Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

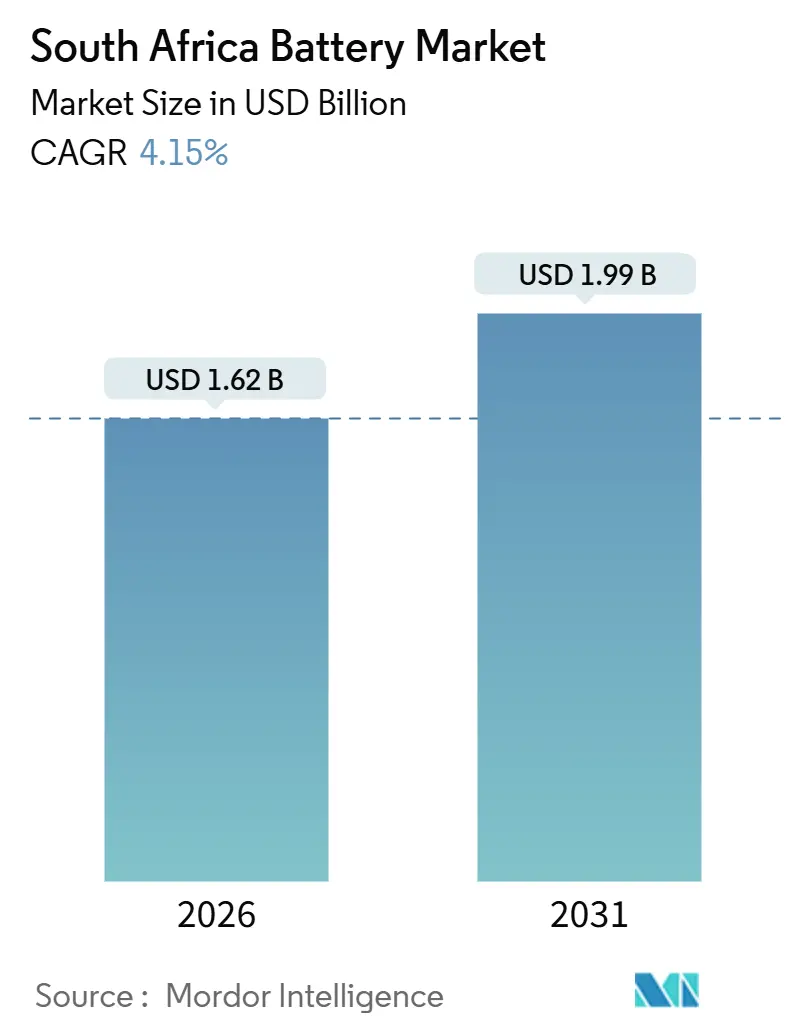

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Battery Market Analysis by Mordor Intelligence

The South Africa Battery Market size is estimated at USD 1.62 billion in 2026, and is expected to reach USD 1.99 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031).

Accelerated investment in utility-scale storage, residential solar-plus-storage, and industrial motive power underpins this expansion, while secondary chemistries displace primary cells across most end uses.[1]Department of Mineral Resources and Energy, “Integrated Resource Plan 2025,” DMRE.gov.za Eskom’s 2,173 MW battery energy storage pipeline, Ford’s plug-in-hybrid export program, and mining electrification targets collectively anchor multi-year demand visibility, insulating the South Africa battery market from cyclical swings in telecom backup purchases.[2]ESI Africa, “Eskom Announces Preferred Bidders for Battery Storage Bid Window 3,” ESI-Africa.com Competitive intensity remains moderate because domestic lead-acid capacity is concentrated in one producer, while all lithium-ion cells are imported, allowing local assemblers to differentiate through balance-of-plant engineering and service offerings.[3]First National Battery, “Products and Services,” FNB.co.za Headwinds revolve around currency depreciation, policy delays in storage licensing, and continued reliance on Asian cell suppliers, yet generous electric-vehicle assembly incentives and a 70% local-content threshold on balance-of-plant components encourage incremental localization, especially in enclosures, inverters, and integration software.

Key Report Takeaways

- By battery type, secondary batteries accounted for 78.3% of the South Africa battery market share in 2025, and are projected to grow at a 7.3% CAGR through 2031.

- By technology, lead-acid held 45.9% share of the South Africa battery market size in 2025, while solid-state is forecast to expand at a 23.6% CAGR through 2031.

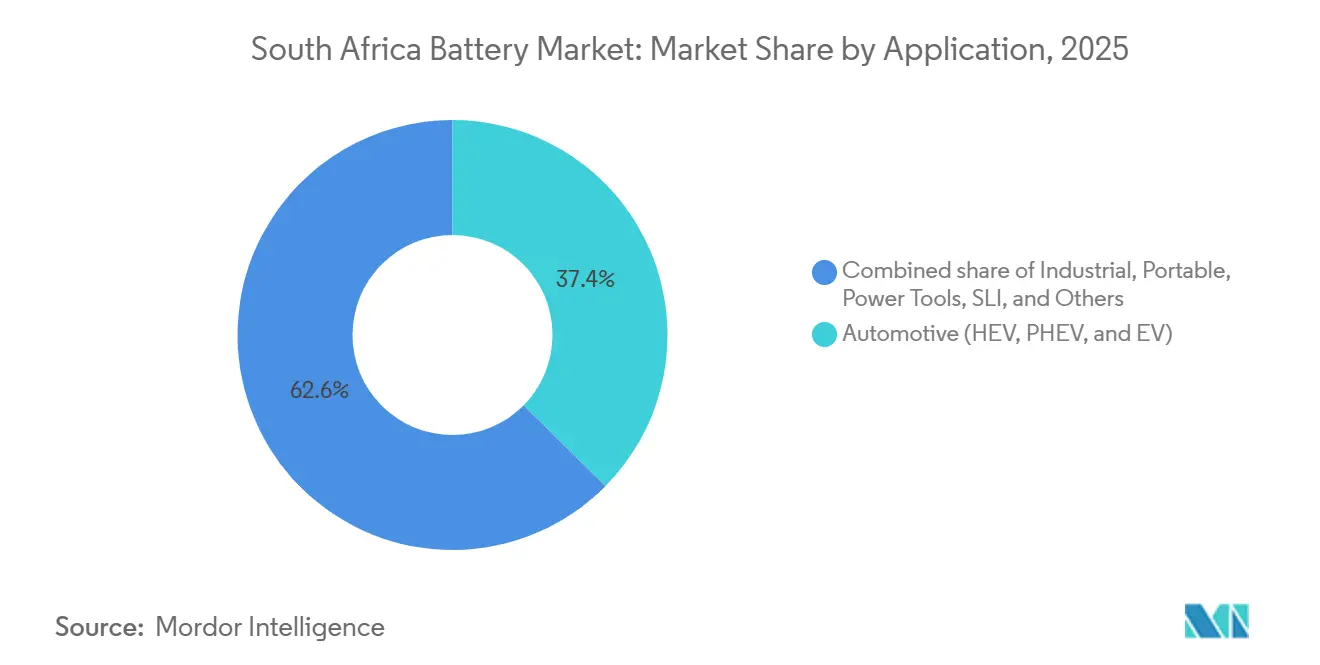

- By application, industrial uses are advancing at an 8.8% CAGR to 2031, outpacing the automotive segment, which led the market share with 37.4% in 2025.

- By geography, Gauteng captured almost 60% of 2025 revenue, reflecting the province’s concentration of automotive, data-center, and telecom activity.

- CATL, LG Energy Solution, and Samsung SDI collectively supplied more than 70% of imported lithium-ion cells in 2025, underscoring a supply chain that remains highly consolidated.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Utility-scale renewables integration mandates | 1.2% | National, with concentration in Northern Cape, Western Cape, and Free State renewable energy zones | Medium term (2-4 years) |

| Telecom tower backup demand surge | 0.6% | National, with highest density in Gauteng, Western Cape metros | Short term (≤ 2 years) |

| EV adoption & localized assembly incentives | 0.9% | National, with assembly concentrated in Gauteng (Ford Silverton, BMW Rosslyn) | Medium term (2-4 years) |

| Mining sector decarbonization targets | 0.5% | Limpopo, North West, Northern Cape mining belts | Long term (≥ 4 years) |

| Eskom BESS procurement programme | 1.3% | National grid integration, priority dispatch zones in Gauteng, KwaZulu-Natal | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Utility-Scale Renewables Integration Mandates

The Integrated Resource Plan 2025 embeds 8,500 MW of battery energy storage by 2039, including 3,100 MW before 2030, effectively tying every new wind or solar plant above 50 MW to four-hour storage systems.[4]Department of Mineral Resources and Energy, “Integrated Resource Plan 2025,” DMRE.gov.za Eskom’s three bid windows already secured 2,173 MW, translating to about 8,700 MWh requiring delivery between 2026 and 2029. Because of 18-to-24-month procurement lead times on cells, developers with tolling arrangements at CATL or LG Energy Solution have a sourcing edge and can lock in forward pricing. Flow batteries, represented by Bushveld Energy’s 1 MW/4 MWh vanadium project, highlight non-lithium alternatives where long cycle life compensates for higher capex. Still, lithium-ion retains cost leadership for four-hour duty cycles, keeping the South Africa battery market firmly oriented toward imported NMC and LFP cells for grid storage.

EV Adoption and Localized Assembly Incentives

A 150% tax deduction on electric-vehicle production costs, effective March 2026, aims to triple domestic plug-in-hybrid and battery-electric output by 2028, even though cell manufacturing remains outside the incentive’s scope. Ford’s Silverton plant produced sixty-two thousand Ranger PHEV packs in 2025, all earmarked for export, while BMW’s Rosslyn facility began next-generation X3 PHEV assembly in late 2024. Domestic EV sales rose from fewer than nine hundred units in 2021 to nearly five thousand in 2022, yet they still account for under 1% of the national fleet, constrained by a charging network of roughly 370 stations. Even so, predictable pack demand from export lines provides steady volume for module assembly and end-of-life recycling, strengthening the South Africa battery industry over the medium term.

Mining Sector Decarbonization Targets

Anglo American activated 84 MW of battery-electric equipment in 2024, including a 290-tonne haul truck with a 1.2 MWh pack, and plans to electrify about 400 trucks by 2030, implying over 500 MWh of cumulative demand. Lithium-ion’s two-to-three-times longer cycle life and opportunity charging yield 15%-to-20% lower total cost of ownership versus lead-acid, despite a 40% premium. Forklift and underground loader fleets are following suit, stimulating orders for modular LFP systems from BlueNova and Freedom Won. Solid-state cells promise higher tolerance to high-ambient temperatures typical of deep mining, but commercial volumes remain at least two years away. Consequently, long-term electrification plans anchor steady demand that reinforces the South Africa battery market beyond automotive cycles.

Eskom BESS Procurement Programme

Bid Windows 1 through 3 awarded 513 MW, 616 MW, and 1,044 MW, respectively, each tied to inflation-indexed twenty-year offtake agreements. Local-content rules require a 70% domestically sourced balance-of-plant components, accelerating investment in enclosures, inverters, and civil works. However, grid-connection delays caused by substation upgrades have extended commissioning by six to twelve months for early projects, compressing developer returns and nudging some sponsors toward refinancing. Despite timing slippage, the procurement guarantees multi-gigawatt-hour cell offtake and cements the South Africa battery market as a core pillar of the national energy transition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import-dependent cell supply chain | -0.4% | National, affecting all lithium-ion segments | Medium term (2-4 years) |

| Limited domestic manufacturing base | -0.3% | National, with potential localization in Gauteng industrial corridors | Long term (≥ 4 years) |

| Policy delays on storage licensing | -0.2% | National, NERSA jurisdiction over grid-connected projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Import-Dependent Cell Supply Chain

South Africa imports more than 95% of its lithium-ion cells, mainly from China, South Korea, and Japan, exposing integrators to shipping disruptions, rand depreciation, and trade disputes. Although the country mines roughly 40% of global manganese ore, fewer than 5% of refined battery-grade manganese sulphate units are produced domestically, forcing two-way trade flows that inflate costs. The planned 10,000-tonne battery-grade manganese sulphate plant from Manganese Metal Company will meet only a fraction of cathode demand by the end of the decade. Each 10% slide in the rand lifts landed cell costs by about 8%, lengthening residential solar storage payback periods by one year or more, and taking some momentum out of the South Africa battery market’s near-term growth.

Policy Delays on Storage Licensing

National Energy Regulator of South Africa guidelines covering third-party-owned storage assets and behind-the-meter systems above 1 MW remain in consultation, deferring nearly 200 MW of private projects. Developers face uncertain wheeling charges and technical compliance criteria, forcing engineers to over-specify inverters to ensure grid-code compatibility, which inflates capex by up to 8%. The absence of a clear interconnection queue adds further unpredictability, with approval timelines ranging from three months to more than a year. Consequently, some investors demand higher hurdle rates, dampening the otherwise positive trajectory of the South Africa battery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeables Gain Dominance

Secondary batteries commanded 78.3% of 2025 revenue within the South Africa battery market. They are projected to advance at a 7.3% CAGR through 2031, underpinned by lithium-ion uptake in automotive export lines and Eskom’s grid-storage build-out. Ford assembles 62,000 plug-in-hybrid packs per year in Silverton, and BMW scales X3 PHEV modules in Rosslyn, reinforcing predictable demand volumes. Primary cells remain confined to consumer electronics where convenience trumps lifecycle economics.

Lead-acid continues to anchor automotive start-lighting-ignition and telecom backup thanks to a mature recycling loop that recovers 96% of content. Yet lithium-ion’s superior depth-of-discharge and high-cycle life make it the chemistry of choice for residential solar, office, uninterrupted-power-supply, and utility storage. REVOV’s second-life EV modules, priced 40% below new cells, illustrate how circular-economy models expand addressable demand for lithium-ion systems. The South Africa battery market size for rechargeable chemistries will therefore widen its lead over primary alternatives throughout the forecast horizon.

By Technology: Incumbent Lead-Acid Meets Emerging Solid-State

Lead-acid technology held 45.9% of the South Africa battery market share in 2025, yet solid-state prototypes are poised for the fastest expansion at a 23.6% CAGR. Lithium-ion remains the performance and cost benchmark today, split between LFP for stationary applications and higher-energy NMC for automotive. International Energy Agency data indicate LFP could capture half of global EV batteries by 2026, owing to cobalt-free cathodes and better thermal stability. Vanadium-redox flow batteries offer a twenty-year cycle life and inherent non-flammability; Bushveld Energy’s 1 MW/4 MWh installation validates the chemistry’s industrial potential, although capex per kilowatt-hour is still double that of lithium-ion.

Sodium-ion and zinc-air technologies remain pre-commercial but could disrupt price-sensitive stationary markets after 2028 if raw-material security becomes critical. Meanwhile, the South Africa battery market size for lead-acid will erode slowly as recycled content advantages are outweighed by lithium-ion’s superior energy density in new applications. Solid-state’s commercial arrival around 2028 may accelerate displacement if cost curves align with automotive pack targets below USD 80 per kWh.

By Application: Industrial Demand Outpaces Automotive

Industrial uses, which include telecom backup, uninterruptible power supplies, motive power, and utility-scale storage, are projected to grow at an 8.8% CAGR through 2031, eclipsing the automotive segment’s 4.1% pace. Eskom’s four-hour BESS mandate alone represents nearly 8,700 MWh of new installations, dwarfing on-road EV demand. Ford and BMW export nearly all locally assembled plug-in-hybrid packs, limiting home-market automotive volumes to fewer than 5,000 EVs in 2022.

Mining electrification reinforces the industrial narrative: Anglo American’s haul-truck prototype signals a potential 500 MWh battery requirement by 2030. Data-center developers in Johannesburg specify lithium-ion UPS systems that occupy half the floor space of valve-regulated lead-acid alternatives and last 10 to 15 years. Telecom operators, after spending R2.5 billion on backup batteries in 2023, are trialing lithium-ion units with GPS tracking to curb theft, which cost MTN R450 million in 2024. Residential demand is moving upscale: Tesla’s Powerwall 3 debuted at R181,873 and integrates with a virtual power plant program that yields bill-credit revenue streams. Collectively, diversified industrial ordering anchors multi-year growth in the South Africa battery market.

Geography Analysis

Gauteng generated nearly 60% of 2025 revenue for the South Africa battery market, driven by automotive assembly, telecom tower density, and Johannesburg’s expanding data-center clusters. Ford Silverton, BMW Rosslyn, and Nissan Rosslyn account for the bulk of localized pack assembly, while high-tech campuses in Midrand specify lithium-ion uninterrupted-power-supply systems to mitigate grid instability. Upscale suburbs in Johannesburg and Pretoria, experiencing frequent Stage 4-to-6 load-shedding, prioritize residential solar storage, underpinning premium sales of BlueNova and Freedom Won modules.

The Western Cape contributes around one-quarter of national demand, anchored by Cape Town’s early adoption of rooftop solar, Time-of-Use tariffs, and municipal incentives for home energy storage. Tesla Powerwall and BlueNova units priced between R66,450 and R181,873 gain traction among affluent households, while commercial installations in Stellenbosch wineries and Table View retail centers underscore small-business uptake. Renewable energy zones in the Western and Northern Cape host the majority of awarded utility-scale BESS projects, leveraging high solar capacity factors to shift midday generation into evening peaks.

Limpopo and North West provinces form a third node, where mining electrification is propelling demand for high-capacity lithium-ion packs in haul trucks and underground loaders. KwaZulu-Natal and Eastern Cape together account for roughly 10% to 15% of the market, driven by Durban’s port logistics and automotive component suppliers. Telecom backup orders, once concentrated in Gauteng and Western Cape, have become more regionally balanced as operators roll out solar-battery hybrids at rural tower sites to curb diesel use. This spatial distribution highlights how the South Africa battery market aligns with industrial hubs, renewable resource corridors, and electrification mandates.

Competitive Landscape

Global cell makers, CATL, LG Energy Solution, Samsung SDI, BYD, and Panasonic, supply over 90% of lithium-ion cells imported into South Africa. Local integrators then assemble modules and packs tailored to residential, commercial, and utility requirements. First National Battery, owned by Metair, manufactures roughly 2.2 million lead-acid units a year and dominates the automotive start-lighting-ignition space with entrenched recycling contracts. Exide Industries supplies aftermarket lead-acid, while BlueNova, Freedom Won, and REVOV address lithium-ion and second-life niches.

Strategic moves in 2025-2026 include Tesla selecting Rubicon Energy and Segen South Africa as Powerwall 3 distributors, bolstering premium residential presence. REVOV opened a Durban facility targeting 2,000 repurposed EV battery sales in 2024, expanding the circular-economy footprint. Bushveld Minerals scaled vanadium electrolyte output to eight million liters a year, positioning itself as a flow-battery component supplier as industrial microgrid demand matures.

Eskom’s 70% local-content rule on balance-of-plant elements has spurred joint ventures between international independent power producers and South African EPCs, such as Scatec’s partnership with WBHO for civil works. BYD’s ongoing discussions with the government for a potential assembly plant underscore rising interest in capturing regional demand for both vehicles and stationary storage. Even so, the absence of a domestic gigafactory leaves the supply chain vulnerable to import logistics and currency swings, maintaining moderate rather than intense competition within the South Africa battery market.

South Africa Battery Industry Leaders

Eveready (Pty) Ltd.

Probe Group

First National Battery

Freedom Won (Pty) Ltd.

BlueNova Energy (Pty) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Eskom confirmed preferred bidders for Battery Energy Storage Bid Window 3, awarding 1,044 MW to international consortia.

- March 2025: Ford commenced full-rate Ranger PHEV production at the Silverton plant after investing R5.2 billion (USD 272 million).

- March 2025: Tesla launched Powerwall 3 in South Africa at a price of R181,873, including Gateway 3, targeting premium residential solar-plus-storage applications.

- September 2024: BYD advanced talks with the South African government on potential local battery and EV manufacturing investment.

South Africa Battery Market Report Scope

A battery can be defined as an electrochemical device (consisting of one or more electrochemical cells) that can be charged with an electric current and discharged whenever required. Batteries are widely employed to power small electric devices such as mobile phones, remotes, and flashlights. Batteries are primarily classified based on technology by the underlying technology upon which they work. A battery contains fundamentally three parts: two electrodes and an electrolyte. A battery works by undergoing a chemical reaction, an oxidation reaction at the cathode, and a reduction reaction at the anode that completes the circuit and maintains charge neutrality. The chemical reaction at the electrode changes when the materials used are different, and subsequently gives rise to different battery types.

The South African battery market is segmented by technology and application. By Battery type, the market is segmented into Primary Batteries and Secondary Batteries. By technology, the market is segmented into Li-ion Battery, Lead-acid Batteries, Nickel Battery, and Others. By application, the market is segmented into Industrial, Portable, Power Tools, SLI, and Others. For each segment, the market sizing and forecasts have been done based on revenue (USD Billions) for all the above segments.

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications |

Key Questions Answered in the Report

How fast is demand for battery growing in South Africa?

How fast is demand for batteries growing in South Africa?

Which chemistry leads residential solar storage sales?

Lithium-ion, particularly LFP modules from BlueNova, Freedom Won and Tesla, dominates because of high cycle life and compact form factors.

What share did secondary batteries hold in 2025?

Secondary chemistries captured 78.3% of market revenue thanks to lithium-ion adoption in automotive export lines and grid storage.

Why is domestic cell production still limited?

Incentives focus on vehicle assembly rather than cell manufacturing, and investors are deterred by scale uncertainty and grid reliability challenges.

Which province generates the most battery demand?

Gauteng accounts for almost 60% of national revenue due to its concentration of automotive plants, data-center clusters and telecom infrastructure.

How big is the opportunity in mining electrification?

Anglo American alone expects to deploy battery packs exceeding 500 MWh by 2030 as it converts diesel haul fleets to electric power.

Page last updated on: