Software As A Medical Device (SaaMD) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

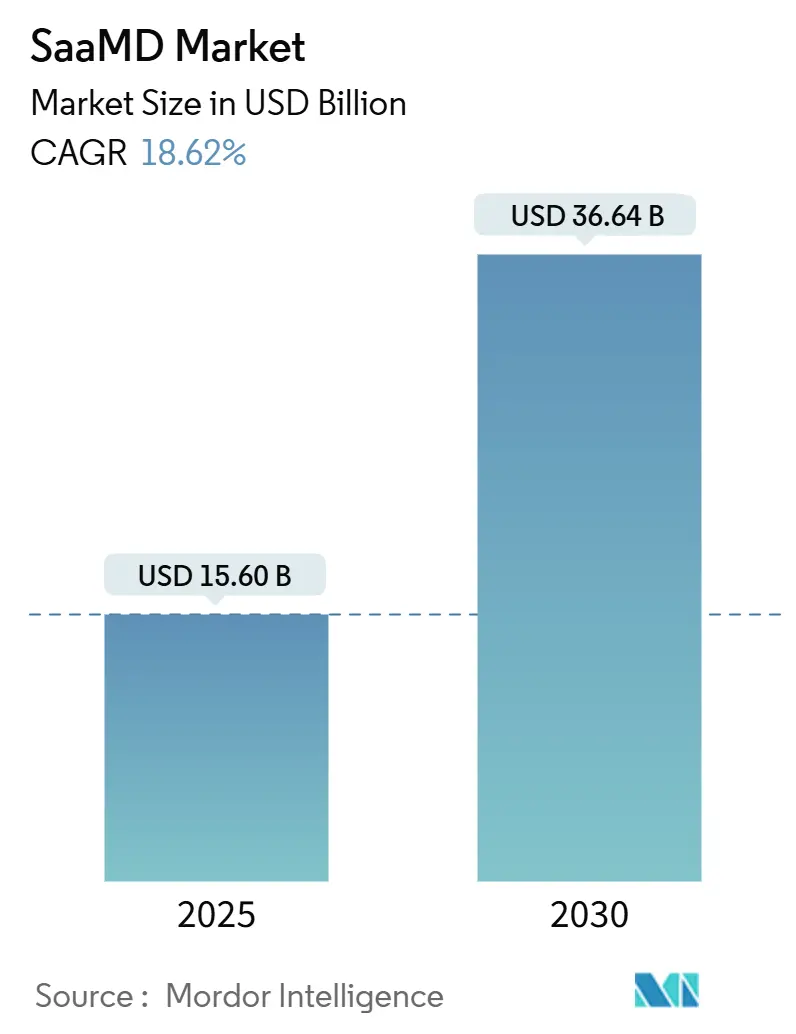

| Market Size (2025) | USD 15.60 Billion |

| Market Size (2030) | USD 36.64 Billion |

| Growth Rate (2025 - 2030) | 18.62% CAGR |

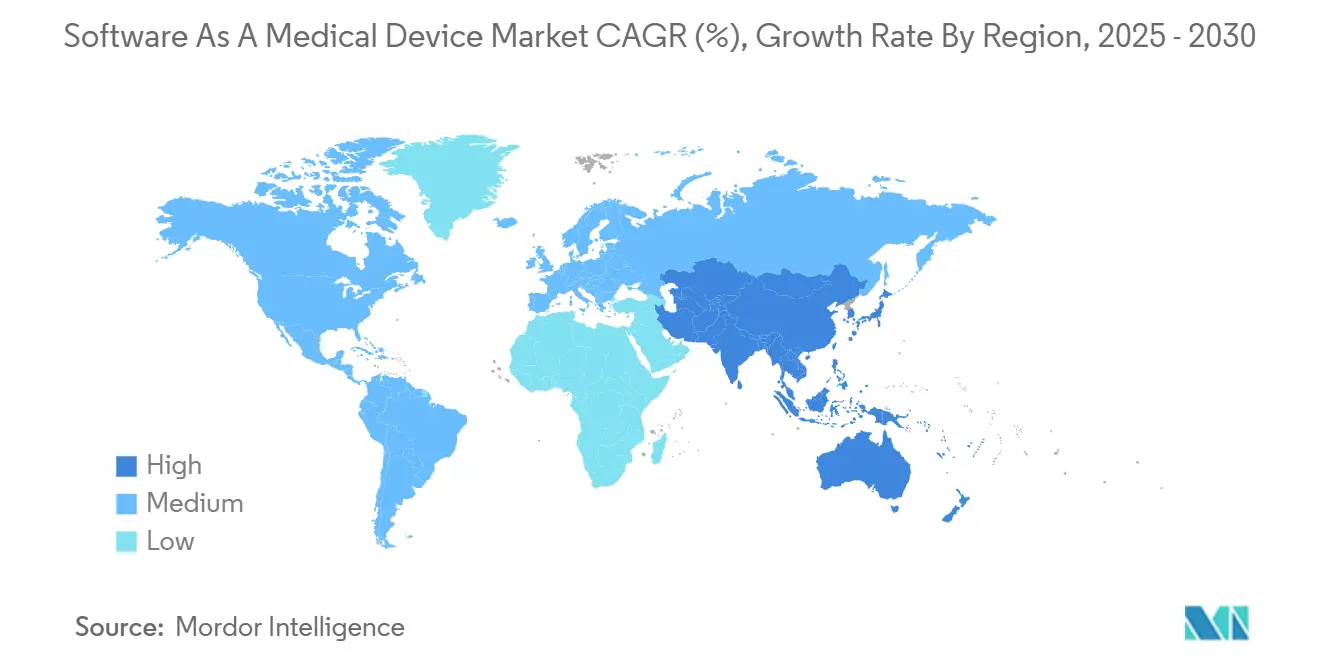

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

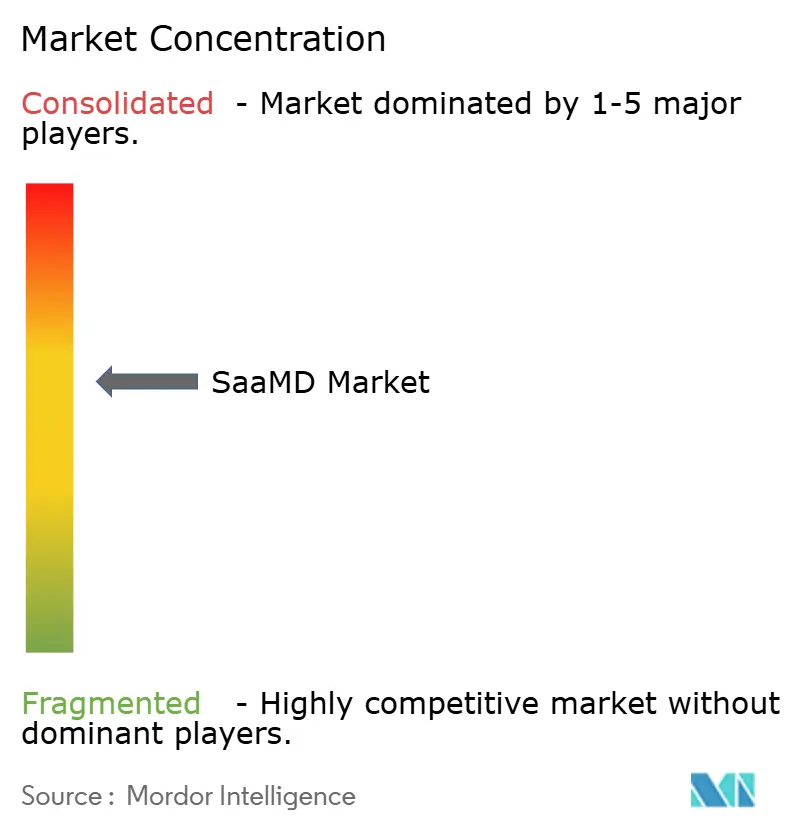

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Software As A Medical Device (SaaMD) Market Analysis by Mordor Intelligence

The software as a medical device market size is valued at USD 15.60 billion in 2025 and is forecast to climb to USD 36.64 billion by 2030, registering an 18.6% CAGR. Demand is propelled by clearer regulatory pathways, expanding reimbursement codes, and growing clinical evidence that positions SaaMD at the heart of precision-care workflows. FDA clearance of more than 1,000 AI-enabled devices by 2024 underscores the regulator’s confidence in algorithm-driven diagnostics and therapeutics[1]Food and Drug Administration, “Guidance for Connected Medical Devices,” fda.gov. Reimbursement support is widening: the Centers for Medicare and Medicaid Services (CMS) introduced dedicated digital mental-health treatment codes effective January 2025, signalling recognition of software-based therapeutics. Hospital-at-home programs, backed by CMS coverage, are speeding cloud adoption, while rising venture investment and strategic collaborations highlight the sector’s growth prospects.

Key Report Takeaways

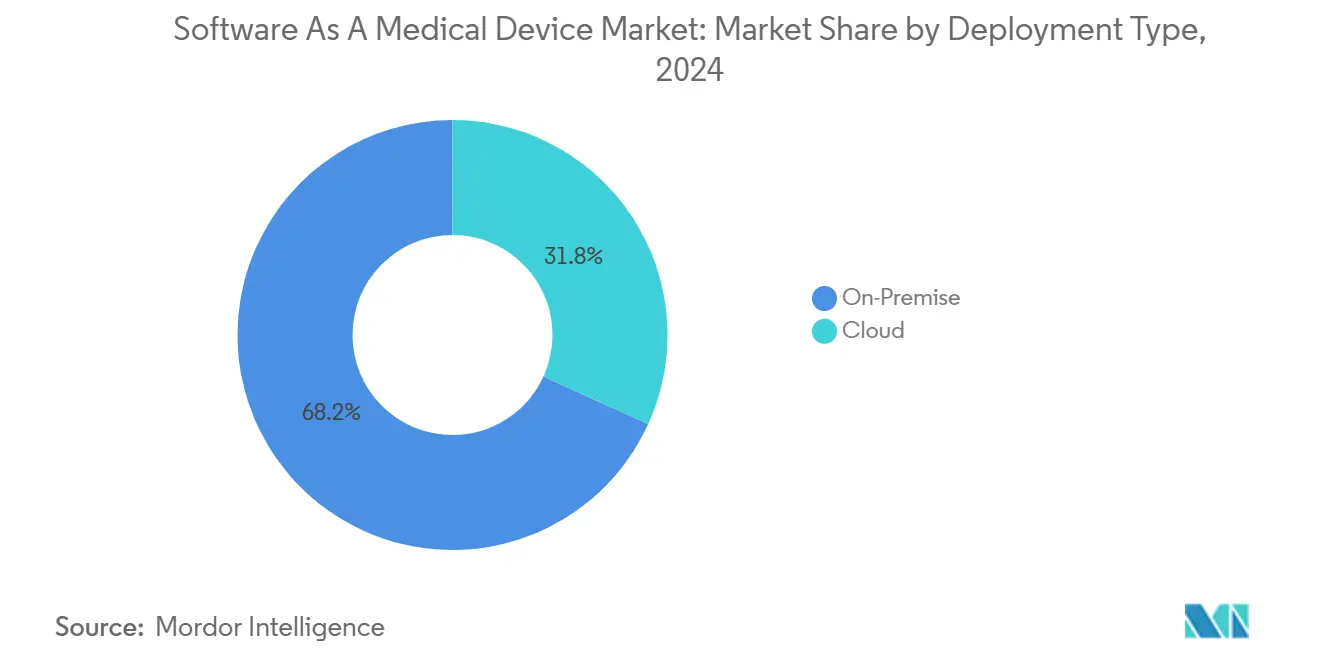

- By deployment type, on-premise solutions led with 68.2% of software as a medical device market share in 2024; cloud deployments are advancing at a 19.7% CAGR to 2030.

- By application, screening and diagnosis accounted for 44.7% of the software as a medical device market share in 2024, while chronic-disease management is projected to expand at an 18.9% CAGR through 2030.

- By end-user, hospitals and clinics held 55.3% revenue share in 2024; home-care settings show the fastest growth at a 19.2% CAGR to 2030.

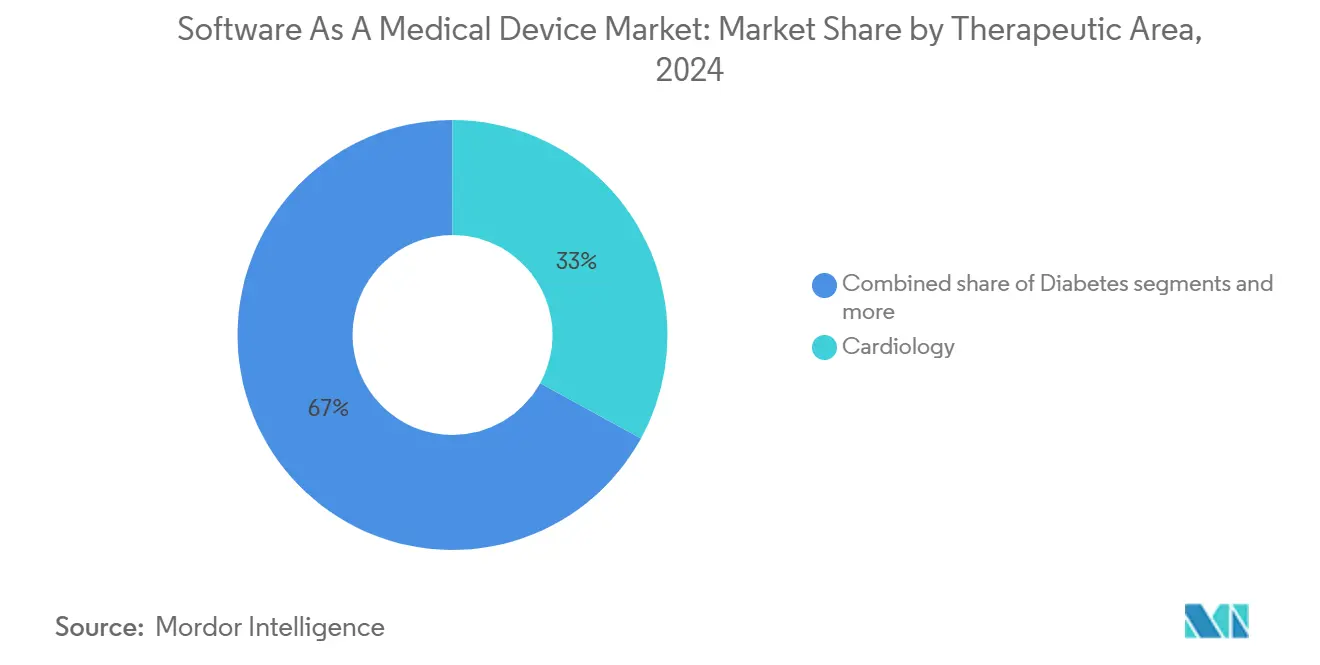

- By therapeutic area, cardiology captured 33.0% market share in 2024; oncology is the quickest-growing segment at an 18.8% CAGR to 2030.

- By geography, North America dominated with 38.1% share in 2024, whereas Asia-Pacific is forecast to deliver a 19.5% CAGR between 2025 and 2030.

Global Software As A Medical Device (SaaMD) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic diseases | +3.2% | Global, highest in aging Japan, Europe, North America | Long term (≥ 4 years) |

| Increasing adoption of AI-driven digital health | +4.1% | North America, EU lead; APAC rising | Medium term (2-4 years) |

| Rising demand for remote patient monitoring | +2.8% | Global, accelerated by hospital-at-home programs | Short term (≤ 2 years) |

| Regulatory incentives for digital therapeutics | +2.3% | North America, EU; ripple into regulated markets | Medium term (2-4 years) |

| Companion-diagnostic convergence | +1.9% | Global oncology markets, mainly developed regions | Long term (≥ 4 years) |

| Hospital-at-home reimbursement models | +2.1% | North America first; EU pilots emerging | Short term (≤ 2 years) |

Source: Mordor Intelligence

Growing Prevalence of Chronic Diseases

Chronic conditions now dominate health-expenditure profiles, compelling care models that track patients continuously rather than episodically. In super-aging Japan, technology is being deployed to offset workforce shortages by automating long-term monitoring and early-warning analytics. SaaMD platforms integrate wearables with predictive models, reducing emergency admissions for diabetes and cardiovascular disorders. Continuous biomarker feeds allow dosage adjustments and targeted coaching, helping providers shift toward outcome-based reimbursement. This persistent need for scalable disease management underpins durable demand across the software as a medical device market.

Increasing Adoption of AI-Driven Digital Health

Machine-learning models now transform SaaMD from static rule sets into adaptive systems that learn from real-world data. Imaging spearheads this shift: 77% of FDA-cleared AI devices assist radiologists, and cardiology already boasts 161 approvals for rhythm-analysis tools. Regulatory innovation matters—FDA guidance on predetermined change-control plans, finalized in December 2024, lets manufacturers update algorithms without reopening lengthy clearance files. With the compliance hurdle lowered, vendors can iterate swiftly, lifting diagnostic accuracy and fostering a virtuous data loop that further enlarges the software as a medical device market.

Rising Demand for Remote Patient Monitoring

Remote monitoring has moved from pandemic expedient to mainstream modality, supported by CMS fee-schedule updates that now cover Federally Qualified Health Centers and Rural Health Clinics[2]Centers for Medicare and Medicaid Services, “CY 2025 Physician Fee Schedule Final Rule,” cms.gov. CMS hospital-at-home pilots, encompassing 366 hospitals and 31,000 patients, demonstrate lower 30-day mortality, proving cloud-connected care is clinically viable. SaaMD unifies FDA-approved devices, telehealth video, and analytics dashboards, giving clinicians a continuous view of vitals, adherence, and symptoms. This allows proactive intervention and aligns with value-based payment models focused on avoiding costly readmissions.

Regulatory Incentives for Digital Therapeutics

Regulators are carving out distinct reimbursement routes for software-only treatments. CMS mental-health codes (G0552-G0554), effective January 2025, reimburse cognitive behavioral therapy apps such as Rejoyn for depression. In Europe, the AI Act offers regulatory sandboxes for high-risk software, letting developers trial products in controlled settings while gathering evidence. The UK’s MHRA AI Airlock applies a similar approach within NHS hospitals, accelerating real-world validation. These mechanisms lower go-to-market friction, fostering revenue certainty and expanding the software as a medical device industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex and evolving regulatory landscape | -2.7% | Global; EU most complex post-AI Act | Medium term (2-4 years) |

| Data-privacy and cybersecurity concerns | -1.8% | Global; strictest in EU and United States | Short term (≤ 2 years) |

Source: Mordor Intelligence

Complex and Evolving Regulatory Landscape

SaaMD developers must reconcile multiple, often overlapping regulations: EU Medical Device Regulation, the new AI Act, and country-specific guidance. Smaller firms can face compliance costs topping USD 1 million per region, elongating launch timelines. While FDA’s De Novo path and change-control guidance ease some US hurdles, inconsistent standards across borders still impede simultaneous global rollout. Harmonization talks within the International Medical Device Regulators Forum are progressing slowly, prolonging uncertainty and tempering the software as a medical device market’s full potential.

Data-Privacy and Cybersecurity Concerns

Connected devices hold sensitive health data, making them prime targets for cyberattacks. FDA rules effective October 2023 require a software bill of materials and secure-by-design evidence for every connected device submission, adding engineering overhead Food and Drug Administration. Healthcare breaches climbed 32% in 2024, spurring hospitals to demand rigorous security postures from vendors. EU GDPR penalties—fines of up to 4% of global revenue—further raise stakes. Vendors that cannot document robust encryption, patch-management, and bias-mitigation protocols risk market exclusion and eroded trust, damping adoption in the software as a medical device market.

Segment Analysis

By Deployment Type: Cloud Migration Accelerates Despite Security Concerns

The software as a medical device market size tied to on-premise architecture captured 68.2% share in 2024, reflecting hospitals’ priority on data sovereignty and established hospital-information-system interfaces. Yet cloud solutions are scaling at a 19.7% CAGR because hospital-at-home programs require real-time analytics and scalable storage. CMS reimbursement for acute-care-at-home illustrates how policy converts cloud from optional to essential infrastructure.

Cloud providers have achieved HIPAA attestation, and FDA cybersecurity guidance now standardizes software bill-of-materials reporting, reducing risk perceptions. Hybrid and edge models store sensitive records locally but offload AI training to secure clouds, meeting latency and compliance needs. As privacy policies mature, hospitals increasingly view cloud as a cost-effective pathway to innovation, reshaping the software as a medical device market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Chronic Disease Management Drives Therapeutic Evolution

Screening and diagnosis held 44.7% of software as a medical device market share in 2024, anchored by imaging AI. Chronic-disease management, however, is forecast to expand at 18.9% CAGR, transforming disease control from episodic visits to continuous algorithms that titrate therapy. CMS mental-health codes validate software as therapy, signalling payer acceptance far beyond diagnostics.

Platforms now blend monitoring, alerting, and therapeutic coaching, creating closed-loop ecosystems. Continuous glucose monitors feeding insulin algorithms, or cardiac wearables guiding medication, underscore how SaaMD reduces clinical workload while improving outcomes. This integrated approach reinforces the software as a medical device market’s momentum toward end-to-end care.

By End-user: Home-care Settings Reshape Delivery Models

Hospitals and clinics still accounted for 55.3% of revenue in 2024, but home-care settings are growing at a 19.2% CAGR. Evidence from CMS demonstrates that supervised home hospitalization yields lower mortality and better patient satisfaction.

Designing for lay users forces manufacturers to prioritize intuitive interfaces and automated calibration. FDA human-factors guidance emphasizes usability studies before clearance. Telehealth connectivity enables clinicians to supervise remotely, marrying patient freedom with professional oversight, widening access and advancing the software as a medical device market.

By Therapeutic Area: Oncology Precision Medicine Accelerates Growth

Cardiology commanded a 33.0% share in 2024. Oncology, though smaller, is rising fastest at an 18.8% CAGR as companion diagnostics merge with AI pathology algorithms. Roche and PathAI’s tie-up on biomarker-driven therapy selection highlights this direction[3]Roche Holding AG, “PathAI Partnership Press Release,” roche.com.

Genomic data combined with imaging and vital signs delivers multi-modal assessment, letting oncologists tailor regimens while tracking toxicity in near real-time. This precision-medicine push expands the software as a medical device market size allocated to oncology, moving software from a supportive tool to a critical therapeutic enabler.

Note: Segment shares of all individual segments available upon report purchase

By Regulatory Class: Class III Complexity Drives Innovation

Class II devices represented 61.0% of 2024 revenue, balancing risk and regulatory agility. Class III, covering autonomous diagnosis and closed-loop therapy, is growing at 19.3% CAGR due to the De Novo route that bypasses slow 510(k) precedent comparison.

FDA change-control guidance lets Class III vendors update algorithms under a pre-approved plan, ensuring safety while sustaining innovation. This clarity encourages investment in higher-risk applications, broadening the software as a medical device market landscape.

Geography Analysis

North America secured 38.1% of global revenue in 2024, benefiting from FDA credibility and CMS reimbursement tools that catalyze rapid commercialization. The introduction of digital mental-health billing codes and the expansion of hospital-at-home pilots furnish predictable revenue streams, anchoring further SaaMD rollouts. Canada’s joint-review pilots with the FDA shorten approval times, while Mexico’s first Class II SaaMD approval shows regional momentum.

Asia-Pacific, projected at a 19.5% CAGR, is the fastest-growing node of the software as a medical device market. Japan’s super-aged population drives the adoption of monitoring platforms that offset caregiver shortages. China’s digital-health investment, combined with evolving approval pathways, accelerates domestic startups. South Korea’s Digital Medical Products Act, effective January 2025, formalizes standards, and India’s National Digital Health Mission opens marketplace access through telemedicine expansion.

Europe balances strict oversight with innovation promotion. The August 2024 AI Act harmonizes classification, easing cross-border trade yet demanding algorithmic transparency. Germany’s DiGA Fast-Track reimburses low-risk apps within statutory insurance. The UK’s AI Airlock gathers real-world evidence in NHS clinics, providing iterative validation. Although compliance costs rise, unified rules eventually simplify multi-country scaling, sustaining Europe’s sizeable portion of the software as a medical device market.

Competitive Landscape

The software as a medical device market remains moderately concentrated. Established device firms leverage regulatory know-how and installed hardware bases to add AI layers—Philips’ SmartSpeed Precise MRI illustrates such platform integration[4]Royal Philips, “Philips SmartSpeed Precise MRI Launch Announcement,” philips.com. Pharmaceutical giants pair with AI specialists: Roche-PathAI targets pathology algorithms that guide therapeutic choices.

Venture investment, topping USD 14 billion since 2010, funds specialist entrants, yet regulatory capital requirements curb fragmented proliferation. Platform ecosystems out-compete single-function apps by embedding multiple algorithms into clinician workflows, reducing procurement complexity. Continuous-learning capability, enabled by FDA change-control plans, becomes a key moat: firms with high-volume data pipelines refine algorithms quicker, raising performance bars that latecomers struggle to meet.

Cybersecurity is another differentiator. Hospitals favor vendors with demonstrable secure-development-lifecycle processes and real-time patching. Specialist security firms partner with device makers, combining cryptography with medical-grade usability. As reimbursement broadens beyond diagnostics into therapeutic codes, rivals that integrate end-to-end disease-management modules will strengthen their hold over the software as a medical device market.

Software As A Medical Device (SaaMD) Industry Leaders

-

Zühlke Engineering AG

-

Koninklijke Philips N.V

-

Siemens Healthcare Private Limited

-

Medtronic plc

-

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Philips launched SmartSpeed Precise MRI with dual AI engines, cutting scan times and automating 80% of MR workflows.

- February 2025: Roche partnered with PathAI to co-develop AI pathology algorithms for companion diagnostics.

- January 2025: CMS implemented digital mental-health treatment codes (G0552-G0554), creating Medicare payment for software-based therapeutics.

- January 2025: South Korea’s Digital Medical Products Act took effect, establishing filing pathways for SaaMD.

- December 2024: FDA finalized guidance on predetermined change-control plans for AI device software.

Global Software As A Medical Device (SaaMD) Market Report Scope

Software as a Medical Device (SaMD) refers to software that delivers medical functions independently of any hardware. SaMD enhances the speed of diagnosing, managing, and treating medical conditions and diseases. By automating certain care aspects, it not only elevates the quality of care but also conserves valuable time.

Software as a Medical Device Market is segmented by deployment type (cloud, on-premise), by application (screening and diagnosis, monitoring and alerting, and chronic disease management) by end user industry (hospitals and clinics, and home care arrangements) by geography (North America, Europe, Asia-Pacific, Latin America and Middle East and Africa).

The report offers market forecasts and size in value (USD) for all the above segments.

| By Deployment Type | Cloud | |||

| On-Premise | ||||

| By Application | Screening and Diagnosis | |||

| Monitoring and Alerting | ||||

| Chronic Disease Management | ||||

| Therapeutic Support | ||||

| By End-user | Hospitals and Clinics | |||

| Home-care Settings | ||||

| Ambulatory Surgical Centers | ||||

| By Therapeutic Area | Cardiology | |||

| Diabetes | ||||

| Oncology | ||||

| Neurology | ||||

| Respiratory | ||||

| By Regulatory Class | Class I | |||

| Class II | ||||

| Class III | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Spain | ||||

| Italy | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia and New Zealand | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Rest of Africa | ||||

| Cloud |

| On-Premise |

| Screening and Diagnosis |

| Monitoring and Alerting |

| Chronic Disease Management |

| Therapeutic Support |

| Hospitals and Clinics |

| Home-care Settings |

| Ambulatory Surgical Centers |

| Cardiology |

| Diabetes |

| Oncology |

| Neurology |

| Respiratory |

| Class I |

| Class II |

| Class III |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the software as a medical device market by 2030?

The market is forecast to reach USD 36.64 billion by 2030, growing at an 18.6% CAGR.

Which region is expanding fastest in the software as a medical device market?

Asia-Pacific is projected to grow at a 19.5% CAGR between 2025 and 2030.

How large is the cloud segment within the software as a medical device market?

While on-premise still leads, cloud deployments are growing at 19.7% CAGR and are expected to close the gap as hospital-at-home programs expand.

What applications are driving future growth?

Chronic-disease management solutions show the highest momentum, outpacing traditional screening & diagnosis with an 18.9% CAGR.

How are regulators supporting digital therapeutics?

CMS introduced mental-health treatment codes in 2025, and the EU’s AI Act provides sandboxes that speed safe market access for therapeutic software.

What cybersecurity requirements apply to SaaMD vendors?

FDA rules require a software bill of materials and secure-by-design evidence, while GDPR imposes strict data-protection obligations in Europe.

Page last updated on: June 18, 2025