Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

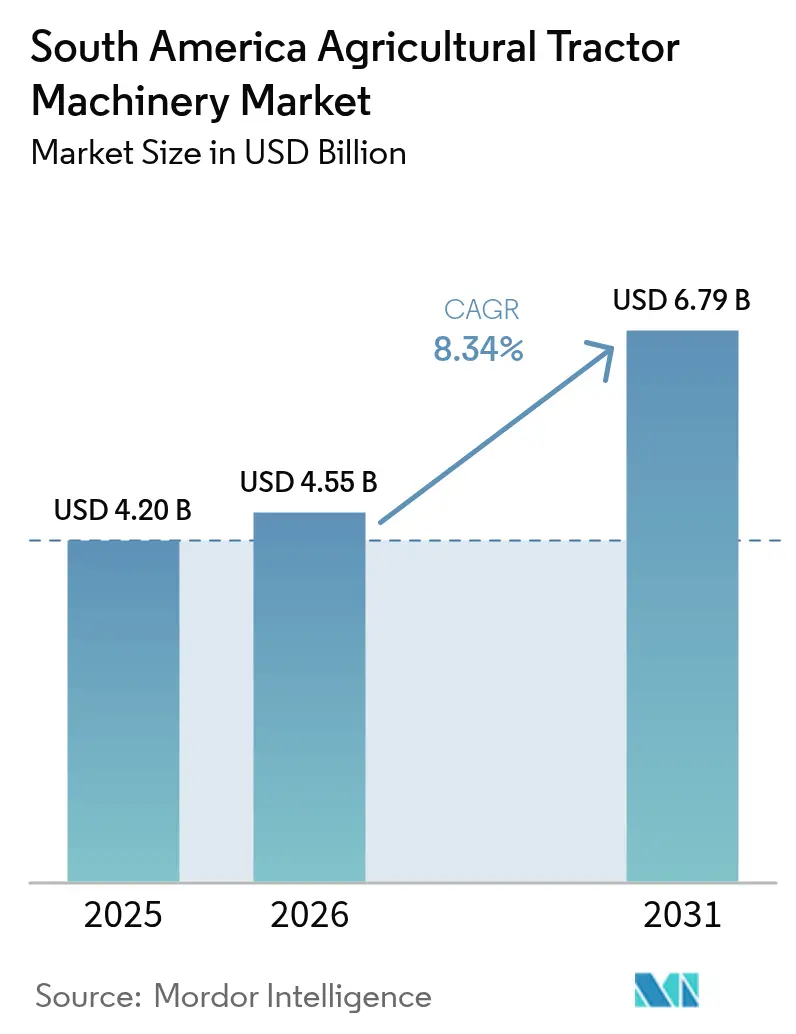

| Base Year Market Size (2025) | USD 4.20 Billion |

| Market Size (2026) | USD 4.55 Billion |

| Market Size (2031) | USD 6.79 Billion |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

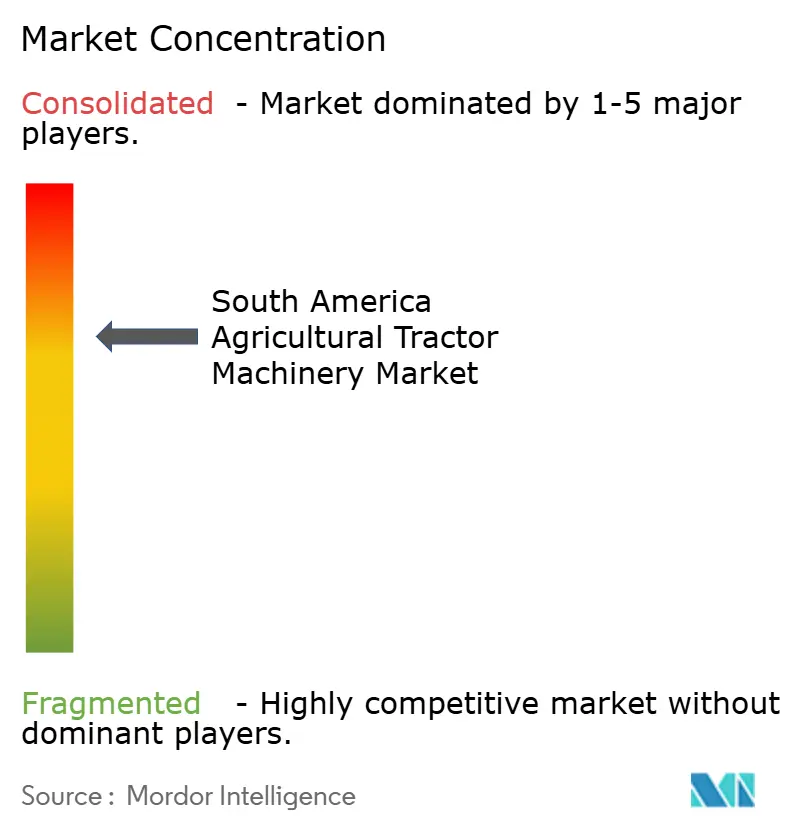

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The South America agricultural tractor machinery market size was valued at USD 4.20 billion in 2025 and estimated to grow from USD 4.55 billion in 2026 to reach USD 6.79 billion by 2031, at a CAGR of 8.34% during the forecast period (2026-2031). The acceleration stems from a structural shift toward mechanized farming that is funded by government-backed credit, spurred by expanding soybean acreage, and amplified by tightening rural labor supply. Credit programs such as Brazil’s Plano Safra and Moderfrota are lowering financing costs, while Argentina’s Banco de la Nación Argentina and multilateral lenders are supplying additional liquidity that pushes machinery demand into mid-sized operations. Labor scarcity is widening the productivity gap between mechanized and manual farms, prompting rapid adoption of self-propelled sprayers and high-capacity planters. Original-equipment manufacturers (OEMs) are responding with connected platforms that blend telematics, artificial intelligence, and subscription pricing to keep total cost of ownership in check. Currency volatility and gray-market imports remain headwinds, yet retrofit kits, precision attachments, and carbon-smart subsidies continue to broaden the addressable base for both high-horsepower units and compact tractors.

Key Report Takeaways

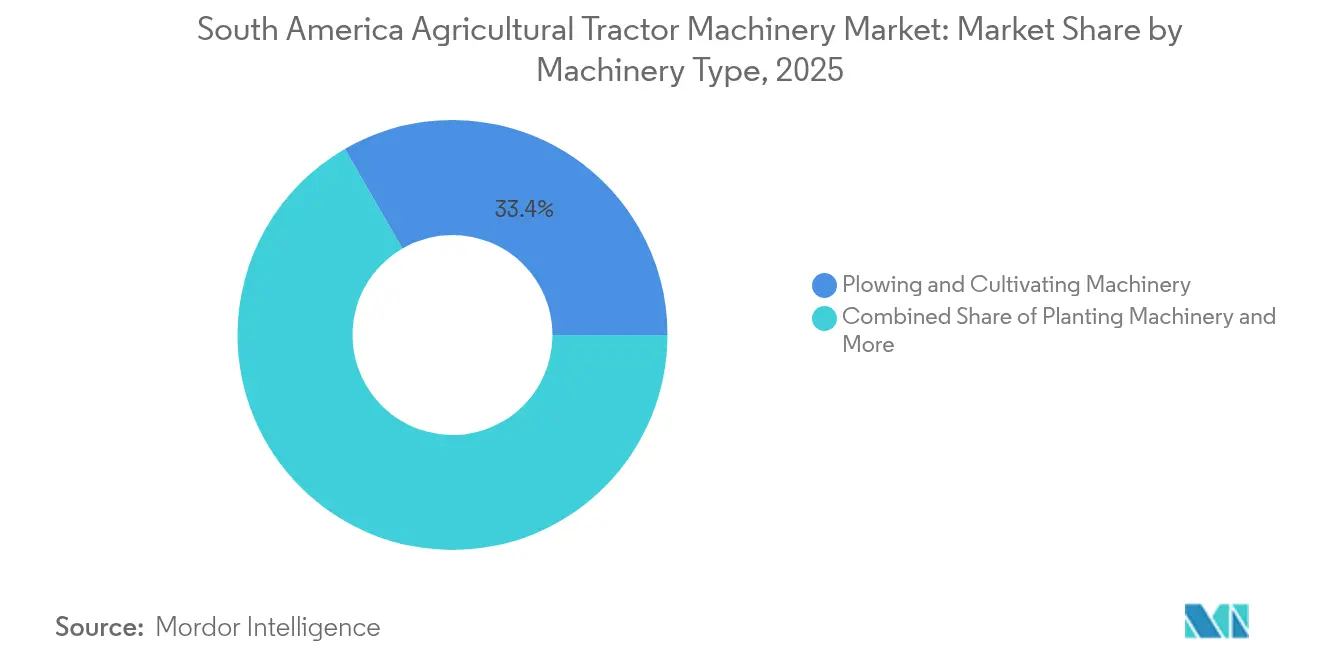

- By machinery type, plowing and cultivating equipment accounted for a 33.35% share of the South America agricultural tractor machinery market in 2025, whereas sprayers are forecast to post the fastest 10.11% CAGR through 2031.

- By geography, Brazil controlled an estimated 56.60% share of the South America agricultural tractor machinery market size in 2025, while Paraguay is projected to expand at the strongest 9.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Agricultural Tractor Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust government credit lines for mechanization | +1.8% | Brazil, Argentina, and Paraguay | Medium term (2-4 years) |

| Rising commercial soybean acreage in Brazil and Argentina | +2.1% | Brazil, Argentina, spillover to Paraguay and Uruguay | Long term (≥ 4 years) |

| Labor scarcity driving demand for self-propelled equipment | +1.5% | Brazil, Argentina, and Chile | Medium term (2-4 years) |

| OEM financing arms lowering total cost of ownership | +1.2% | Brazil, Argentina, and Colombia | Short term (≤ 2 years) |

| Precision-ag retrofit kits boosting attachment sales | +1.0% | Brazil, Argentina, and regional diffusion | Medium term (2-4 years) |

| Carbon-smart farming subsidies for low-HP machinery | +0.9% | Brazil and Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Government Credit Lines for Mechanization

Brazil’s Moderfrota program, managed by the Brazilian Development Bank (BNDES), earmarked around USD 2.3 billion for the 2024/25 crop year at interest rates between 7% and 10.5%[1]Source: BNDES, “Moderfrota Funding Details,” bndes.gov.br. The allocation rose 15% from the previous cycle and filled the gap left by an 8% drop in commercial bank lending. Argentina’s Banco de la Nación Argentina extended USD 1.2 billion in machinery loans, yet peso devaluation trimmed purchasing power and narrowed growers’ shopping lists. Paraguay’s Crédito Agrícola de Habilitación disbursed funds in 2024 and channeled almost one-quarter into equipment, reflecting the nation’s plan to double soybean exports by 2030. Captive finance subsidiaries of CNH Industrial and John Deere are leveraging these programs to package below-market loans with bundled service plans that lock in brand loyalty.

Rising Commercial Soybean Acreage in Brazil and Argentina

Brazil’s soybean area reached 47–48.2 million hectares for the 2024/25 cycle, up from 46.3 million hectares in the prior year[2]Source: USDA Foreign Agricultural Service, “Brazil Soybean Area Expands to 47-48 Million Hectares for 2024/25,” usda.gov. Argentina followed with a 7% jump to 44 million acres, pushing regional output to 237.8 million metric tons. Double-cropping systems compress planting windows, which favors high-capacity planters, autonomous sprayers, and harvesters equipped with yield monitors. Farms in MATOPIBA routinely span 2,000–5,000 hectares and require machinery that can work around frequent rain events. Precision planting lifted yields 5–10% according to Argentina’s National Institute of Agricultural Technology (INTA), reinforcing the value proposition of variable-rate technology for both seed and crop protection inputs. Robust crush margins and steady Chinese demand keep cash flow healthy, driving machinery reinvestment rates that are 30% greater than for other crops.

Labor Scarcity Driving Demand for Self-Propelled Equipment

Brazil’s rural workforce contracted 3% in 2024 to 7.88 million, the lowest figure since 2012, while agricultural output kept expanding at roughly 3% per year[3]Source: Brazilian Institute of Geography and Statistics, “Brazilian Agricultural Employment Falls to 7.88 Million in 2024,” ibge.gov.br. Urban migration among 18- to 35-year-olds has left vacancy rates above 15% during critical field operations in São Paulo and Mato Grosso. In Argentina, farm labor declined 4% and real wages rose 18%, compressing margins for labor-intensive tasks. Self-propelled sprayers cover up to 500 hectares per day, quadrupling the productivity of towed units and delivering fast payback. Autonomous platforms such as Solinftec’s SOLIX robot already manage 50,000 hectares in Brazil, signaling an emerging robotics wave that could reshape staffing models within five years.

OEM Financing Arms Lowering Total Cost of Ownership

CNH Industrial Financial Services and John Deere Financial financed nearly USD 1.8 billion of equipment purchases across South America in 2024 at interest rates 200–300 basis points below comparable bank loans. Payment terms stretch to 84 months, and trade-in guarantees shelter buyers from volatile residual values. John Deere’s Solution-as-a-Service model, piloted in Brazil, converts machinery ownership into per-hectare subscriptions that turn capital outlays into operating expenses. AGCO Corporation’s Fuse platform combines predictive maintenance and over-the-air updates that cut downtime 15% and extend asset life by up to three seasons. Brazil’s Desenrola Rural debt-relief program restored credit to 180,000 producers, many of whom immediately requalified for OEM finance packages.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency-exchange volatility inflating imported component prices | -1.3% | Brazil, Argentina, and Colombia | Short term (≤ 2 years) |

| Fragmented land-holding patterns limiting large equipment penetration | -1.1% | Brazil, Paraguay, and Colombia | Long term (≥ 4 years) |

| Slow roll-out of Tier III emission norms | -0.8% | Brazil and Argentina | Medium term (2-4 years) |

| Gray-market inflow of used tractors undermining new sales | -0.9% | Brazil, Argentina, and Paraguay | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency-Exchange Volatility Inflating Imported Component Prices

The Brazilian real weakened 11% against the United States dollar during 2024, lifting the landed cost of imported engines, transmissions, and hydraulic subsystems that form up to half of a tractor’s bill of materials. Argentina’s peso depreciation accelerated to 25% per month by late 2024, forcing OEMs to reprice every six weeks and pushing many growers to delay purchases. Colombia’s peso lost 8%, adding USD 3,000–5,000 to the price of imported planters and sprayers. Local assembly cushions part of the shock, yet electronic control units and precision guidance modules still rely on offshore suppliers. OEMs are testing local-currency supply contracts and fast-tracking regional sourcing, but meaningful localization takes at least two seasons to execute.

Fragmented Land-Holding Patterns Limiting Large-Equipment Penetration

Sixty-seven per cent of Brazilian farms cover less than 100 hectares, and 84% sit below 200 hectares, restricting the economic case for 200-plus horsepower tractors and 40-meter boom sprayers that require at least 500 hectares to reach efficient utilization. Paraguay counts 250,000 smallholders averaging 15–30 hectares, while Colombia’s coffee and cocoa plots average 2–5 hectares on steep terrain. These structural realities bifurcate the South America agricultural tractor machinery market: large commercial farms upgrade to high-capacity equipment, whereas smallholders rely on used units, co-ops, or service providers. Brazil’s Nova Indústria Brasil initiative aims to form mechanisation cooperatives covering 30% of family farms by 2033, but progress remains slow due to governance hurdles and uneven credit access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Tillage Dominance Meets Precision Spraying Surge

Plowing and cultivating equipment generated the largest slice of the South America agricultural tractor machinery market size, accounting for 33.35% of 2025 revenue, as conventional tillage remained prevalent across Brazil’s Cerrado and Argentina’s Pampas. Strip-till adoption softens but does not yet displace deep-plowing demand, especially where double-cropping squeezes field preparation into narrow weather windows. Manufacturers capitalize by offering reversible plows and heavy-duty cultivators engineered for clay soils and high residue loads that characterize soybean-corn rotations. On farms experimenting with no-till, shallow cultivators equipped with residue managers find niche demand that preserves soil structure while improving seedbed quality.

Sprayers are the fastest-growing category, projected to log a 10.11% CAGR through 2031 and steadily capture a larger share of the South America agricultural tractor machinery market. Artificial-intelligence weed-detection systems from Cromai cut herbicide use up to 65% and appeal to growers facing rising input costs. Self-propelled platforms with 40-meter booms and customizable nozzle banks dominate purchases on estates above 1,500 hectares. Plug-and-play retrofits push growth farther down the acreage ladder, as mid-sized farmers outfit existing chassis with spot-spray modules that upgrade performance for a fraction of the replacement cost. Manufacturers offering broad telematics compatibility unlock data-driven agronomy services that deepen client stickiness.

Geography Analysis

By geography, Brazil controlled an estimated 56.60% share of the South America agricultural tractor machinery market size in 2025, while Paraguay is projected to expand at the strongest 9.34% CAGR to 2031. Brazil’s leadership position in the South America agricultural tractor machinery market rests on scale, credit depth, and accelerating digitalization. Large-area farms in Mato Grosso, Goiás, and Mato Grosso do Sul routinely deploy fleets of 250- to 350-horsepower tractors, 16-row planters, and self-propelled sprayers with artificial-intelligence boom control. The government’s Plano Safra allocation directs through Moderfrota for machinery alone, while the ABC+ program lowers interest rates for low-horsepower models that cut emissions. John Deere chose Brazil for its Operations Technology Center, reflecting the nation’s role as a testbed for tropical-climate innovation.

Argentina’s market remains precision-agriculture forward despite macro volatility. Growers leverage variable-rate seeders and yield-mapped combine harvesters to maximize narrow margins squeezed by rapid peso depreciation. The INTA drone network integrates with variable-rate sprayers, trimming input waste by up to 18%. Banks denominate leases in soybeans, letting farmers match payments to harvest proceeds. These financial innovations sustain demand for mid- and high-horsepower units even during currency instability.

Paraguay and Uruguay focus on soybean and livestock systems, respectively. Paraguay’s goal to double soybean exports by 2030 spurs mechanization in the eastern region, while Uruguay’s beef and dairy sectors invest in haying and forage machinery that supports intensive pasture systems. Chile’s topography favors compact tractors capable of working vineyards and orchards, whereas Colombia’s coffee belt requires machines under 50 horsepower to navigate steep slopes. Collectively, these markets present fragmented land holdings but high upside for specialized equipment and precision retrofits.

Regulatory Landscape

Brazil has tightened equipment traceability and road-safety compliance for agricultural tractors through mandatory registration on RENAGRO/ID Agro, anchored by Decree 11.014/2022 and CONTRAN Resolution 1017/2024, which together formalize national records used in financing, insurance, and circulation controls. Environmental and conformity requirements also shape product offerings and import content, with IBAMA licensing (LCVM) linked to engine and vehicle configuration compliance under CONAMA rules. In parallel, INMETRO and ABNT provide the standards and certification ecosystem that frequently aligns with ISO/IEC references.

Across the region, rules for used machinery are diverging between trade facilitation and biosecurity tightening. Argentina moved to remove legacy barriers for used capital goods by eliminating the Used Goods Import Certificate (CIBU) and certain licensing steps via Decree 273/2025, supporting the availability of lower-cost tractors and implements during periods of constrained purchasing power. Paraguay, by contrast, adopted Law 7565/2025 to regulate imports of used agricultural machinery, with SENAVE-led sanitary certification and cleaning verification, including a maximum age limit of five years. This raises compliance costs for used inflows while reducing pest and invasive-species risks.

Competitive Landscape

The top five vendors, John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, and Mahindra and Mahindra Ltd., command a modest percentage of 2024 revenue in the South America agricultural tractor machinery market. Competitive intensity is climbing as regional specialists carve out share in attachments, retrofits, and low-horsepower niches. John Deere’s subscription-based Solution-as-a-Service aims for 10% of corporate sales by 2030, bundling hardware, agronomic analytics, and in-field support. CNH Industrial’s BemAgro partnership layers drone imagery onto Case IH and New Holland guidance platforms, enabling in-cab variable-rate control without aftermarket apps. AGCO Corporation exploits Fuse diagnostics to lower downtime and lock parts and service revenue streams.

Local manufacturers leverage agility and proximity. Stara’s Sol Quarantatre planter attaches modular precision units to existing frames, shortening delivery times and cutting acquisition costs for farms that already own toolbar infrastructure. Grupo Jacto’s Arbus 4000 JAV sprayer integrates with Trimble and Raven sensors, positioning the firm as a retrofit-friendly alternative to premium imports. Agrale serves the under-100-horsepower tractor bracket, appealing to family farms that prioritize service accessibility and parts availability. Technology differentiation extends beyond iron, with Solinftec’s SOLIX autonomous robot demonstrating viable robotics at scale and Kilimo’s irrigation software saving water and input costs across nine million hectares.

Emission regulation timelines add a strategic layer. Manufacturers with advanced Tier III portfolios bet on early movers seeking fuel savings and environmental compliance, while assemblers lobbying for delays aim to clear legacy inventory. Currency volatility and gray-market influx force continuous adaptation of pricing, inventory, and financing schemes, strengthening the value of flexible captive finance programs that absorb residual-value swings and cushion farmers against currency shocks.

South America Agricultural Tractor Machinery Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

Mahindra & Mahindra Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large, program-backed credit lines and targeted industrial financing in Brazil are creating near-term room for OEMs and implement makers to bundle machines with digital services and localized aftersales. MOVE Brasil credit actions in 2026 (including a line publicized at R$ 10 billion and the start of operations for a R$ 14 billion line) and the 2026/2027 Crop Plan investment allocation for machinery renewal and innovation expand addressable financed demand for tractors, implements, and connected retrofits, particularly when combined with captive finance offerings. On the supply side, BNDES approval of R$ 129 million for CNH Industrial Brazil across eight R&D and innovation projects (including tractors and accessibility-focused designs) points to active development funding for higher-tech platforms that fit better with labor-scarce, time-compressed planting and spraying windows.

Compact and specialty segments also offer a clearer build-out lane, supported by new local manufacturing commitments and compliance-driven product differentiation. Yanmar’s announced R$ 280 million investment for a new Indaiatuba (SP) factory to consolidate production and target 7,000 compact tractors per year by 2030 highlights capacity being positioned around smaller-horsepower demand tied to fragmented landholdings, orchards/vineyards, and diversified livestock systems. At the same time, stricter traceability and used-import sanitary controls (for example, Brazil registration requirements and Paraguay Law 7565/2025) raise the value of OEM-certified used programs, dealer-inspected trade-ins, and retrofit kits that upgrade older fleets while staying within evolving administrative and phytosanitary rules.

Recent Industry Developments

- April 2026: CNH Industrial (Case IH and New Holland) announced an investment of more than USD 20 million to localize production of MacDon Draper FD2 cutter platforms at its Curitiba (PR) facility in Brazil. The move shortens lead times and reduces exposure to currency-driven import cost swings for a critical harvesting attachment that is sold alongside high-horsepower tractor and harvesting fleets.

- January 2026: John Deere inaugurated a new sprayer factory in Canoas (RS), Brazil, to produce the 1025E sprayer, replacing the PLA brand line. Adding dedicated capacity in-country reinforces Deere’s position in self-propelled application equipment, a fast-adopting category tied to labor scarcity and tighter agronomic windows.

- April 2024: John Deere announced an investment of about R$ 700 million in its Catalao (GO) factory to expand infrastructure and nationalize See & Spray technology. The program strengthens local manufacturing and supports broader adoption of precision spraying capabilities through a Brazil-based supply chain.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks the value of agricultural tractor machinery sold and used across South America, where tractors are counted along with the key tractor types and horsepower classes used for common farm field operations.

Scope exclusions: Construction or industrial tractors, road tractors for hauling semi-trailers, and non-agricultural tractor categories are excluded from this sizing.

Segmentation Overview

- By Machinery Type

- Plowing and Cultivating Machinery

- Plows

- Harrows

- Rotovators and Cultivators

- Other Plowing and Cultivating Machinery

- Planting Machinery

- Seed Drills

- Planters

- Spreaders

- Other Planting Machinery

- Haying and Forage Machinery

- Mowers and Conditioners

- Balers

- Other Haying and Forage Machinery

- Sprayers

- Other Types

- Plowing and Cultivating Machinery

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the addressable tractor machinery pool by country, then tying it to farm activity indicators that describe how often tractors are used. We rely on public sources such as FAOSTAT for crop and farm equipment context, national statistics agencies for agriculture and production indicators, UN Comtrade for import and export patterns, and central bank or finance ministry releases for inflation and FX context.

To keep assumptions grounded, we also read manufacturer annual reports and investor decks, customs and port updates, industry association publications, and trusted press coverage on planting seasons and machinery financing. A paid company financials and intelligence subscription is used selectively to normalize revenue splits and to avoid double counting when companies report across regions. These desk sources are not exhaustive, and many other public references are consulted to collect data, validate it, and clarify unclear points.

Primary Interviews and Surveys

Primary work focuses on conversations with distributors, dealers, farm contractors, large farms, and service networks, since pricing and mix can move faster than public data. We also speak with regional experts across the main South American demand pockets to confirm how the horsepower mix, financing availability, and replacement cycles are changing, and then we adjust inputs that looked inconsistent in desk findings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 46% |

| Mid tier: 50% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 21% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where we reconstruct the demand pool using country-level farm activity indicators and tractor adoption signals, then translate it into value through observed price bands. In parallel, we run selective bottom-up checks using sampled dealer sell-through, typical annual unit flows by horsepower class, and average selling price ranges, which are then used to correct totals when either method drifts.

Key inputs include planted area and crop mix shifts, since tractor utilization differs by crop, replacement cycle patterns, and horsepower mix movement across below-80 HP, 81-130 HP, and above-130 HP categories. We also account for import intensity versus local assembly signals, and annual price changes tied to FX and inflation. Forecasts are built using scenario analysis, since credit availability, season timing, and policy changes can swing purchases. Scenario weights are stress-tested with expert views, and where bottom-up gaps appear for smaller countries or informal channels, we bridge using trade signals and dealer network density before totals are finalized.

Data Validation & Update Cycle

Outputs are triangulated by checking whether implied unit volumes and pricing trends align with external signals such as trade movement, financing conditions, and observed shifts in tractor class demand. When a country shows an unusual jump, we trace the driver back to a specific assumption, and we re-contact sources if the explanation remains weak.

A second analyst reviews the model logic, the key assumptions, and the math before sign-off. We then align the narrative to what the numbers show. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery scan is done so clients receive the most current view.

Mordor Intelligence's South America Agricultural Tractor Machinery Market Estimate Compared With Other Published Estimates

Published market sizes rarely match perfectly because each publisher draws the line differently on what counts as tractor machinery, what geography is included, and how they treat price inflation and currency conversion. Timing also matters, since agricultural machinery demand can shift quickly with credit conditions and planting seasons.

The main gap comes from whether the estimate stays within South America agricultural tractor machinery and farm-use tractor categories only, or whether it expands into broader Latin America coverage or adds adjacent tractor definitions, and then applies a different price basis. Some numbers also lean on a single base year and straight-line growth, while others adjust horsepower mix and replacement cycles, which can change the value even when unit trends look similar. The scope and pricing logic used by Mordor Intelligence counts South America agricultural tractor machinery in 2025 at USD 4.20 B by keeping the geography tight and by treating horsepower mix and FX timing as explicit inputs instead of rolling them into one blended growth rate.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.20 B (2025) | |

| Regional Consultancy A | USD 4.50 B (2023) | Uses an earlier base year and frames the market mainly as agricultural tractors, which can shift totals when attachments and tractor machinery activities are treated differently, and when 2024-2025 FX and price swings are not re-based. |

| Trade Journal B | USD 9.20 B (2024) | Covers a wider region (Latin America and the Caribbean) and includes agricultural and forestry tractor categories in nominal wholesale prices, which inflates the value versus a South America-only tractor machinery scope. |

The spread across the three values is mainly explained by geography expansion and by what is counted as tractor machinery versus tractors in a broader regional category. By keeping the inputs traceable to farm demand signals, class mix, and country-level pricing adjustments, the resulting number stays easier to reproduce and to update when conditions change.

Key Questions Answered in the Report

How large is the South America agricultural tractor machinery market in 2026?

The market is valued at USD 4.55 billion in 2026 and is projected to reach USD 6.79 billion by 2031.

Which machinery segment holds the largest revenue share?

Plowing and cultivating equipment leads with a 33.35% revenue share in 2025.

What is the fastest-growing machinery category through 2031?

Sprayers are anticipated to register a 10.11% CAGR over the forecast period (2026-2031).

Why is Brazil the dominant geography?

Brazil combines expansive farm sizes, substantial rural-credit programs, and rapid precision-agriculture adoption, supplying about 56.60% of regional sales.

Page last updated on: