Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

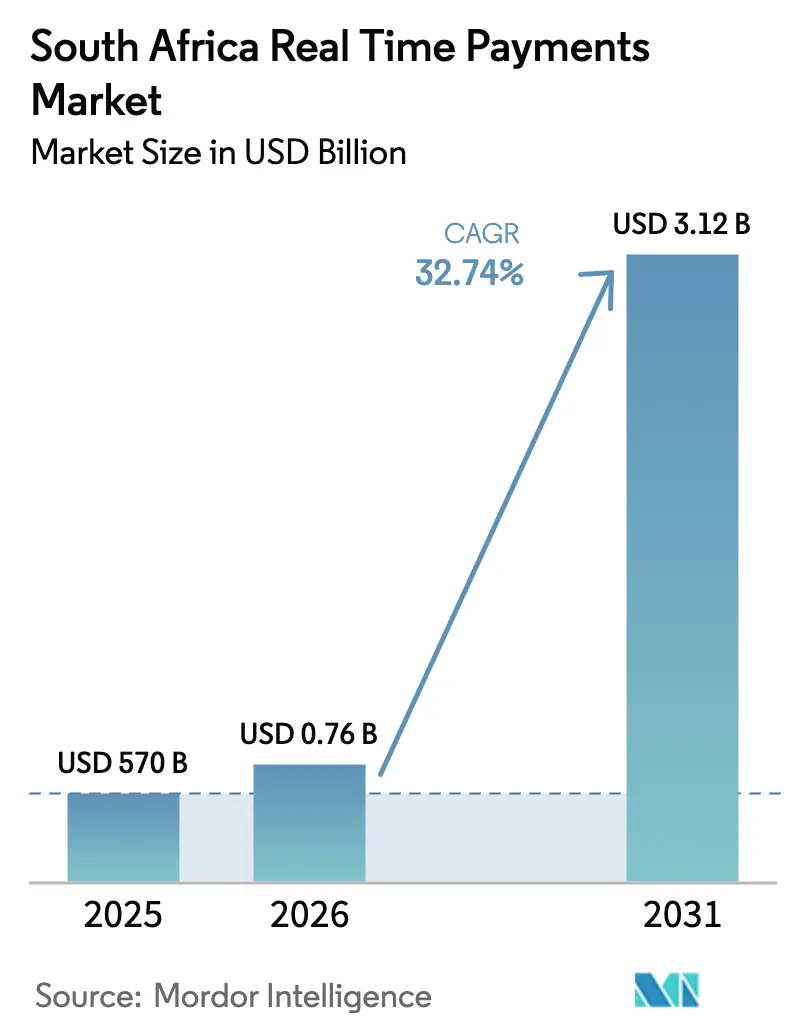

| Base Year Market Size (2025) | USD 570 Billion |

| Market Size (2026) | USD 0.76 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 32.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Real Time Payments Market Analysis by Mordor Intelligence

The South Africa real time payments market size is expected to grow from USD 570 million in 2025 to USD 756.6 million in 2026 and is forecast to reach USD 3.12 billion by 2031 at 32.74% CAGR over 2026-2031. Rapid scale-up is supported by the South African Reserve Bank’s PayShap rail, a sharp drop in mobile-data prices, and a national pivot toward digital commerce. Heavy fintech funding, topping USD 100 million during 2024-2025, accelerates product innovation while cloud migration reshapes bank cost structures.[1]National Treasury, “Budget Review 2024,” treasury.gov.za Competitive intensity remains moderate as incumbents Standard Bank, FNB, Nedbank, and Absa jostle with rising fintechs such as Stitch and Ozow. Still, structural frictions—transaction fees of R6-10 per instant payment, legacy cores at tier-2 lenders, and a 15% rise in authorised push-payment fraud—temper the near-term growth trajectory.

Key Report Takeaways

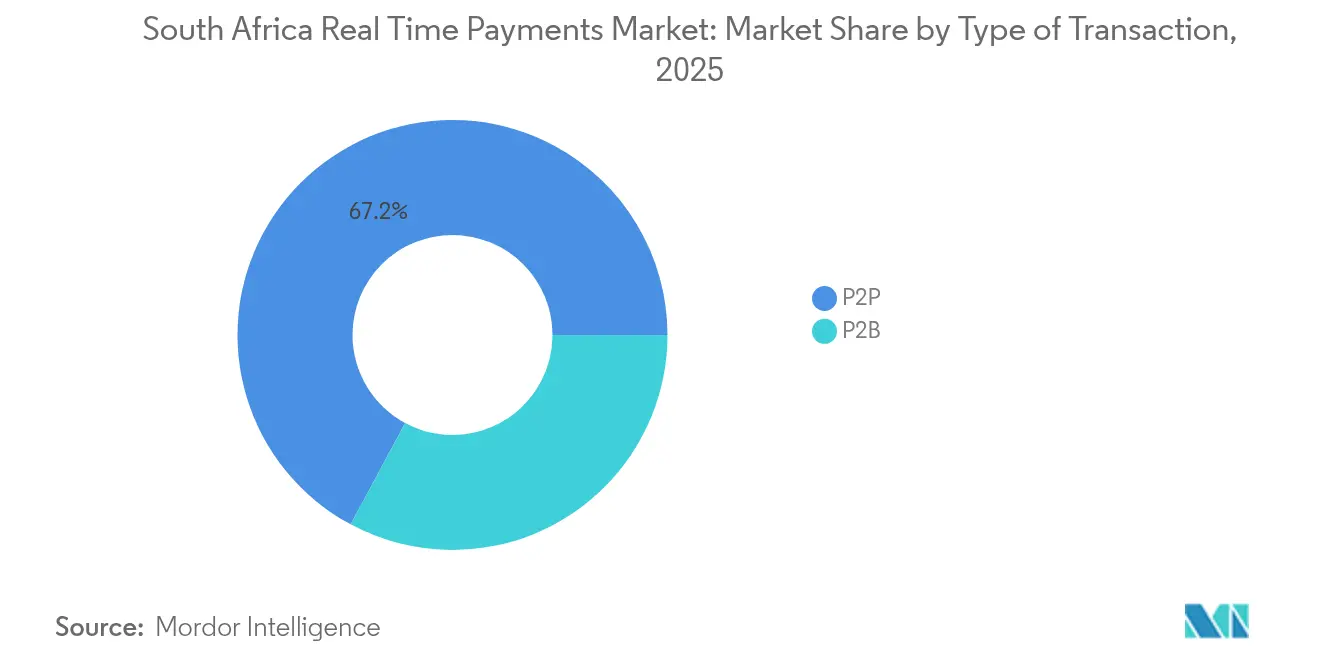

- By type of payment, person-to-person transfers captured 67.15% of South Africa real time payments market share in 2025, while person-to-business flows are projected to compound at 34.38% CAGR through 2031.

- By component, solutions accounted for 79.20% share of the South Africa real time payments market size in 2025; services are set to advance at a 35.70% CAGR to 2031.

- By deployment, on-premises systems held 64.20% share of the South Africa real time payments market size in 2025, whereas cloud models are forecast to grow at 36.10% CAGR.

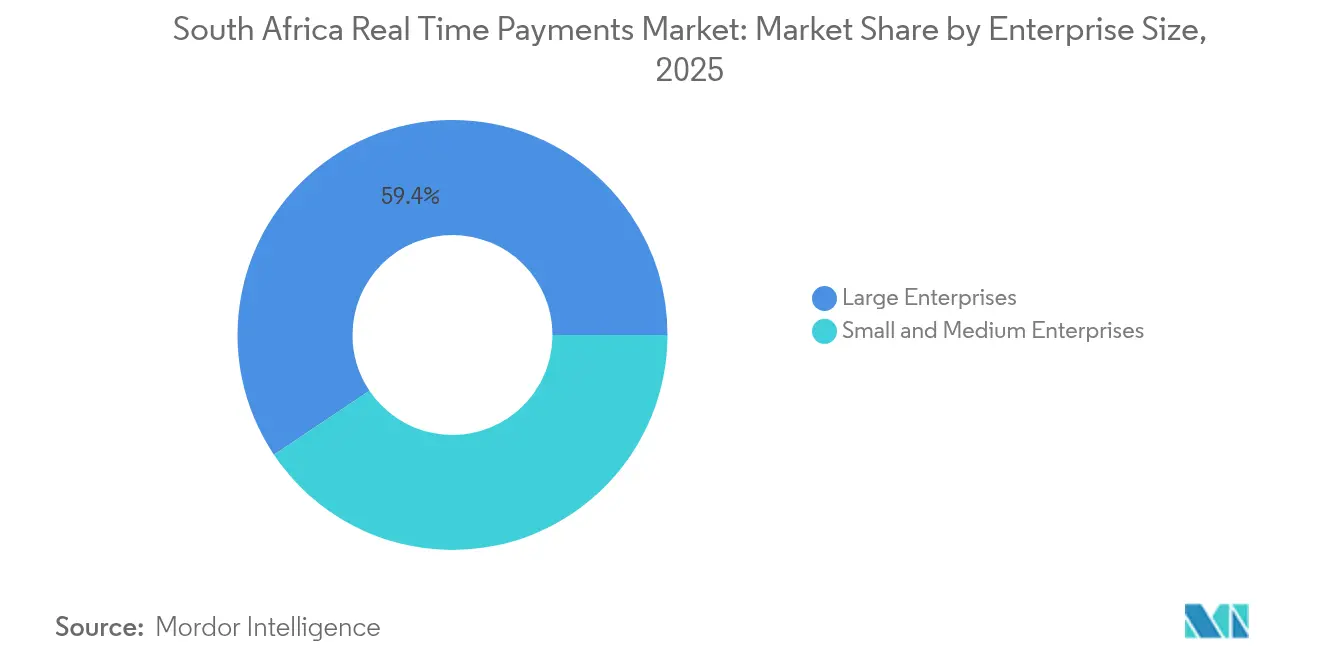

- By enterprise size, large enterprises commanded 59.40% share of the South Africa real time payments market size in 2025, but the SME segment is expanding at 33.10% CAGR.

- By end-user industry, retail and e-commerce led with a 39.30% share of the South Africa real time payments market size in 2025; government and utilities represent the fastest path, rising at 35.60% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SARB PayShap Launch Accelerating Instant Low-Value Transfers | +8.2% | National, with early gains in Western Cape, Gauteng | Short term (≤ 2 years) |

| Fintech VC Surge Enabling Innovative RTP Front-Ends | +6.1% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Declining Mobile-Data Costs Expanding Smartphone-Based RTP | +4.8% | National, with higher impact in rural provinces | Long term (≥ 4 years) |

| Township e-Commerce Sellers Demanding Immediate Settlement | +3.9% | Gauteng, Western Cape, KwaZulu-Natal townships | Medium term (2-4 years) |

| On-Demand Payroll and Gig-Economy Disbursements | +3.2% | Major metropolitan areas | Short term (≤ 2 years) |

| Open-Banking Mandates Under COFI Bill Fueling API-Driven RTP | +2.8% | National, phased implementation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SARB PayShap Launch Accelerating Instant Low-Value Transfers

PayShap processed 74.2 million transactions worth R46 billion by October 2024, proving that a simplified alias-based design can motivate mainstream adoption.[2]Standard Bank, “PayShap Adoption Update,” standardbank.co.za Average ticket sizes have slid to R498 (USD 28.04), signalling deep penetration into micro-payments once dominated by cash. Transfers below R100 (USD 5.63) remain free, encouraging price-sensitive users to accept the service for daily purchases.[3]Nedbank, “Digital Fees Disclosure 2024,” nedbank.co.za With Capitec and Discovery Bank now live, national coverage is broadening. Rising competitive pressure has pushed major banks to trim instant-payment fees, narrowing the cost gap with batch EFT alternatives. PayShap’s small-business rollout, slated for late-2024, could redirect R2.1 trillion (USD 0.12 trillion) in MSME turnover onto real-time rails.

Fintech VC Surge Enabling Innovative RTP Front-Ends

South African fintechs clinched record capital in 2024-2025, highlighted by Stitch’s USD 55 million Series B round that unlocked omnichannel payment APIs for retailers such as Takealot and MTN. Smaller startups like Happy Pay raised USD 1.8 million to broaden BNPL options for 150,000 users, evidence of deepening investor confidence. Consolidation is under way: Stitch acquired ExiPay to merge in-person and online acceptance, while Ozow joined forces with EBANX for cross-border reach. Available funding accelerates front-end experimentation—chat-based checkout, QR acceptance, and earned-wage APIs—that plug directly into the South Africa real time payments market backbone.

Declining Mobile-Data Costs Expanding Smartphone-Based RTP

Average data prices fell from USD 12.44 in 2010 to USD 1.77 per GB in 2025, spurring internet reach to 646 million Africans and setting a path to 1.1 billion by 2029. More than 50 million South Africans hold smartphones, enabling secure P2P apps such as Bank Zero which rests on IBM LinuxONE hardware for sub-millisecond latency. Cheaper connectivity also boosts crypto-linked QR payments: Pick n Pay now clears R1 million (USD 0.056 million) in Bitcoin transactions each month across 700 stores. Rural uptake is improving because mobile coverage often precedes bank branches, aligning perfectly with alias-based PayShap IDs. Sustained cost declines underpin long-run expansion of the South Africa real time payments market into peri-urban areas.

Township e-Commerce Sellers Demanding Immediate Settlement

Informal MSMEs generate R5 trillion in annual turnover yet stay largely cash-reliant, delaying scale-up and credit access. The FinScope MSME 2024 survey shows 72% of micro-enterprises operate off the formal grid, making instant, low-fee transfers vital for daily liquidity. Budget 2024 earmarked funds to digitise township payments through Swiss-backed pilots, supporting OECD-aligned financial-inclusion targets. Real-time settlement gives sellers proof-of-payment and inventory cash the same day. That facility also interfaces neatly with courier networks serving “spaza-to-door” commerce models, sharpening township competitiveness with formal supermarkets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Interchange and Scheme Fees for RTP Rails | -4.3% | National, higher impact on price-sensitive segments | Short term (≤ 2 years) |

| Legacy Core Systems of Tier-2 Banks Slowing Integration | -3.1% | Regional banks, community financial institutions | Medium term (2-4 years) |

| Rising Cyber-Enabled Authorised Push-Payment Fraud | -2.8% | National, concentrated in urban digital payment hubs | Short term (≤ 2 years) |

| Low Financial Literacy in Rural Provinces | -2.2% | Rural provinces: Limpopo, Eastern Cape, Northern Cape | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Interchange and Scheme Fees for RTP Rails

Major banks charge R6-10 (USD 0.34 to USD 0.56) per Pay-by-Bank transaction versus R1-3 (USD 0.056 to USD 0.17) for standard EFTs, creating sticker shock for mass users. Capitec has broken rank with a R6 (USD 0.34) flat fee, showing how aggressive pricing can capture volume. The disparity drives consumers to split their payment flows: real time for urgent transfers, EFT for routine bills. New CMA rules forcing cross-border remittances onto SWIFT rails raise costs further, dampening adoption in border towns. Unless fees fall quickly, price elasticity could shave several points off the South Africa real time payments market trajectory.

Legacy Core Systems of Tier-2 Banks Slowing Integration

Upgrading a regional bank’s core to ISO 20022-native rails can exceed R50 million (USD 2.82) and require multiyear programmes, a burden many tier-2 lenders cannot carry. Absa’s own overhaul, tied to stringent capital-markets rules such as FRTB, highlights the operational drag and compliance complexity. Standard Bank’s wide-ranging partnership with Volante shows the scale needed to embed real-time at continental level. Smaller banks risk falling behind, producing a dual-speed market where only big players deliver full RTP functionality, constraining inclusive growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Payment: P2B Growth Outpaces P2P Dominance

The P2P segment held 67.15% of total 2025 volume, anchored in family remittances and PayShap’s consumer-first roll-out. Person-to-business flows, however, are climbing faster at 34.38% CAGR, powered by township sellers, ride-hailing payouts, and invoice settlement. Uber alone channels thousands of micro-wage pushes daily, proving the viability of real-time disbursement for service marketplaces. PayShap’s forthcoming SME features will catalyse merchant uptake, shifting share toward business traffic. Informal retail chains and last-mile couriers already queue for beta access, suggesting a migration of working-capital cycles onto the South Africa real time payments market.

The South Africa real time payments market size for person-to-business flows is forecast to widen substantially as MSMEs formalise digital acceptance, cutting cash-handling losses and creating invoice data trails helpful for credit scoring. Meanwhile, the South Africa real time payments market share of P2P will gradually decline, yet volumes will keep growing in absolute terms as remittance activity shifts entirely to alias-based rails. Consumers value the instant confirmation and lower cost compared with cash deposits at branches. Payment providers are adding value-added services—split bills, request-to-pay, and cashback—to defend their P2P franchises.

By Component: Services Segment Accelerates Infrastructure Modernisation

Solutions, including core switches, mobile apps, and API platforms, owned 79.20% of revenue in 2025 due to capital-intensive buildouts. Yet services post a 35.70% CAGR as banks outsource integration, testing, and compliance. Standard Bank’s Volante contract exemplifies end-to-end managed services encompassing ISO 20022 conversion, fraud analytics, and 24/7 uptime monitoring. Financial institutions prefer OpEx-based models that shift cyber-risk and skills shortages to specialist vendors.

The South Africa real time payments market size for services is projected to close the gap with solutions by 2031, fostering annuity revenues for consultancies and cloud SIs. Integration complexity, especially for tier-2 banks with dated cores, ensures sustained demand. Vendors that bundle KYC orchestration, dispute management, and analytic dashboards create lock-in advantages. Conversely, pure-software providers feel margin pressure as open-source projects commoditise basic routing engines.

By Deployment: Cloud Migration Transforms Banking Infrastructure

On-premises deployments controlled 64.20% of 2025 spend, reflecting regulatory caution and sunk hardware assets. Cloud rails, however, compound at 36.10% CAGR as institutions chase elasticity, sub-second latency, and lower capex. Bank Zero’s all-cloud stack serves as a poster child, delivering under-one-second transfers facilitated by IBM FlashSystem arrays. Capitec’s cloud estate drives the bank’s low-fee model, illustrating cost advantages.

The South Africa real time payments market size allocated to cloud is expected to overtake on-premises spend before 2029, barring policy reversals. Regulators have signalled comfort provided data resides in-country and redundancy is proven. Multi-cloud strategies will rise as banks seek to avoid hyperscaler lock-in. Cybersecurity posture improves through automated patching and shared-responsibility models, countering the perception that cloud is less secure for financial workloads.

By Enterprise Size: SME Adoption Accelerates Despite Large Enterprise Dominance

Large enterprises captured 59.40% of 2025 transaction value due to established ERP integrations and stringent treasury mandates. SMEs, however, are forecast to post 33.10% CAGR as they digitalise point-of-sale and supply-chain payments. Happy Pay’s BNPL rails tailor settlement terms to SME cash cycles, evidence that credit-embedded payments resonate with smaller merchants.

The South Africa real time payments market share controlled by SMEs will widen as government pilots focus on township and rural entrepreneurs. Lower fee regimes and alias-based onboarding reduce friction that once deterred informal traders. Fintechs offering plug-and-play POS kits are best placed to capture early wallet share. Large enterprises will continue to invest in API orchestration to connect multiple banks and hedge counterparty risk, sustaining their monetary volume lead.

By End-User Industry: Government & Utilities Growth Challenges Retail Leadership

Retail and e-commerce held a 39.30% slice of 2025 value, buoyed by omnichannel roll-outs and QR acceptance at chains such as Pick n Pay. Government and utilities outpace at 35.60% CAGR, a function of SASSA grants disbursement automation and municipal bill digitisation. Public-sector modernisation avoids cash leakage, cuts fraud, and satisfies National Treasury inclusion goals.

The South Africa real time payments market size in government workflows may double by 2031 as water, power, and toll operators migrate to instant clearing. Education and healthcare represent latent demand once tariff frameworks finalise. Retailers, meanwhile, experiment with crypto rails, loyalty-linked micropayments, and same-day refunds to defend share. Each vertical will require tailored risk and chargeback policies, expanding service-provider revenues.

Geography Analysis

Western Cape and Gauteng lead with 47% and 42% digital-payment penetration respectively, sustained by dense smartphone ownership, fintech clusters, and broadband availability. Cape Town hosts Stitch, Yoco, and over 40 payment startups funded since 2020, creating a virtuous cycle of talent and capital. Gauteng benefits from Johannesburg’s corporate HQ base and rising township e-commerce nodes in Soweto and Tembisa.

KwaZulu-Natal shows mid-tier uptake at 35%. Durban’s port logistics and growing B2B e-commerce provide catalysts, while Budget 2024 township pilots aim to expand merchant-payment infrastructure. Limpopo and Eastern Cape trail at 18-22% due to sparse ATM density, higher data-cost-to-income ratios, and limited bank branch networks. Government and donor programmes are subsidising smartphone acquisition and merchant QR kits in these provinces.

Cross-border flows in the Common Monetary Area now route via SWIFT after a 2024 rule change, elevating fees and lengthening settlement windows, which may slow adoption along Namibia and Eswatini corridors. Yet PayShap’s reach expanded after Capitec, Discovery, and Postbank integrations, narrowing urban-rural gaps. Nationwide, the South Africa real time payments market benefits from consistent regulator messaging: Vision 2025 targets 90% electronic transaction penetration by mid-decade.

Regulatory Landscape

The South African Reserve Bank (SARB) oversees the National Payment System (NPS) under the National Payment System Act 78 of 1998, with the Payments Ecosystem Modernisation (PEM) Programme shaping reforms that affect real-time, low-value rails such as PayShap, operated by BankservAfrica (PayInc). In 2025, SARB issued an interoperability consultation within the NPS, and in February 2026 it published the NPS Vision 2030+ Consultation Paper, extending the Vision 2025 agenda toward longer-horizon digital public infrastructure priorities and broader ecosystem access.

Policy direction in 2026 focuses on widening participation beyond banks while tightening conduct and cross-border controls. The Prudential Authority issued Prudential Communication 10 of 2026 (May 2026) to support an exemption notice for specified payment activities, with intent to move toward activity-based authorization for non-banks. In parallel, SARB released a 2026 draft directive for public comment on conduct in the NPS relating to issuing and acquiring for goods and services provided by offshore merchants, alongside a coordinated approach for cross-border payment facilitators. Together, these measures influence how pay-by-bank and acquiring models are structured for e-commerce and merchant RTP use cases.

Value Chain Analysis

The value chain begins with rule-setting and oversight by SARB and industry governance bodies, including PASA, and then moves to shared infrastructure operators and schemes that run clearing and switching for low-value instant payments. In South Africa, PayShap is the primary domestic real-time rail for simplified account-to-account transfers. It is operated by BankservAfrica (PayInc) and supports interoperability across participating banks using ISO 20022.

Upstream enablers include core banking and payment-switch vendors, fraud and identity/KYC providers, and cloud and data-center infrastructure for low-latency processing. Downstream, banks and licensed payment service providers deliver RTP capabilities through mobile banking apps, APIs, and merchant acceptance products, while fintechs such as Stitch and Ozow package routing, reconciliation, and checkout for retailers and platforms. Merchant and platform adoption relies on payment gateways, POS and QR acceptance, ERP and treasury integration, and settlement and dispute workflows, with BankservAfrica and participating banks handling settlement and liquidity. Bottlenecks remain concentrated in pricing and legacy integration at smaller institutions, while the 2026 policy push toward an exemption notice and an updated authorization framework reduces friction for non-bank participation and increases the set of PSPs that can connect into RTP flows.

Competitive Landscape

Incumbents and fintechs share a moderately concentrated ecosystem. BankservAfrica operates the PayShap switch, processing 74.2 million transactions for R46 billion (USD 2.59 billion) within 18 months of launch. Standard Bank leverages Volante Technologies to modernise across 20 African markets, signalling a platform-sized bet on Payments-as-a-Service. Absa, FNB, and Nedbank are re-architecting cores with ISO 20022 semantics to maintain compliance and latency parity.

Fintech challengers target niches. Stitch’s USD 107 million war-chest funds unified checkout for retailers and subscription platforms. Ozow collaborates with EBANX to extend reach to global merchants needing local instant-pay options. Bank Zero’s cloud-native build sidesteps legacy constraints, offering free checking and under-one-second transfers to win digital natives.

Pricing remains the battleground. Capitec shaved immediate payment fees to R6 (USD 0.34) for 2025, undercutting rivals and courting value seekers. Fraud mitigation maturity differentiates players: FNB deploys AI-based anomaly detection while fintechs embed behavioural biometrics. Market share shifts will depend on the capacity to pair low fees with hardened security and broad alias interoperability inside the South Africa real time payments market.

South Africa Real Time Payments Industry Leaders

Peach Payments

PayU South Africa

iVeri Payment Technologies

Fiserv Inc.

MyGate (Wirecard SA)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Merchant enablement on domestic instant rails is a key white-space area as PayShap expands from person-to-person into person-to-business workflows, including request-to-pay. Rail maturity is visible in PayShap reaching 74.2 million transactions worth R46 billion by October 2024, which supports low-value retail checkout, township commerce settlement, and gig-economy payouts where immediate confirmation can reduce failed delivery and cash-handling risk. The SARB PEM Programme focus on fast, simple digital payments also supports demand for value-added RTP services, including fraud analytics, dispute handling, and ISO 20022 data enrichment that can automate reconciliation for SMEs and large enterprises.

Interoperability and open access initiatives also create room for technology providers and PSPs to standardize acceptance and build API-led payment experiences. SARB published the NPS Vision 2030+ Consultation Paper (February 2026) and, via Prudential Communication 10 of 2026 (May 2026), indicated an intended exemption notice for specified payment activities. This supports a broader set of non-bank participants to deliver RTP-based products without relying only on traditional bank-centric models. Standardization work under PEM, including the QR+ program, with a PayShap payload for structured data exchange, supports national QR acceptance and reduces fragmented merchant checkout experiences. It also increases demand for QR orchestration, token and alias services, and multi-bank routing in retail and e-commerce.

Recent Industry Developments

- July 2026: The South African Reserve Bank released version 1.2 of the QR+ standard under the Payments Ecosystem Modernisation (PEM) Programme, adding a PayShap payload for structured interoperability. The update supports a more uniform QR acceptance layer for merchants and wallets, reducing fragmentation at checkout and linking QR data exchange more tightly to domestic instant payment rails.

- May 2026: The Prudential Authority issued Prudential Communication 10 of 2026 outlining the intention to introduce an exemption notice for specified payment activities and support the updated Authorisation Framework for non-banks. This step advances activity-based participation in the national payment system, widening the set of entities that can build RTP-enabled services while still operating within SARB oversight.

- April 2025: Stitch closed a USD 55 million Series B funding round to scale its payment APIs and support expansion activity. The additional capital increases competitive pressure on banks and established gateways by accelerating omnichannel RTP front-ends and merchant integrations tied to pay-by-bank and instant settlement use cases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the South Africa real-time payments market covers the value of domestic instant account-to-account payment activity that clears in seconds over local real-time rails and related service revenues across the payment flow.

Scope exclusions: Card-scheme routed payments, deferred-net EFT batches, cross-border real-time transfers, and high-value wholesale settlement are excluded from this market sizing.

Segmentation Overview

- By Type of Transaction

- P2P

- P2B

- By Component

- Solutions

- Services

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Deployment

- Cloud

- On-Premises

- By End-user Industry

- BFSI

- Retail and E-commerce

- Government and Utilities

- Healthcare

- Transportation and Education

- Other End-user Industries

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the payments ecosystem and fixing clean reference points for payment volumes, adoption, and the counting rules that define what is included. We relied on public and official sources such as South African Reserve Bank publications, BankservAfrica updates, Statistics South Africa releases, National Treasury and tax authority notes where formalization is relevant to transaction behavior, and Bank for International Settlements CPSS-style payment systems materials.

We also reviewed bank and fintech annual reports, investor presentations, audited financial statements, and trusted press coverage to track product rollouts, pricing shifts, and customer onboarding patterns. Where useful, we pulled supporting company financial intelligence, news and financials, patent databases, and a global contracts and tenders database to assess implementation timing and procurement signals. These are illustrative source types only, and additional references were used during data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to test which rails are actually carrying which transaction types, and how pricing and usage vary across banks, payment processors, billers, and merchant-facing enablers. We covered a mix of incumbents and fast-growing mid-sized providers, then validated assumptions with operational roles in South Africa who see day-to-day volumes and also monitor fraud and dispute patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | |

| Mid tier: 50% | Functional/Unit leaders: 37% | |

| Smaller Players: 15% | Managers: 50% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach where payment-system volume signals and adoption rates are used to reconstruct the domestic real-time transfer total, then mapped to monetized revenue pools through pricing and take-rate assumptions. Those totals were checked with selective bottom-up approximations, including sampled provider volume bands, channel mix checks (P2P versus merchant and bill pay), and ASP-style fee benchmarks observed in interviews.

Key inputs that shaped the model included the rollout pace of the real-time rails, active user and merchant acceptance growth, average transaction value and frequency, and bank or participant pricing (including low-value fee tiers). We also included fraud and chargeback-related friction that can slow repeat usage. When company disclosures left gaps, we used proxy indicators such as app adoption commentary, customer onboarding timelines, and announced product milestones, then narrowed ranges after re-checks with operators.

Forecasting relied on scenario analysis supported by short-series trend smoothing, with adoption and price progression as the main levers. In practice, we ran conservative, base, and faster-uptake paths linked to rail participation expansion, fee reduction expectations, and digital commerce growth, and then aligned the final curve to what experts said is achievable over the next few years.

Data Validation & Update Cycle

Each major assumption was tested in at least two ways, first against an independent signal such as payment-system trends, and then against what interviewees see in day-to-day processing. Outliers were flagged early, and inputs were reworked if they failed logical checks such as unrealistic fee per transaction, implausible active user intensity, or sudden share shifts that were not supported by rollout events.

Before sign-off, the model goes through a multi-step analyst review where calculation logic, unit consistency, and year-to-year bridges are rechecked. Reports are refreshed annually, and interim updates are made when a material event occurs, for example a rail rule change, a major pricing reset, or a notable participation expansion. Right before delivery, we run a final refresh pass to ensure the numbers reflect the latest available public signals.

Mordor Intelligence's South Africa Real Time Payments Market Size Compared With Other Published Estimates

Published estimates for South Africa real-time payments can look far apart because the term can be interpreted differently, and because some models start from payments value while others start from revenue earned across the payment chain. Timing also affects comparability, since rail participation, pricing, and consumer behavior have been changing quickly following new instant-payment launches.

By tracking rail-level participation milestones and applying fee-per-transaction logic, Mordor Intelligence keeps the estimate anchored to domestic low-value instant A2A transfers, rather than blending in cards, batch EFT, or cross-border activity that can inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.57 B (2025) | |

| Trade Journal A | USD 0.49 B (2025) | Often anchored on a narrower definition of real-time transfers that undercounts merchant and biller flows, and may apply conservative adoption assumptions due to early-stage usage patterns. |

| Industry Association B | USD 0.72 B (2025) | Typically uses a broader instant payments bucket that can partially mix in fast EFT variants or adjacent digital transfer products, and may apply a higher average fee assumption without rechecking realized price tiers. |

The spread mainly comes down to what is counted as real-time, and how pricing and usage intensity are translated into value. When scope is kept to domestic instant rails and the fee and volume bridges are checked step by step, the output is easier to reproduce and explain in a planning discussion.

Key Questions Answered in the Report

What is the current value of the South Africa real time payments market?

It stands at USD 756.6 million in 2026 and is projected to climb to USD 3.12 billion by 2031 at a 32.74% CAGR.

Which payment segment is growing fastest?

Person-to-business transfers are expanding at 34.38% CAGR as township merchants and gig-economy platforms demand instant settlement.

How significant is cloud deployment in this space?

Cloud models hold a minority share today but are growing at 36.10% CAGR, poised to overtake on-premises systems before 2029.

Why are interchange fees considered a restraint?

Banks charge R6-10 per instant transaction versus R1-3 for EFTs, discouraging price-sensitive users and slowing mass adoption.

Which provinces lead in real-time payment penetration?

Western Cape and Gauteng top uptake at 47% and 42% respectively, thanks to robust digital infrastructure and fintech ecosystems.

What recent move did Capitec make to gain share?

Capitec slashed its immediate-payment fee to R6 in 2025, undercutting rivals and aligning with national inclusion goals.

Page last updated on: