Smart Baggage Handling System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

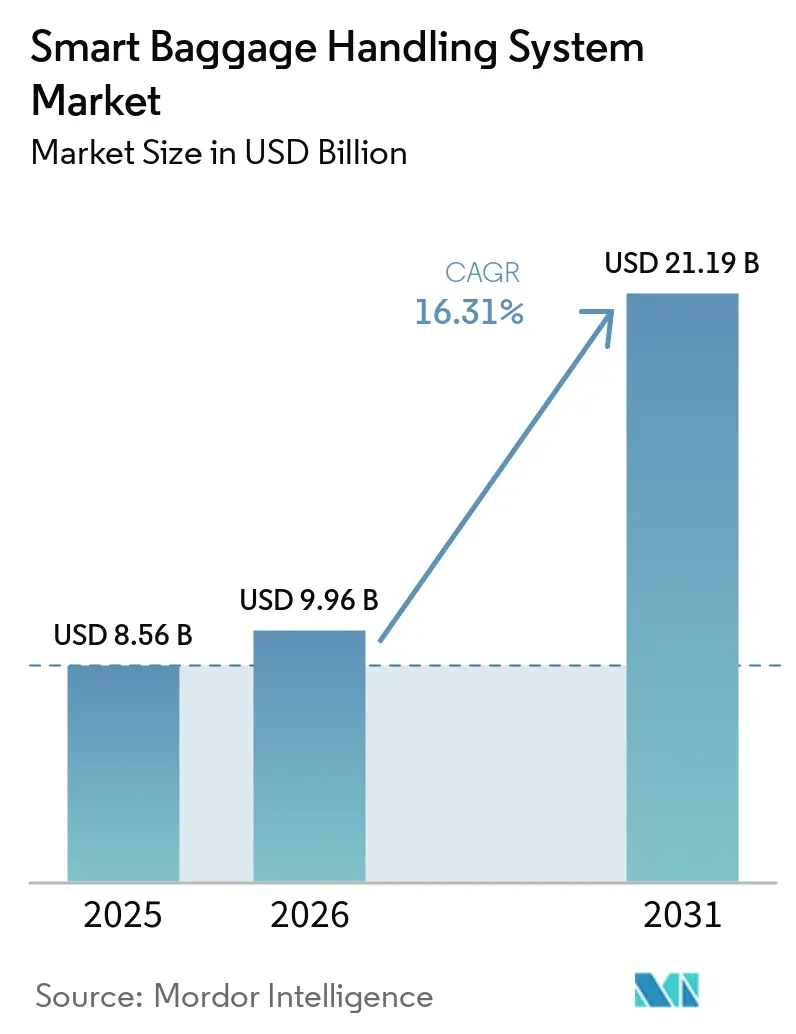

| Market Size (2026) | USD 9.96 Billion |

| Market Size (2031) | USD 21.19 Billion |

| Growth Rate (2026 - 2031) | 16.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Baggage Handling System Market Analysis by Mordor Intelligence

The Smart Baggage Handling System market size was valued at USD 8.56 billion in 2025 and estimated to grow from USD 9.96 billion in 2026 to reach USD 21.19 billion by 2031, at a CAGR of 16.31% during the forecast period (2026-2031). Passenger growth, stricter compliance with IATA Resolution 753, and airport operators’ pivot toward data-driven orchestration are accelerating investment decisions. Procurement teams now rank software-defined control platforms ahead of conveyor horsepower, because predictive analytics demonstrably cut mishandling and compensation costs. Greenfield mega-hubs in Asia-Pacific and the Middle East are embedding fully autonomous networks from day one, while legacy hubs in North America and Europe are layering RFID and ultra-wideband tracking onto barcode foundations to preserve sunk infrastructure. System integrators able to bundle hardware, software, and multi-year maintenance contracts are capturing disproportionate share as airports seek turnkey execution.

Key Report Takeaways

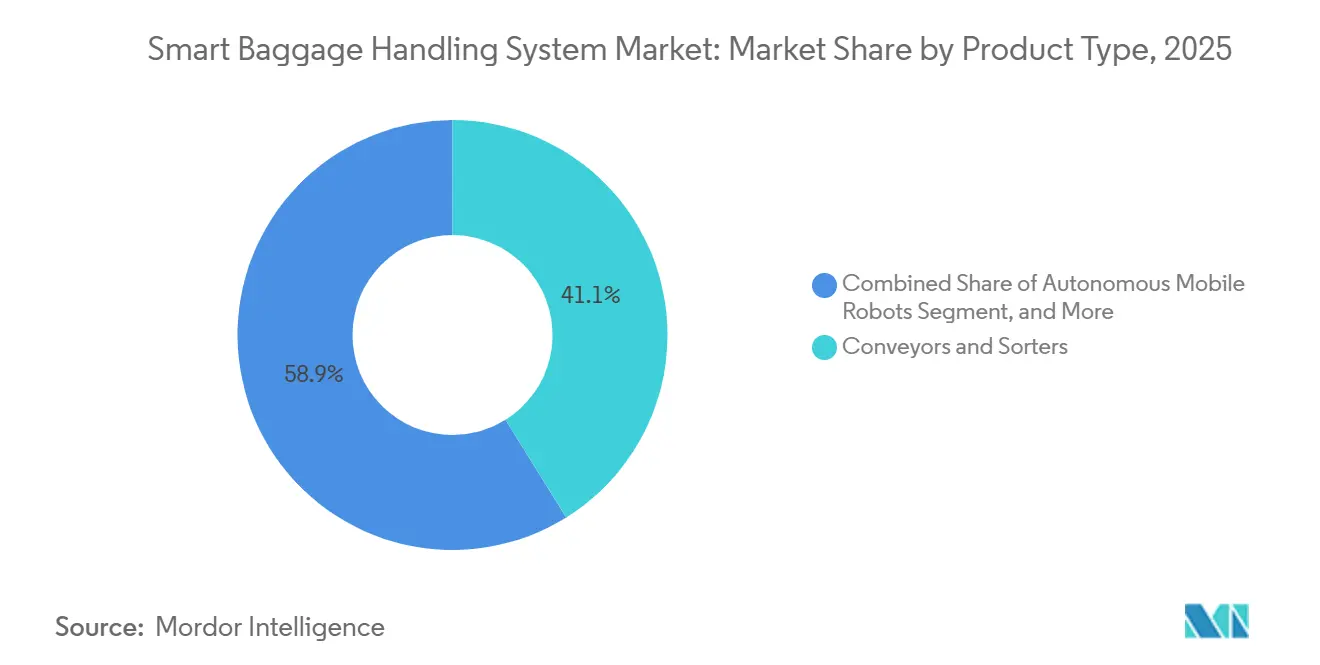

- By product type, conveyors and sorters led with 41.13% of the Smart Baggage Handling System market share in 2025, whereas autonomous mobile robots are the fastest-growing product, expanding at a 17.11% CAGR through 2031.

- By solution, checked-baggage reconciliation systems commanded 36.32% of 2025 revenue, while real-time tracking is projected to record a 17.09% CAGR through 2031.

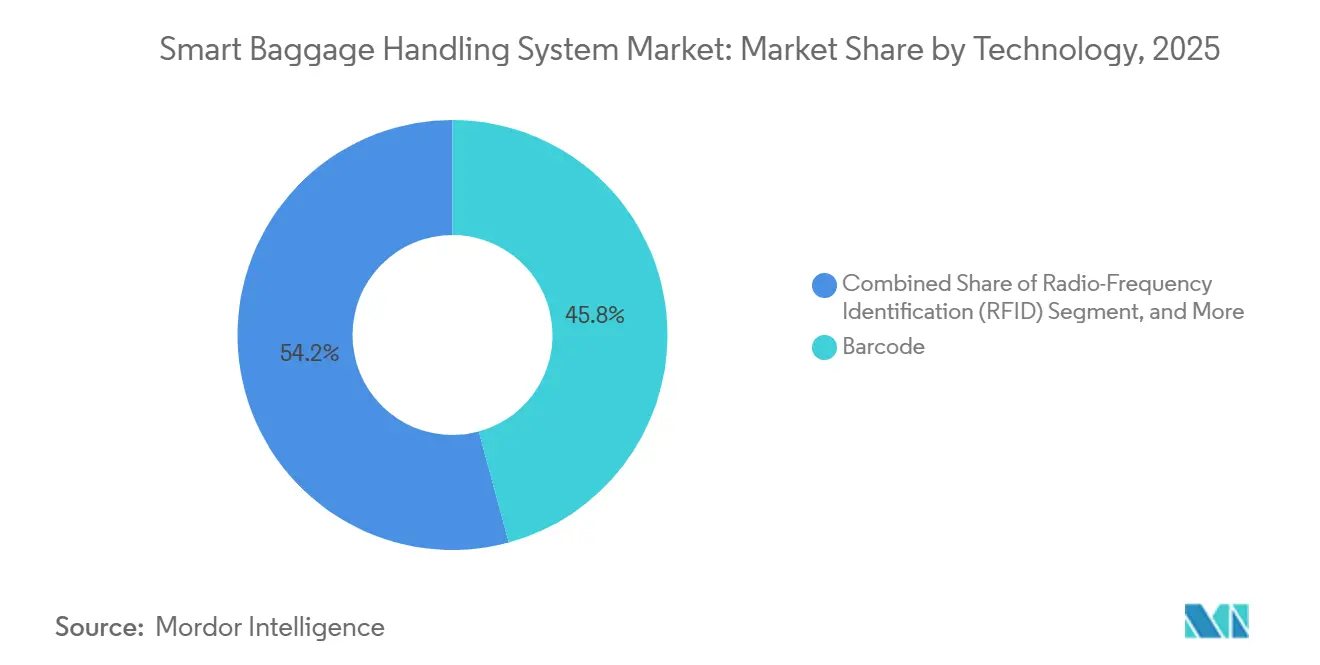

- By technology, barcode retained 45.78% share in 2025, yet ultra-wideband is advancing at a 17.28% CAGR over 2026-2031.

- By end-user, Tier-1 airports accounted for 58.51% spending in 2025, but Tier-3 facilities are forecast to grow at 17.39% CAGR to 2031.

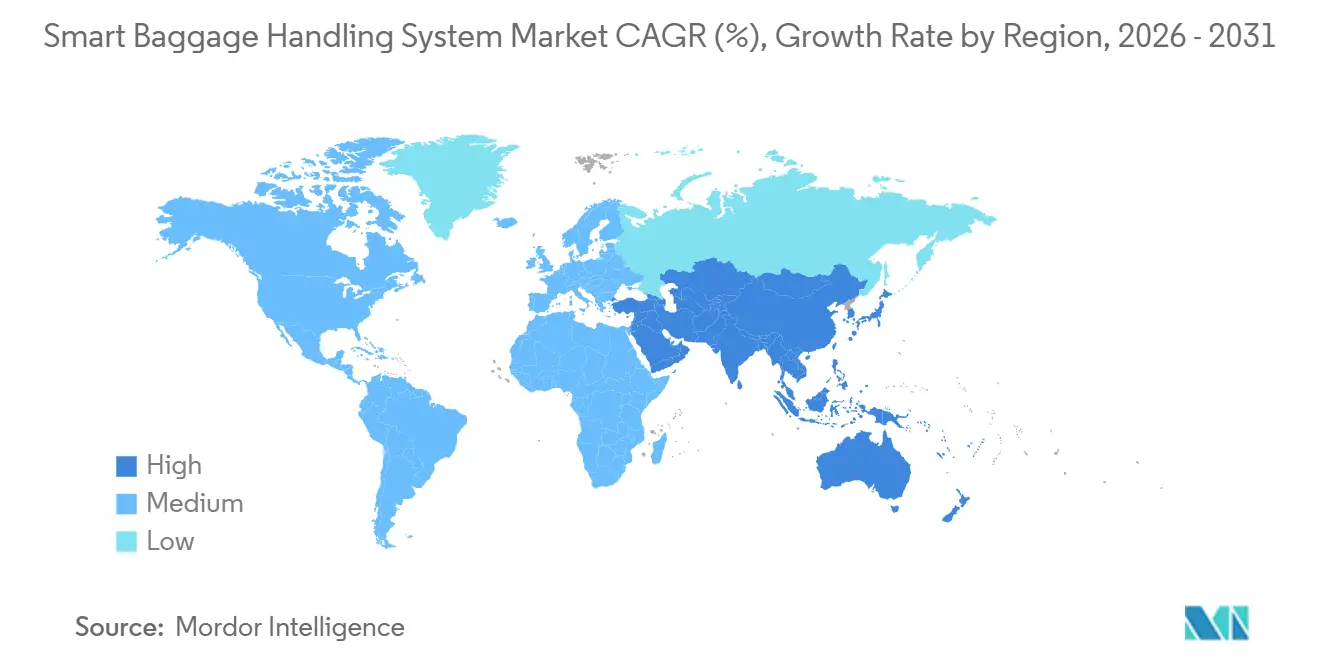

- By geography, Asia-Pacific held 35.28% share in 2025 and the Middle East is projected to grow at an 18.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Baggage Handling System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Mandate for End-to-End Baggage Tracking Under IATA Resolution 753 | +3.2% | Global, with accelerated adoption in Europe and North America | Short term (≤ 2 years) |

| Rapid Airport Capacity Expansions in Asia-Pacific and the Middle East | +4.1% | Asia-Pacific core, Middle East, spill-over to Africa | Medium term (2-4 years) |

| Rising Passenger Preference for Touch-Free Self-Service Journeys | +2.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Deployment of AI-Enabled Predictive Maintenance to Cut Conveyor Downtime | +2.3% | Global, early gains in Tier-1 airports across all regions | Medium term (2-4 years) |

| Integration of Digital Twins for Real-Time Baggage-Flow Optimization | +1.9% | North America and Europe, pilot deployments in Asia-Pacific | Long term (≥ 4 years) |

| Airports Monetizing Baggage Data Through Ancillary Revenue Streams | +1.4% | Global, concentrated in Tier-1 hubs with mature analytics infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Mandate for End-to-End Baggage Tracking Under IATA Resolution 753

The 2018 regulation obliges carriers and handlers to record bag custody at acceptance, loading, transfer, and arrival. By 2024, 75% of airports and 44% of airlines were compliant, but many still rely on barcode-only scans that lack real-time visibility. Continuous RFID and Bluetooth Low Energy tracking trims mishandling a further 25% beyond barcode baselines. Carriers that serve a single international route must still upgrade entire networks to avert interline breakdowns, creating a multiplier effect for tag vendors. European and North American regulators enforce compliance more stringently, accelerating retrofit programs.

Rapid Airport Capacity Expansions in Asia-Pacific and the Middle East

Mega-projects such as Dubai’s USD 35 billion Al Maktoum expansion and Riyadh’s USD 293 million cargo hub are embedding autonomous sortation, robotic tugs, and AI flow optimization from inception. Greenfield sites bypass legacy constraints, allowing modular architectures that scale 30%-50% via firmware rather than concrete. China’s Fuzhou Changle Airport illustrates this path, operating 6,000 bags per hour with RFID-enabled storage that flexes for early check-in. These deployments ripple into Africa as contractors replicate proven blueprints.

Rising Passenger Preference for Touch-Free Self-Service Journeys

Post-pandemic surveys indicate that 68% of travelers favor self-service bag drop, and deployments at Denver and San Francisco have achieved up to 60% capacity gains per lane.[1]SITA, “RFID Baggage Tracking: The Future Is Now,” SITA.AERO Facial recognition, RFID wristbands, and weight-verification sensors streamline transactions to under 90 seconds, easing labor cost pressures. North America and Europe lead adoption because unionized workforces amplify the automation value proposition, but Asia-Pacific is catching up as traffic rebounds to record levels.

Deployment of AI-Enabled Predictive Maintenance to Cut Conveyor Downtime

Unplanned failures cause up to 20% of mishandled bags. AI platforms ingest vibration, temperature, and motor-current data to flag issues 7-14 days early. Christchurch Airport cut unscheduled downtime 40% in the first year, while UPS’s Incheon hub achieved 99.9% uptime at 1.2 million parcels per day. Maintenance logs feed digital twins, producing a virtuous cycle of continual parameter refinement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Capital Expenditure for Legacy System Modernization | -2.7% | Global, acute in North America and Europe with aging infrastructure | Short term (≤ 2 years) |

| Limited Standardization Across Airlines, Airports, and Technology Vendors | -1.9% | Global, fragmentation highest in Asia-Pacific and South America | Medium term (2-4 years) |

| Cybersecurity Vulnerabilities in IoT-Connected Baggage Networks | -1.3% | Global, elevated risk in Tier-1 hubs with high connectivity | Medium term (2-4 years) |

| Shortage of Skilled Technicians for Robotics and Automation Upkeep | -1.1% | Global, most severe in Asia-Pacific and Middle East with rapid deployment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capital Expenditure for Legacy System Modernization

Retrofitting a mid-sized hub costs USD 50-200 million with payback horizons of 8-12 years. Austin-Bergstrom spent USD 241.5 million in 2025, and Seattle-Tacoma has earmarked USD 190 million through 2028. Smaller airports struggle to amortize fixed costs, although FAA grants, such as Denver’s USD 26.6 million award, soften the blow in the United States.[2]Federal Aviation Administration, “Airport Safety Grants Program,” FAA.GOV Emerging markets rarely offer comparable subsidies, slowing adoption despite rising passenger expectations.

Limited Standardization Across Airlines, Airports, and Technology Vendors

The ecosystem spans proprietary airline departure-control systems, vendor-specific conveyor controls, and fragmented tag protocols. IATA’s XML messaging push remains uneven, forcing projects like Copenhagen Terminal 3 to insert custom middleware that adds 15%-20% to costs. Frequency variations in RFID and UWB tags oblige airports to stock multiple reader types, heightening complexity in Asia-Pacific and South America where low-cost carriers proliferate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Robotics Reshape Fixed-Infrastructure Dominance

Conveyors and sorters captured the largest share of 41.13% in the 2025 revenue slice, yet airports now pilot flexible robotic fleets to handle seasonal surges without permanent construction. The Smart Baggage Handling System market size for autonomous mobile robots is projected to expand at a 17.11% CAGR between 2026 and 2031. dnata’s deployment of six TractEasy tractors at Dubai International Airport for AED 6 million (USD 1.6 million) validated the effectiveness of peak-period augmentation. EasyMile’s tractors at Frankfurt logged 20,000 kilometers with 99.5% uptime, demonstrating industrial-grade reliability.

Robotics also lowers emissions by replacing diesel tugs, aligning with carbon-reduction mandates. Aurrigo’s Auto-DollyTug trials at Schiphol and Changi target an 8%-12% drop in ground emissions. Cyberdyne’s HAL exoskeleton pilots in Haneda cut musculoskeletal injuries 30%. These successes persuade Tier-3 airports that modular robots can deliver much of Tier-1 functionality at a fraction of capital outlay.

By Solution: Real-Time Tracking Challenges Reconciliation Incumbency

Checked-baggage reconciliation systems accounted for 36.32% of revenue in 2025, highlighting their critical role as the compliance backbone for the aviation industry. These systems ensure that baggage is accurately tracked and matched with passengers, reducing the risk of mishandling and improving operational efficiency. Real-time tracking, however, is projected to grow faster, with an annual growth rate of 17.09%, as airlines increasingly leverage data to proactively address potential misrouting issues. Collins Aerospace has reported sub-one-minute transaction times on its ARINC SelfDrop kiosks, which significantly reduce queuing space requirements at airports.[3]Collins Aerospace, “Self-Service Bag Drop,” COLLINSaerospace.COM Similarly, SITA’s Bag Radar system identifies at-risk bags several hours in advance, enabling ground crews to intercept and resolve issues before passengers miss their connections.

Self-service technologies are also helping operators overcome labor bottlenecks, a persistent challenge in the aviation sector. For instance, Qatar Aviation Services has successfully saved 70,000 labor hours annually by integrating Amadeus software into its operations. This reduction in manual labor not only streamlines processes but also allows staff to focus on higher-value tasks. Although the lost-luggage recovery segment remains relatively small, every avoided mishandled bag contributes to preserving customer goodwill. This goodwill is a critical metric that directly influences Net Promoter Scores, which in turn can drive potential ancillary revenue opportunities for airlines.

By Technology: Ultra-Wideband Gains Ground on Barcode Incumbency

Barcode’s 45.78% Smart Baggage Handling System market share in 2025 reflects its low cost and three-decade install base. However, UWB’s centimeter-level accuracy supports robotic handoffs and automated loading verification, justifying a 17.28% CAGR forecast. Eliko’s Tallinn Airport pilot achieved sub-10-centimeter resolution at 40 Hz, enabling conveyor-to-robot transfers without human checks. RFID reached 27% penetration by 2024, with 99.98% read accuracy, slashing mishandling by 25%.

Hybrid layering mitigates budget limits, smaller airports overlay BLE beacons atop barcode scanners to gain incremental visibility and enhance operational efficiency. This approach allows these airports to improve baggage tracking without requiring significant infrastructure upgrades. Additionally, declining tag prices and the availability of modular readers are expected to facilitate UWB technology adoption among Tier-2 facilities by 2028. This development is expected to expand the addressable market for suppliers, enabling them to serve a broader range of airport operations and needs.

By End-User: Tier-3 Airports Accelerate Automation Adoption

Tier-1 hubs processed 58.51% of the 2025 investment, but growth momentum is shifting toward Tier-3 airports, which are projected to expand at a robust CAGR of 17.39%. The Smart Baggage Handling System market size for regional facilities is experiencing significant growth as regulators increasingly extend tracking mandates to improve operational efficiency and passenger satisfaction. For instance, Bozeman Yellowstone International Airport invested USD 23.9 million in inline screening systems to enhance baggage handling for its 2.4 million annual passengers. Similarly, Sarasota-Bradenton International Airport allocated USD 46.9 million to consolidate baggage flows across its terminals, aiming to streamline operations and accommodate rising passenger volumes.

Tier-2 airports occupy a middle ground, combining traditional fixed conveyor systems with advanced modular robotics to optimize baggage handling processes. Leonardo’s USD 120 million contracts at Houston Hobby Airport and Melbourne Orlando International Airport highlight how flexible financing options can facilitate the adoption of innovative technologies, even when capital budgets are constrained. Additionally, airlines and ground handlers are making separate investments in mobile scanners to ensure consistent and accurate baggage data management, even when operating across multiple airport locations. This approach underscores the growing emphasis on interoperability and efficiency within the baggage handling ecosystem.

Geography Analysis

Asia-Pacific dominated with 35.28% Smart Baggage Handling System market share in 2025, driven by China’s rapid airport construction boom and India’s ongoing privatization initiatives in the aviation sector. Greenfield projects, such as Fuzhou Changle International Airport and Delhi Terminal 1, are implementing end-to-end RFID networks and self-drop kiosks from the outset.[4]New Delhi Airport, “Terminal Information,” NEWDELHIAIRPORT.IN This proactive approach allows these airports to bypass the challenges associated with brownfield retrofits, which often slow down modernization efforts in Western markets.

The Middle East is projected to be the fastest-growing region, with an impressive 18.31% CAGR through 2031. Dubai’s Al Maktoum International Airport is targeting a capacity of 260 million annual passengers, supported by a fully autonomous baggage handling backbone. Similarly, Saudi Arabia’s King Abdulaziz International Airport is planning to accommodate 114 million passengers by 2030, leveraging integrated RFID systems and predictive maintenance technologies. Sovereign wealth funds in the region are channeling significant investments into aviation infrastructure as part of broader economic diversification strategies, ensuring a steady flow of funding for long-term projects.

North America and Europe face unique challenges due to their century-old terminals, which must remain operational during extensive refurbishments. For instance, Austin-Bergstrom International Airport completed a USD 241.5 million upgrade in 2025, following a phased construction approach that minimized disruptions to flight operations. Similarly, Seattle-Tacoma International Airport is navigating comparable complexities, with its modernization efforts expected to continue through 2028. Meanwhile, South America and Africa, though still in the early stages of adoption, are exploring modular solutions that enable them to leapfrog to modern baggage-handling standards, bypassing the incremental upgrades seen in more developed regions.

Competitive Landscape

The top five integrators, Vanderlande, BEUMER, Siemens Logistics, Daifuku, and SITA, control an estimated 40%-50% of global contract value, giving the Smart Baggage Handling System market a moderate concentration. These companies maintain a competitive edge by offering comprehensive solutions that bundle conveyors, RFID systems, software, and long-term maintenance services, effectively locking in customers at the design phase. For instance, Vanderlande’s EUR 115 million (USD 123 million) Warsaw CPK contract, which includes 16 kilometers of conveyors, highlights the multiyear revenue visibility these integrators achieve through such large-scale projects. Additionally, these firms leverage their established reputations and extensive experience to secure contracts for both greenfield and brownfield projects, further solidifying their market position.

Emerging disruptors in the market are focusing on niche areas of robotics that the larger incumbents often underserve. Companies like Aurrigo specialize in autonomous dollies, while EasyMile provides electric tractors, capturing opportunities in projects where airports prefer modular, plug-and-play solutions over traditional fixed spurs. These disruptors are also leveraging advancements in artificial intelligence and machine learning to enhance the efficiency and adaptability of their solutions. Additionally, cybersecurity has become a key differentiator in the market. For example, BEUMER has partnered with DIREC to develop encrypted IoT frameworks that demonstrated full intrusion-detection capabilities during trials conducted in Zagreb.[5]BEUMER Group, “Cybersecurity Solutions,” BEUMERGROUP.COM Such innovations are becoming increasingly critical as airports prioritize data security and operational resilience.

Greenfield hubs are increasingly opting for end-to-end RFID and UWB technologies from the outset, enabling seamless integration and advanced functionality. These technologies enable real-time tracking and improved baggage-handling efficiency, which are essential for meeting the demands of modern air travel. In contrast, legacy airports are adopting incremental upgrades to safeguard their existing investments in infrastructure while gradually modernizing their systems. The fragmented nature of industry standards often extends integration timelines, creating opportunities for firms with extensive middleware expertise to bridge compatibility gaps. Furthermore, flexible financing options, such as operating leases, are expanding the addressable market by making advanced baggage handling systems accessible to Tier-2 and Tier-3 airports, which typically lack the capacity to issue bonds for large-scale investments. These financing models are particularly beneficial for smaller airports aiming to enhance their operational capabilities without incurring high upfront costs.

Smart Baggage Handling System Industry Leaders

Beumer Group GmbH & Co. KG

Siemens Logistics GmbH

Vanderlande Industries B.V.

Daifuku Co., Ltd.

SITA N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Incheon International Airport expanded remote baggage screening to Detroit and Minneapolis, allowing downtown check-in and cutting peak terminal congestion by 20%.

- April 2026: Narita International Airport unveiled a cargo masterplan featuring autonomous robots and AI sortation to increase freight throughput by 50% by 2029.

- March 2026: Leonardo won a contract to modernize Malta International Airport’s baggage system, including RFID and predictive maintenance, for 8 million passengers.

- December 2025: Leonardo completed USD 120 million installations at Houston Hobby and Melbourne Orlando, integrating inline screening and automated sortation.

Global Smart Baggage Handling System Market Report Scope

The Smart Baggage Handling System market refers to the global industry focused on advanced technologies, integrated solutions, and services that enable the efficient, automated, and intelligent movement, tracking, sorting, and management of passenger baggage across airport ecosystems. These systems leverage digital technologies such as IoT, data analytics, automation, and real-time tracking to enhance operational efficiency, improve baggage visibility, and reduce mishandling rates throughout the baggage journey.

The Smart Baggage Handling System Market Report is Segmented by Product Type (Conveyors and Sorters, RFID and IoT Tracking Hardware, Autonomous Mobile Robots, and Software and Analytics Platforms), Solution (Checked-Baggage Reconciliation System, Self-Service Bag-Drop, Real-Time Baggage Tracking, and Lost-Luggage Recovery and Return), Technology (Barcode, RFID, BLE, and UWB), End-User (Tier-1, Tier-2, Tier-3 Airports, and Airline and Ground-Handling Companies), and Geograph (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Conveyors and Sorters |

| RFID and IoT Tracking Hardware |

| Autonomous Mobile Robots |

| Software and Analytics Platforms |

| Checked-Baggage Reconciliation System (BRS) |

| Self-Service Bag-Drop |

| Real-Time Baggage Tracking |

| Lost-Luggage Recovery and Return |

| Barcode |

| Radio-Frequency Identification (RFID) |

| Bluetooth Low Energy (BLE) |

| Ultra-Wideband (UWB) |

| Tier-1 (≥40 MPPA) Airports |

| Tier-2 (10-40 MPPA) Airports |

| Tier-3 (<10 MPPA) Airports |

| Airlines and Ground-Handling Companies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Conveyors and Sorters | ||

| RFID and IoT Tracking Hardware | |||

| Autonomous Mobile Robots | |||

| Software and Analytics Platforms | |||

| By Solution | Checked-Baggage Reconciliation System (BRS) | ||

| Self-Service Bag-Drop | |||

| Real-Time Baggage Tracking | |||

| Lost-Luggage Recovery and Return | |||

| By Technology | Barcode | ||

| Radio-Frequency Identification (RFID) | |||

| Bluetooth Low Energy (BLE) | |||

| Ultra-Wideband (UWB) | |||

| By End-User | Tier-1 (≥40 MPPA) Airports | ||

| Tier-2 (10-40 MPPA) Airports | |||

| Tier-3 (<10 MPPA) Airports | |||

| Airlines and Ground-Handling Companies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current Smart Baggage Handling System market size?

The market was valued at USD 8.56 billion in 2025 and is projected to reach USD 21.19 billion by 2031.

Which product category is growing the fastest through 2031?

Autonomous mobile robots are forecast to post a 17.11% CAGR, outpacing all other product types.

Why are airports adopting ultra-wideband tracking?

UWB offers sub-10-centimeter location accuracy that supports robotic handoffs and automated loading verification, enabling higher throughput and lower mishandling.

Which region will witness the highest growth by 2031?

The Middle East is expected to expand at an 18.31% CAGR as sovereign wealth funds bankroll large-scale aviation infrastructure.

How are airlines monetizing baggage data?

Real-time tracking analytics reduce compensation claims and enable premium delivery guarantees, creating new ancillary revenue streams.

What is the main barrier for smaller airports to modernize baggage systems?

High up-front capital requirements, often between USD 50 million and USD 200 million, lengthen payback periods and deter immediate upgrades.

Page last updated on: