South America Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

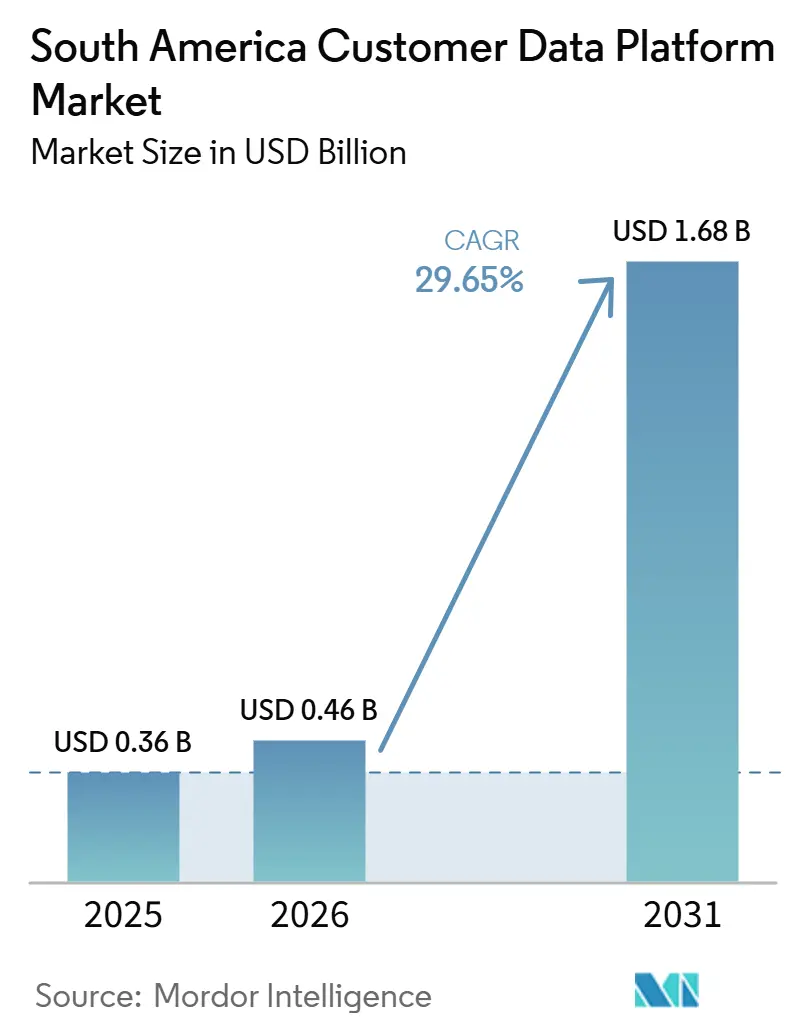

| Base Year Market Size (2025) | USD 0.36 Billion |

| Market Size (2026) | USD 0.46 Billion |

| Market Size (2031) | USD 1.68 Billion |

| Growth Rate (2026 - 2031) | 29.65% CAGR |

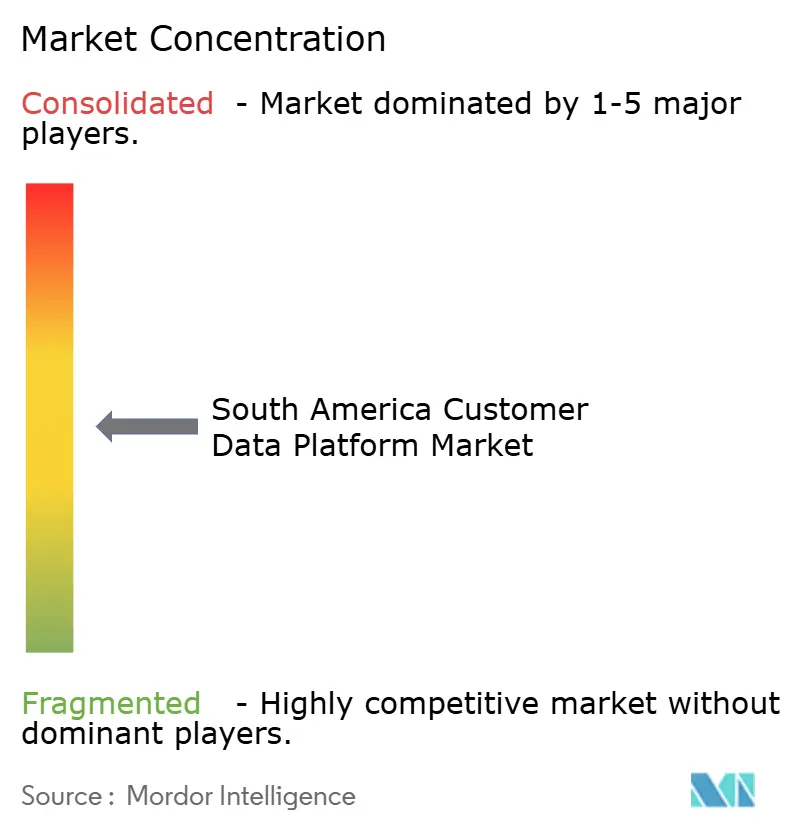

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Customer Data Platform Market Analysis by Mordor Intelligence

The South America customer data platform market size was USD 0.36 billion in 2025 and is forecast to reach USD 1.68 billion by 2031, advancing at a CAGR of 29.65% during 2026-2031. The South America customer data platform market is being shaped by the shift away from third-party cookies, stronger privacy oversight, and wider use of cloud-based data environments. Enterprises are moving toward first-party data ownership because fragmented customer records now impose direct costs on campaign execution, compliance, and personalization speed. The market is also benefiting from rising interest in real-time identity resolution and AI-enabled activation, especially in retail, banking, and digital commerce settings where response speed matters. Competitive activity remains active because large platform vendors are deepening product integration, while specialist providers are trying to win with faster deployment and focused use cases. A further lift comes from the growing commercial value of first-party audience activation, which is turning the South America customer data platform market from a marketing tool category into a broader data infrastructure decision.

Key Report Takeaways

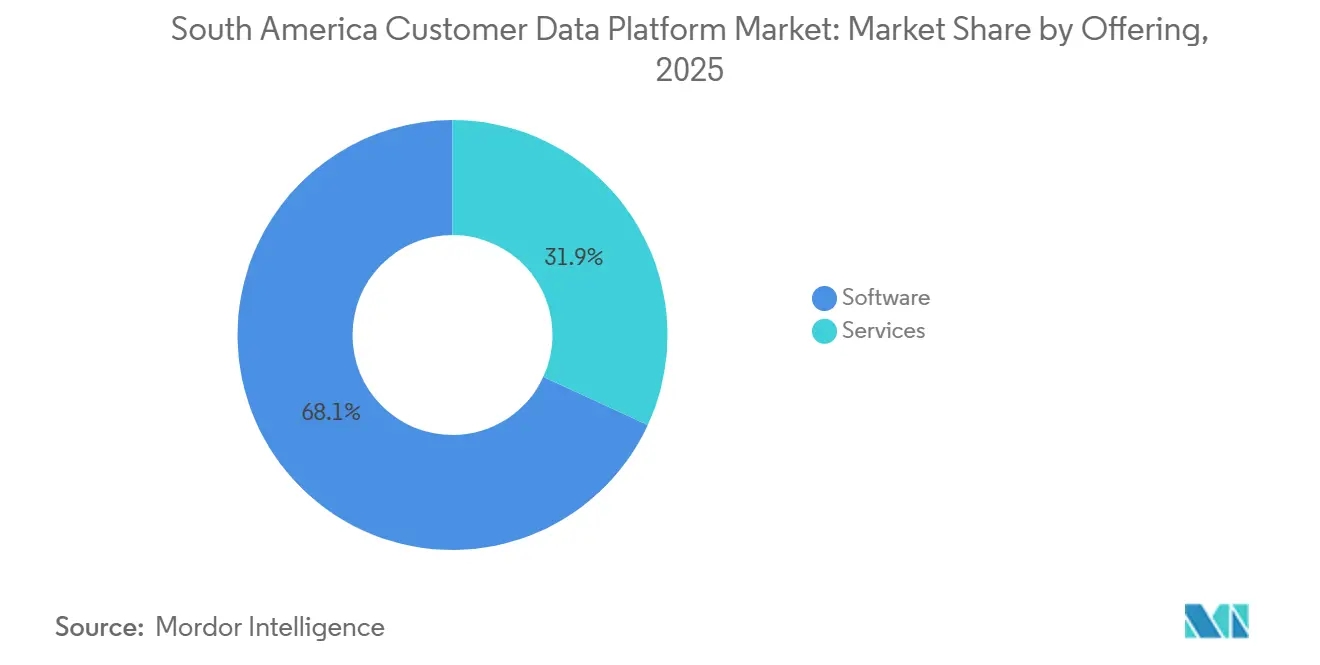

- By offering, software accounted for 68.13% share of the South America customer data platform market size in 2025, while services are projected to expand at a 32.45% CAGR through 2031.

- By deployment mode, cloud held a 66.19% share of the South America customer data platform market in 2025 and is expected to record the highest CAGR of 32.08% through 2031.

- By organization size, large enterprises represented 71.29% of the South America customer data platform market revenue in 2025, while SMEs are projected to grow at a 32.88% CAGR through 2031.

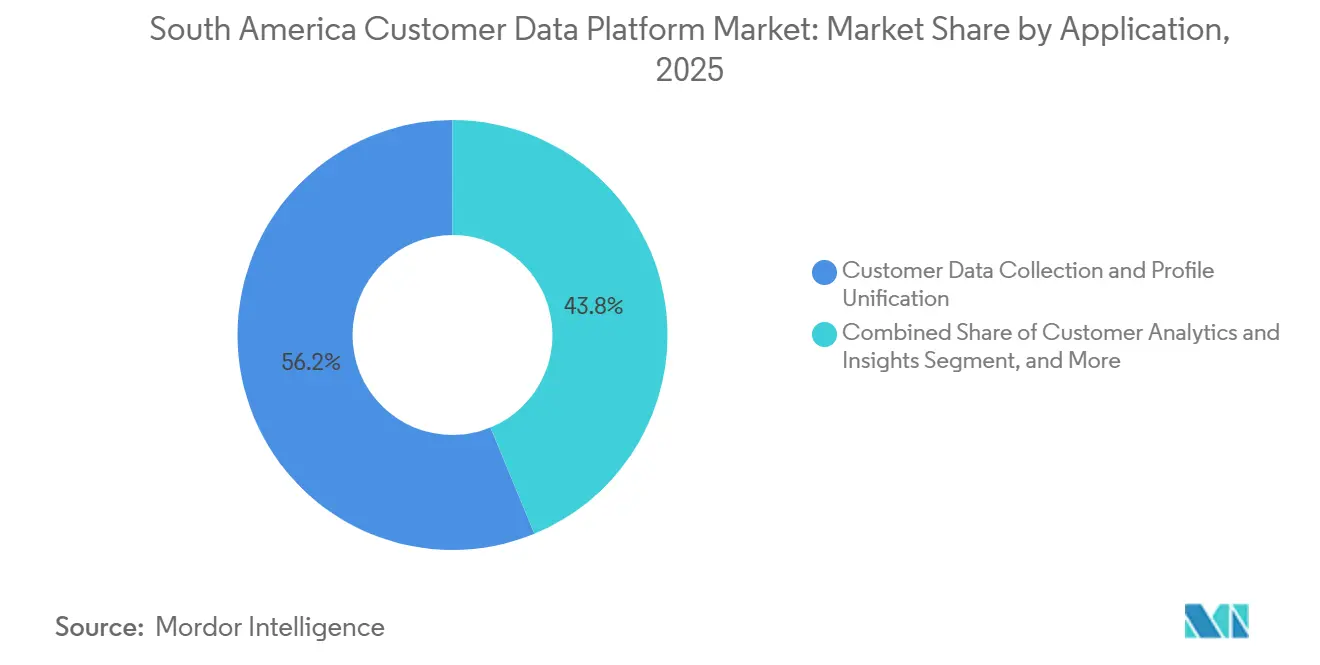

- By application, customer data collection and profile unification captured 56.22% of revenue in 2025, while audience segmentation and personalization are projected to expand at a 31.39% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 24.56% of the South America customer data platform market revenue in 2025, while BFSI is projected to grow at a 31.04% CAGR through 2031.

- By geography, Brazil held 49.51% of the South America customer data platform market share in 2025, while Chile is projected to register the fastest CAGR at 31.72% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising First-Party Data Prioritization Amid Cookie Deprecation | +5.5% | Brazil, Chile, Argentina | Short term (≤ 2 years) |

| Accelerating Real-Time Customer Profile Unification Needs | +4.8% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Expanding Cloud Migration Across Marketing Data Stacks | +4.2% | All geographies, strongest in Brazil and Chile | Medium term (2-4 years) |

| Increasing Demand for AI-Driven Personalization and Next-Best-Action Orchestration | +4.0% | Brazil, early-stage in Argentina | Medium term (2-4 years) |

| Retail Media and Omnichannel Commerce Activation Pressure | +3.5% | Brazil, emerging in Chile and Colombia | Short term (≤ 2 years) |

| Cross-Border Data Localization and Privacy Compliance Complexity | +3.0% | Brazil, Chile, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising First-Party Data Prioritization Amid Cookie Deprecation

The South America customer data platform market is gaining support from the region’s shift toward first-party data control. In Brazil, ANPD enforcement and the broader regulatory agenda have kept privacy compliance high on enterprise priorities, underscoring the value of platforms that can connect consent, identity, and activation within a single environment. This change matters because brands can no longer rely on older tracking models as customer consent, auditability, and data-handling practices come under greater scrutiny. The commercial effect is clear: systems that embed consent logic in the profile layer are becoming more attractive than tools that place privacy controls outside the core customer record. That preference favors platforms built around persistent customer identity rather than point solutions built only for ad targeting. It also supports longer-term demand visibility, as privacy obligations affect both current campaign execution and future cross-border data design.

Accelerating Real-Time Customer Profile Unification Needs

The South America customer data platform market is also being pushed by the need to unify customer records fast enough to support real-time engagement. Banco Bradesco showed the scale of this issue when it built an in-house platform on Databricks that processed 2.9 billion raw monthly observations and cut full pipeline latency by more than 94%, bringing core processes down to 3.5 hours from 60-80 hours. The same environment influenced at least 30% of credit transactions in 2024 and handled 7.7 billion communications across 14 channels, which shows how closely unified profiles are tied to revenue and service response in BFSI. This matters beyond one bank because it confirms that fragmented data is no longer just a reporting issue. It is now a constraint on decision speed, conversion quality, and channel coordination. That is why demand is shifting toward platforms that can support identity stitching, profile refresh, and orchestration within a single operating layer.

Expanding Cloud Migration across Marketing Data Stacks

The South America customer data platform market continues to benefit from wider cloud migration across enterprise data environments. Salesforce’s investments in Argentina and Mexico signal that global vendors see the region as a long-term zone of expansion for AI and CRM, supporting the broader move toward cloud-based customer data infrastructure. This shift lowers the burden of on-premises hardware ownership and reduces the need for scarce local engineering capacity at the start of a deployment. It also makes warehouse-native and composable designs more practical, since enterprises can activate data closer to existing cloud storage instead of forcing a full system replacement. The demand case is strongest when enterprises want faster deployment with fewer integration steps and greater flexibility for future AI use cases. Cloud migration, therefore, supports both near-term adoption and the longer path toward multi-environment customer data management.

Increasing Demand for AI-Driven Personalization and Next-Best-Action Orchestration

The South America customer data platform market is receiving another lift from rising demand for AI-based personalization and next-best-action workflows. Adobe’s product direction reflects this shift, with Real-Time CDP Collaboration becoming generally available in February 2025 and later platform updates continuing to strengthen real-time profile and segmentation capabilities in 2026. The change is important because enterprises are not treating AI as a separate add-on. They are increasingly expecting it to work inside the same environment that stores, resolves, and activates customer profiles. That raises the baseline for vendors because audience building, campaign logic, and profile intelligence now need to operate together with low latency. It also makes platform depth more valuable in large retail and financial accounts where orchestration speed can directly affect conversion and retention outcomes. As a result, AI capability is becoming a purchase factor tied to the core platform rather than a later-stage enhancement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy Martech and CRM Environments | -3.2% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Budget Constraints among Mid-Market Buyers | -2.5% | Argentina, Brazil, Rest of South America | Short term (≤ 2 years) |

| Shortage of In-House Customer Data Engineering Talent | -2.0% | Region-wide, most acute in Argentina and Chile | Long term (≥ 4 years) |

| Data Quality Fragmentation across Multichannel Consumer Journeys | -1.8% | Brazil and Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Martech and CRM Environments

Legacy integration remains the most immediate operating barrier for deployment across the region. The issue is not only technical, as enterprises often need to connect customer data platforms with CRM, ERP, commerce, messaging, analytics, and compliance systems simultaneously. That raises deployment time, increases service dependence, and pushes more value toward vendors or partners that can handle region-specific implementation work. In the South America customer data platform market, this creates a split between providers that can scale through partner ecosystems and those that can only win cleaner enterprise environments. The problem is especially relevant in large organizations where data lineage and governance must be maintained across many connected systems under stricter privacy rules. Even when enterprise demand is clear, integration debt can delay revenue recognition and extend the path from contract signing to business use.

Budget Constraints among Mid-Market Buyers

Budget pressure among mid-market buyers is a second major restraint for the category. On-premises deployments in Brazil and Argentina have been observed at over USD 500,000 over 3 years, while lower-cost cloud tiers have helped bring entry points below USD 50,000 for smaller-profile bases, showing how wide the pricing gap still is between platform models in the region. The cost issue matters because many of the strongest whitespace opportunities lie in mid-market retail, fintech, and healthcare accounts that need better customer data management but cannot absorb the expense of an enterprise-style implementation. Salesforce’s January 2025 investment commitment in Argentina demonstrated long-term confidence in the market, yet macroeconomic pressures still limit short-cycle purchasing behavior among many local buyers.[1]Salesforce, “Salesforce to Invest USD 500 Million in Argentina Over 5 Years,” Salesforce Press Release, salesforce.com This means adoption often starts with a narrower scope instead of a full-stack rollout. The restraint is easing gradually, but it still slows the speed at which the category can move from large accounts into its next wave of regional demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Anchors Revenue While Services Gain Weight

Software held 68.13% of the South America customer data platform market share in 2025, confirming that platform licensing remained the top spending priority for early- and mid-stage adopters. Large enterprises preferred to secure the core system first because identity resolution, profile unification, and activation logic serve as the foundation for all subsequent use cases. This was especially evident in financial services and large retail settings, where internal teams could already manage parts of the orchestration stack using in-house data resources. The pattern also shows that many buyers still entered the customer data platform industry through platform ownership rather than through outsourced transformation programs. In practical terms, software remained the anchor because enterprises wanted direct control over the profile layer before widening use into analytics, campaign coordination, and compliance workflows.

The services segment is smaller today, yet it is projected to grow at a 32.45% CAGR through 2031, faster than software, which points to a change in how the category is scaling. As the South America customer data platform market moves deeper into mid-market accounts, more buyers will need configuration, connector work, journey design, governance setup, and ongoing operational support. That shift gives services a larger role in total contract value, even when software still leads in revenue. It also underscores the importance of local delivery capacity, as integration complexity often determines whether a deployment becomes usable within a reasonable time frame. For vendors, the implication is direct, since regional service reach is becoming a competitive requirement rather than a secondary support layer.

By Deployment Mode: Cloud Combines Scale With The Highest Growth

Cloud commanded 66.19% share of the South America customer data platform market size in 2025 and is projected to grow at a 32.08% CAGR through 2031. This combination of leadership in both share and growth is notable because mature markets often see the largest segment slow before its alternatives. Here, cloud is still expanding because it eliminates upfront hardware costs and provides enterprises with a more flexible path to unified customer data operations. The model is also well aligned with warehouse-native and composable approaches, which reduce the pressure to replace every legacy component at once, for the South America customer data platform market, where cloud has become the default route for organizations that want faster implementation with room to scale into AI and orchestration later.

On-premises deployments remain relevant in regulated environments, especially when internal security policies or data residency concerns still outweigh cost and agility benefits. Hybrid configurations are also becoming more important because multinational retailers and banks often need to balance regional privacy obligations with global system architecture. That keeps deployment choice from becoming a simple cloud-versus-on-premises decision. Instead, the market is moving toward a flexible environment design shaped by governance, latency, and connector needs. This reinforces a broader point in the customer data platform industry: deployment preferences are now tied as much to compliance design and system fit as to basic infrastructure spending.

By Organization Size: Large Enterprises Lead While SMEs Open the Next Demand Layer

Large enterprises accounted for 71.29% of revenue in 2025, indicating that scale still determines who can adopt most easily at the current stage of category development. These buyers can spread platform costs across many campaigns, channels, and internal functions, making enterprise licensing easier to justify. They also tend to have stronger internal governance structures and larger customer data pools, which make unification more valuable. In the South America customer data platform market, this has kept the largest organizations at the center of current revenue even as the buyer base is widening. Their lead also reflects the fact that many enterprise accounts treat the platform as shared infrastructure for CRM, analytics, marketing, and service operations.

SMEs are projected to grow at a 32.88% CAGR through 2031, making them the fastest-growing organization-size segment, even though their revenue base is smaller today. That growth is being driven by pay-as-you-go identity resolution models and lower-cost warehouse-native configurations that better align with shorter budget cycles. A study published in SciELO on Chilean SMEs linked ICT adoption to greater operational efficiency, which supports the broader case that smaller firms are becoming more willing to invest in digital operating tools when the setup burden is manageable. SMEs are also different from large enterprises in one important way: many lack dedicated data engineering staff and therefore need simpler setups and self-service operations. That is why vendors offering no-code segmentation, easier workflow design, and lighter implementation demands are likely to convert this part of the South America customer data platform market faster than platforms built for high-touch enterprise deployment.

By Application: Profile Unification Holds the Base While Personalization Draws Future Spend

Customer data collection and profile unification accounted for 56.22% of revenue in 2025, underscoring the centrality of foundational data consolidation to current demand. This leading share indicates that many organizations are still focused on solving the first problem: creating a persistent, usable customer record across disconnected systems. Without that base, later applications such as predictive decisioning, cross-channel orchestration, or advanced analytics cannot produce consistent results. In the South America customer data platform market, that makes profile unification is the most common starting point rather than the final goal. It also explains why buyers continue to prioritize identity resolution, ingestion quality, and governance controls during early deployment phases.

Audience segmentation and personalization are projected to grow at a 31.39% CAGR through 2031, which signals where spending is likely to move once unification work is in place. As organizations complete foundational data work, they can shift more budget toward precision targeting, next-best-action logic, and journey activation tied to specific commercial outcomes. Consent and preference management is also gaining importance because regulatory enforcement now affects how profiles are built and used, not just how notices are displayed. Marketing orchestration and customer analytics, therefore, become more valuable when the profile base is stable, and permission logic is embedded in it. This progression shows how the South America customer data platform market is moving from record consolidation toward monetization and control of the same underlying data asset.

By End-User Industry: Retail and E-Commerce Lead While BFSI Advances Fastest

Retail and e-commerce accounted for 24.56% of revenue in 2025, keeping consumer-facing commerce as the largest buyer group in the category. The segment’s lead reflects the constant need to connect browsing, purchase, loyalty, store, and campaign signals into one customer view. That operating requirement is stronger in large digital commerce environments where personalization speed and channel coordination directly affect conversion and repeat engagement. In the South America customer data platform market, retail demand also benefits from the region’s push toward first-party audience activation and more measurable campaign targeting. This keeps the segment at the front of current adoption even as new industries deepen their use of customer data tools.

BFSI is projected to grow at a 31.04% CAGR through 2031, which makes it the fastest-growing end-user segment in the current forecast window. Banco Bradesco’s documented deployment showed how real-time customer data handling can support credit decisions, communications management, and contextual offer performance at scale. Healthcare and life sciences are also becoming increasingly relevant following the Brazilian Ministry of Health's formalization of the Rede Nacional de Dados em Saúde as the official integration platform for SUS data in July 2025.[2]Ministry of Health, “Ministry of Health Institutes Rede Nacional de Dados em Saúde as Official SUS Integration Platform,” Government of Brazil, gov.br That move matters because it normalizes health data infrastructure and interoperability at the national scale. IT and telecom, media, manufacturing, and public administration remain earlier-stage verticals, but the end-user mix is widening as the South America customer data platform market becomes relevant to more data-rich operating environments.

Geography Analysis

Brazil held 49.51% of the South America customer data platform market share in 2025, which kept it far ahead of the rest of the region. Its lead rests on enterprise scale, a large digital commerce base, and a regulatory setting that makes data governance more urgent. The ANPD regulatory agenda and enforcement posture continue to support this environment by keeping privacy oversight active and visible for organizations handling customer records at scale. Brazil also offers one of the clearest operating examples in the region, since Banco Bradesco used a large-scale in-house platform to manage billions of observations and communications across many channels.

Chile is projected to record the fastest CAGR of 31.72% through 2031, which will give it a different role in the regional picture. The country combines strong digital policy direction with meaningful IT spending, and the U.S. Trade and Development Agency reported USD 1.2 billion in financial-services IT investment in 2025.[3]U.S. Trade and Development Agency, “Chile, Information Technologies,” Country Commercial Guide, trade.gov Chile Digital 2035 also supports long-run demand by targeting full digitalization of public services and treating data infrastructure as a strategic asset. That matters for commercial adoption because policy-backed digital infrastructure tends to improve the case for enterprise data platforms across private and public end users. Chile also stands out as a favorable setting for SME technology expansion, with Scielo-published research linking ICT adoption to stronger operational efficiency in smaller firms.

Argentina sits between opportunity and purchasing pressure in the current cycle. Salesforce’s January 2025 commitment to invest USD 500 million over 5 years showed continued confidence in Argentina’s AI and digital transformation potential. The Rest of South America, including markets such as Colombia, Peru, and Ecuador, remains earlier in deployment maturity even though demand for data unification and personalization is building. These countries appear more limited by implementation capacity and local delivery depth than by a lack of commercial interest. That leaves room for future expansion as the South America customer data platform market spreads beyond its present core geographies.

Competitive Landscape

The South America customer data platform market remains moderately concentrated, with global suite vendors holding an advantage through product breadth, integration depth, and regional go-to-market capacity. Adobe Inc., Salesforce Inc., Oracle Corporation, Microsoft Corporation, and SAP SE remain the most visible large-platform competitors, while specialist vendors continue to compete on activation speed, flexibility, and narrower use cases. The competitive shape of the market reflects a balance between scale and specialization rather than a winner-takes-all structure. This keeps the South America customer data platform market active for both broad enterprise stacks and focused providers that can solve a specific pain point faster.

Adobe has continued to strengthen its position through product development focused on privacy-safe activation and real-time profile management. The company announced the general availability of Real-Time CDP Collaboration in February 2025, providing brands and publishers with a consent-aware path to first-party data partnership workflows.[4]Adobe, “Adobe Announces General Availability of Real-Time CDP Collaboration,” Adobe Newsroom, news.adobe.com This was followed by May 2026 platform updates that added profile ingestion tracking and stronger segmentation capabilities in Adobe Experience Platform. Salesforce also remained active through regional investment moves, including its USD 500 million commitment in Argentina and its USD 1 billion plan in Mexico, both of which support broader expansion of its AI, CRM, and data platform. These steps matter because the competitive battle is no longer only about profile storage, but also about how well vendors integrate infrastructure, AI, activation, and governance into a single operating model.

Challenger activity is also meaningful because specialist vendors are trying to close the gap between customer data unification and journey execution. BlueConic’s June 2026 acquisition of Blueshift showed this direction clearly by combining real-time behavioral context with AI decisioning and cross-channel execution. That type of move is important because it narrows the historical distance between data platforms and campaign systems. The remaining whitespace is strongest in the SME tier, where modular pricing, simpler deployment, and no-code workflow design still offer room for non-incumbent vendors to differentiate. This means competitive pressure in the South America customer data platform market is likely to remain broad, even as larger vendors continue to shape the top end of enterprise demand.

South America Customer Data Platform Industry Leaders

Adobe Inc.

Salesforce, Inc.

Oracle Corporation

Twilio Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: BlueConic Inc. acquired Blueshift, the AI-powered cross-channel marketing platform, to close the loop between first-party behavioral data capture, AI-driven next-best-action decisioning, and cross-channel execution across email, push, in-app, SMS, and web.

- May 2026: Adobe Experience Platform released updated real-time customer profile capabilities in its May 2026 platform update, including batch profile ingestion progress tracking and enhanced segmentation services, continuing the company’s quarterly feature release cadence under its Agent Orchestrator strategy.

- October 2026: Salesforce announced plans to invest USD 1 billion in Mexico over 5 years, including AI innovation, public-sector digital transformation, and workforce development, a commitment that reinforces Salesforce’s strategic expansion across the broader South America customer data platform market and signals continued Agentforce and Data Cloud capability deployment in the region.

- February 2025: Adobe announced the general availability of Real-Time CDP Collaboration, purpose-built for privacy-safe first-party data partnerships between brands and publishers, built on Adobe Experience Platform and integrated with Snowflake and Amazon Web Services for secure cross-ecosystem data connection.

South America Customer Data Platform Market Report Scope

The South America Customer Data Platform (CDP) Market comprises software solutions and associated services that collect, unify, manage, and activate customer data from multiple online and offline sources to create persistent customer profiles. These platforms help businesses improve audience segmentation, personalization, campaign execution, customer analytics, and consent management across customer engagement channels. Growing digital transformation initiatives, expanding e-commerce activity, and increasing demand for data-driven marketing strategies drive the market across the region. CDPs help organizations enhance customer experiences, optimize marketing performance, and improve customer lifecycle management.

The South America Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries), and Geography (Brazil, Argentina, Chile, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

Key Questions Answered in the Report

What is the South America customer data platform market size in 2025 and 2031?

The South America customer data platform market size was USD 0.36 billion in 2025 and is forecast to reach USD 1.68 billion by 2031, at a 29.65% CAGR during 2026-2031.

Which deployment model leads customer data platform adoption in South America?

Cloud led with 66.19% share in 2025 and is also projected to post the fastest growth at 32.08% CAGR through 2031.

Why is Brazil the leading country for customer data platforms in South America?

Brazil held 49.51% of regional revenue in 2025 because it combines large enterprise demand, strong digital commerce activity, and a more active privacy compliance environment.

Which end-user segment is growing fastest in this space?

BFSI is projected to expand at a 31.04% CAGR through 2031, supported by real-time decisioning needs, open-finance use cases, and large-scale communication volumes.

What is the main application area for customer data platforms in South America today?

Customer data collection and profile unification led with 56.22% of application revenue in 2025, showing that most organizations are still building a unified customer record as the first step.

Where is the next major growth opportunity beyond large enterprises?

SMEs are projected to grow at a 32.88% CAGR through 2031 because lower-cost and warehouse-native models are making adoption more feasible for smaller buyers.

Page last updated on: