Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

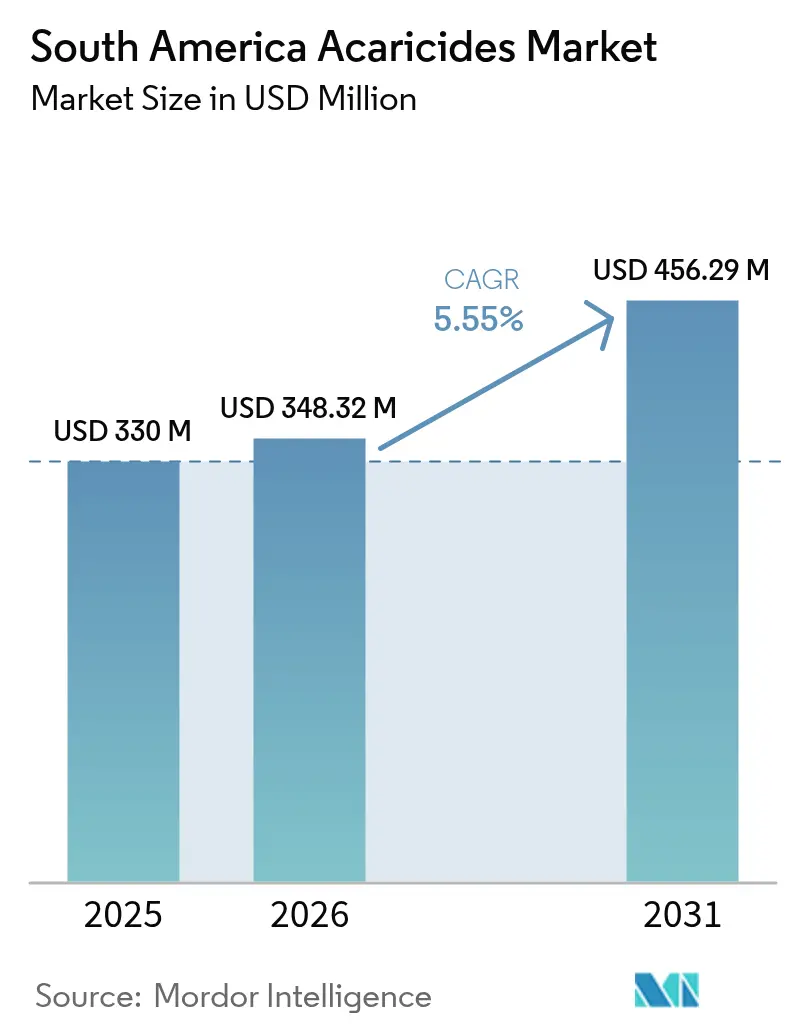

| Base Year Market Size (2025) | USD 330 Million |

| Market Size (2026) | USD 348.32 Million |

| Market Size (2031) | USD 456.29 Million |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Acaricides Market Analysis by Mordor Intelligence

The South America acaricides market size was valued at USD 330 million in 2025 and estimated to grow from USD 348.32 million in 2026 to reach USD 456.29 million by 2031, at a CAGR of 5.55% during the forecast period (2026-2031). Sustained mite pressure in soybeans, citrus, coffee, and greenhouse vegetables, rising adoption of precision sprayers, and export‐oriented residue standards anchor this expansion. Growers are rotating chemical groups to manage resistance, while government credit lines lower the real cost of premium systemic miticides. Multinational suppliers are consolidating formulation assets to secure local supply and barter financing, and digital sales channels are reshaping price discovery by shortening the route to farms. The South America acaricides market continues to benefit from climate‐linked pest migration that extends the spray calendar, prompting producers in temperate zones to budget more applications per season.

Key Report Takeaways

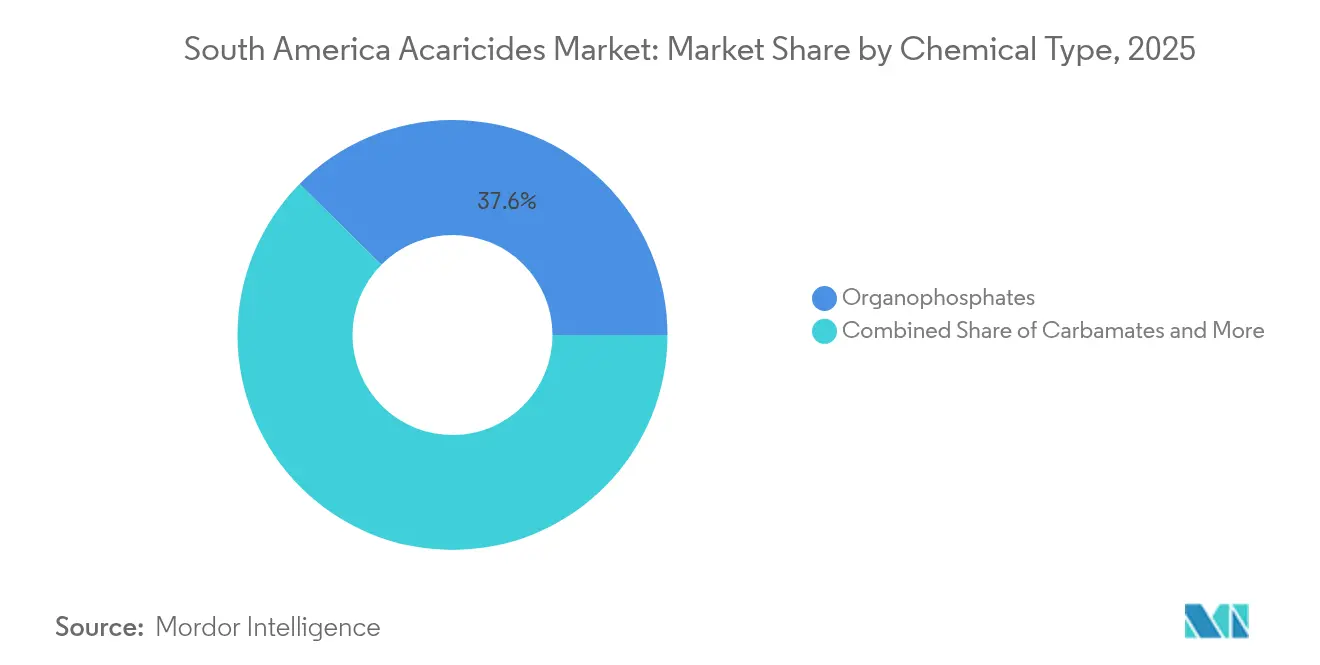

- By chemical type, organophosphates led with 37.60% of the South America acaricides market share in 2025, while pyrethroids are forecast to expand at a 7.35% CAGR through 2031.

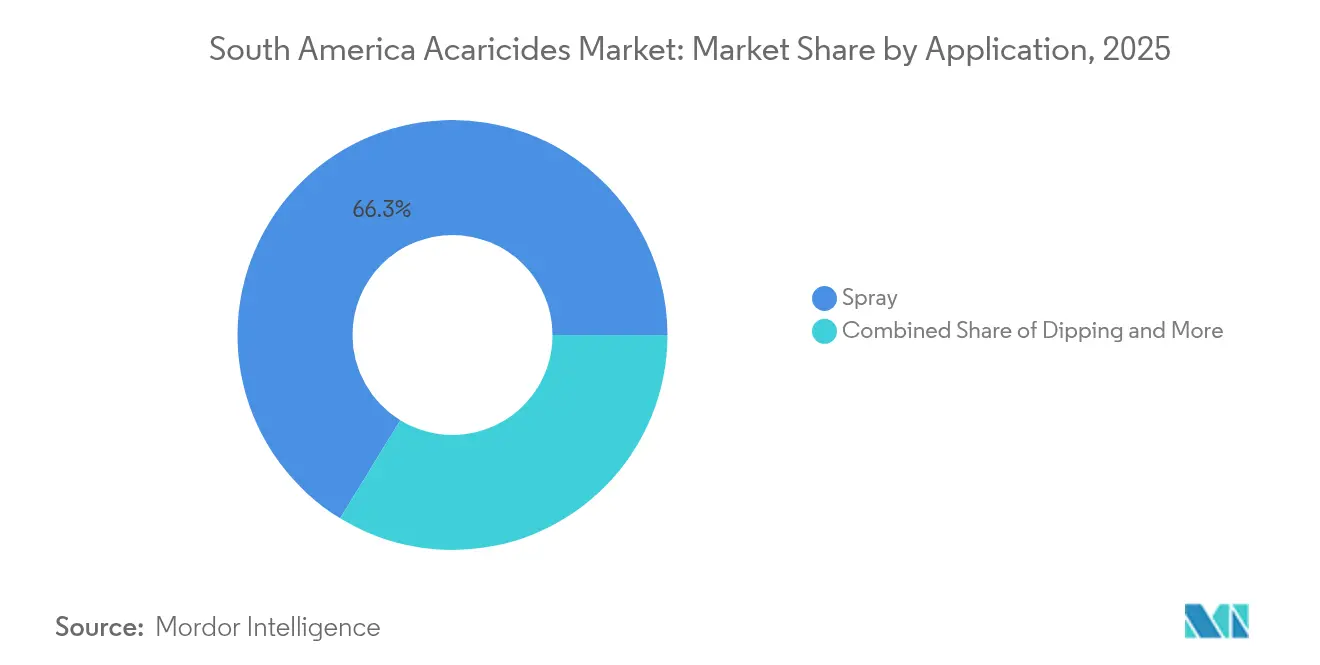

- By application, spray methods accounted for 66.25% of the South America acaricides market share in 2025, while dipping is projected to grow at a 6.28% CAGR to 2031.

- By geography, Brazil contributed 50.65% of the South America acaricides market share in 2025, whereas Argentina is on track for a 6.62% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Acaricides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-sprayer adoption cuts input costs | +1.2% | Brazil and Argentina | Medium term (2-4 years) |

| Climate-linked mite migration into temperate zones | +1.0% | Argentina, Southern Brazil, and Uruguay | Long term (≥ 4 years) |

| Government soybean revitalization programs | +0.9% | Brazil, Argentina, Paraguay | Short term (≤ 2 years) |

| Push for export-compliant Maximum Residue Limits (MRLs) | +0.8% | Brazil and Argentina export corridors | Medium term (2-4 years) |

| Adoption of long-residual systemic miticides | +0.7% | Brazil, Argentina, and Colombia | Medium term (2-4 years) |

| E-commerce agro-retail penetration | +0.6% | Brazil and Argentina | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Precision-Sprayer Adoption Cuts Input Costs

Field trials by the Brazilian Agricultural Research Corporation (Embrapa) showed that global positioning system guided boom sprayers and variable-rate controllers reduced miticide use per hectare by 15% to 25% in Mato Grosso during the 2023–2024 season [1]Source: Embrapa, “Precision Agriculture Adoption in Brazilian Soybean Systems,” embrapa.br. Large farms recover capital outlays within three cycles through lower chemical spend and reduced fuel. Penetration among Brazilian properties above 500 hectares reached 38% in 2024, up from 22% in 2020, with cotton and soybean belts posting the fastest growth. Argentine uptake remains close to 18% because of higher equipment prices and limited subsidized machinery credit. Precision delivery favors high-potency actives such as abamectin and spiromesifen because optimal rates can be calibrated precisely. Dealers that bundle sprayer audits with product sales strengthen grower loyalty and differentiate on service rather than price.

Climate-Linked Mite Migration into Temperate Zones

Average winter lows in Argentina’s Pampas and southern Brazil rose by 1.2 °C between 2019 and 2023, allowing two-spotted spider mites and citrus rust mites to survive year-round. Research published in the Journal of Applied Entomology traced a 200-kilometer southward shift of Tetranychus urticae during that period, extending the spray window by four to six weeks. Chilean table grape and avocado farms now schedule preventive treatments before bud break, a practice unnecessary before 2020. Natural predator populations lag behind migrating pest fronts, so chemical control fills the gap. Climate pressure also raises application frequency, expanding demand for low-residue formulas acceptable to export markets. Suppliers offering predictive pest maps earn a service premium because timely intervention minimizes flare-ups.

Government Soybean Revitalization Programs

Brazil’s Plano Safra 2024–2025 earmarked BRL 400.6 billion (USD 80 billion) in rural credit, including BRL 108 billion (USD 21.5 billion) for medium-sized farms [2]Source: Brazilian Ministry of Agriculture, “Plano Safra 2024–2025: Rural Credit Allocation,” gov.br. Argentina’s USD 500 million Fondo de Desarrollo Oleaginoso provides zero-interest loans for inputs. These subsidies compress the effective cost of acaricides by 20% to 30% and encourage growers to rotate multiple modes of action rather than depend on a single chemistry. Paraguay added USD 150 million to support soybean and corn producers in early 2025, widening the addressable acreage. Credit programs spur acreage expansion and larger spray budgets, reinforcing volume growth for systemic miticides that extend protection between sprays.

Push for Export-Compliant Maximum Residue Limits (MRLs)

The European Union’s 2024 revision of Regulation 396/2005 lowered the soybean and citrus MRL for chlorpyrifos from 0.05 mg/kg to 0.01 mg/kg, effectively excluding the active from export supply chains [3]Source: European Commission, “Regulation 396/2005: Maximum Residue Limits Update,” ec.europa.eu. Brazil sent USD 52 billion of soy and soy products abroad in 2024, with 60% going to China and the European Union. As buyers demand lower residues, growers shift to cyflumetofen or acequinocyl, which clear tissues within two weeks. Syngenta introduced an application timing app in 2024 that alerts citrus producers when to spray to stay below tolerance limits. Compliance pressures, therefore, accelerate premium active sales and favor companies with residue-monitoring support tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter chemical re-registration in Brazil | -0.9% | Brazil and neighbors using Brazilian registrations | Medium term (2-4 years) |

| High upfront cost of patented actives | -0.7% | Argentina and smaller markets | Short term (≤ 2 years) |

| Registration backlog delaying access to new chemistries | -0.6% | Brazil, Argentina, and Colombia | Medium term (2-4 years) |

| Emerging mite resistance to pyrethroids | -0.5% | Brazil and Argentina hotspots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Chemical Re-Registration in Brazil

Law 14 785 of 2023 and Resolution 950 of December 2024 require companies to provide updated toxicology, ecotoxicology, and residue data for all active ingredients registered before 2010. The high compliance costs are likely to force smaller formulators out of the market and could lead to the removal of chlorpyrifos and methamidophos by 2027. Paraguay and Uruguay rely on Brazilian dossiers for technical equivalence, meaning any withdrawal in Brazil could disrupt their supply chains. Growers may need to transition to higher-cost substitutes or face potential yield losses during the adjustment period.

High Upfront Cost of Patented Actives

Corteva estimates that developing a new molecule and bringing it to market requires significant investment over a period of several years. Spiromesifen and cyflumetofen are protected by patents until the late 2020s and are priced substantially higher than generic alternatives. In recent years, Argentina's high inflation significantly reduced growers' purchasing power, creating a divide between export-focused farms, which opt for low-residue formulations, and domestic suppliers relying on off-patent organophosphates. Syngenta's barter program allows producers to pay for chemical products with harvested grain, improving affordability but only for those participating in the program.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Type: Organophosphates Anchor Legacy Demand, Pyrethroids Lead Innovation

Organophosphates captured 37.60% of the South America acaricides market share in 2025 share in 2025, making them the bedrock of many soybean and citrus programs. The organophosphates reached their trajectory is limited by stricter re-registration requirements that could delist chlorpyrifos by 2027. Pyrethroids posted the fastest forecast growth at 7.35% CAGR from 2026 to 2031 because growers combine them with systemic actives to delay resistance. Bifenthrin and lambda-cyhalothrin stand out for delivering comparable control at 15% to 20% lower rates per hectare than legacy options, which appeals to farms investing in variable-rate sprayers.

Nano-encapsulation research from Syngenta Group and Bayer AG indicates that controlled-release pyrethroids can extend residual effectiveness by up to 60% without exceeding residue limits, with commercial launches projected in 2026. Carbamates remain niche products in livestock dipping, where propoxur and carbaryl provide rapid knockdown. Botanical pyrethrins satisfy organic producers but require frequent reapplication because their residual activity seldom exceeds five days. Dimpropyridaz, the active in BASF’s Efficon, launched in January 2025, exemplifies dual-mode products that bridge insect and mite control, streamlining spray calendars.

By Application: Spray Dominates, Dipping Gains in Livestock Segments

Spray techniques accounted for 66.25% of the South America acaricides market share in 2025. Boom, aerial, and backpack sprayers offer flexibility across crop systems, and precision upgrades reduce waste by matching dose to observed mite pressure. Drone-based ultra-low-volume sprayers are under pilot studies in Argentina, cutting water use by 70% and opening new service opportunities for contractors.

Dipping is forecast to post a 6.28% CAGR through 2031. Uruguay and southern Brazil are investing in concrete plunge tanks and mobile pour-on chutes to meet beef export protocols that stipulate zero visible ectoparasite presence at slaughter. Seed treatments and soil drenches constitute a small but growing category, systemic miticides applied pre-plant reduce foliar sprays and attract growers dealing with labor shortages. Registration fast-tracking under Argentina’s Resolution 694 should shorten the path to market for such novel delivery routes.

Geography Analysis

Brazil contributed 50.65% of the South America acaricides market share in 2025 size in 2025 on the back of 45 million hectares of soybeans, 5.5 million hectares of citrus, and 2.2 million hectares of coffee. The government’s credit program raised rural financing to BRL 400.6 billion (USD 80 billion) for the 2024–2025 cycle, lowering the effective cost of multi-mode chemistry rotations. Meanwhile, the re-registration mandate threatens older organophosphates, pushing distributors to stock more pyrethroids and insect growth regulators. E-commerce now captures a noticeable share of chemical sales, rewarding suppliers with efficient order fulfillment systems and penalizing slow-moving regional wholesalers.

Argentina is the fastest-growing geography, forecast at 6.62% CAGR from 2026 to 2031. Climate change has brought mite infestations deeper into the Pampas, extending the spray season by over a month. Resolution 694 slashes pesticide approval times to under 12 months by recognizing technical dossiers from seven reference countries, expediting entry for patented miticides. The USD 500 million support fund cushions growers transitioning toward low-residue chemistries. However, triple-digit inflation forces many domestic-market farms to continue using older, lower-priced actives, which may hinder residue compliance for potential export expansion.

The Paraguay, Uruguay, Chile, Colombia, and smaller markets made up roughly 20.25% of revenue in 2025. Paraguay’s USD 150 million aid package for eastern soybean departments boosts spray budgets. Chile’s USD 1.2 billion table grape export trade imposes zero-tolerance residue rules, prompting rapid replacement of chlorpyrifos with cyflumetofen. Uruguay’s beef industry exports 80% of production, necessitating stringent dipping protocols for cattle ticks. Colombia faces a 400-application registration backlog that prioritizes biologicals, delaying arrival of new synthetic actives for coffee and cut flowers. Each sub-region presents distinct regulatory or crop profiles, yet all are converging on lower residue thresholds that favor modern chemistries.

Competitive Landscape

The South America acaricides market is moderately concentrated. The top five suppliers, Bayer AG, UPL Limited, Syngenta Group, BASF SE, and Corteva Agriscience, held about a major share in 2024. Multinationals differentiate through patented molecules, digital agronomy tools, and local formulation plants. Syngenta’s July 2024 purchase of Produtécnica added eight Brazilian production sites and direct ties to 12,000 retail outlets, deepening its barter financing capabilities.

BASF’s Efficon introduces a sodium-channel blocker that spans insect and mite targets, showcasing portfolio convergence. Local formulators such as Nortox and Alta Defensivos compete on price, flexible credit, and proximity to growers. Adama Agricultural Solutions, a global generics specialist, leverages scale to supply off-patent organophosphates and pyrethroids at competitive rates. Biological specialists Koppert BV and FMC Corporation’s alliance with Ballagro targets integrated pest management users through predatory mite releases and microbial agents, although synthetic products still dominate volume.

Technology adoption is altering the playing field, suppliers offering sprayer calibration services, variable-rate prescription maps, or residue tracking apps position themselves as partners rather than commodity sellers. Patent filings for nano-encapsulation delivery at Brazil’s National Institute of Industrial Property surged in 2024, indicating a forthcoming wave of controlled-release launches.

South America Acaricides Industry Leaders

Bayer AG

BASF SE

UPL Limited

Syngenta Group

Corteva Agriscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Cropchem has introduced Brazil’s first dual-action acaricide-insecticide, designed to control both mites and insects in crops. The product combines two active mechanisms, offering broader pest management and longer residual protection. This launch strengthens Brazil’s crop protection portfolio, reflecting innovation in South America’s agricultural market.

- November 2024: Alta Defensivos has launched Vilora, a new acaricide in Brazil, aimed at controlling mites in crops such as coffee, citrus, and coconut. The product is highlighted for its long residual effect and effectiveness against resistant mite populations. This launch strengthens pest management options in South America’s agricultural sector, particularly for high-value perennial crops.

South America Acaricides Market Report Scope

Acaricides are crop protection chemicals used to control mites and ticks. The South American Acaricides Market is segmented by Type into Organophosphates, Carbamates, Organochlorines, Pyrethrins, Pyrethroids, and Other Chemical Types, by Application into Spray, Dipping, Hand Dressing, and Others Applications and Geography into Brazil, Argentina, and Rest of South America. The report offers market estimates and forecasts in value (USD) for all the above segments.

By Chemical Type

| Organophosphates |

| Carbamates |

| Organochlorines |

| Pyrethrins |

| Pyrethroids |

| Other Chemical Types |

By Application

| Spray |

| Dipping |

| Hand Dressing |

| Other Applications |

By Geography

| Brazil |

| Argentina |

| Rest of South America |

| By Chemical Type | Organophosphates |

| Carbamates | |

| Organochlorines | |

| Pyrethrins | |

| Pyrethroids | |

| Other Chemical Types | |

| By Application | Spray |

| Dipping | |

| Hand Dressing | |

| Other Applications | |

| By Geography | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America acaricides market in 2026?

The South America acaricides market size stands at USD 348.32 million in 2026.

What is the projected CAGR for acaricides in South America through 2031?

The market is forecast to grow at a 5.55% CAGR from 2026 to 2031.

Which chemical group is growing fastest in the region?

Pyrethroids show the highest forecast growth at 7.35% CAGR by layering with systemic actives to manage resistance.

Why is Argentina the fastest-growing geography?

Climate-induced mite migration, expedited product approvals under Resolution 694, and government credit for oilseed producers drive a 6.62% CAGR.

Page last updated on: