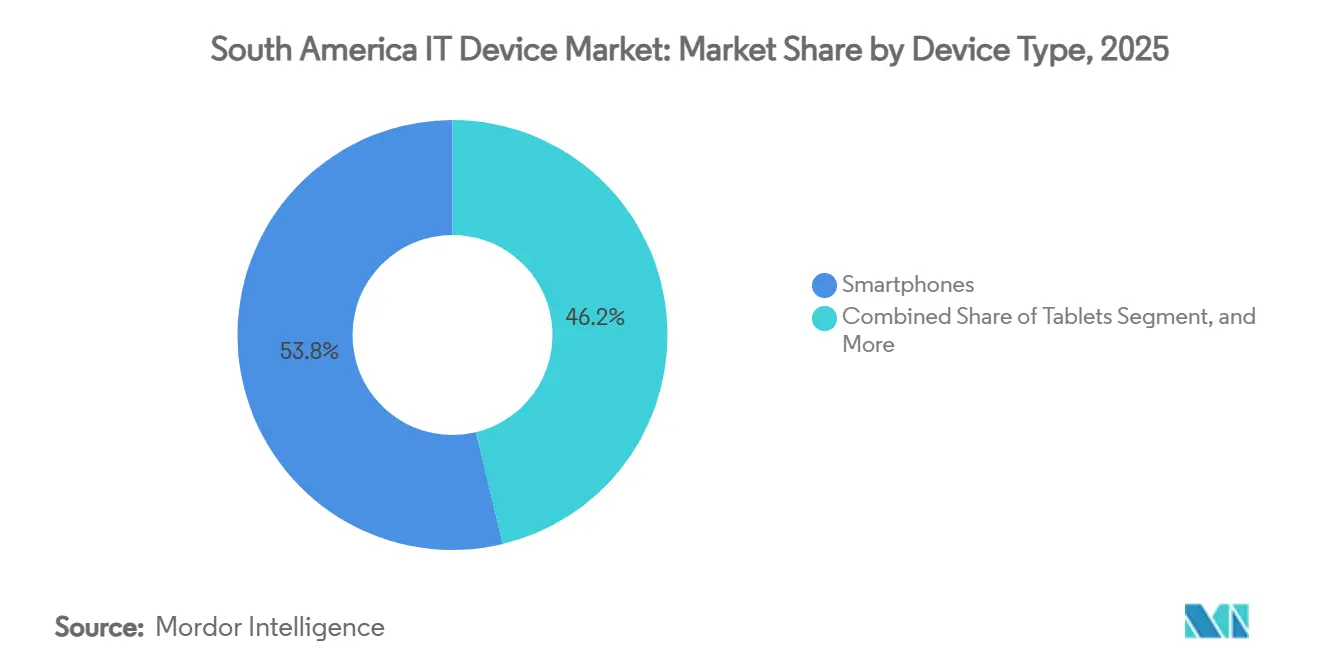

- By device type, smartphones led with 53.76% revenue share in 2025, while wearables are advancing at a 7.77% CAGR through 2031.

- By end-user industry, the consumer segment commanded 65.12% of revenue in 2025, whereas enterprise procurement is projected to expand at a 7.37% CAGR over 2026-2031.

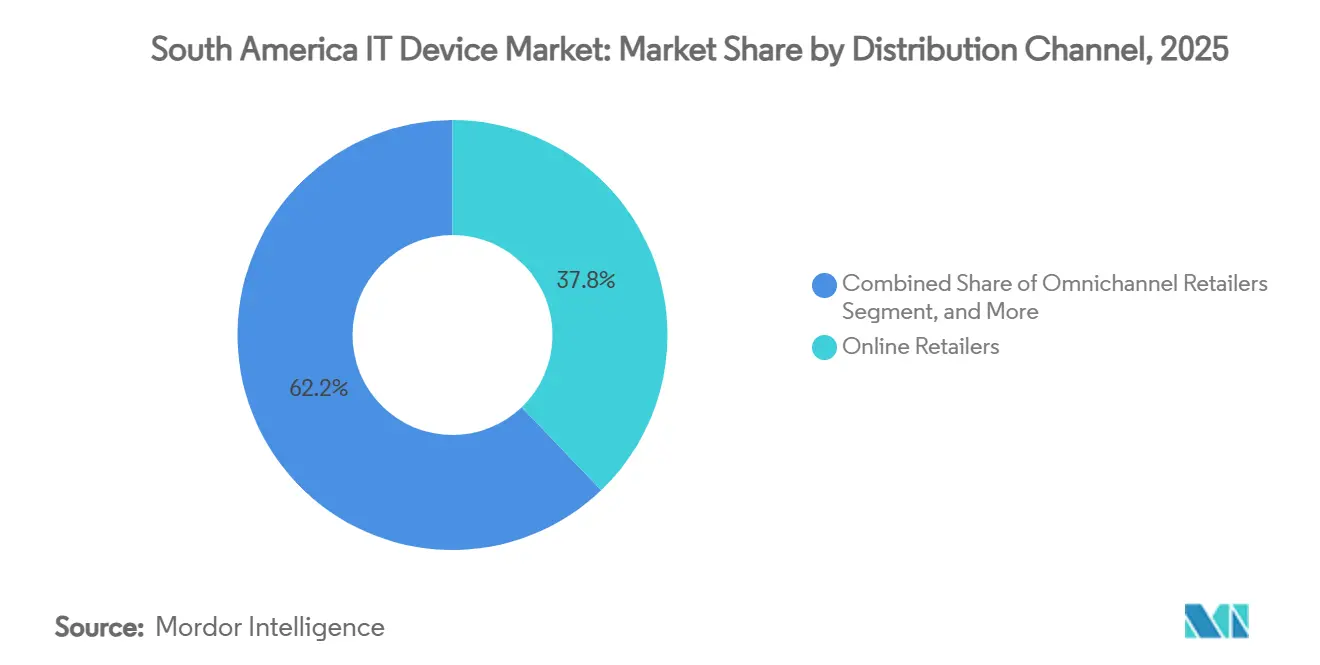

- By distribution channel, online retailers captured 37.84% share in 2025 and are growing at a 7.17% CAGR, outpacing all store-based formats.

- By price band, the budget tier below USD 200 represented 48.32% of unit sales in 2025, yet the premium tier above USD 601 is rising at a 7.48% CAGR as installment financing unlocks aspirational demand.

- By geography, Brazil accounted for 53.39% of regional revenue in 2025; Colombia is forecast to post the fastest growth at a 7.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America IT Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Middle-Class Smartphone Penetration | +1.2% | Brazil, Mexico, Colombia, Argentina | Medium term (2-4 years) |

| Shift to Remote and Hybrid Work Boosting PC and Tablet Demand | +1.0% | Brazil, Mexico, Chile, Colombia | Short term (≤ 2 years) |

| E-commerce Growth Accelerating Online Device Sales | +0.9% | Brazil, Mexico, Argentina | Medium term (2-4 years) |

| Manaus Free Trade Zone Tax Incentives Enabling Local Assembly Lines | +0.7% | Brazil, regional exports | Long term (≥ 4 years) |

| PIX Instant-Pay Installment Scheme Unlocking High-Ticket Device Purchases | +0.6% | Brazil | Short term (≤ 2 years) |

| Semiconductor Supply Diversification Mitigating Price Volatility | +0.4% | Global, Brazil and Mexico assembly gains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Middle-Class Smartphone Penetration

Rising disposable incomes in Brazil, Mexico, and Colombia are converting feature phone users into smartphone owners, lifting mobile internet penetration to 84% in Brazil in 2025. Secondary cities posted double-digit shipment gains as 4G coverage expanded to 92% of households and carriers bundled entry-level 5G handsets at below USD 200. Samsung’s Galaxy A07 5G debut in Peru in 2026 illustrates how vendors compress costs to target first-time upgraders. Remittance inflows of USD 63.3 billion into Mexico funded premium upgrades, pushing devices above MXN 10,000 (approximately USD 588) to a 17.1% share in Q3 2025. Together, these trends enlarge the addressable base for the South America IT device market.

Shift to Remote and Hybrid Work Boosting PC and Tablet Demand

Corporate hardware budgets pivoted to notebooks and tablets as hybrid work became entrenched, lifting Brazil’s ICT hardware outlays to USD 43.2 billion in 2024, or 48% of total ICT spend. Enterprises now request AI-accelerated chipsets that enable on-device translation and noise suppression, and Lenovo’s 2026 tie-up with Positivo to deploy Spark AI workstations underscores the emphasis on edge compute. Rugged tablets are also proliferating in field services, reinforcing device diversity across the South America IT device market.

E-commerce Growth Accelerating Online Device Sales

Online channels accounted for 37.84% of device revenue in 2025 and continue to grow as MercadoLibre and Amazon expanded fulfillment into tier-2 and tier-3 cities. Brazil’s PIX system processed 42 billion transactions in 2025, embedding installment plans that spread device payments across up to 12 months.[1]Banco Central do Brasil, “Pix Completes 4 Years With 42 Billion Transactions in 2024,” bcb.gov.br Same-day delivery now reaches 60% of the Brazilian population, and cross-border platforms let Argentine buyers evade import restrictions by sourcing from Chile and Uruguay. As a result, the South America IT device market is increasingly shaped by digital storefronts rather than physical shelves.

Manaus Free Trade Zone Tax Incentives Enabling Local Assembly Lines

The Manaus cluster generated BRL 209.57 billion (USD 38 billion) in revenue from January to November 2025, sheltering 553 factories that assemble smartphones, tablets, and notebooks.[2]Ministério do Desenvolvimento Indústria Comércio e Serviços, “Polo Industrial de Manaus Fatura R$ 209,57 Bilhões de Janeiro a Novembro de 2025,” gov.br Zero-rated import duties and suspended IPI tax lower landed costs by up to 40%, prompting Samsung, Positivo, and Multilaser to scale production. New entrants Chint, Kaifa, and Megmeet committed a combined BRL 320 million to fresh plants in 2026, broadening the supplier base. The fiscal shield underpins long-run cost competitiveness for the South America IT device market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency Volatility and Inflation Eroding Consumer Purchasing Power | -1.1% | Argentina, Brazil, Colombia | Short term (≤ 2 years) |

| High Import Tariffs on Finished Electronics | -0.8% | Brazil, Mexico, Argentina | Medium term (2-4 years) |

| Memory Supply Crunch Raising Average Selling Prices | -0.5% | Global, budget devices | Short term (≤ 2 years) |

| Gray-Market Devices Undercutting Official Channels | -0.3% | Brazil, Argentina, Paraguay border | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility and Inflation Eroding Consumer Purchasing Power

Argentina’s peso fell 54% against the dollar in 2024, while Brazil’s real swung within a 15% band, escalating import costs for both components and finished goods. Inflation averaged 7.2% in Colombia during 2025, squeezing discretionary budgets and stretching smartphone replacement cycles from 24 to 30 months. Brazil’s sweeping tax overhaul under Complementary Law 214 introduced pricing uncertainty that retailers passed on to consumers, and cross-border shopping surged as buyers exploited duty-free thresholds in Paraguay and Chile. These dynamics restrain near-term unit growth for the South America IT device market

High Import Tariffs on Finished Electronics

Brazil levies a 50% tariff on finished smartphones, tablets, and notebooks, inflating retail prices by up to 50% versus global averages and incentivizing gray-market smuggling. Mexico introduced new duties on electronics from non-FTA partners in 2025, while Argentina temporarily suspended its 16% levy before reinstating selective rates in 2026. Such policy gyrations force vendors to juggle country-specific price lists and trim premium assortments, hindering seamless scaling across the South America IT device market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Wearables Surge Amid Health-Data Monetization

Wearables have been gaining significant traction, even though smartphones continue to dominate the South America IT device market, accounting for 53.76% of the revenue in 2025. The growing adoption of wearables is being driven by innovative insurance programs in countries like Brazil and Colombia, where insurers now offer premium rebates of 10-15% to customers who agree to share their biometric data. This trend is expected to drive a compound annual growth rate (CAGR) of 7.77% for the wearables category through 2031. Major players such as Samsung, Huawei, and Amazfit have introduced affordable trackers priced under USD 100, equipped with advanced features like heart-rate monitoring and SpO₂ sensors, during the 2024-2026 period. Meanwhile, Xiaomi has strategically positioned its Watch 5 at a price point of MXN 5,000 (approximately USD 294) to encourage users to transition from basic fitness bands to fully featured smartwatches.

In addition to wearables, tablets and 2-in-1 notebooks have also witnessed increased demand, particularly as hybrid work models continue to expand across the region. Enterprises are increasingly specifying devices with stylus support to meet the needs of field workers, further driving their adoption. While desktops remain a niche segment, they continue to hold steady demand in specialized environments such as design studios and public agencies, where their performance and reliability are critical. As health-monitoring incentives become more widespread and regulatory frameworks for over-the-counter diagnostics become clearer, the wearables segment in the South America IT device market is expected to gradually close the gap with smartphones, solidifying its position as a key growth driver in the region.

By End-User Industry: Enterprise Digitalization Outpaces Consumer Refresh

Consumers accounted for 65.12% of 2025 spending, primarily driven by the surge in smartphone purchases during holiday promotions. The consumer segment continues to dominate the market as individuals increasingly prioritize personal devices for communication, entertainment, and productivity. However, corporate demand is also on the rise, advancing at an annual growth rate of 7.37%. This growth is reshaping procurement habits, with businesses opting for bundled solutions that include enhanced security features, managed services, and AI-ready endpoints to meet evolving operational needs. Lenovo, for instance, has capitalized on this trend by offering multi-year frameworks that combine hardware with on-site support services. This strategic approach has enabled Lenovo to secure over 20% of the South America IT device market share in the PC segment.

Government and education orders are also witnessing significant growth, particularly in Colombia, where a national initiative aims to equip 10,000 schools with tablets by 2027.[3]MinTIC Colombia, “Colombia Invertirá en Digitalización de 10.000 Escuelas Públicas,” mintic.gov.co This program underscores the increasing role of technology in education and the government’s commitment to bridging the digital divide. However, fiscal austerity measures in Argentina have constrained large-scale deployments, highlighting regional disparities in public-sector investment. Meanwhile, enterprises across South America are increasingly viewing IT devices as critical compliance tools, especially under Brazil’s LGPD (General Data Protection Law). Businesses are prioritizing devices with advanced features, such as biometric authentication and remote wipe capabilities, to ensure data security and regulatory compliance. These preferences are driving up device average selling prices, further influencing the dynamics of the South America IT device market.

By Distribution Channel: Online Platforms Capture Tier-2 Cities

Online retailers already hold a 37.84% share and are forecast to grow 7.17% annually, surpassing multi-brand physical chains in both volume and value in the South America IT device market. MercadoLibre, a leading e-commerce platform in the region, operates 50 distribution centers that ensure sub-24-hour delivery to 60% of Brazilians, significantly enhancing customer satisfaction and loyalty. Similarly, Amazon has adopted a comparable model in Mexico, leveraging its extensive logistics network to meet growing consumer demand. While omnichannel formats remain relevant for providing experiential demos and hands-on product trials, the increasing reliability of urban delivery services has shifted consumer behavior, with a significant portion of checkout conversions now occurring on mobile devices.

Social commerce platforms, such as WhatsApp Business and Instagram Shops, have further transformed the retail landscape by enabling neighborhood vendors to list their inventory without developing full-fledged web storefronts. This approach has added long-tail momentum, particularly in secondary cities where traditional retail infrastructure may be limited. Regulatory bodies, such as Brazil’s PROCON, have taken steps to address consumer concerns by imposing fines on several marketplaces for misleading offers in 2025, prompting companies to adopt clearer and more transparent return policies. Additionally, the widespread adoption of PIX-based installment plans, which are now a default option at checkout, has made digital channels more accessible and appealing to a broader audience. These factors are expected to continue driving the growth and penetration of digital channels in the South America IT device market.

By Price Band: Premium Tier Gains as Financing Unlocks Aspirational Demand

Budget devices priced under USD 200 accounted for 48.32% of the 2025 unit volume, underscoring their significant market presence. However, their dominance is gradually declining as installment financing options make high-end models more accessible to a broader consumer base. Premium phones priced above USD 601 are growing at an annual rate of 7.48%, driven by rising consumer demand for advanced features and premium designs. This trend is further supported by Brazil’s average selling price, which rose to BRL 3,009 (USD 545) in Q1 2025, reflecting a shift toward higher-value devices. Additionally, remittance-backed spending in Mexico contributed to the premium segment’s growth, with its share reaching 17.1% by Q3 2025. Samsung’s Galaxy S26 line, manufactured in Campinas and Manaus, has played a pivotal role in capturing this growing demand for premium devices.

Meanwhile, Chinese brands are intensifying competition in the mid-range segment by launching aggressively priced models, such as the Redmi Note 15 Series, which is available at USD 280. These competitive pricing strategies are putting pressure on the margins of established players in the market. Retailers are also adapting to these market dynamics by bundling accessories with financed device purchases, thereby increasing transaction values. This approach not only enhances the overall value proposition for consumers but also creates new opportunities for attachment sales within the South America IT device market.

Geography Analysis

Brazil dominated the South America IT device market with a 53.39% revenue share in 2025, supported by Campinas and Manaus plants that turned out 11.6 million Samsung phones in Q3 2025 alone. The widespread adoption of PIX-enabled financing, which enables seamless, instant payments, has significantly contributed to the market's growth. Additionally, 92% 5G coverage nationwide and premium insurance incentives have further bolstered consumer confidence, ensuring steady growth through 2031. However, gray-market imports still account for 25% of the total volume, posing challenges to the formal market. Federal enforcement efforts have intensified, resulting in the seizure of counterfeit electronics worth USD 217 million in 2025, showcasing the government’s commitment to curbing illegal trade.

Mexico ranks second in the South America IT device market, leveraging its strategic position for nearshoring to North American clients and benefiting from surging remittances. The demand for high-end devices priced above MXN 10,000 (approximately USD 588) has grown significantly, climbing to a 17.1% share by Q3 2025. This growth has been further supported by the implementation of new tariffs on non-FTA imports, which have shifted consumer demand toward models assembled in Manaus. Meanwhile, Argentina faces challenges due to peso volatility, which has curtailed discretionary upgrades. However, temporary duty suspensions introduced in late 2025 provided short-term relief to the market before selective levies were reinstated in 2026, impacting the overall market dynamics.

Colombia is experiencing the fastest growth in the region, with a 7.79% CAGR, driven by government initiatives such as public school tablet programs and the expansion of Bogotá-based software outsourcing, which has increased hardware demand. The country’s 4G coverage now spans 92% of its population, facilitating greater smartphone adoption, particularly in Pacific-coast cities. Elsewhere in the region, Chile maintains the highest per-capita ownership of IT devices, reflecting its advanced market maturity. Uruguay has emerged as a shopping hub for Argentines, attracting cross-border consumers due to favorable pricing. In Peru, the launch of the sub-USD 180 Galaxy A07 5G model underscores manufacturers' efforts to target first-time 5G buyers and capture a significant share of the entry-level segment. Collectively, these trends underscore the diverse opportunities available within the South America IT device market, driven by varying consumer preferences and regional dynamics.

Competitive Landscape

Competition is moderate, with the top five vendors controlling just over 60% of revenue across smartphones and PCs in 2025. Samsung leads smartphones in Brazil with a 40% share and 33% region-wide, enabled by local production that meets data-residency rules and quick model localization. Lenovo tops PCs with more than 20% share after eight consecutive years of expansion, buoyed by enterprise bundles that wrap devices with support and security subscriptions.

Motorola secures 24% share in Brazil by focusing on mid-range handsets, while Xiaomi’s 16% stake stems from value-rich devices priced 20-30% below incumbents. Apple, although only 7% of units, commands a lucrative premium niche. Domestic firms Positivo and Multilaser tap BNDES financing, BRL 330 million (USD 66 million approximately) and BRL 294.1 million (USD 58.82 million approximately) respectively, to automate factories for 5G and Industry 4.0, anchoring national value capture in the South America IT device market.[4]BNDES, “BNDES Financia R$ 294,1 Milhões para Multilaser Digitalizar Produção,” bndes.gov.br

New Chinese entrants Chint, Kaifa, and Megmeet pledged BRL 320 million (USD 64 million) to Manaus capacity in early 2026, widening sourcing options beyond Taiwanese contractors. Strategic focal points center on AI-driven features that warrant premium pricing, local assembly to dodge tariffs, and embedded financing that converts aspirational interest into purchases. Enforcement against smuggling tightened, with seizures jumping 118% in 2025, yet gray-market dealers still siphon budget-segment demand. Overall, vendor dynamics ensure sustained innovation while preventing any single firm from overwhelming the South America IT device market.

South America IT Device Industry Leaders

Samsung Electronics Co., Ltd.

Apple Inc.

Lenovo Group Limited

Xiaomi Corporation

HP Inc.

- *Disclaimer: Major Players sorted in no particular order

South America IT Device Market Report Scope

The South America IT Device Market encompasses the manufacturing, distribution, and adoption of computing and connected electronic devices across consumer, enterprise, and public-sector applications in the region. This market includes a broad range of hardware such as smartphones, tablets, laptops and notebooks, desktops and workstations, and wearables, which support communication, productivity, and digital services.

The South America IT Device Market Report is Segmented by Device Type (Smartphones, Tablets, Laptops and Notebooks, Desktops and Workstations, and Wearables), End-User Industry (Consumer, Enterprise, and Government and Education), Distribution Channel (Online Retailers, Omnichannel Retailers, Brand-owned Stores, and Multi-brand Physical Outlets), Price Band (Budget ≤USD 200, Mid-range USD 201-600, and Premium ≥USD 601), and Geography (Brazil, Mexico, Argentina, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Smartphones |

| Tablets |

| Laptops and Notebooks |

| Desktops and Workstations |

| Wearables |

| Consumer |

| Enterprise |

| Government and Education |

| Online Retailers |

| Omnichannel Retailers |

| Brand-owned Stores |

| Multi-brand Physical Outlets |

| Budget (≤ USD 200) |

| Mid-range (USD 201-600) |

| Premium (≥ USD 601) |

| Brazil |

| Mexico |

| Argentina |

| Colombia |

| Rest of South America |

| By Device Type | Smartphones |

| Tablets | |

| Laptops and Notebooks | |

| Desktops and Workstations | |

| Wearables | |

| By End-User Industry | Consumer |

| Enterprise | |

| Government and Education | |

| By Distribution Channel | Online Retailers |

| Omnichannel Retailers | |

| Brand-owned Stores | |

| Multi-brand Physical Outlets | |

| By Price Band | Budget (≤ USD 200) |

| Mid-range (USD 201-600) | |

| Premium (≥ USD 601) | |

| By Geography | Brazil |

| Mexico | |

| Argentina | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the projected size of the South America IT device market by 2031?

It is forecast to reach USD 148.94 billion by 2031.

Which device category is expected to grow fastest in South America through 2031?

Wearables, advancing at a 7.77% CAGR as insurers and employers subsidize health-tracking devices.

How is PIX influencing high-end device purchases in Brazil?

PIX enables installment financing embedded at checkout, spreading payments over 12-18 months and boosting sales of smartphones priced above USD 601.

Why are enterprises in South America refreshing PCs and tablets more frequently?

Hybrid-work policies and demand for on-device AI accelerators push corporations to upgrade notebooks and tablets on three-to-four-year cycles.

Which country is forecast to record the fastest growth in IT device spending until 2031?

Colombia, with a projected 7.79% CAGR driven by nearshoring and public-sector digitalization programs.

What strategies are leading vendors using to sidestep Brazil's 50% electronics import tariff?

They manufacture in the Manaus Free Trade Zone, which offers tax exemptions that lower landed costs by up to 40

Page last updated on: