Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

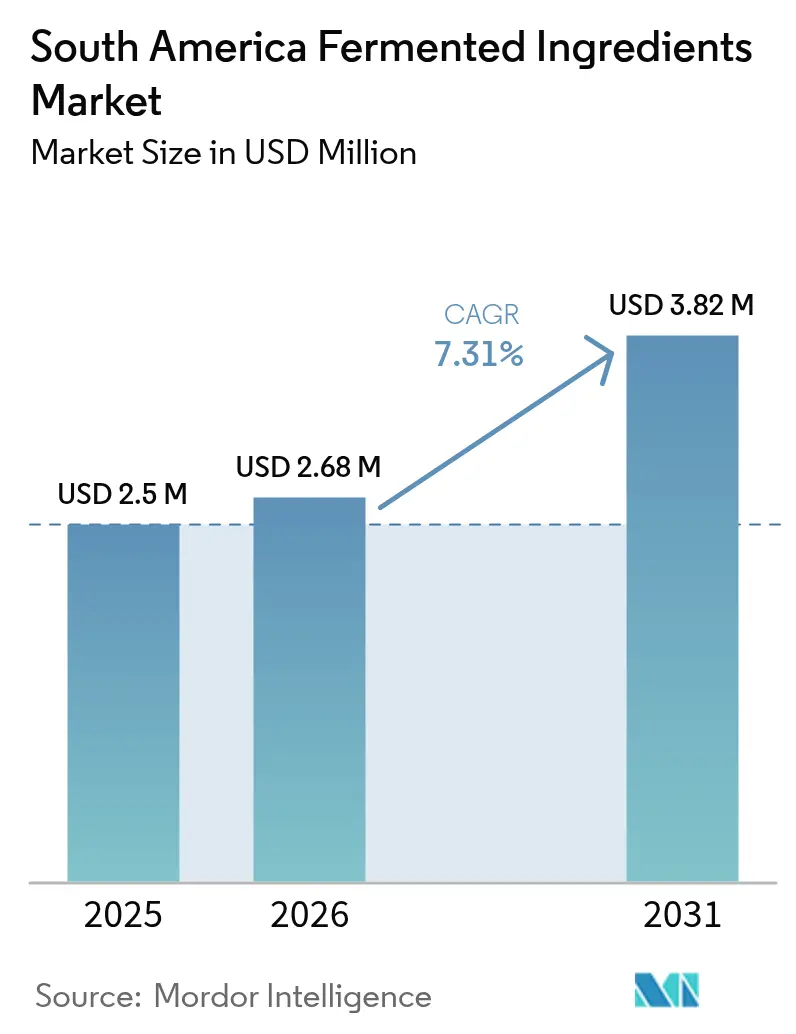

| Base Year Market Size (2025) | USD 2.50 Million |

| Market Size (2026) | USD 2.68 Million |

| Market Size (2031) | USD 3.82 Million |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

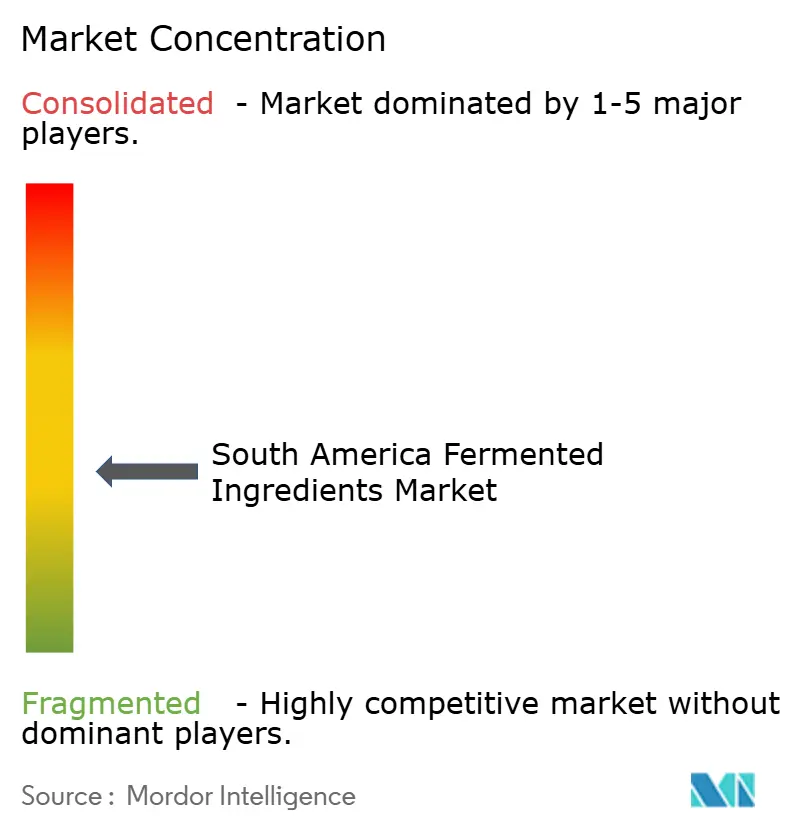

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Fermented Ingredients Market Analysis by Mordor Intelligence

South American fermented ingredients market size in 2026 is estimated at USD 2.68 million, growing from 2025 value of USD 2.50 million with 2031 projections showing USD 3.82 million, growing at 7.31% CAGR over 2026-2031. Expansion rests on the region’s plentiful crop feedstocks, improving bio-inputs legislation, and manufacturers’ pivot toward bio-based solutions in food, feed, and industrial uses. Livestock growth in Brazil and Argentina sustains steady demand for amino-acid feed additives, while national bioeconomy programs funnel public funds into fermentation capacity. Multinational players add scale through green-field factories, yet local start-ups remain agile in specialty niches that leverage indigenous fermentation know-how. Supply-chain resilience is improving as ethanol and sugar co-products are valorized into substrates, but cost parity with petrochemical substitutes remains elusive in capital-intensive polymers and specialty proteins.

Key Report Takeaways

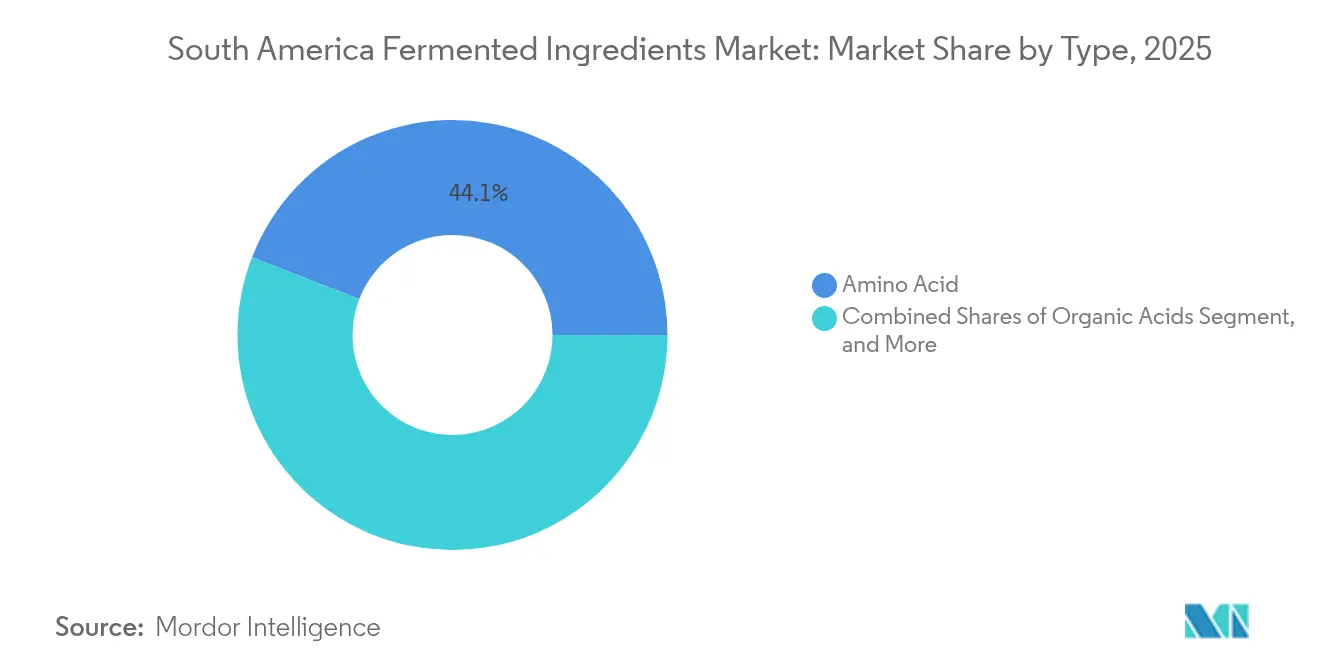

- By product type, amino acids led with 44.12% of the South America fermented ingredients market share in 2025, and polymers are projected to expand at a 9.18% CAGR through 2031.

- By form, dry products accounted for 59.05% share of the South America fermented ingredients market size in 2025, while liquid formulations are set to grow at a 9.88% CAGR through 2031.

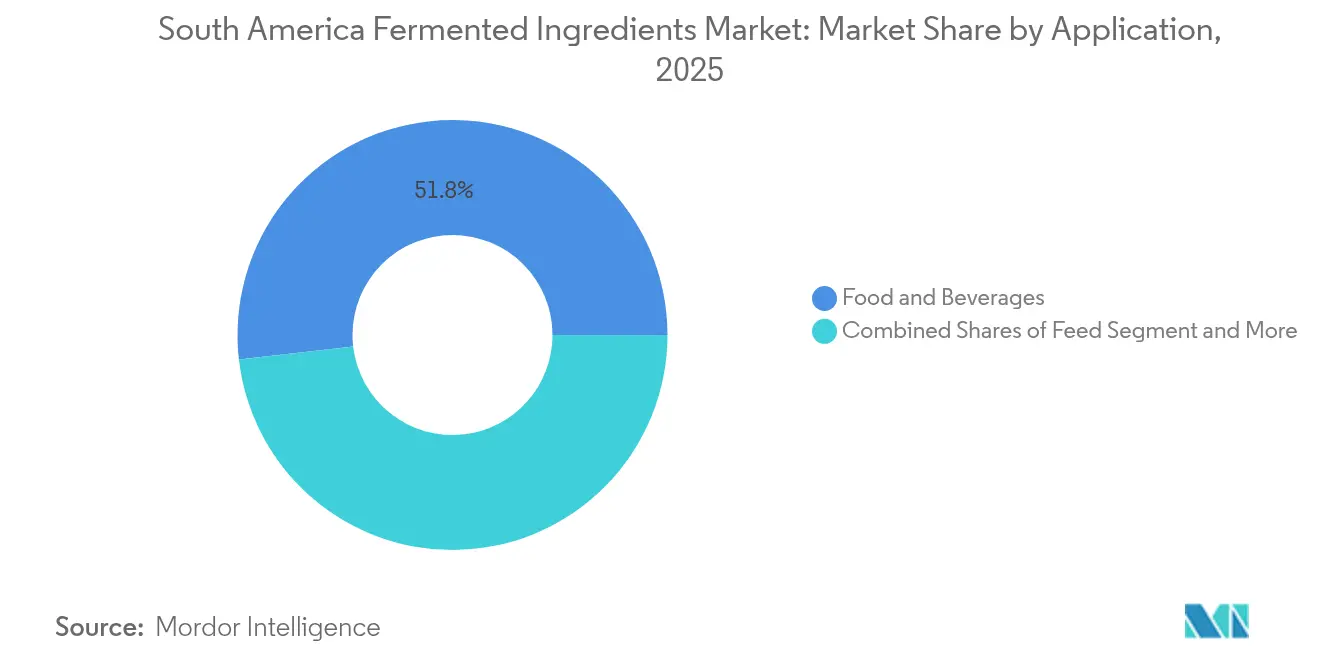

- By application, food and beverages held 51.82% of the South America fermented ingredients market in 2025, and industrial uses are forecast to climb at an 8.63% CAGR through 2031.

- By geography, Brazil dominated with a 59.48% share in 2025, whereas Chile is anticipated to register a 8.79% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Fermented Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming animal-protein exports fuelling demand for feed-grade amino acids | +1.8% | Brazil, Argentina core, spillover to Uruguay and Paraguay | Medium term (2-4 years) |

| Rising clean-label trend in Food and Beverages driving switch to bio-based additives | +1.5% | Global, with early gains in Brazil, Chile, Colombia | Long term (≥ 4 years) |

| National bio-inputs programs in Brazil and Argentina subsidising fermentation capacity | +1.2% | Brazil and Argentina, limited spillover to MERCOSUR partners | Short term (≤ 2 years) |

| Cultural Affinity for Fermented Foods Supporting Traditional Fermentation Ingredients | +0.9% | Regional, strongest in Peru, Ecuador, Colombia indigenous areas | Long term (≥ 4 years) |

| Rising consumer awareness and demand for natural, healthy foods | +1.1% | Urban centers across South America, led by Brazil and Chile | Medium term (2-4 years) |

| Advancements in Biotechnology Supporting Scalable Fermentation Processes | +1.0% | Brazil core, emerging in Argentina and Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Animal-Protein Exports Fuelling Demand for Feed-Grade Amino Acids

South America's livestock sector expansion creates cascading demand for fermented feed additives, particularly as the region consolidates its position as the world's protein supplier. This protein boom drives amino acid demand beyond traditional lysine and methionine toward specialized fermentation-derived compounds like threonine and tryptophan, essential for optimizing feed conversion ratios in intensive production systems. Brazil's position as the world's largest beef exporter and second-largest poultry producer creates structural demand for fermentation-derived feed additives, particularly as environmental regulations push producers toward bio-based alternatives to synthetic growth promoters. The sector's projected growth to 43.7 billion liters of ethanol demand by 2033 also generates substantial co-product streams suitable for fermentation substrate applications, according to the International Energy Agency data[1]Source: International Energy Agency, “Biofuels Annual Report 2024,” iea.org. Argentina's recent reduction in export tariffs on soybean products enhances the region's competitiveness in global protein markets, further amplifying demand for feed-grade fermentation products as producers seek margin optimization through improved feed efficiency.

Rising Clean-Label Trend in Food and Beverages Driving Switch to Bio-Based Additives

Brazil’s food-processing sector generated USD 209 billion in 2022, and updated supplement rules under Normative Instruction 284/2028 clarify the use of enzymes and probiotics in finished products, according to the ANVISA data. Brand owners respond by replacing synthetic preservatives with fermentation-derived lactic and citric acids that deliver recognizable labels and acidic impact. Consumer surveys in major Brazilian and Chilean cities show a willingness to pay premiums for naturally sourced texturizers, spurring uptake of fermented gums and cultures in snacks and dairy lines. Retailers amplify demand by expanding “free-from” aisles, nudging processors toward short-ingredient panels rooted in bio-derived components. Together, regulatory clarity and purchasing shifts translate into sustained, margin-accretive growth for clean-label solutions within the South American fermented ingredients market.

National Bio-Inputs Programs in Brazil and Argentina Subsidising Fermentation Capacity

Brazil’s Federal Law 15,070/2024 mandates registration, inspection, and innovation incentives for bio-inputs factories, opening doors for commercial and on-farm fermentation units. The legislation allows both commercial biofactories and personal-use production units, creating multiple market entry points for fermentation technology providers. Argentina's Agricultural Bio-inputs Program (PROBIAAR) supports domestic companies producing bio-fertilizers and bio-pesticides, with 131 registered companies by 2022, of which 97 are domestic enterprises. These programs reduce regulatory barriers and provide financial incentives that lower the cost of capital for fermentation capacity investments, particularly benefiting small and medium enterprises seeking to commercialize traditional fermentation knowledge.

Cultural Affinity for Fermented Foods Supporting Traditional Fermentation Ingredients

Traditional fermentation practices in South America present opportunities to scale artisanal processes for commercial use, driven by consumer demand for authentic, traditional food experiences. These fermented products contain significant levels of lactic acid bacteria, specifically Lactiplantibacillus plantarum and Lacticaseibacillus species, which demonstrate robust stress tolerance and adhesion properties beneficial for probiotic development. Fermentation's cultural importance in the region encompasses both beverages and dairy products such as kumis and suero costeño, which has established consumer acceptance of fermented ingredients in processed foods. Traditional fermented products function as nutraceuticals, delivering essential nutrients and health benefits to communities while providing models for new product development using traditional ingredients. This established cultural acceptance facilitates market entry for fermentation-derived ingredients, especially when products emphasize their connection to traditional food practices. The increased focus on preserving indigenous food heritage creates opportunities to develop fermentation-derived ingredients that maintain traditional methods while adhering to modern food safety and production standards.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Competition from Synthetic Petrochemical-Based Ingredients | -1.4% | Global, particularly impacting Brazil and Argentina export competitiveness | Short term (≤ 2 years) |

| Limited Research and Development and Technical Expertise | -1.1% | Regional, most acute in Chile, Colombia, and smaller economies | Medium term (2-4 years) |

| Economic and Geopolitical Uncertainties | -0.8% | Argentina core, spillover effects across MERCOSUR trade relationships | Short term (≤ 2 years) |

| Dependence on Imported Raw Materials for Fermentation Processes | -0.6% | Regional, affecting specialized fermentation substrates and equipment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Competition from Synthetic Petrochemical-Based Ingredients

Global synthetic amino acids and organic acids benefit from decades-long optimization and large-scale Asian plants that deliver low cost per kilogram. Latin America currently lacks extensive food-grade fermentation infrastructure, forcing many users to import at higher landed costs. Until regional biofactories reach similar economies of scale, price-sensitive feed and industrial buyers will gravitate toward petrochemical alternatives, trimming addressable volumes for the South American fermented ingredients market. Currency volatility in Argentina and local financing costs compound the challenge by inflating capital expenditure for new fermentation lines. Producers mitigate risk through waste-to-substrate programs and regional purchasing agreements, yet cost parity remains a near-term hurdle.

Limited Research and Development and Technical Expertise

Technical capability gaps across South America constrain fermentation industry development, particularly in countries lacking established biotechnology infrastructure and specialized human capital. Brazil, despite strong scientific output in health biotechnology and established institutions like FIOCRUZ and the Butantan Institute, faces challenges from economic volatility and a fragmented private sector that limits sustained research and development investment in fermentation technologies. Technical expertise limitations become particularly evident in precision fermentation applications, where successful commercialization requires transdisciplinary approaches involving multiple stakeholders and sophisticated process optimization capabilities that exceed current regional capabilities. The shortage of qualified professionals creates bottlenecks in scaling fermentation operations, particularly as Brazil's new bioinputs regulations require qualified professionals for commercial production, potentially constraining industry growth until educational institutions expand relevant training programs

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Amino Acids Lead Despite Polymer Innovation

Amino acids accounted for 44.12% of the South American fermented ingredients market revenue in 2025. The segment's growth stems from feed optimization requirements in the region's livestock sector. Manufacturers utilize the region's corn and soybean resources to produce lysine, methionine, and threonine, which improve feed-conversion efficiency in poultry and swine production. Brazil's dual role as a protein exporter and ethanol producer provides co-products that reduce glucose production costs, enabling competitive amino acid pricing. The polymer segment is expected to grow at a 9.18% CAGR, driven by new plastic waste regulations that encourage biodegradable packaging adoption. Government purchasing policies in Chile and Colombia favor compostable materials, increasing market opportunities for fermentation-based polyhydroxyalkanoates.

Organic acids and vitamins maintain consistent demand in food and beverage production as natural preservatives and fortification ingredients. Industrial enzymes secure contracts with biofuel and brewing facilities that need specific catalytic properties. While antibiotics represent a smaller market share due to regional restrictions on medicated feed, they maintain steady sales in veterinary applications. Brazil's Center-West region continues to expand amino acid production, with integrated soy processing facilities utilizing fermentation by-products for energy generation. Polymer production attracts investment for pilot facilities that use sugarcane bagasse hydrolysate to reduce raw material costs. Organic acid manufacturers collaborate with fruit processors to utilize peel waste, supporting circular economy initiatives. The vitamin segment faces challenges from global price fluctuations but benefits from domestic blending operations that reduce import costs.

By Form: Liquid Growth Outpaces Dry Dominance

Dry offerings accounted for 59.05% of sales in 2025, reflecting superior shelf life, ambient transport, and compatibility with existing feed-mill dosing systems. These attributes make dry formats indispensable for rural supply chains that stretch thousands of kilometers across the Amazon basin. Conversely, liquids are forecast to expand at a 9.88% CAGR, riding investments in refrigerated logistics and automated food-processing lines requiring pumpable concentrates. Marker applications include dairy starters delivered in cryoprotectant liquids and industrial enzyme solutions formulated for in-line dosing. The South American fermented ingredients market size for liquid formats will benefit from urban cold-chain build-outs in São Paulo and Santiago, where same-day grocery platforms demand ready-to-use inputs.

Dry formulations will retain leadership in feed, crop-care, and dietary supplement channels that value ease of handling and dilution flexibility. Powder amino acids integrate seamlessly into mash feeds while dry probiotics upscale into capsules for retail pharmacies. Liquid concentrates gain traction in craft-brew and plant-based beverages, where real-time fermentation speed is critical. Some producers deploy dual-format strategies—spray-drying surplus liquid streams to maximize plant utilization—thereby stabilizing margins and mitigating inventory risks across the South America fermented ingredients market.

By Application: Industrial Growth Challenges Food Dominance

Food and beverages maintain market leadership with 51.82% share in 2025, driven by South America's expanding food processing sector, which generated USD 209 billion in Brazil alone during 2022, and increasing consumer demand for natural ingredients and functional foods, according to the Food Export. Fermented ingredients like amino acids and organic acids have applications in various dairy products such as cheese, yogurt, and others. As the consumption of these products is increasing in the region, the demand for these ingredients is increasing. According to the Food and Agriculture Organization data from 2023, per capita consumption of cheese in Brazil was 3.37 kilograms. Industrial applications emerge as the fastest-growing segment with 8.63% CAGR through 2031.

Pharmaceutical applications remain constrained by regulatory complexities and limited local production capabilities, though Brazil's health biotechnology sector shows promise with government prioritization and established research institutions like FIOCRUZ leading development efforts. The industrial segment's rapid growth reflects increasing adoption of fermentation-derived chemicals in manufacturing processes, supported by government initiatives like Brazil's National Bioeconomy Strategy that promotes renewable resource utilization and sustainable manufacturing practices. Other applications, including cosmetics and personal care, show emerging potential as consumer preferences shift toward natural ingredients, though market development remains early-stage compared to established food and feed applications.

Geography Analysis

Brazil commanded 59.48% of regional revenue in 2025, underpinned by its sophisticated bio-inputs law, the 2nd-largest global ethanol output, and a sizable livestock complex. The country’s ANVISA reforms grant clarity on probiotics and enzymes, enabling food-ingredient launches that align with global clean-label standards. DSM-Firmenich’s 100,000-ton Minas Gerais facility illustrates foreign direct investment confidence and supplies cattle supplements to the Midwest ranch belts. Brazil’s farmers' adoption of bio-inputs surpassing 50% further entrenches domestic demand.

Argentina ranks second, supported by export-oriented fruit and vegetable processing and a refreshed Food Code that simplifies import-export formalities. According to the UN Comtradedata from 2024, Argentina exported USD 126.36 million worth of citrus fruits. Owing to this, the market players are processing these fruits into citric acid and other fermented ingredients. Macroeconomic stabilization initiatives aim to lower inflation and unlock credit channels, enhancing the investment climate for the South American fermented ingredients market.

Chile posts the swiftest trajectory with a 8.79% CAGR forecast to 2031, propelled by aggressive circular-economy mandates and venture-backed precision-fermentation start-ups such as Luyef Cultivated X. Government grants encourage conversion of fruit and viticulture waste into substrates, shrinking raw-material costs, and advancing carbon goals. Colombia and the rest of South America—Peru, Ecuador, and Bolivia—capitalize on traditional fermented beverages that foster consumer acceptance of bio-based ingredients, albeit with limited industrial infrastructure compared to Brazil or Argentina. Cross-border knowledge-sharing alliances seek to elevate pilot plants into commercial clusters, broadening geographic balance within the South American fermented ingredients market.

Competitive Landscape

The South American fermented ingredients market is moderately fragmented. Global companies like DSM-Firmenich, BASF, Evonik, and Novonesis leverage their advantages in scale, strain development capabilities, and regulatory expertise to secure profitable contracts. These multinational corporations maintain sophisticated research facilities and quality control systems across the region. Their established presence and technical capabilities enable them to meet stringent requirements for high-value applications.

Regional companies, including Proquiga Biotech and Lesaffre Group (Bio Springer), specialize in producing amino acids, organic acids, and bio-fertilizers adapted to local agricultural needs. These regional players compete with imports through their strong supply chain relationships and faster delivery times. Their understanding of local market dynamics and agricultural practices provides a competitive edge. In emerging segments, companies like Typical and Future Cow use precision fermentation technology to produce mycoprotein and dairy protein alternatives for hybrid meat and beverage products.

Companies in the market compete through three main approaches: integration with raw material sources, proprietary strain development, and customer application support. Companies that integrate fermentation facilities with sugar-ethanol operations secure access to cost-effective raw materials. Those that develop advanced metabolic engineering capabilities can produce specialized molecules that meet strict specifications and command higher prices. Application laboratories in São Paulo and Buenos Aires provide technical support to bakeries, breweries, and feed manufacturers, helping strengthen customer relationships and expand the South American fermented ingredients market.

South America Fermented Ingredients Industry Leaders

Evonik Industries AG

Novozymes A/S

BASF SE

Archer Daniels Midland Company

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Lubrizol, a global specialty chemistry company, announced the pre-launch of Carbopol BioSense polymer in Brazil. This is the first readily biodegradable ingredient in the Carbopol product line. Carbopol rheological modifiers enhance viscosity and consistency in hair gels, body lotions, moisturizing gels, hair styling gels, shampoos, sunscreens, pharmaceutical products, and household care products.

- April 2023: Royal DSM launched a comprehensive toolkit aimed at enhancing plant-based fermented products, such as yogurt alternatives. This toolkit features four newly crafted starter cultures and five consumer-ready concepts. With its Plant Power Toolkit, DSM simplifies the formulation process for producers, enabling them to swiftly introduce high-quality plant-based fermented products to the market.

South America Fermented Ingredients Market Report Scope

South America fermented ingredient market is segmented by Type into Amino Acids, Organic Acids, Polymers, Vitamins, Industrial Enzymes, and Antibiotics. The market is segmented by Form into Dry and Liquid. The market is segmented by Application into Food & beverages, Feed, Pharmaceutical, Industrial Use, Others. The report also includes the geographical segmentation of the market fragmented as Brazil, Argentina, and Rest of South America.

By Product Type

| Amino Acids | Lysine |

| Methionine | |

| Threonine | |

| Other Amino Acid | |

| Organic Acids | Lactic Acid |

| Citric Acid | |

| Others | |

| Polymers | |

| Vitamins | |

| Industrial Enzymes | Proteases |

| Amylases | |

| Other Industrial Enzymes | |

| Antibiotics |

By Form

| Dry |

| Liquid |

By Application

| Food and Beverages | Dairy |

| Bakery and Confectionery | |

| Beverages | |

| Meat and Seafood Products | |

| Functional and Fortified Foods | |

| Other Food and Beverage Applications | |

| Feed | |

| Pharmaceutical | |

| Industrial Application | |

| Other Applications |

By Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Product Type | Amino Acids | Lysine |

| Methionine | ||

| Threonine | ||

| Other Amino Acid | ||

| Organic Acids | Lactic Acid | |

| Citric Acid | ||

| Others | ||

| Polymers | ||

| Vitamins | ||

| Industrial Enzymes | Proteases | |

| Amylases | ||

| Other Industrial Enzymes | ||

| Antibiotics | ||

| By Form | Dry | |

| Liquid | ||

| By Application | Food and Beverages | Dairy |

| Bakery and Confectionery | ||

| Beverages | ||

| Meat and Seafood Products | ||

| Functional and Fortified Foods | ||

| Other Food and Beverage Applications | ||

| Feed | ||

| Pharmaceutical | ||

| Industrial Application | ||

| Other Applications | ||

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the South America fermented ingredients market?

The South America fermented ingredients market stands at USD 2.68 million in 2026 with a projection of USD 3.82 million by 2031.

Which country holds the largest share of the South America fermented ingredients market?

Brazil leads with 59.48% revenue share in 2025.

Which product segment grows the fastest?

Polymers are projected to expand at a 9.18% CAGR through 2031 on mounting demand for biodegradable packaging.

How fast is the industrial application segment growing?

Industrial uses such as bio-based chemicals are forecast to climb at an 8.63% CAGR between 2026-2031 as circular-economy policies take hold.

Page last updated on: