Infection Surveillance Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

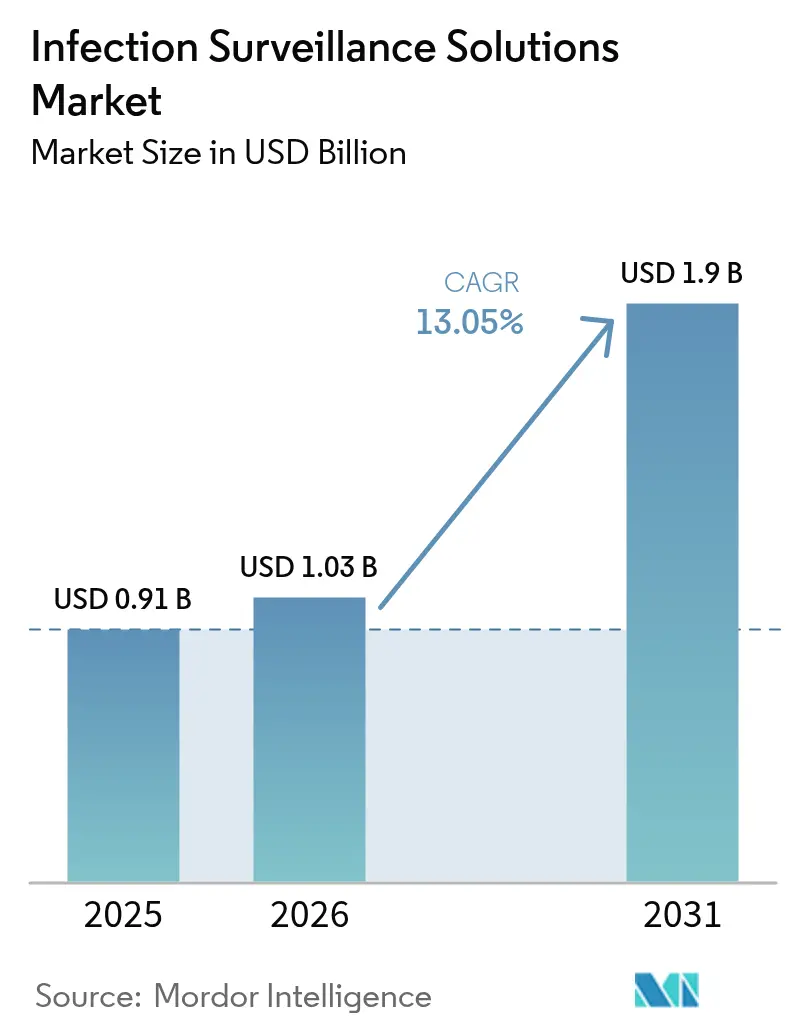

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.9 Billion |

| Growth Rate (2026 - 2031) | 13.05% CAGR |

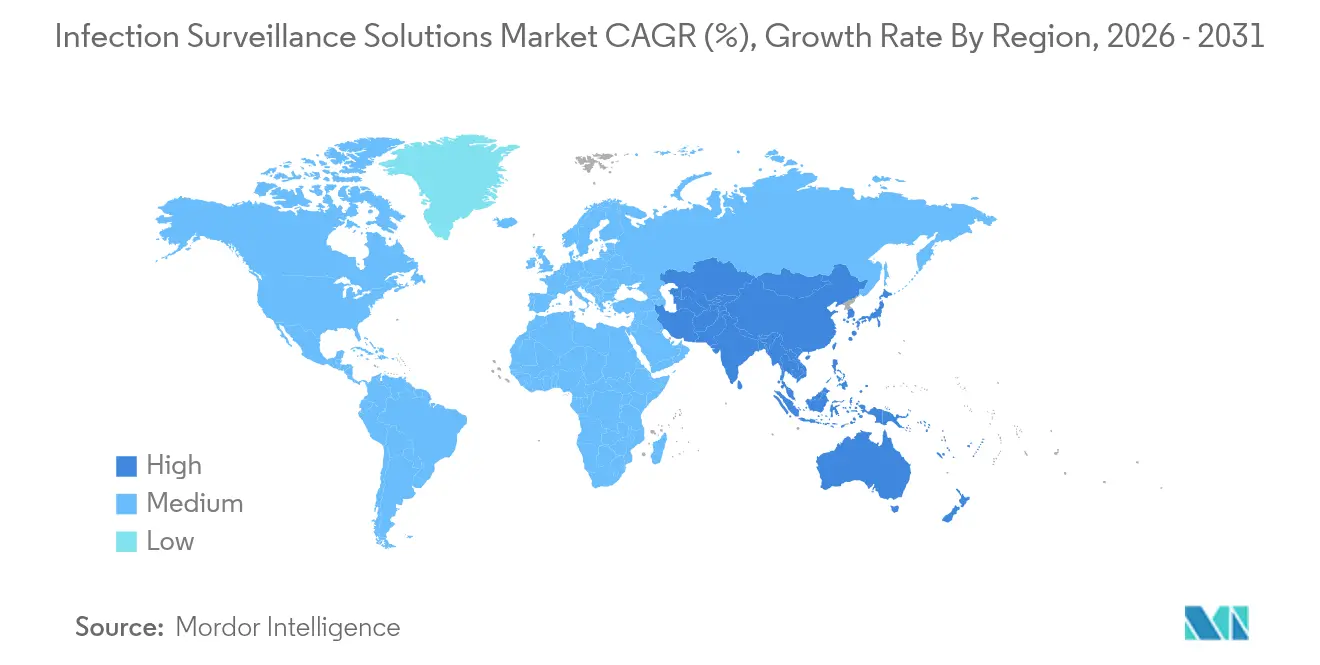

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infection Surveillance Solutions Market Analysis by Mordor Intelligence

The infection surveillance solutions market size is expected to grow from USD 0.91 billion in 2025 to USD 1.03 billion in 2026 and is forecast to reach USD 1.9 billion by 2031 at 13.05% CAGR over 2026-2031. Expansion is propelled by new U.S. and EU rules obligating electronic submission of healthcare-associated infection (HAI) data, tighter value-based reimbursement, and rapid uptake of AI-based early-warning algorithms that cut sepsis detection times. Hospitals accelerate spending to avoid CMS penalties tied to respiratory illness reporting, while smaller facilities gravitate toward cloud subscriptions that trim capital budgets despite lingering cybersecurity fears following the 2024 Change Healthcare breach. Vendors differentiate on interoperability with EHRs, HL7-FHIR readiness, and embedded predictive analytics, and most are layering managed services on top of core software to relieve staffing constraints. Overall, the infection surveillance solutions market benefits from a convergence of regulation, economics, and technology that turns digital surveillance from a “nice-to-have” into mandatory clinical infrastructure.

Key Report Takeaways

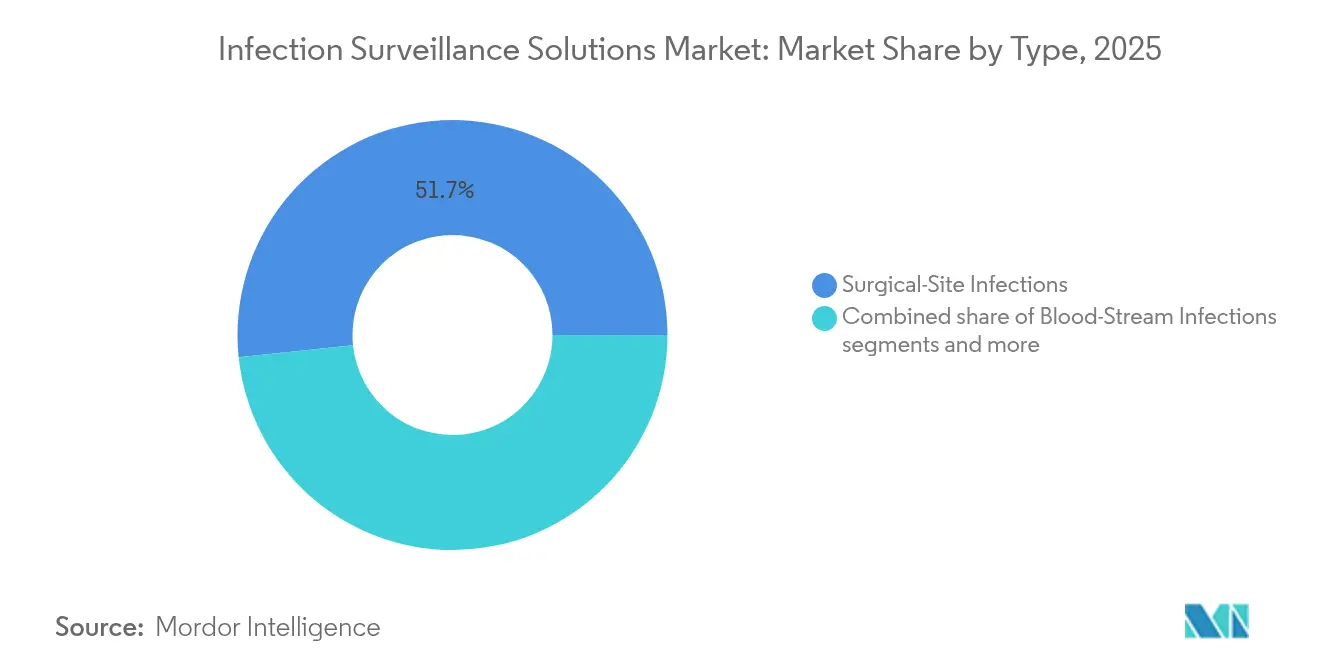

- By infection type, surgical-site infections led with 51.65% of infection surveillance solutions market share in 2025, whereas blood-stream infections are forecast to post the highest 13.45% CAGR through 2031.

- By offering, software accounted for 67.25% of the infection surveillance solutions market size in 2025; services are expanding fastest at 14.2% CAGR to 2031.

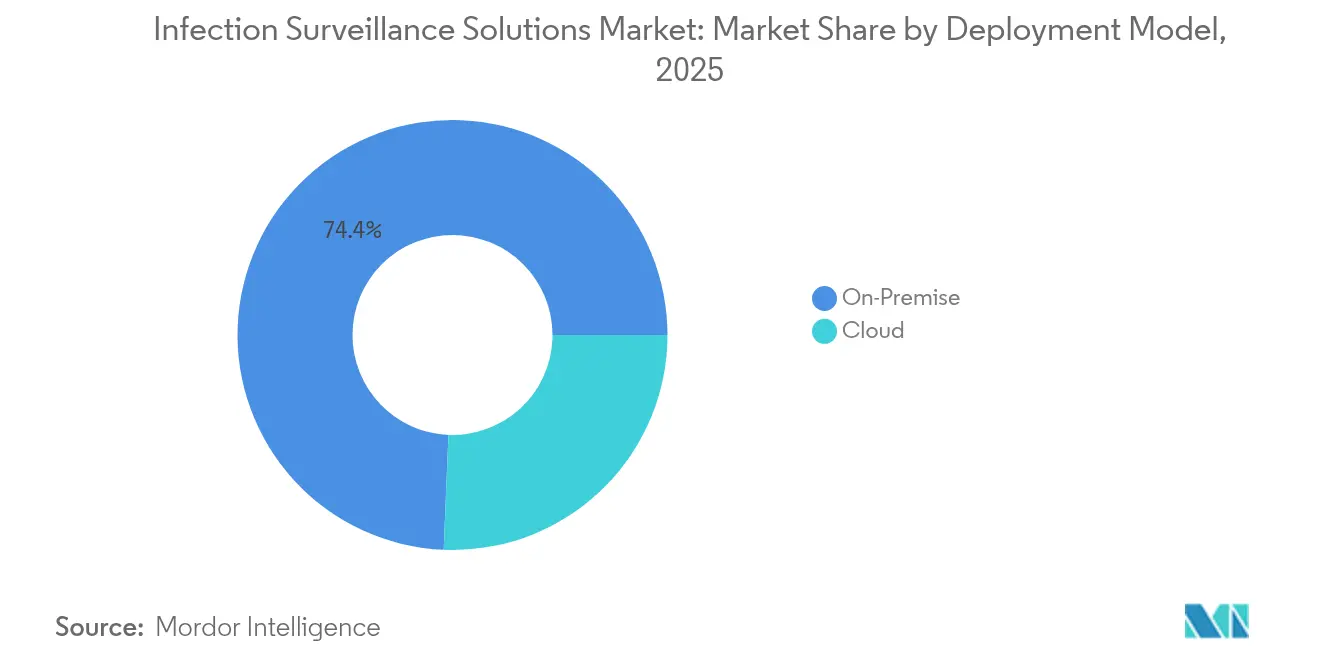

- By deployment model, on-premise platforms held 74.35% share of the infection surveillance solutions market in 2025, while cloud deployments are advancing at a 14.4% CAGR.

- By end user, hospitals commanded 55.70% of 2025 revenue; long-term care facilities are set to grow at 13.9% CAGR through 2031.

- By geography, North America secured 37.60% of 2025 revenue; Asia-Pacific records the sharpest regional CAGR at 13.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Infection Surveillance Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of HAIs and stringent regulation | +2.8% | Global (North America, EU strongest) | Medium term (2-4 years) |

| Government penalties and reimbursement reforms | +2.1% | North America first, expanding into Asia-Pacific | Short term (≤ 2 years) |

| Rapid EHR adoption enabling seamless data feeds | +1.9% | Global, led by developed markets | Medium term (2-4 years) |

| Migration to cloud-based surveillance platforms | +1.7% | Global, accelerating in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| AI-driven predictive analytics for stewardship | +1.4% | North America & EU core, global expansion | Long term (≥ 4 years) |

| Real-time syndromic surveillance capabilities | +1.3% | Global, strongest in pandemic-prone regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of HAIs and Stringent Regulation

Healthcare-associated infections cost U.S. hospitals USD 25-45 billion a year, making surveillance investment an economic imperative. CMS finalized fresh quality measures for catheter-associated UTIs and central-line infections in its FY 2025 rule set, and the European Health Data Space will require standardized infection reporting across 27 member states by 2029[1]European Commission, “European Health Data Space Regulation,” ec.europa.eu. German facilities illustrate the payoff: preventing a single nosocomial episode can avoid 12 added bed-days and generate EUR 390-650 in incremental revenue. As penalties tighten, the infection surveillance solutions market becomes non-discretionary infrastructure.

Government Penalties and Reimbursement Reforms

CMS’s Hospital-Acquired Condition Reduction Program imposes 1% payment cuts on the worst-performing quartile of hospitals, linking revenue directly to infection metrics. New participation rules effective November 2024 extend mandatory weekly respiratory-illness uploads, forcing institutions to automate reporting or forfeit Medicare dollars. Parallel frameworks in Japan attach reimbursement uplifts to certified EHR and surveillance connectivity. The penalty-or-pay dynamic generates predictable demand for infection surveillance solutions market deployments across acute and post-acute settings.

Rapid EHR Adoption Enabling Seamless Data Feeds

Epic added 176 U.S. facilities in 2024, while Oracle Health lost share after Cerner integration issues, underscoring the competitive value of clean data exchange. CDC digital quality measures built on FHIR now accept real-time uploads into the National Healthcare Safety Network, eliminating duplicate manual entry. Asia-Pacific EHR roll-outs grow 7.29% annually, with Japan and China embedding surveillance hooks in national digitization programs. This infrastructure maturity accelerates infection surveillance solutions market penetration because surveillance modules can simply “plug-in” to live clinical feeds.

Migration to Cloud-Based Surveillance Platforms

Cyberattacks on Change Healthcare and Ascension in 2024 rattled confidence, yet subsequent federal proposals earmarking USD 800 million for hospital cybersecurity flipped sentiment toward hardened cloud providers. Cloud platforms cut implementation outlays by up to 60% and auto-scale during outbreaks—a premium feature after COVID-19 strained on-premise servers. EU regulators explicitly endorse certified secure-processing environments under EHDS, giving European buyers legal clarity to move infection data into the cloud.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front costs for smaller facilities | -2.0% | Global, acute in developing and rural markets | Short term (≤ 2 years) |

| Clinical workflow resistance to new IT systems | -1.3% | Global, strongest in traditional health systems | Medium term (2-4 years) |

| Interoperability gaps across disparate standards | -1.1% | Global, especially fragmented healthcare networks | Medium term (2-4 years) |

| Heightened cybersecurity and privacy concerns | -0.8% | Global, most visible in highly regulated jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Costs for Smaller Facilities

Basic EMR deployments still demand USD 13,100 per provider and full-featured surveillance can add USD 50,000 annually—tough numbers for rural hospitals[2]Agency for Healthcare Research and Quality, “Costs and Benefits of Electronic Health Records,” ahrq.gov. Nonetheless, five-year net benefits reach USD 86,400 via avoided HAIs and charge capture. Pending U.S. legislation aims to subsidize rural adoption, while cloud Software-as-a-Service offerings align spend with usage, easing entry into the infection surveillance solutions market.

Clinical Workflow Resistance to New IT Systems

Surveys show 60% of clinicians view tech complexity as the biggest AI barrier, and alert-fatigue remains a risk when surveillance engines over-notify. Best-practice implementations now allocate up to 75% of project budgets to training and change management. Emerging voice-enabled interfaces promise to embed surveillance passively into routine charting, reducing keystrokes and resistance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Surgical-Site Infections Retain the Lead

Surgical-site infections contributed USD 0.47 billion in 2025, representing the largest slice of the infection surveillance solutions market. CMS penalty structures and public reporting keep surgical metrics in executive dashboards, sustaining investment in perioperative surveillance modules. AI-augmented image and vital-sign analyzers now flag wound deterioration within hours, enhancing compliance and trimming readmission risks. In contrast, blood-stream infections generated a smaller base but clock the highest 13.45% CAGR thanks to continuous physiological data streams that feed machine-learning sepsis predictors. The infection surveillance solutions market size for blood-stream monitoring is projected to hit USD 0.44 billion by 2031 as validation studies prove 26% mortality reduction. Other categories such as catheter-associated UTIs and ventilator-associated pneumonia benefit from device usage audits and bedside dashboards that push adherence reminders in real time.

Clinical priority differences steer vendor road maps. Surgical-site modules emphasize operating-room scheduling links and antimicrobial prophylaxis timers, while blood-stream modules pivot around real-time lab cultures and antibiotic stewardship tools. Emerging whole-genome sequencing tie-ins will likely blur boundaries, enabling unified dashboards that overlay pathogen lineage on infection type. Still, hospitals are expected to license separate analytic bundles through 2031, ensuring the infection surveillance solutions market continues to generate type-specific revenue streams.

By Offering: Software Dominance with Services Upshift

Software platforms delivered 67.25% of overall revenue in 2025 and continue to anchor most RFPs due to health systems’ preference for integrated EHR plug-ins. Market leaders invest in low-code configurations so infection-control teams can tweak alert thresholds without programmer support. Yet services revenue rises at a faster 14.2% clip as facilities outsource rule tuning, report generation, and AI model retraining. Managed-service providers package 24/7 monitoring, regulatory updates, and analytics talent, appealing to resource-strained safety-net hospitals. As a result, the infection surveillance solutions market size attributable to services may near USD 0.68 billion by 2031, blurring the classic product-versus-services distinction.

Vendor strategies increasingly bundle outcome-based contracts in which monthly fees flex with performance on HAI benchmarks. That shift moves risk off hospital balance sheets while guaranteeing recurring revenue for suppliers. Expect further migration toward platform-plus-service subscriptions, solidifying long-tail value capture across the infection surveillance solutions market.

By Deployment Model: Cloud Gains Despite On-Premise Majority

On-premise installations still accounted for 74.35% of 2025 revenue as large integrated delivery networks cling to existing data centers and custom interfaces. However, cloud subscriptions grow 14.4% annually, driven by small-to-mid provider adoption and hybrid expansions among enterprise systems seeking disaster-recovery resilience. Providers report 40–60% lower up-front costs and quicker go-lives—often under 90 days—when using multitenant SaaS models. The infection surveillance solutions market share for cloud is forecast to rise beyond 40% by 2031 as regulatory clarity around encrypted processing environments matures.

Cybersecurity remains the sticking point. Vendors now include end-to-end managed security layers, audit trails, and zero-trust segmentation as standard SLAs. These technical assurances, supported by pending federal grants, erode resistance and are expected to tilt procurement decisively toward cloud in the latter half of the forecast window.

By End User: Hospitals Anchor Demand, Long-Term Care Accelerates

Hospitals produced 55.70% of 2025 sales, reflecting tight alignment between inpatient quality penalties and surveillance spend. Tertiary systems deploy enterprise dashboards that correlate hand-hygiene compliance with HAI trends, feeding board-level scorecards. Long-term care facilities, however, register the fastest 13.9% CAGR as CMS extends Enhanced Barrier Precautions and respiratory-pathogen reporting into nursing homes. The infection surveillance solutions market size for long-term care is projected to rise from USD 0.13 billion in 2026 to USD 0.24 billion by 2031.

Ambulatory surgery centers and home-health operators represent emerging niches as procedures migrate outside hospitals. Vendors reacting quickly with lightweight, mobile-first interfaces will capture incremental share given limited IT support in these decentralized settings.

Geography Analysis

North America generated 37.60% of 2025 revenue, underpinned by mandatory NHSN reporting and CMS reimbursement levers that compel every acute-care facility to maintain certified electronic surveillance. Federal rules effective November 2024 now require hospitals to upload weekly COVID-19, influenza, and RSV counts, cementing demand for automated platforms. High-profile AI pilots across leading U.S. IDNs stimulate peer adoption and validate ROI calculations for budget committees.

Asia-Pacific records the highest 13.1% CAGR through 2031 as Japan, China, and South Korea leapfrog legacy architectures with cloud-native deployments. Japan’s super-aged demographics amplify the value proposition for labor-saving surveillance, while China’s top-down digitization funds EHR nodes even in tier-2 cities. Private equity flows into telehealth and hospital-at-home models further expand the infection surveillance solutions market because remote-care workflows still require infection-risk oversight.

Europe advances steadily on the back of the European Health Data Space. EHDS mandates interoperable EHRs and cross-border infection reporting by 2029, a deadline accelerating procurement cycles. Strict GDPR rules elevate demand for platforms with embedded anonymization and secure-processing zones, and wastewater-plus-genomic pilots across 10 EU nations showcase the region’s integrated, multi-modal approach to pathogen monitoring.

Competitive Landscape

The market remains moderately fragmented: top EHR players, diagnostics giants, and niche analytics specialists coexist. Epic leverages its EHR footprint to embed native infection dashboards, gaining integration speed over stand-alone rivals. BD pushes end-to-end pathways by pairing rapid diagnostics with HealthSight analytics, reinforced by recent FDA clearances and a USD 2.5 billion domestic manufacturing program. Wolters Kluwer capitalizes on its clinical knowledge assets, integrating evidence-based content via its 2025 AI Labs initiative to improve model explainability.

Disrupters such as Boston University’s open-source BEACON platform showcase large-language-model surveillance, attracting global health grants that offset commercial scale disadvantages. Meanwhile, Inovalon’s VigiLanz earns #1 KLAS rankings for pharmacy surveillance, underscoring the weight buyers place on peer-validated usability. Mergers and acquisitions activity centers on acquiring AI teams and cloud orchestration tools, suggesting eventual consolidation but no near-term shakeout given diverse buyer preferences and regional compliance idiosyncrasies.

Infection Surveillance Solutions Industry Leaders

IBM Corporation (Truven Health Analytics)

Gojo Industries Inc

VigiLanz Corporation

Cerner Corporation

RL Datix Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BD launched the FACSDiscover A8 Cell Analyzer featuring spectral, real-time imaging for 50+ biomarkers, improving infection research throughput.

- May 2025: BD reported Q2 FY 2025 revenue of USD 5.3 billion and announced USD 2.5 billion U.S. manufacturing investments alongside FDA clearance of an integrated antimicrobial-resistance diagnostic.

- March 2025: Epic unveiled agentic AI with 125 generative features; 66% of providers cite administrative time savings.

- March 2025: Wolters Kluwer introduced AI Labs powered by UpToDate across 100 hospitals, prioritizing validated clinical content in generative AI.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the infection-surveillance-solutions market as the global sale of purpose-built software platforms and connected professional services that continuously capture, analyze, and alert on clinical, laboratory, and administrative data to prevent, detect, and report healthcare-associated infections (HAIs) across inpatient and long-term-care settings.

Scope exclusion: single-function hand-hygiene counters, standalone sterilization equipment, and any outsourced infection-control services not bundled with surveillance analytics have been kept outside the model.

Segmentation Overview

- By Type

- Surgical-Site Infections

- Blood-Stream Infections

- Catheter-Associated UTIs

- Ventilator-Associated Pneumonia

- By Offering

- Software

- Services

- By Deployment Model

- On-Premise

- Cloud

- By End User

- Hospitals

- Long-term Care Facilities

- Ambulatory Surgery Centers

- Public-Health and Reference Labs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured interviews with infection-prevention nurses, hospital CIOs, surveillance-software product leads, and regional health-authority officials across North America, Europe, Asia-Pacific, and the GCC. Insights on average license fees, deployment timelines, and reporting pain points helped refine adoption curves and verify desk-based assumptions.

Desk Research

Mordor analysts began with authoritative datasets such as CDC-NHSN dashboards, WHO GLASS alerts, OECD Health Statistics, Eurostat hospital activity files, and peer-reviewed work in the Journal of Hospital Infection, which frame global HAI burden and reporting mandates. Company 10-Ks, CMS HAC penalty tables, regional procurement portals, and D&B Hoovers financials filled gaps on vendor revenue streams and hospital digitization budgets. Supplementary inputs from Dow Jones Factiva news flow and Questel patent counts signaled emerging technology traction. The sources listed here illustrate the caliber of references consulted; many additional public and proprietary materials were reviewed before numbers were finalized.

Market-Sizing & Forecasting

A blended top-down and bottom-up logic is followed. Starting from hospital and long-term-care bed stocks by country, HAI incidence rates, and mandatory reporting coverage, the team sized the total addressable demand pool, then applied region-specific surveillance-software penetration and average annual subscription values. Selective bottom-up checks, supplier revenue roll-ups, channel partner quotes, and sampled contract values were used to corroborate totals. Key model drivers include inpatient surgical volume, cloud-IT spend per bed, EHR integration rates, regulatory penalty intensity, and median software ASPs. Projections out to 2030 employ multivariate regression supported by ARIMA smoothing, with scenario adjustments validated by our primary respondents. Gap areas in bottom-up inputs (e.g., private-hospital contracts in developing markets) were bridged through conservative interpolation anchored to comparable public facilities.

Data Validation & Update Cycle

Outputs run through automated variance screening, senior-analyst peer review, and a sign-off meeting before publication. Models refresh annually; interim updates are triggered when sentinel variables, regulatory mandates, major vendor mergers, or >5% swing in quarterly vendor revenue shift materially.

Why Our Infection Surveillance Solutions Baseline Commands Reliability

Published figures often diverge because firms choose different infection definitions, pricing bundles, and refresh cadences. According to Mordor Intelligence, our disciplined scope selection and yearly recalibration keep users grounded in reality.

Key gap drivers arise when others bundle sterilization hardware, assume uniform cloud pricing, or extrapolate five-year hospital counts without verifying bed closures. Our model, in contrast, filters non-analytics revenue, applies tiered ASP ladders, and revisits the facility universe each cycle, thereby moderating extremes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.91 B (2025) | Mordor Intelligence | - |

| USD 0.71 B (2024) | Global Consultancy A | Excludes long-term-care facilities and uses uniform software pricing |

| USD 0.58 B (2022) | Industry Journal B | Counts only on-premise licenses and relies on outdated HAI incidence rates |

In sum, the variance review shows that Mordor's transparent variable set, bi-modal sizing logic, and brisk refresh cycle deliver a balanced, decision-ready baseline that market participants can trust.

Key Questions Answered in the Report

What is the current size of the infection surveillance solutions market?

It totals USD 1.03 billion in 2026 and is on course to reach USD 1.9 billion by 2031 at a 13.05% CAGR.

Which infection type generates the most demand for surveillance software?

Surgical-site infections account for 51.65% of 2025 revenue due to stringent CMS quality mandates.

Are cloud-based deployments surpassing on-premise systems?

Not yet; on-premise still holds 74.35% share, but cloud platforms are the fastest-growing segment at a 14.4% CAGR.

Why are long-term care facilities suddenly investing in surveillance?

CMS expanded Enhanced Barrier Precautions and respiratory-pathogen reporting to nursing homes, driving a 13.9% CAGR for this segment.

How does AI improve infection surveillance outcomes?

AI-equipped platforms cut sepsis detection times by hours, boost charting accuracy 55%, and can yield USD 18.74 in benefits for every dollar invested through prevented infections.

Which region will see the quickest adoption through 2031?

Asia-Pacific leads in growth at a 13.1% CAGR as Japan and China fund cloud-native, AI-ready surveillance infrastructure.

Page last updated on: