South America Agricultural Tractors Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

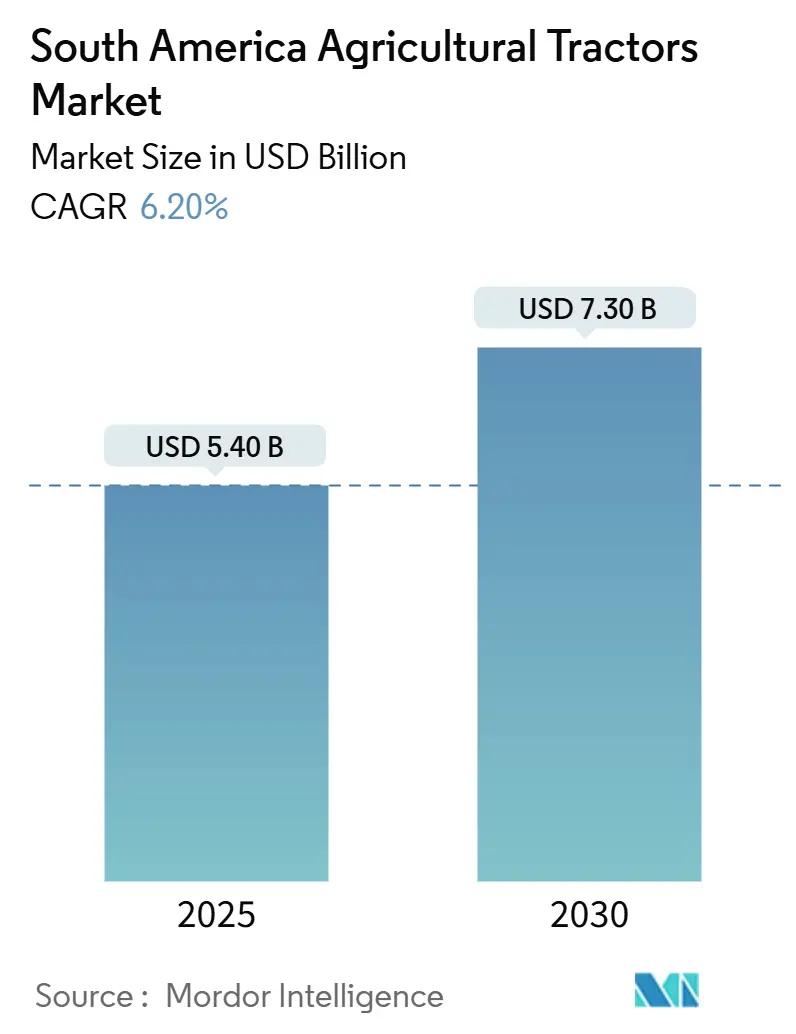

| Market Size (2025) | USD 5.40 Billion |

| Market Size (2030) | USD 7.30 Billion |

| Growth Rate (2025 - 2030) | 6.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Agricultural Tractors Market Analysis by Mordor Intelligence

The South America agricultural tractors market size stands at USD 5.4 billion in 2025 and is projected to reach USD 7.3 billion by 2030, registering a 6.2% CAGR over the forecast period. Growth is being steered by expanding soybean and corn acreage, sustained government credit lines, and incremental mechanization in high-value fruit belts. Demand fluctuations remain closely tied to commodity-price swings and financing costs, yet long-run fundamentals such as labor shortages and the push for climate-smart production continue to pull the market upward. Leading suppliers are insulating margins by localizing manufacturing, shortening R&D cycles, and layering precision-agriculture software onto hardware bundles.[1]Source: Monetary Policy Committee, “Selic Rate Decision,” Banco Central do Brasil, bcb.gov.br These moves are timely because Chinese and European competitors are positioning for tariff-driven price realignments once the Mercosur-EU–EU agreement clears its political hurdles[2]Source: Agricultural Machinery Department, “Agricultural Machinery Sales 2024,” ANFAVEA, anfavea.com.br.

Key Report Takeaways

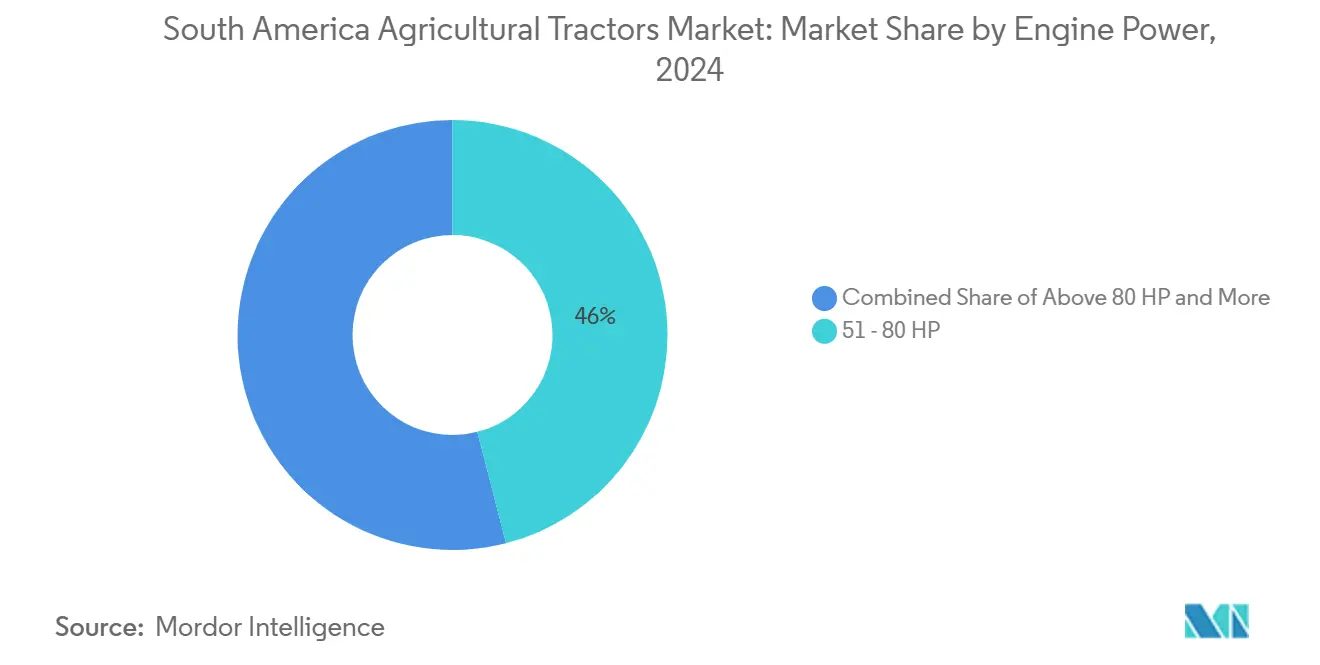

- By engine power, the 51–80 HP segment captured 46% of the South America agricultural tractors market share in 2024, and the Above 80 HP segment is forecast to expand at an 8.7% CAGR through 2030.

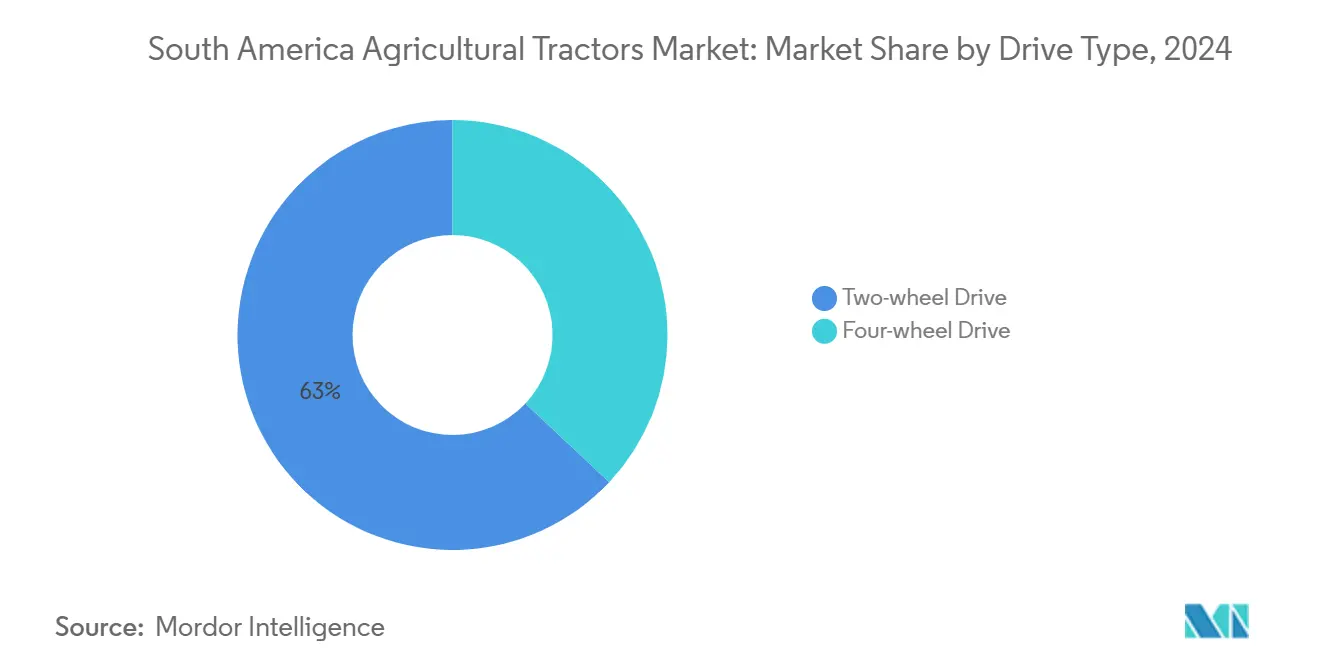

- By drive type, two-wheel drive units held 63% of the South America agricultural tractors market size in 2024, while four-wheel drive units are advancing at a 9.5% CAGR due to the adoption of Cerrado and slope farming.

- By application, row-crop tractors led with 58% of the South America agricultural tractors market size in 2024, whereas orchard tractors are projected to grow at a 7.1% CAGR through 2030.

- By country, Brazil commanded 61% of the South America agricultural tractors market share in 2024, while Paraguay is projected to grow at an 8.6% CAGR through 2030.

South America Agricultural Tractors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies and soft loans for farm mechanization | +1.2% | Brazil and Argentina | Medium term (2–4 years) |

| Labor shortage and rising wages | +0.9% | Brazil, Chile, and Colombia | Long term (≥ 4 years) |

| Expansion of soybean and corn acreage | +1.5% | Brazil and Argentina | Short term (≤ 2 years) |

| Surge in sugarcane-specific precision tractor demand | +0.7% | Brazil | Medium term (2–4 years) |

| Rise of subscription-based tractor-as-a-service models | +0.4% | Brazil and Argentina | Long term (≥ 4 years) |

| Climate-smart agriculture funds for low-emission tractors | +0.5% | Brazil and Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies and Soft Loans for Farm Mechanization

Brazil’s Moderfrota program allotted BRL 12.3 billion (USD 2.3 billion) in 2024/25 at 11.5% interest, narrowing the cost of capital gap even as the Selic rate heads toward 14.25% by March 2025. Provincial lines in Argentina complement national schemes, but recurring import-license delays push dealers toward private financing. John Deere’s tie-up with Bradesco is filling part of the void, and LS Tractor Finance grew 41% in 2023 by offering longer tenors. ABC+- the Low Carbon Agriculture credit window sweetens terms for low-emission models, although adoption still tilts toward large estates with compliance teams. Smaller growers in Paraguay and Uruguay lack equivalent subsidy depth, widening a regional mechanisation divide that continues to channel most sales into Brazil and Argentina.

Labor Shortage and Rising Wages

Brazil’s farm labor pool slipped 3% in 2024 to 7.88 million workers, the lowest level since 2012[3]Source: Agricultural Employment Survey Q3 2024, Brazilian Institute of Geography and Statistics, ibge.gov.br. In Chile, fruit exporters forecast a 469,000-worker shortfall by 2025. Mechanization is the principal release valve. Sugarcane harvesting in Brazil moved past 95% mechanization once manual burning bans took full effect, eliminating roughly 200,000 jobs and creating sustained demand for GPS-guided inter-row tractors. Rising rural wages now shorten machinery payback periods; a 75 HP tractor repays in two harvest cycles on a 200-hectare soybean operation at current margin levels. While peso devaluation tempers nominal wages in Argentina, younger workers across the region display little appetite for manual fieldwork, signaling a structural labor deficit.

Expansion of Soybean and Corn Acreage

Soybean area in Brazil increased 2.8% to 117 million acres in 2024/25, with the Matopiba frontier providing most of the gains. Argentina posted a 7% jump to 44 million acres, the largest uptick since 2015-16, as producers shifted away from corn after pest-linked acreage losses. Double-cropping potential could unlock 40 million additional acres of second-crop corn, compressing planting windows and lifting average horsepower demand. Precision planting raises the value of auto-steer functionality, which adds a price premium yet also drives stronger resale values, a fact that sophisticated operators include in total cost of ownership analyses. Smaller farms in Bolivia and Paraguay stay on older sub-50 HP units, thereby elongating the replacement cycle for a sizable part of the installed base.

Surge in Sugarcane-Specific Precision Tractor Demand

Brazil produced 30.5 billion liters of ethanol in 2023/24, reinforcing sugarcane’s pull on mechanization budgets. Specialized tractors with narrow track widths and high clearance guard against crop damage during inter-row work. CNH Industrial’s Austoft line and John Deere’s CH570 harvester integrate precision guidance that slashes transport costs by up to 12% through smarter haul scheduling. Ethanol’s 27% blend mandate cushions growers against grain price swings, supporting premium equipment purchases even in down commodity cycles. Deere’s ethanol-powered tractor pilot hints that sugarcane estates could become early adopters of low-emission units qualifying for RenovAgro’s preferential financing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront equipment cost | -1.1% | Paraguay, Uruguay, and Bolivia | Short term (≤ 2 years) |

| Commodity-price volatility | -1.3% | Brazil and Argentina | Short term (≤ 2 years) |

| Mercosur tariff uncertainty on imports | -0.6% | Argentina and Brazil | Medium term (2–4 years) |

| Restricted rural credit in smaller economies | -0.8% | Paraguay, Uruguay, Bolivia, Colombia, and Peru | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Upfront Equipment Cost

A 75 HP four-wheel-drive tractor retails at USD 45,000–55,000, equating to 3–4 years of net income for a 200-hectare soybean farm at 2024 margins. Chinese brands underprice incumbents by up to 30% and lifted Brazilian market share to 12.7% in 2024, although lingering doubts around parts supply restrain growth beyond price-sensitive tiers. Farmers in Paraguay face 18–22% interest rates and loan-to-value caps of 60%, extending replacement cycles to 12–15 years. Subscription models cover less than 5% of units, and used-equipment markets remain thin, depriving growers of trade-in liquidity.

Commodity-Price Volatility

Soybean quotes slid from USD 14 per bushel in 2022 to USD 10–11 in 2024, while corn dipped from USD 7 to USD 4–4.50, slicing Brazilian soybean margins from USD 165 to USD 105 per acre. Despite a 2.8% soybean-area expansion, tractor sales fell 19.8% to 48,900 units, underscoring the decoupling of acreage and equipment demand. In Argentina, peso depreciation amplifies repayment risk on dollar-denominated loans, tightening dealer inventory finance and slowing deliveries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Power: Large Farms Drive High-Horsepower Shift

The South America agricultural tractors market records an 8.7% CAGR for units Above 80 HP through 2030, fueled by Argentina’s farm consolidation where producer numbers dropped from 62,379 to 58,039 in five years. These machines let single operators cover more than 1,000 hectares each season, cutting fuel use per hectare by 12%. The 51–80 HP band still commands 46% of 2024 sales and offers versatility for mid-sized grain and sugarcane farms. Under 30 HP tractors have niche relevance in Andean coffee zones, but credit scarcity curtails growth. John Deere’s new Indaiatuba center tailors 60–90 HP models for tropical soils, shortening development lead times by 40%.

Average horsepower continues to edge higher as double-cropping spreads; operators need to harvest soybeans and seed corn within a four-week window to capture soil moisture. Yanmar’s 105 HP unit became a bestseller within months of its 2024 release, and a 125 HP model arrives in 2025. Precision-ag features add weight, demanding stronger engines to maintain field speed without causing compaction, reinforcing the upward horsepower drift within the South America agricultural tractors market.

By Drive Type: Traction Needs Favor Four-Wheel Systems

Two-wheel drive retained 63% of the South America agricultural tractors market size in 2024 because price-sensitive smallholders dominate flat regions like Argentina’s Pampas. Four-wheel drive, grows at 9.5% CAGR as clay-heavy Cerrado soils and hillside orchards demand better traction. Embrapa trials show 18% lower planting-time variance with 4WD, yielding 3–5% output gains. Chilean vineyards use compact 4WD units to navigate 10-degree slopes, and SAME Deutz-Fahr offers 14 tailored models.

Growth links tightly to horsepower migration because OEMs rarely sell 2WD above 90 HP. CNH Industrial’s Sorocaba line now ships 4WD row-crop tractors worldwide, leveraging Brazil’s cost base for export competitiveness. Resale premiums for 4WD average eight percentage points after five years, helping offset the upfront differential and further accelerating adoption within the South America agricultural tractors market.

By Application: Orchard Mechanization Accelerates

Row-crop tractors held 58% of the South America agricultural tractors market share in 2024, reflecting regional dominance in soybeans and corn. Orchard tractors expand at 7.1% CAGR because cherry, blueberry, avocado, and coffee producers struggle with seasonal labor gaps. Chile shipped 413,979 metric tons of cherries in 2023/24 and expects shortages of 469,000 workers by 2025. Compact, high-clearance tractors with 1.5–1.8 meter track widths meet the maneuverability mandate yet cost 10–15% more than row-crop peers. Colombia’s 540,000-hectare coffee belt is slowly mechanizing, shortening manual picking payback periods amid wage inflation.

Row-crop dominance endures because Brazil and Argentina exported 133 million metric tons of soybeans and corn in 2024, a volume requiring roughly 180,000 serviceable tractors. Precision guidance is now bundled in 35–40% of new row-crop units sold in Brazil. Orchard operators lag in data-centric tools but AGCO’s Valtra pilots GPS-guided sprayers that cut chemical use by 12%.

Geography Analysis

Brazil contributed 61% of the South America agricultural tractors market share in 2024, translating into the largest single-nation slice of the South America agricultural tractors market size and reflecting its outsized 117 million-acre soybean footprint and deep federal credit lines. The country’s 48,900 unit sales nevertheless dipped 19.8% in 2024 as higher borrowing costs outweighed acreage gains, signaling that policy rate shifts can overpower subsidy programs when the spread tightens. High-horsepower and four-wheel-drive models remain the backbone of Brazilian demand because double-cropping schedules compress the planting window into as little as three weeks in Mato Grosso and Goiás. Precision guidance adoption is accelerating; roughly 40% of new Brazilian row-crop tractors shipped with factory-installed auto-steer, driving aftermarket software and service revenues that improve total cost of ownership. Competitive positioning is reinforced by localized manufacturing at plants in Montenegro, Sorocaba, and Canoas, which hedge currency swings and shorten delivery lead times.

Paraguay, while accounting for a modest slice of 2024 unit volume, is forecast to log an 8.6% CAGR from 2025 to 2030, the fastest in the region, as soybean acreage expands along the Brazilian border and smallholder cooperatives tap rising export receipts to upgrade fleets. The market is starting from a low mechanization base, average fleet age tops 12 years, and leasing pilots plus tractor-as-a-service pools are gaining traction because local producers face interest rates that are 8–10 percentage points above Brazil’s subsidized loans.

Chile, Colombia, and Peru collectively underpin incremental upside through orchard and coffee mechanization, though fragmented landholdings and rugged topography cap horsepower requirements below 80 HP. Uruguay’s growth remains muted due to shallow credit markets, while Argentina’s rebound hinges on currency stability and the easing of import-license bottlenecks. Overall, widening credit access and rising commodity exports position the smaller Andean and Guarani nations to outpace the regional average, even if Brazil continues to anchor absolute demand.

Competitive Landscape

The South America agricultural tractors market shows moderate concentration. John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra together hold modest percentage of share in 2024, translating into a moderate market concentration. Chinese manufacturers raised import share in 2024 by undercutting prices, yet parts-availability concerns temper broader penetration.

Incumbents counter with localized engineering: Deere’s Indaiatuba center reduces tropical model lead times by 40% and CNH’s Sorocaba hub exports half its output. Precision-ag platforms create sticky ecosystems; switching costs equal 8–12% of tractor value once data migration and training are counted. Yanmar gained traction, climbing to 11% market share by October 2024 and targeting 14% by end-year through dealer expansion and mid-range horsepower launches.

SAME Deutz-Fahr widened its Brazilian network to 28 dealerships, aiming for 35 by 2026 to tap Matopiba’s frontier growth. White-space opportunities lie in tractor-as-a-service and low-emission powertrains. RenovAgro incentives and ethanol-fueled prototypes could see alternative drivetrains capture up to 8% of new sales by 2030 if infrastructure keeps pace.

South America Agricultural Tractors Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

Mahindra & Mahindra Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Mahindra is expanding its South American footprint by entering Argentina’s tractor market, leveraging its new Brazil plant to boost regional production. This move positions Mahindra against established players like Deere & Company, AGCO Corporation, and CNH Industrial N.V., targeting small and medium farmers with affordable tractors.

- February 2025: AGCO is expanding its Jundiaí, Brazil operations with a focus on sustainability and workforce development. This move reinforces its tractor manufacturing capacity in South America, bolstering its presence in the regional agri-machinery market.

- November 2024: TAFE Tractors expanded its operations into South America, targeting Chile, Colombia, Ecuador, and Peru with a variety of compact and utility tractors. The company supports local farming communities by providing cost-effective and fuel-efficient machinery designed to suit diverse crops and terrains.

South America Agricultural Tractors Market Report Scope

| Less than 30 HP |

| 31 - 50 HP |

| 51 - 80 HP |

| Above 80 HP |

| Two-wheel Drive |

| Four-wheel Drive |

| Row-Crop Tractors |

| Orchard Tractors |

| Other Applications |

| By Engine Power | Less than 30 HP |

| 31 - 50 HP | |

| 51 - 80 HP | |

| Above 80 HP | |

| By Drive Type | Two-wheel Drive |

| Four-wheel Drive | |

| By Application | Row-Crop Tractors |

| Orchard Tractors | |

| Other Applications |

Key Questions Answered in the Report

What is the current value of the South America agricultural tractors market?

The market is valued at USD 5.4 billion in 2025 and is forecast to climb to USD 7.3 billion by 2030.

Which engine-power segment leads in sales?

The 51 - 80 HP segment holds 46% of 2024-unit shipments, serving versatile mid-sized farms.

Why is four-wheel drive demand growing?

Rolling Cerrado landscapes and precision tillage needs push growers toward four-wheel drive, which is expanding at a 9.5% CAGR.

How will the Mercosur-EU trade deal affect equipment prices?

If ratified, European tractors could arrive with tariffs 14-18 percentage points lower, intensifying price competition.

Page last updated on: