Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.20 Billion |

| Market Size (2026) | USD 11.45 Billion |

| Market Size (2031) | USD 12.54 Billion |

| Growth Rate (2026 - 2031) | 1.84% CAGR |

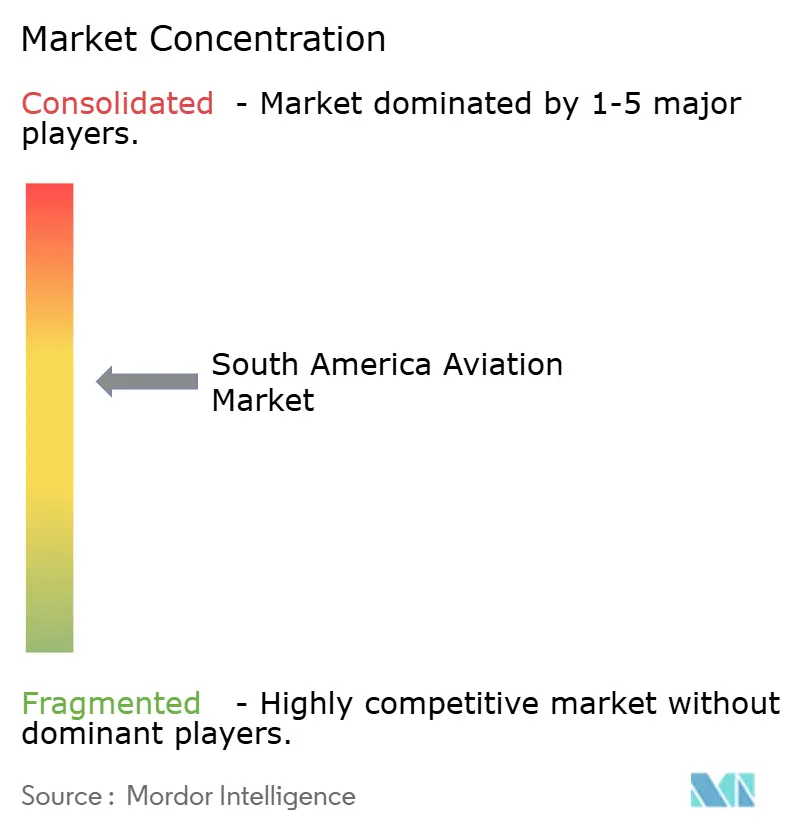

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Aviation Market Analysis by Mordor Intelligence

The South America aviation market size is expected to grow from USD 11.20 billion in 2025 to USD 11.45 billion in 2026 and is projected to reach USD 12.54 billion by 2031, at a 1.84% CAGR over 2026-2031. This trajectory reflects capacity discipline after restructurings, selective modernization of airports and airspace systems, and targeted fleet renewal that favors efficient single-aisle and regional jets suited to the region’s stage lengths. Brazil remains the anchor of regional connectivity as airlines rebuild networks and optimize schedules, while Colombia’s hub position strengthens with rising throughput and route diversification. The market benefits from underserved secondary city pairs and low air travel penetration outside major metros, which creates structural room for demand capture as frequencies and aircraft gauge are tuned to local conditions. Digital operations, predictive analytics, and cargo network upgrades support margins and resilience as carriers balance cost inflation and currency volatility.

Key Report Takeaways

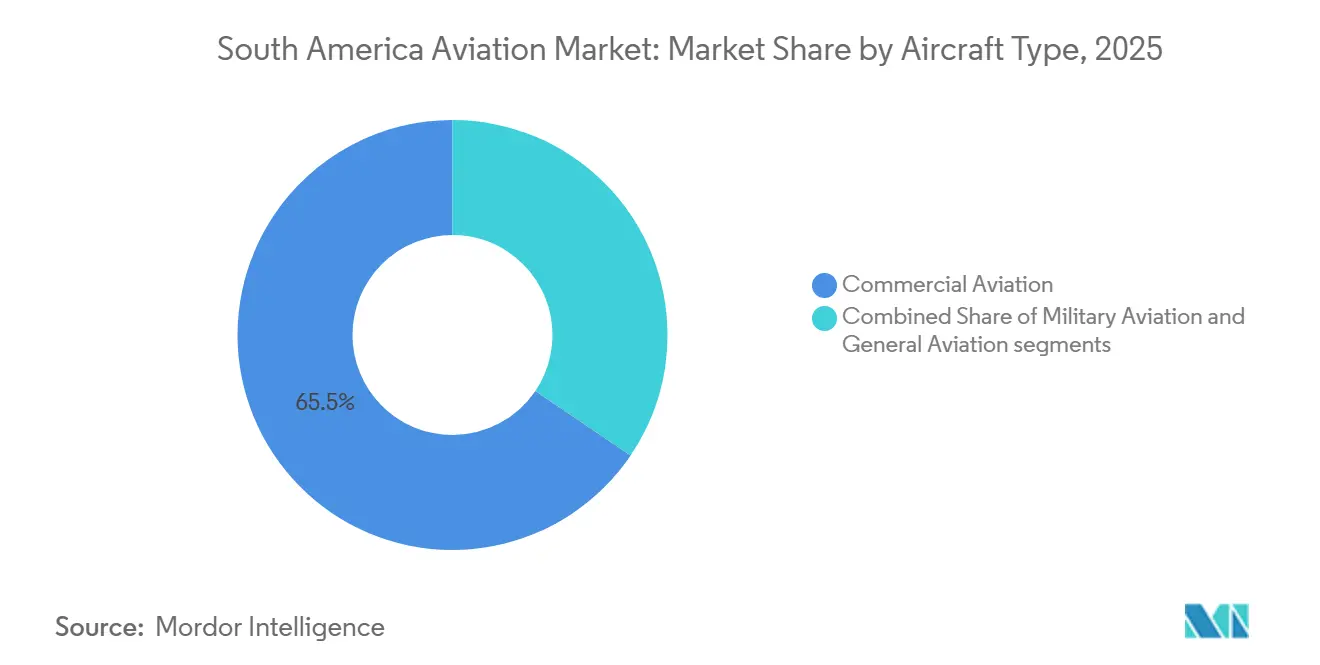

- By aircraft type, commercial aviation led with 65.54% of the South America aviation market share in 2025, and military aviation is projected to expand at a 5.10% CAGR through 2031.

- By propulsion technology, turbofan engines commanded 62.41% share of the South America aviation market size in 2025, while turboshaft applications are projected to post the fastest growth at a 3.10% CAGR through 2031.

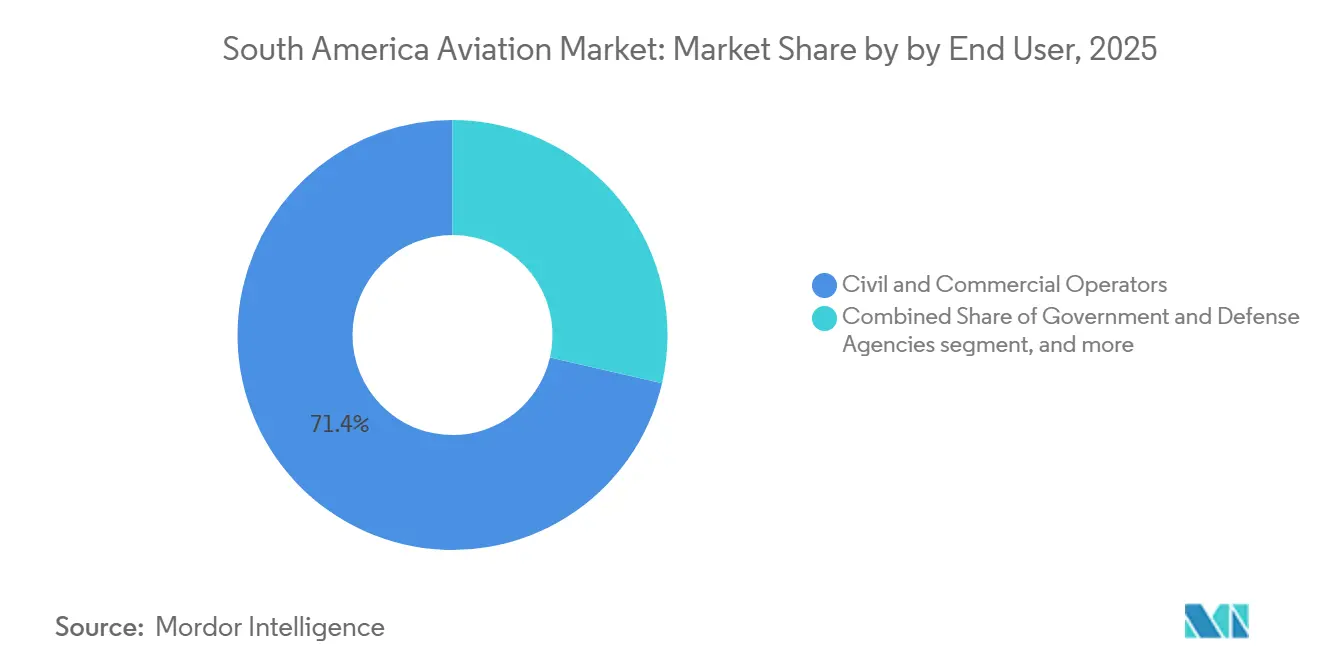

- By end user, civil and commercial operators held a 71.40% share in 2025, while business and general aviation owners are projected to grow at a 3.78% CAGR through 2031.

- By geography, Brazil held 47.87% of the South America aviation market in 2025, and Colombia is projected to have the fastest growth outlook of 3.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Aviation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged fleet renewal cycles favor fuel-efficient regional jets | +0.6% | Brazil, Colombia, Chile, with orders rippling across South America | Medium term (2-4 years) |

| Near-shoring of supply-chain components into Brazil’s aero-clusters | +0.4% | Brazil, with supplier links into Mexico | Medium term (2-4 years) |

| Cross-border e-commerce boosts dedicated narrowbody freighter conversions | +0.3% | Brazil, Mexico, with Peru and Colombia as secondary hubs | Medium term (2-4 years) |

| Government-backed green-aviation funds support SAF R&D | +0.3% | Brazil, Chile, and Colombia | Long term (≥ 4 years) |

| 5G ATG and connectivity corridors improve business-aviation economics | +0.2% | Brazil, Mexico, early deployment in Argentina and Colombia | Short term (≤ 2 years) |

| Monetizing real-time flight-data analytics | +0.2% | Global, with early uptake in Brazil, Colombia, and Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Fleet Renewal Cycles Favor Fuel-Efficient Regional Jets

Airlines are pivoting to newer single-aisle and modern regional jets to reduce seat-mile costs and open thinner routes that connect secondary cities with shorter runways. This shift aligns with the South America aviation market’s stage lengths, where efficient narrowbodies and right-sized regional aircraft match demand and infrastructure constraints. Delivery outlooks support this pivot as carriers prioritize operating economics over widebody expansion in the near term. OEM roadmaps emphasize fuel burn improvements and reliability, which helps airlines defend margins when fuel and currency costs are volatile. The result is a network design that adds frequencies, increases gauge flexibility, and improves load factor stability across domestic and intra-regional corridors.

Near-Shoring Of Supply Chains Into Brazil’s Aero-Clusters

Aerospace suppliers are investing in engineering centers and R&D footprints around São José dos Campos and Campinas to shorten lead times and deepen collaboration with OEMs.[1]Source: Safran, “Safran moves to a new engineering center in Brazil,” safran-group.com These moves consolidate specialized talent and enable more responsive support for aircraft programs that will shape fleet renewal across the market. Localized engineering, testing, and certification functions also reduce logistics risk and strengthen maintenance, repair, and overhaul readiness for the installed base. Near-shoring builds a pipeline of high-skilled roles in avionics, structures, and data engineering, accelerating the diffusion of technology across operators. The broader effect is a more resilient supply chain that can better align production schedules with airline procurement plans in the region.

Cross-Border E-Commerce Boosts Narrowbody Freighter Conversions

Express logistics and cross-border retail are driving demand for time-definite delivery, underscoring the need for dedicated narrowbody freighters to complement belly capacity. Operators in the market are turning to B737 and A321 conversion programs to serve high-frequency, medium-range lanes with better yields. The focus is on overnight networks that connect key production and distribution centers with consumer markets where road infrastructure adds unpredictable transit times. New digital cargo standards and process automation reduce dwell times and improve visibility from tender to delivery. These improvements support aircraft utilization and asset payback assumptions for freighter fleets sized to intra-regional demand patterns.

Government-Backed SAF R&D In Chile And Brazil

National programs and early-stage consortia are laying the groundwork for sustainable aviation fuel pathways, including mapping of feedstocks and prospective production sites. The near-term impact on the South America aviation market is limited by cost and scale, but policy signals are aligning industry planning and R&D investment. Partnerships between industry and academia are profiling regional potential while preparing permitting and certification frameworks. Over the medium term, this foundation can support pilot projects and offtake agreements that reduce future compliance risk. Long-term benefits hinge on bridging the cost gap and scaling production to meet mandated blending or operator ESG commitments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility raising CAPEX financing costs | -0.4% | Brazil, Argentina, Colombia, Peru | Short term (≤ 2 years) |

| Airline bankruptcies suppress near-term order backlogs | -0.3% | Brazil and broader South America | Short term (≤ 2 years) |

| Limited SAF production capacity delays net-zero road-maps | -0.2% | Regionwide, with Brazil and Chile planning initiatives | Long term (≥ 4 years) |

| Rising import tariffs on aero-engines and avionics in Argentina | -0.1% | Argentina with regional effects on fleet plans | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Raises CAPEX Financing Costs

A structural exposure to dollar-denominated inputs and financing raises costs when local currencies weaken against the US dollar. Airlines absorb mismatches between hard-currency leases, fuel, and debt service and local-currency revenues, which tighten margins and slow fleet expansion plans. Interest rate cycles and inflation also influence refinancing, lease renewals, and working capital needs across the South America aviation market. Industry outlooks for the Americas have highlighted currency and inflation as material headwinds even as traffic and yields normalize.[2]Source: International Air Transport Association, “Airline Profitability to Strengthen Slightly in 2025 Despite Headwinds,” iata.org Stabilization will depend on macro conditions improving and airlines maintaining capacity discipline and cost rigor in the near term.

Airline Bankruptcies Temper Near-Term Order Backlogs

Recent restructurings created healthier balance sheets but introduced a cautious stance on new orders and deliveries. Lessors and OEMs are sequencing commitments to match financial recovery timelines, which keeps capacity growth measured in the South America aviation market. Network rebuilds focus on core routes and profitable frequencies with careful deployment of new aircraft. Competitive dynamics have shifted toward efficiency, reliability, and digital operations rather than rapid fleet expansion. As earnings stabilize, airlines can revisit deferred fleet decisions aligned with sustainable cash generation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbody Proliferation Locks in Regional Jet Dependency Through 2031

Commercial aviation commanded a 65.54% share in 2025, reflecting the dominance of single-aisle operations aligned to the region’s 800 to 2,500 kilometer stage lengths. This footprint keeps network design anchored to high-frequency, medium-haul routes that balance load factors and yields across domestic and near-neighbor corridors. The market continues to favor aircraft families that combine short field performance with maintenance efficiency and competitive fuel burn. Narrowbody and modern regional jet programs are positioned to address both trunk and secondary city pairs as airport upgrades proceed unevenly. The near-term schedule growth focuses on restoring connectivity and right-sizing the gauge, with widebody usage focused on long-haul flows where premium demand supports twin-aisle economics.

As corporate mobility, fractional programs, and mission operations expand in major economies, General aviation is set to outpace the overall market, boasting a projected 3.54% CAGR through 2031. Demand patterns reflect a mix of point-to-point business travel, aeromedical, and special missions, favoring reliable light and midsize jets and high-performance turboprops. This segment enhances network resilience in the South America aviation market by serving thousands of locations beyond the reach of scheduled airlines. Fleet additions and avionics upgrades are supported by substantial OEM backlogs for business jets and a healthy pipeline of mission equipment integrations. Military aviation also contributes a steady demand through air power recapitalization and training, with additional lift from emerging unmanned platforms over the forecast window.

By Propulsion Technology: Turbofan Dominance Persists Yet Turboshaft Applications Diversify into Mining and Offshore Energy

Turbofan engines accounted for a 62.41% share in 2025, driven by single-aisle fleets that anchor commercial operations across the region. Airlines continue to prioritize engine variants that reduce fuel burn and maintenance burden while delivering high dispatch reliability. This technology path aligns with the market, where aircraft cycle counts and stage lengths reward efficiency upgrades and durability. The adoption of engine health monitoring and predictive maintenance further enhances availability, reinforcing operator preference for proven families. The installed base will keep turbofans as the primary propulsion choice through the forecast period as replacement programs and incremental deliveries proceed.

Turboshaft platforms are projected to grow at the fastest rate, with a 3.10% CAGR through 2031, driven by demand in offshore energy, mining logistics, public safety, and aeromedical missions. Rotorcraft fleets support personnel transfers, remote-area access, and critical services in geographies where fixed-wing runways are scarce or terrain-limited. OEM order momentum and in-region deployments signal durable mission demand and evolving fleet modernization cycles in large markets. This acceleration complements fixed-wing growth and adds resilience to the South America aviation market by enabling year-round access to complex operating environments. As operators upgrade mission avionics and pursue performance improvements, MRO activity and training expand in tandem across primary heli-hubs.[3]Source: Bell, “Bell Celebrates a Record-Breaking Year in Latin America,” bellflight.com

By End User: Civil Operators’ Load-Factor Optimization Contrasts with Business Aviation’s Fractional Proliferation

Civil and commercial operators held a 71.40% share in 2025, underscoring the scale of scheduled passenger and cargo flows that define the region’s connectivity. Airlines are optimizing capacity and load factors through dynamic network planning and digital revenue management amid persisting macro headwinds. Seat growth remains measured and concentrated in corridors that balance price-sensitive demand and stable yields. Low-cost and hybrid carriers expand addressable markets by improving frequency choices and stimulating new-to-fly customers. The South America aviation market reflects this balance by pairing disciplined capacity with continued connectivity restoration across domestic and intra-regional routes.

Business and general aviation owners, with a projected CAGR of 3.78% through 2031, are broadening their operational reach. This expansion is facilitated by fractional models and managed fleets, which are easing entry barriers for corporate users. Connectivity, safety enhancements, and predictable availability increase the value proposition relative to on-demand charter for frequent flyers. This segment adds flexibility to the market by serving routes and schedules that scheduled carriers cannot reach. OEM forecasts point to steady deliveries into South America over the decade as fleets refresh and expand. Mission diversity and network reach will sustain the segment’s above-market growth profile through the forecast horizon.

Geography Analysis

In 2025, Brazil commands a dominant 47.87% share of the market, solidifying its status as the region's leading aviation hub, buoyed by its extensive domestic network and multiple operational hubs. Airlines have returned capacity to routes that connect economic centers and tourist destinations while rebuilding international connectivity. Regulatory modernization has also progressed, including surveillance mandates and data infrastructure that support safety and efficiency gains for operators. Cargo flows benefit from airport facilities that provide specialized handling for pharmaceuticals and perishables. The South America aviation market in Brazil combines scale, diversified demand, and modernization initiatives that, together, anchor growth through the forecast period.

Colombia, the fastest-growing major geography, is set to achieve a CAGR of 3.65% from 2026 to 2031, driven by network expansion and airport upgrades that enhance both throughput and service quality. The main hub has strengthened its leadership in regional connectivity through more long-haul and intra-regional links. Domestic carriers have increased frequencies on trunk routes and refined fleet mixes to serve both price-sensitive and time-sensitive travelers. These moves broaden access in secondary cities and lift the utilization of regional aircraft across key corridors. Colombia's infrastructure momentum gains recognition, with schedules amplifying the benefits.

Chile shows mixed signals as international routes remain resilient while domestic traffic has softened under economic headwinds. Carriers have adjusted frequencies and capacity to match demand and fare elasticity in the short term. Mining-linked travel and selected city pairs continue to perform, supported by premium demand on specific rotations. Policy discussions on sustainability and noise management are ongoing alongside airlines' operational adjustments. Chile's market adeptly merges global prowess with a measured local capability, ensuring both yield protection and reliability.

Competitive Landscape

South America’s competitive dynamics reflect a post-restructuring equilibrium in which legacy carriers defend their share through joint ventures, network optimization, and cost discipline. Seat capacity growth is modest and targeted, with carriers prioritizing reliability, fleet efficiency, and digital operations to sustain margins. Low-cost and hybrid models add frequencies on high-demand lanes, reduce average fares, and bring new customers into the system. OEMs and suppliers align to this landscape through backlogs that favor single-aisle and regional aircraft and through in-region support footprints.

On the supply side, manufacturers and system providers expand their presence and partnerships to support operators across the lifecycle. Safran’s expansion in Brazil strengthens engineering and certification capabilities close to airline and OEM partners. Airbus Helicopters and leasing partners are delivering new rotorcraft to serve offshore energy and public services, while Bell reports robust regional order activity. Textron Aviation is adding new business jet customers in South America as corporate demand broadens. These moves deepen the region’s ecosystem and align with the South America aviation market’s fleet renewal and mission needs.

Digital capabilities are now a core differentiator. Airlines and airports are leveraging real-time data and APIs for operations control, disruption recovery, and passenger service. Business aviation and corporate operators are investing in onboard connectivity that transforms travel time into productive time. Cargo stakeholders are adopting data-sharing standards that improve transparency and speed across borders. The market rewards these technology investments with better asset utilization, higher customer satisfaction, and improved cost control.

South America Aviation Industry Leaders

Embraer S.A.

Airbus SE

The Boeing Company

Bombardier Inc.

Dassault Aviation S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Embraer unveiled the Praetor 600E and Praetor 500E, signaling a strategic advancement in general aviation. The introduction of reimagined cabins and exclusive technologies, such as the 42-inch 4K OLED Smart Window, positions Embraer to address growing demand for productivity-focused, long-range private jets.

- September 2025: Embraer secured a strategic agreement with LATAM Airlines Group S.A. for up to 74 E195-E2 aircraft, including 24 firm orders and 50 purchase options. Deliveries will begin in 2026, initially supporting LATAM Airlines Brazil.

South America Aviation Market Report Scope

The South America aviation market encompasses the sales of fixed-wing and rotary-wing aircraft in the region's commercial, military, and general aviation sectors. The report offers the latest trends, size, share, and market overview.

The South America aviation market is segmented by aircraft type, propulsion technology, and end user. By aircraft type, the market is segmented into commercial aviation, military aviation, and general aviation. By propulsion technology, the market is segmented into turboprop, turbofan, piston engine, turboshaft, and others. By end user, the market is segmented into civil and commercial operators, government and defense agencies, and business and general aviation owners. The report also covers the market sizes and forecasts for five countries throughout the region. The market size and forecast for each segment are provided in terms of value (USD).

By Aircraft Type

| Commercial Aviation | Passenger Aircraft | Narrowbody Aircraft |

| Widebody Aircraft | ||

| Regional Jets | ||

| General Aviation | Business Jets | Large Jet |

| Mid-Size Jet | ||

| Light Jet | ||

| Piston and Turboprop Aircraft | ||

| Commercial Helicopters | ||

| Military Aviation | Fixed-Wing Aircraft | Combat Aircraft |

| Multi-Role Aircraft | ||

| Transport Aircraft | ||

| Training Aircraft | ||

| Rotorcraft | Multi-Mission Helicopter | |

| Transport Helicopter | ||

| Others | ||

By Propulsion Technology

| Turboprop |

| Turbofan |

| Piston Engine |

| Turboshaft |

| Others |

By End User

| Civil and Commercial Operators |

| Government and Defense Agencies |

| Business and General Aviation Owners |

By Geography

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Aircraft Type | Commercial Aviation | Passenger Aircraft | Narrowbody Aircraft |

| Widebody Aircraft | |||

| Regional Jets | |||

| General Aviation | Business Jets | Large Jet | |

| Mid-Size Jet | |||

| Light Jet | |||

| Piston and Turboprop Aircraft | |||

| Commercial Helicopters | |||

| Military Aviation | Fixed-Wing Aircraft | Combat Aircraft | |

| Multi-Role Aircraft | |||

| Transport Aircraft | |||

| Training Aircraft | |||

| Rotorcraft | Multi-Mission Helicopter | ||

| Transport Helicopter | |||

| Others | |||

| By Propulsion Technology | Turboprop | ||

| Turbofan | |||

| Piston Engine | |||

| Turboshaft | |||

| Others | |||

| By End User | Civil and Commercial Operators | ||

| Government and Defense Agencies | |||

| Business and General Aviation Owners | |||

| By Geography | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the South America aviation market?

The South America aviation market size is expected to grow from USD 11.20 billion in 2025 to USD 11.45 billion in 2026 and is projected to reach USD 12.54 billion by 2031, at a 1.84% CAGR over 2026-2031.

Which aircraft and engine segments lead the South America aviation market?

Commercial aviation leads by aircraft type and turbofan engines hold the largest share by propulsion, supported by single-aisle fleet dominance across regional stage lengths.

Where are the strongest geographic opportunities within South America?

Brazil remains the largest market, while Colombia shows the fastest growth outlook supported by hub development and network expansion across domestic and intra-regional routes.

How are technology and data shaping competitive advantage in the region?

Predictive maintenance, real-time flight data, and cargo data standards improve reliability, reduce costs, and accelerate cross-border flows, strengthening operator performance.

What are the main constraints on growth through 2031?

Currency volatility, cautious post-restructuring fleet plans, and limited SAF availability are the primary brakes, with cost and scale gaps delaying decarbonization timelines.

How is business aviation evolving in South America?

Connectivity upgrades and fractional models are broadening access and improving utilization, reinforcing above-market growth for corporate and mission operations across the region.

Page last updated on: