Sodium Sulfur Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 0.33 Billion |

| Market Size (2030) | USD 1.12 Billion |

| Growth Rate (2025 - 2030) | 27.25% CAGR |

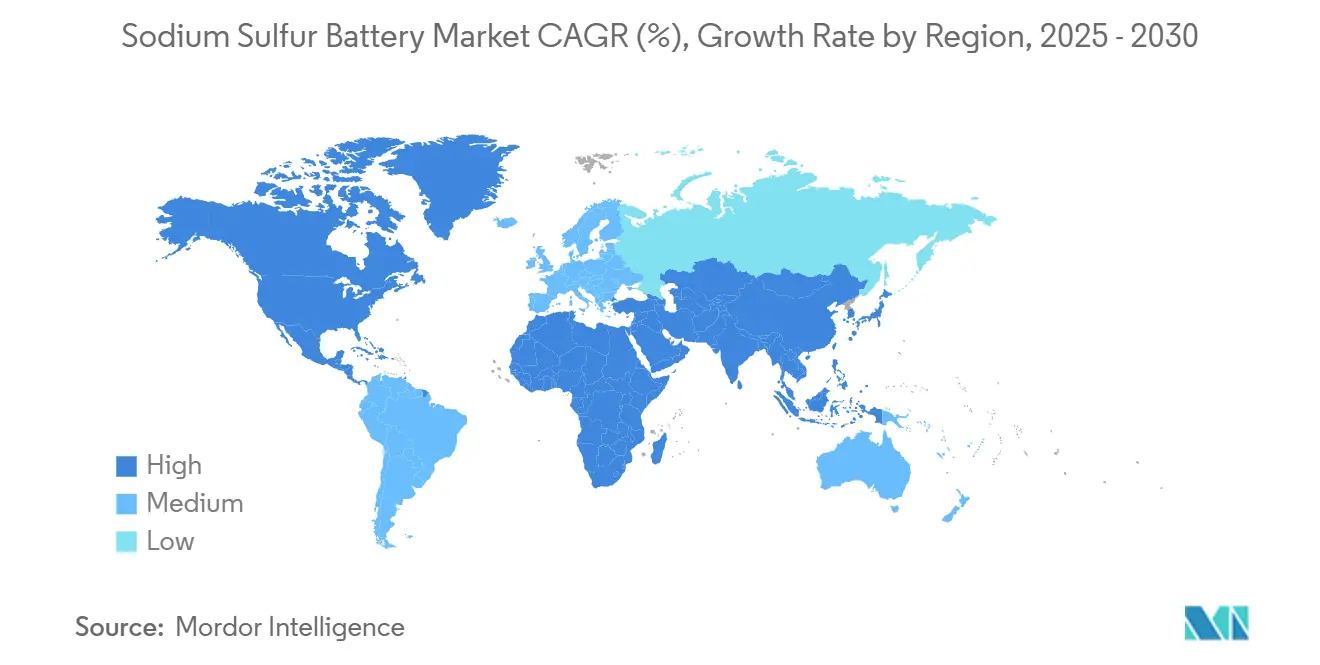

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

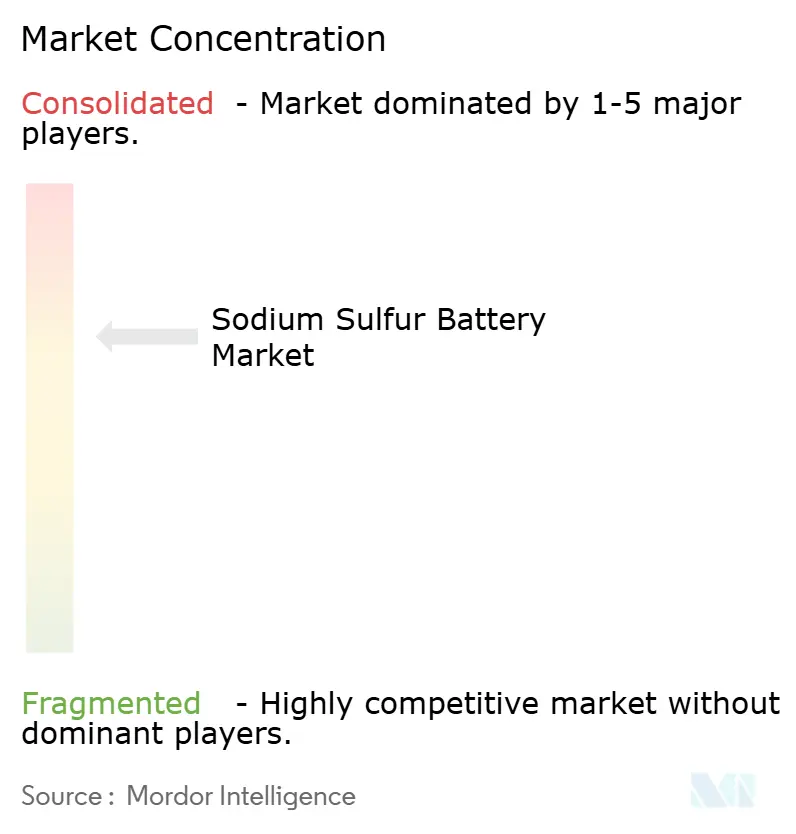

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sodium Sulfur Battery Market Analysis by Mordor Intelligence

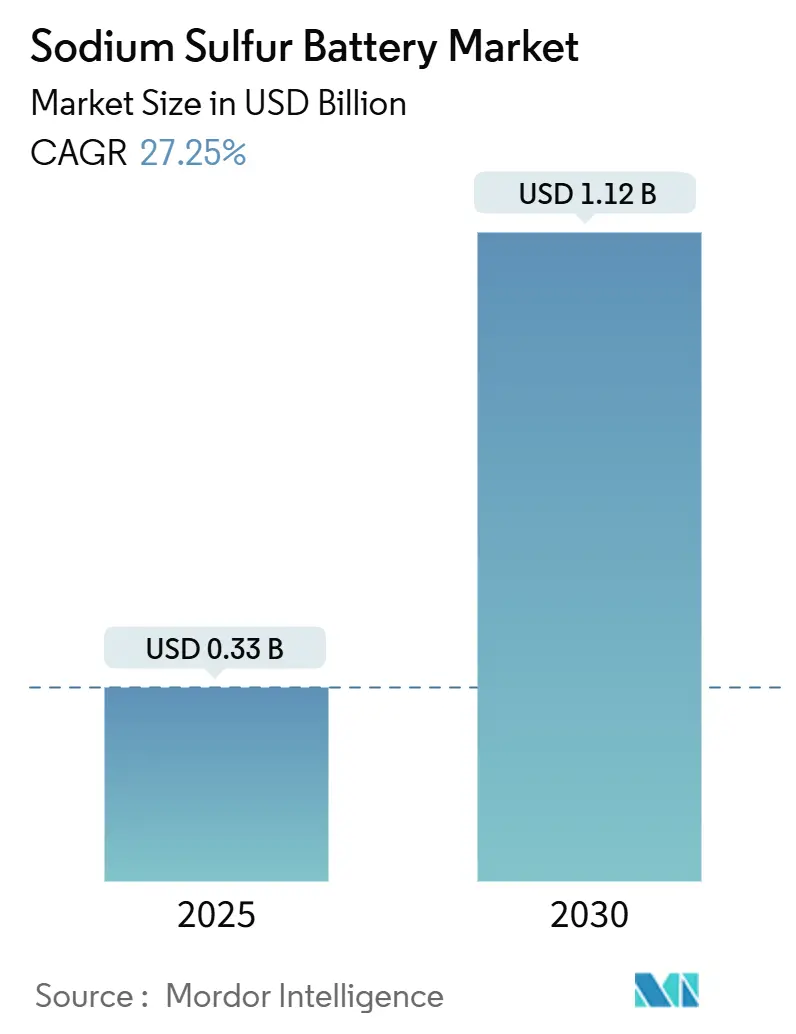

The Sodium Sulfur Battery Market size is estimated at USD 0.33 billion in 2025, and is expected to reach USD 1.12 billion by 2030, at a CAGR of 27.25% during the forecast period (2025-2030).

Policy incentives, grid-hardening needs, and the shift toward long-duration energy storage solutions exceeding 6 hours underpin this growth. Utilities are replacing lithium-ion systems for multi-hour discharge duties, while manufacturers are standardising containerised modules to shorten project timelines. Regional demand is led by Asia-Pacific owing to Japan’s established NaS base, but North America is closing the gap as the Inflation Reduction Act channels tax credits toward non-lithium chemistries. Competitive intensity remains moderate: NGK Insulators retains a strong installed base, yet BASF’s new modules claim 20% cost cuts, prompting wider adoption in commercial and industrial (C&I) applications.

Key Report Takeaways

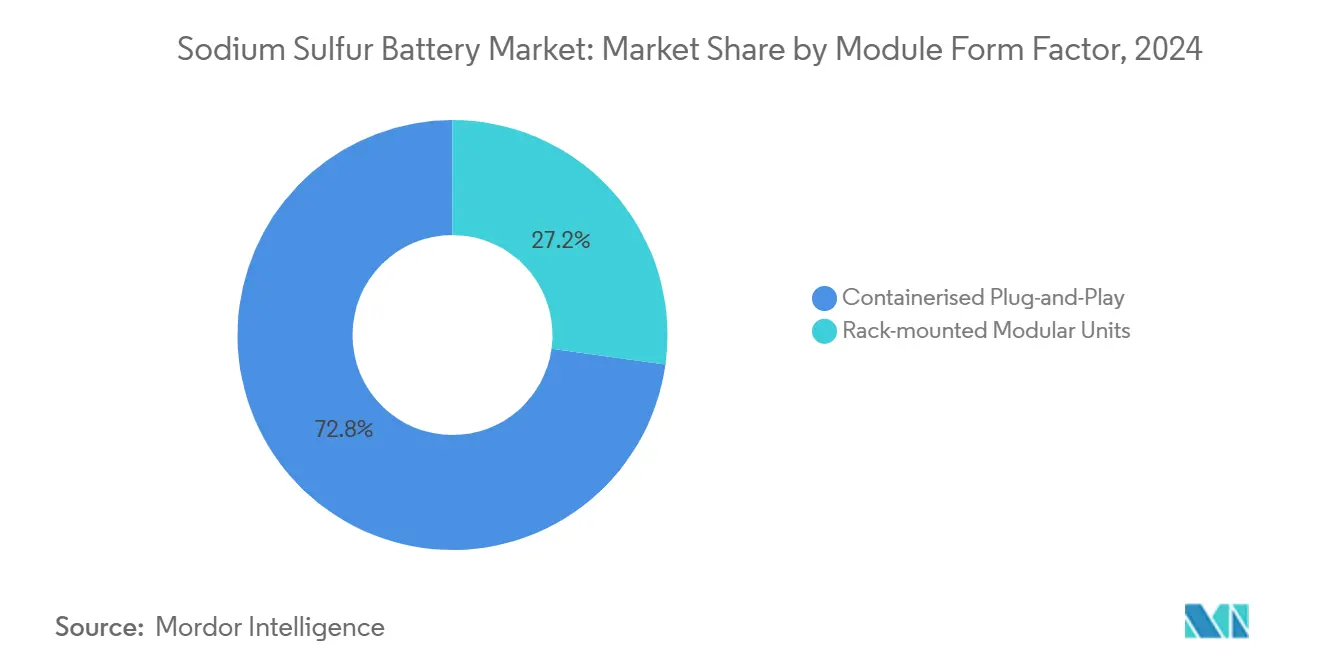

- By module form factor, containerised plug-and-play systems held 72.8% of the sodium sulfur battery market share in 2024, while rack-mounted units are forecast to advance at a 31.5% CAGR to 2030.

- By capacity range, systems above 500 kWh captured 61.2% of the sodium sulfur battery market size in 2024; the 100-500 kWh band posts the quickest expansion at 37.6% CAGR through 2030.

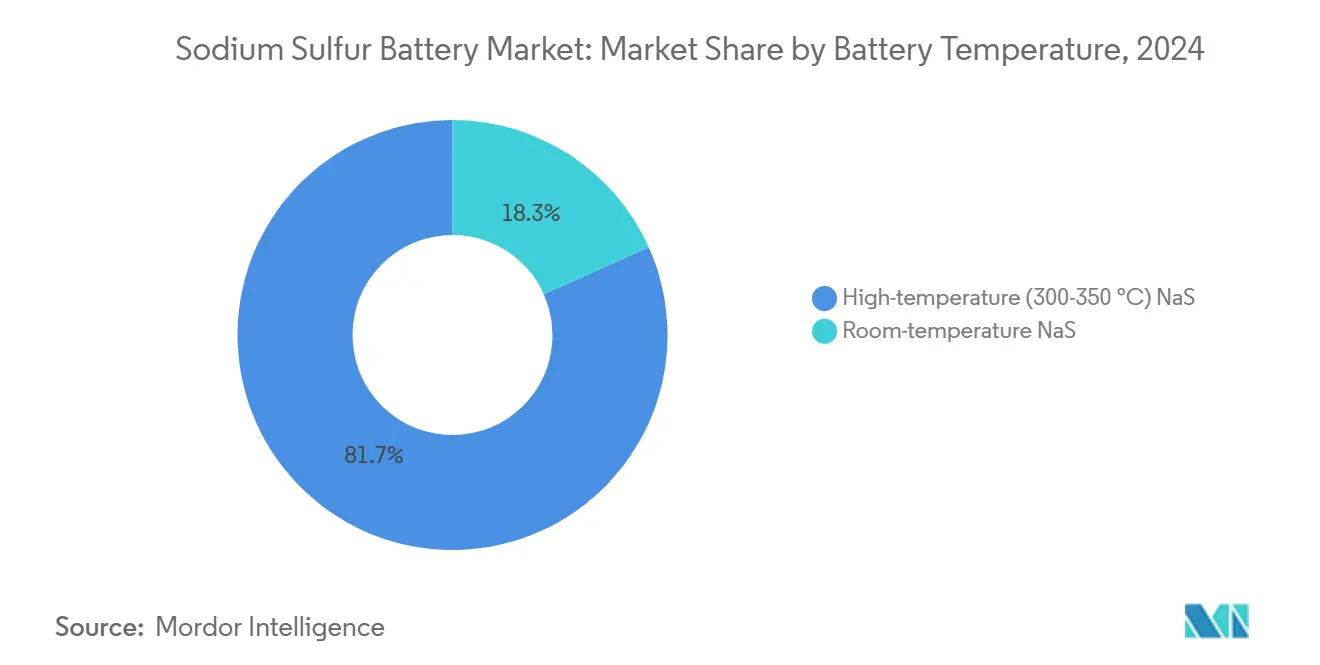

- By battery temperature, high-temperature NaS technology accounted for 81.7% market share in 2024, while room-temperature variants are projected to grow at a 32.8% CAGR by 2030.

- By installation type, grid-scale projects above 10 MWh commanded a 59.4% share in 2024; C&I installations between 0.5–10 MWh show the fastest pace at 34.9% CAGR toward 2030.

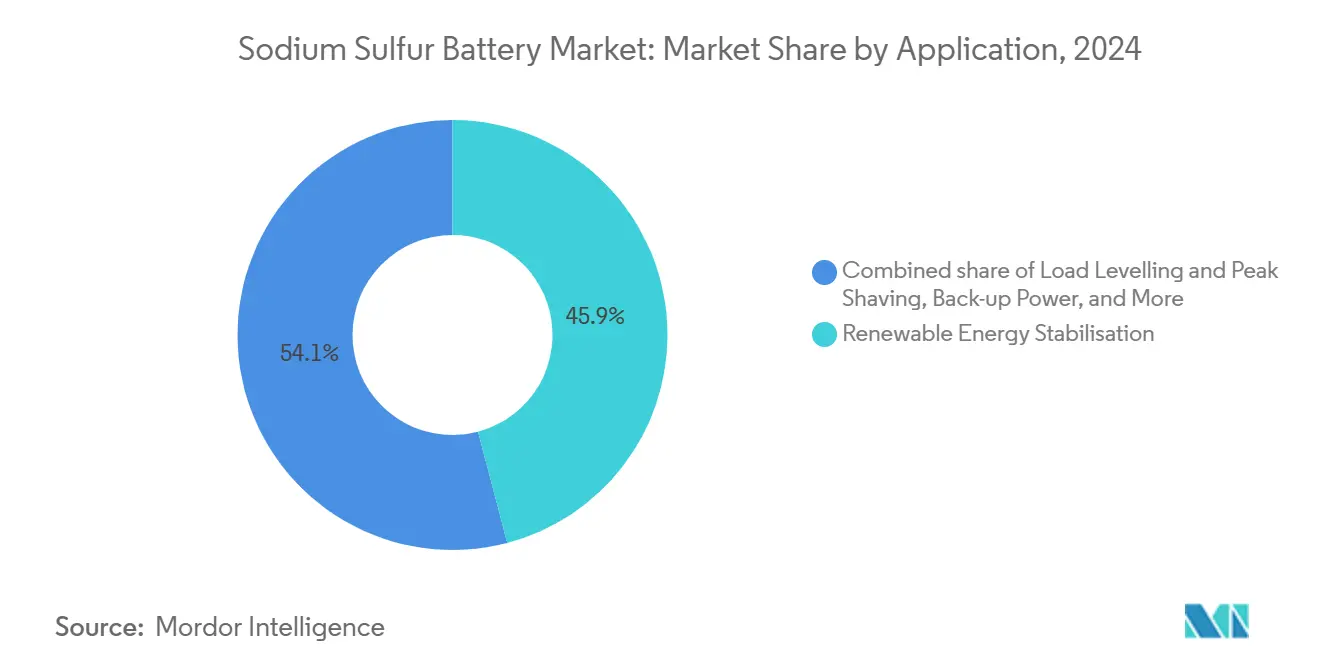

- By application, renewable-energy stabilisation represented 45.9% of total demand in 2024; load-levelling and peak-shaving uses register the highest forecast CAGR at 33.7% through 2030.

- By geography, Asia-Pacific accounted for the largest share, 42.3% in 2024, while North America is likely to grow the fastest, at a CAGR of 39.2% through 2030.

- NGK Insulators, BASF, and Wärtsilä collectively held just over 70% of global capacity additions in 2024, highlighting a concentrated supplier mix.

Global Sodium Sulfur Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid build-out of long-duration energy-storage tenders (≥6 h) | +8.50% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Declining $/kWh versus Li-ion in 4-hour-plus applications | +6.20% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Favourable policy incentives for non-Li chemistries (e.g., U.S. IRA bonus credits) | +4.80% | North America, with EU following similar frameworks | Medium term (2-4 years) |

| Grid-hardening needs in typhoon-/wild-fire-prone regions | +3.70% | APAC (Japan, Philippines), North America (California, Texas) | Long term (≥ 4 years) |

| Industrial by-product sodium & sulfur streams lowering feed-stock costs | +2.10% | Global, with advantages in industrial regions | Long term (≥ 4 years) |

| Repurposing idle alumina-smelter sites as NaS module plants | +1.20% | Australia, Middle East, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Build-out of Long-Duration Energy-Storage Tenders (≥6 h)

Utility procurement is shifting toward solutions that can deliver six or more hours of discharge, positioning the sodium sulfur battery market as a preferred option for emerging long-duration energy-storage projects. The U.S. Department of Energy targets a 90% cost reduction in long-duration storage by 2030, and sodium-based systems are projected to deliver levelised costs below USD 0.280 per kWh, compared with USD 0.553 per kWh in 2024. Orders such as NGK’s 230 MWh installation for a German green-hydrogen project illustrate how extended discharge ability secures premium contracts. California assessments suggest 100-hour storage could capture a tenth of the state market if costs remain competitive with lithium-ion solutions.(1)Source: California Energy Commission, “Long-Duration Energy Storage Assessment,” cec.ca.gov These developments are reshaping grid-planning models that once centred on four-hour lithium-ion assets, and they elevate sodium sulfur technology where energy duration trumps power density.

Declining $/kWh versus Li-ion in 4-hour-plus Applications

Economics are pivotal: BASF’s newest containerised NaS modules shave 20% off prior costs, placing system prices in the USD 250–300 per kWh bracket that competes directly with lithium iron phosphate offerings. Cost curves continue to benefit from industrial by-product sodium and sulfur streams that lessen exposure to volatile lithium prices.(2)Source: Chemical & Engineering News, “Sodium and Sulfur Feedstocks,” cen.acs.org Forschungszentrum Jülich trials revealed energy densities of 280 Wh/kg, closing the performance gap with lithium-ion while maintaining material-cost advantages. As manufacturing scales and beta-alumina production efficiency improve, the crossover point at which NaS systems undercut lithium-ion on total ownership cost inches toward even shorter durations.

Favourable Policy Incentives for Non-Li Chemistries (e.g., U.S. IRA bonus credits)

The Inflation Reduction Act grants production tax credits of up to USD 45 per kWh for domestically manufactured cells, propelling a trebling U.S. energy-storage development pipeline since 2023. Complementary investment tax credits reward projects that meet domestic-content thresholds, benefitting the sodium sulfur battery industry, which relies on abundant local feedstocks rather than imported lithium. Europe mirrors this push: the EU Batteries Regulation calls for supply-chain diversification, boosting developer interest in NaS installations. Japan has formalised solid-electrolyte development as a critical industry, ensuring research funding continues for NaS-related materials.

Grid-hardening Needs in Typhoon-/Wild-fire-prone Regions

Extreme weather drives demand for long-duration, thermally robust storage. Studies on typhoon impacts in Japan show repeated outages encouraging utilities to seek high-temperature-tolerant batteries. California’s grid-hardening blueprint prioritises storage capable of safe operation in elevated ambient temperatures, where NaS chemistry avoids the thermal runaway risk associated with lithium-ion. Microgrid pilots in high-risk regions have demonstrated over 50 hours of autonomy during outages, reinforcing NaS suitability for critical infrastructure. Large-scale projects such as Saudi Arabia’s 2.5 GW energy-storage programme underscore this resilience-driven demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety codes limiting high-temperature installations in dense urban zones | -4.30% | North America & EU urban centers | Short term (≤ 2 years) |

| Fragility of β-alumina solid electrolyte tubes | -3.80% | Global manufacturing and deployment | Medium term (2-4 years) |

| Accelerating cost downs in LiFePO₄ & sodium-ion alternatives | -5.20% | Global, with APAC leading cost reductions | Short term (≤ 2 years) |

| Scarcity of insurance underwriting for molten-salt systems | -2.10% | North America & EU regulatory environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety Codes Limiting High-Temperature installations in Dense Urban Zones

Regulations such as U.S. 49 CFR 173.189 impose stringent transport and installation conditions on molten-salt batteries, necessitating hermetic sealing and fire-suppression provisions that hinder rooftop or basement siting.(3)Source: Electronic Code of Federal Regulations, “49 CFR 173.189,” ecfr.gov European directives similarly restrict high-temperature storage near occupied structures, limiting NaS uptake in space-constrained cities. As urban renewables targets rise, these codes divert demand toward lithium-ion or emerging solid-state chemistries, constraining near-term NaS penetration until room-temperature designs mature.

Fragility of β-alumina Solid Electrolyte Tubes

Mechanical cracks and dendrite penetration remain leading failure modes. Research in Electrochimica Acta shows that minor impedance rises may precede catastrophic tube fracture, demanding stringent quality control. Manufacturing yields, therefore, affect reliability perceptions and warranty costs. Composite-electrolyte approaches under study aim to enhance toughness, but commercial roll-out is still two to three years away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Form Factor: Containerised Systems Drive Market Standardization

Containerised modules captured the bulk of demand in 2024, reflecting a clear preference for factory-assembled, ISO-compliant units that streamline shipping and commissioning. Grid operators recognise that containerised designs bundle thermal management and fire-suppression subsystems, reducing engineering lead times and smoothing regulatory approvals. Although smaller in volume, Rack-mounted units grew briskly as C&I clients adopted flexible designs that slot into existing equipment rooms. This expansion at a 31.5% CAGR widens the sodium sulfur battery market as integrators address space-restricted industrial sites without resorting to bespoke builds. Manufacturers highlight that containerised layouts cut project schedules by up to three months, a decisive factor for developers chasing incentive deadlines.

By Capacity Range: Large-Scale Dominance with Mid-Range Momentum

Systems exceeding 500 kWh governed over half of 2024 deployments, yet the 100-500 kWh category posted the sharpest growth through 2030. Utility procurement drove the top tier as state-level tenders in Germany and Saudi Arabia prioritised multi-megawatt hours per site. Mid-range uptake rose in distribution-level grid reinforcement, where operators need extended discharge without the land footprint of traditional peaker plants. This pattern underscores the sodium sulfur battery market size concentration in high-value projects, signalling diversification into industrial load-shifting and microgrid roles. As mid-range installations approach economies of scale, integrators expect turnkey costs to align more closely with lithium iron phosphate benchmarks, elevating total addressable demand.

By Battery Temperature Type: High-Temperature Systems Remain Predominant

Operating at 300–350 °C, high-temperature NaS technology maintained an 81.7% share in 2024. Utilities value its established track record of over 20 years and millions of cumulative cycles. Room-temperature prototypes are gaining traction, aided by solid-electrolyte breakthroughs that resolve historical cycle-life shortfalls. Projects piloted by European research consortia have shown 81% capacity retention after 200 cycles, advancing commercial readiness. Should room-temperature designs reach parity on durability and cost, they will unlock dense-urban opportunities currently blocked by fire codes. Until then, the sodium sulfur battery market continues to lean on proven high-temperature platforms for bankable revenue streams.

By Installation Type: Grid-Scale Projects Lead, C&I Gains Ground

Grid-scale facilities above 10 MWh accounted for 59.4% of revenue in 2024, benefiting from policy-driven procurements and bulk-purchase economies. However, C&I projects between 0.5–10 MWh are climbing fastest as factories, data centres, and campuses seek multi-hour resilience without diesel generators. These customers prize NaS batteries’ long cycle life and limited degradation at partial-state-of-charge, factors that lower lifetime operating expenditure. Residential and community microgrids remain marginal because unit costs still favour lithium iron phosphate at kilowatt-scale power levels. Future cost reductions and room-temperature offerings could expand NaS relevance in this segment.

By Application: Renewable-Energy Stabilisation Remains Core

Almost half of 2024 shipments addressed renewable-energy stabilisation, highlighting NaS batteries' vital role in balancing wind and solar variability. Load-levelling and peak-shaving uses now represent the fastest-growing slice, spurred by tariff structures that reward off-peak charging and on-peak discharge. Backup power and defence microgrids form a steady but smaller niche, using NaS technology to guarantee mission-critical uptime in remote locales. Collectively, these patterns confirm the sodium sulfur battery market’s orientation toward duties where discharge duration and cycle endurance outweigh sheer energy density.

Geography Analysis

Asia-Pacific retained a 42.3% market share in 2024, with Japan’s mature install base and China’s scale-up incentives driving volume. Projects like Hubei’s 200 MWh Na-ion storage plant showcase Beijing’s wider strategy to lessen reliance on imported lithium, complementing NaS efforts and feeding component supply chains. South Korea and Southeast Asian states are following with pilot programmes that integrate NaS units into existing diesel grids, extending renewables adoption targets without overhauling network infrastructure. Australia’s alumina-smelter conversions further cement the region’s manufacturing proposition.

North America is the fastest riser, set for a 39.2% CAGR through 2030 thanks to federal tax credits and wildfire resilience mandates. California’s legislated storage goals and Texas grid stability plans form bookends of state-level support. Utilities like Duke Energy have begun piloting Japanese-built NaS modules, signalling cross-regional technology flows that shorten learning curves. Canada’s hydro-rich provinces evaluate NaS to manage seasonal surpluses, while Mexico allows NaS to flatten solar output peaks linked to its fast-growing PV base.

Europe maintains steady growth centred on energy security and industrial decarbonisation. Germany’s 230 MWh hydrogen-linked order positions NaS in the continent’s green-molecules push. The UK’s Energy Act 2023 opened merchant-revenue routes for storage, drawing interest in NaS for capacity-market participation. France and Italy are commissioning feasibility studies focused on integrating NaS into legacy gas-fired assets to smooth retirement timetables. Eastern Europe, led by Hungary’s 4.35 MWh demonstration, illustrates how smaller grids leverage NaS to stabilise renewable influx without expanding interconnector capacity.

Competitive Landscape

NGK Insulators anchors the sodium sulfur battery market with over 250 operating sites and proprietary beta-alumina production know-how. Its long operating record eases bankability concerns, giving the firm a first-mover edge. BASF’s entry in 2024 injected fresh price discipline, claiming 20% cost savings through modular container integration. Wärtsilä, Fluence, and Saft explore hybrid configurations that blend NaS with lithium iron phosphate to cover power and energy services in single installations. Materials suppliers such as Idemitsu and Sumitomo Chemical are racing to commercialise tougher solid electrolytes, signalling upstream diversification.

Strategic moves since 2024 include NGK expanding into Eastern Europe, BASF scaling a second NaS production line in Germany, and Wärtsilä winning a 300 MW Scottish project using high-energy modules. Partnerships between utilities and NaS makers have tightened: Duke Energy’s procurement from NGK demonstrates cross-border collaboration, while Saudi grid operators have signed framework agreements for multi-gigawatt NaS portfolios. Venture capital funding flows toward room-temperature NaS start-ups, reflecting investor belief that urban safety upgrades represent the next unlock for addressable market expansion.

Future competition may pivot on electrolyte breakthroughs and manufacturing localisation. Should room-temperature designs commercialise by 2027, a new wave of entrants could erode NGK’s lead. Until then, market concentration continues to favour incumbents with proven field data and vertically integrated component supply.

Sodium Sulfur Battery Industry Leaders

NGK Insulators Ltd.

BASF SE

Contemporary Amperex Technology Ltd (CATL)

Mitsubishi Heavy Industries, Ltd.

Sumitomo Electric Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NGK sodium-sulfur batteries deployed at 70MWh Japan project, picked for pilot by US utility Duke Energy. NGK’s sodium-sulfur (NAS) battery is one of the most commercially mature non-lithium electrochemical technologies for grid-scale energy storage applications.

- January 2025: Researchers at Fujian Normal University reported a dual-salt quasi-solid polymer electrolyte retaining 81% capacity after 200 cycles, supporting room-temperature NaS viability.

- June 2024: BASF, in collaboration with NGK, has unveiled the NAS MODEL L24, an upgraded sodium-sulfur (NaS) battery system that achieves a 20% reduction in cost of ownership compared to previous models. This next-generation system is designed for medium- to long-duration energy storage (LDES) applications, typically requiring 6 hours or more storage.

- April 2024: NGK Insulators secured a contract to supply NAS batteries with a total capacity exceeding 230 MWh for a German green hydrogen project being developed by HH2E along the Baltic Sea coast.

Global Sodium Sulfur Battery Market Report Scope

The sodium sulfur battery market report includes:

| Containerised Plug-and-Play |

| Rack-mounted Modular Units |

| Below 100 kWh |

| 100 to 500 kWh |

| Above 500 kWh |

| High-temperature (300-350 °C) NaS |

| Room-temperature NaS |

| Grid-scale (Above 10 MWh) |

| Commercial and Industrial (0.5 to 10 MWh) |

| Residential/Community Micro-grids (Below 0.5 MWh) |

| Renewable Energy Stabilisation |

| Back-up Power |

| Load Levelling and Peak Shaving |

| Defence and Remote Micro-grids |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Module Form Factor | Containerised Plug-and-Play | |

| Rack-mounted Modular Units | ||

| By Capacity Range | Below 100 kWh | |

| 100 to 500 kWh | ||

| Above 500 kWh | ||

| By Battery Temperature Type | High-temperature (300-350 °C) NaS | |

| Room-temperature NaS | ||

| By Installation Type | Grid-scale (Above 10 MWh) | |

| Commercial and Industrial (0.5 to 10 MWh) | ||

| Residential/Community Micro-grids (Below 0.5 MWh) | ||

| By Application | Renewable Energy Stabilisation | |

| Back-up Power | ||

| Load Levelling and Peak Shaving | ||

| Defence and Remote Micro-grids | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving rapid growth in the sodium sulfur battery market?

Utilities need storage capable of six-hour or longer discharge, and government tax credits favour non-lithium chemistries, lifting demand at a 27.25% CAGR through 2030.

How large will the sodium sulfur battery market be by 2030?

Forecasts indicate USD 1.117.22 million in annual revenue by 2030, up from USD 334.85 million in 2025.

Why are containerised modules so popular?

Standard ISO containers arrive factory-tested with integrated thermal control, cutting project timelines and making up 72.8% of 2024 shipments.

Which region is expanding the fastest?

North America posts the highest growth rate at 39.2% CAGR, helped by the Inflation Reduction Act’s production credits.

Are room-temperature sodium sulfur batteries commercially ready?

Prototype cells show promising durability, but large-scale commercial adoption is expected toward the end of the decade as solid-electrolyte toughness improves.

How do sodium sulfur batteries compare with lithium iron phosphate on cost?

Next-generation NaS systems target USD 250–300 per kWh, rivaling LiFePO₄ for applications that need more than four hours of discharge.

Page last updated on: