Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Slurry Pumps Market Report is Segmented by Product Type (Horizontal Slurry Pump, Vertical Slurry Pump, Submersible Slurry Pump, and More), Power Source (Electric, Hydraulic, Pneumatic, Diesel, Solar), End-Use Industry (Mining, Oil and Gas, Waste-Water Treatment, and More), Liner Material (High-Chrome Iron, Rubber-Lined, Polymeric and Morel), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

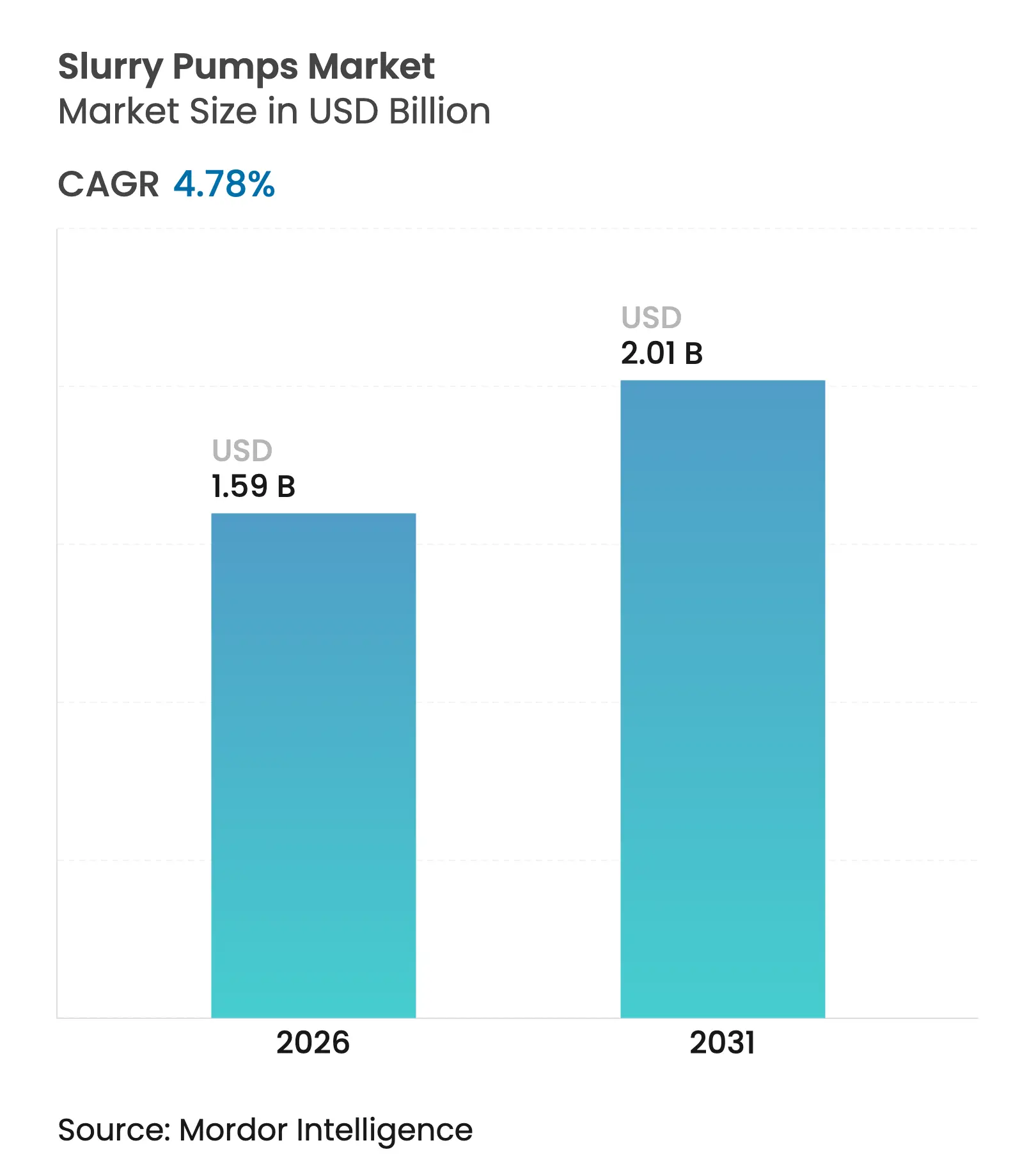

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2026 - 2031) | 4.78 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The slurry pumps market size was valued at USD 1.52 billion in 2025 and estimated to grow from USD 1.59 billion in 2026 to reach USD 2.01 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031). Demand resilience came from battery-metal mining, stricter tailings regulation, and rapid uptake of AI-enabled maintenance, all of which elevated the need for reliable pumps across mining, construction, wastewater, and process industries. The slurry pumps market benefited from miners adding capacity for lithium, cobalt, and rare-earth concentrates while construction contractors adopted 3-D concrete printing solutions that depend on high-precision slurry handling. Solar-powered pump packages moved from pilot stage to mainstream procurement as operators sought off-grid energy savings, and composite liners gained traction as users balanced wear life against rising high-chrome iron costs. Competitive intensity rose as global leaders layered digital services onto hardware sales, while regional manufacturers protected share through cost-focused offerings.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Boom in hard-rock and battery-metal mining

Boom in hard-rock and battery-metal mining

| +1.2% | Global, led by Australia, Chile, Canada | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, led by Australia, Chile, Canada

|

Impact Timeline

:

Long term (≥ 4 years)

|

Tailing-dam regulation tightening

Tailing-dam regulation tightening

| +0.8% | Global, especially North America and Australia | Medium term (2-4 years) | |||

Up-cycling of brown-field oil-sand assets

Up-cycling of brown-field oil-sand assets

| +0.4% | Canada | Medium term (2-4 years) | |||

Rapid expansion of Chinese rare-earth refining

Rapid expansion of Chinese rare-earth refining

| +0.6% | Asia-Pacific | Long term (≥ 4 years) | |||

AI-driven predictive maintenance roll-outs

AI-driven predictive maintenance roll-outs

| +0.7% | North America and Europe | Short term (≤ 2 years) | |||

Surge in abrasive 3-D concrete printing slurries

Surge in abrasive 3-D concrete printing slurries

| +0.5% | Developed markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Boom in Hard-Rock and Battery-Metal Mining

Rising electric-vehicle adoption spurred investment in lithium, cobalt, and rare-earth deposits, lifting pump demand across crushing, grinding, and tailings circuits. Large Australian spodumene mines increased plant throughput, while Chilean copper mines upgraded mill circuits to handle harder ore. Imperial Oil’s Kearl complex set a December 2024 production record, illustrating how autonomous fleets raised slurry volumes that must be moved reliably.[1]Oil Sands Magazine, “Imperial Kearl shatters production records,” oilsandsmagazine.com Miners cited pump uptime as a key productivity lever because every unscheduled shutdown can trim daily output worth millions. Government incentives, such as Queensland’s AUD 245 million critical-minerals funding, signaled multiyear mine-build pipelines, anchoring long-term replacement cycles.

Tailing-Dam Regulation Tightening

Tailing-Dam Tightening

The Global Industry Standard for Tailings Management accelerated retrofits by requiring higher factors of safety and continuous monitoring. Operators added multi-stage dewatering trains to reach higher solids content, thereby shrinking storage footprints and mitigating failure risk. Sensor-enabled pumps that transmit real-time flow and vibration data became the new baseline for compliance, particularly in jurisdictions still responding to the Brumadinho disaster. Engineering teams now specify redundant pump capacity to guarantee flow continuity during maintenance, broadening the installed base of medium-size horizontal units.

AI-Driven Predictive Maintenance Roll-Outs

Industrial plants adopted machine-learning diagnostics that cut unplanned pump failures by up to 75% and trimmed maintenance spend by 8-12%. Saudi Aramco reported 80% cost reduction after linking vibration analytics to work-order systems. Algorithms evaluate multi-sensor data to forecast wear on bearings, liners, and impellers, enabling spare-parts staging before failure. Vendors raced to embed wireless gateways and cloud dashboards, turning data services into recurring revenue streams alongside hardware sales. Integration with legacy fleets remained a hurdle but still drove retrofitting activity.

Surge in Abrasive 3-D Concrete Printing Slurries

Construction firms scaled 3-D printing from prototypes to full-scale elements such as bridge segments and tunnel linings. Printable mixes that include nano-silica and slag improved sustainability but raised abrasiveness, accelerating wear on pump wet-ends. Projects demonstrated pumping distances exceeding 1.3 km while holding ±5 mm tolerance, underscoring the need for high-pressure, variable-speed systems that maintain rheology. Manufacturers responded with hardened impellers and coatings that doubled service life, making this niche one of the fastest demand multipliers within the slurry pumps market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Pump component erosion and corrosion synergy

Pump component erosion and corrosion synergy

| -0.9% | Global, harsh chemical sites | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Global, harsh chemical sites

|

Impact Timeline

:

Long term (≥ 4 years)

|

Cap-ex freeze in new coal projects

Cap-ex freeze in new coal projects

| -0.6% | Global, variable by region | Medium term (2-4 years) | |||

Shortage of foundry-grade high-chrome iron

Shortage of foundry-grade high-chrome iron

| -0.7% | Global | Short term (≤ 2 years) | |||

Mismatch between IIoT protocols and legacy fleets

Mismatch between IIoT protocols and legacy fleets

| -0.4% | Developed markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Pump Component Erosion and Corrosion Synergy

Laboratory trials showed that particle impingement multiplied water-droplet erosion up to 5.9 times on 17-4PH stainless substrates, cutting expected component life sharply. Operators in chemical processing faced dual attack from abrasive solids and corrosive fluids, forcing frequent liner changes that raise total cost of ownership. Coating options such as HVOF-sprayed Cr3C2-NiCr extended life but added material expense. While condition monitoring helped sequence change-outs, the unpredictability of synergy effects remained a planning obstacle.

Shortage of Foundry-Grade High-Chrome Iron

Supply disruptions in specialized foundry feedstock constrained production of wear-resistant casings and impellers. Chinese manufacturers flagged limited domestic innovation capacity and dependency on imported alloy design expertise, delaying deliveries.[2]Zhejiang Rebecca Pumps & Valves Technology, “Challenges in Domestic Pump Industry,” zjrebecca.com Foundries fast-tracked expansion projects but still faced lengthy permitting cycles. Some OEMs shifted to composite liners or tungsten-carbide overlays, yet price premiums slowed broad adoption. Users diversified sourcing to hedge risk, adding transactional complexity and inventory buffering costs.

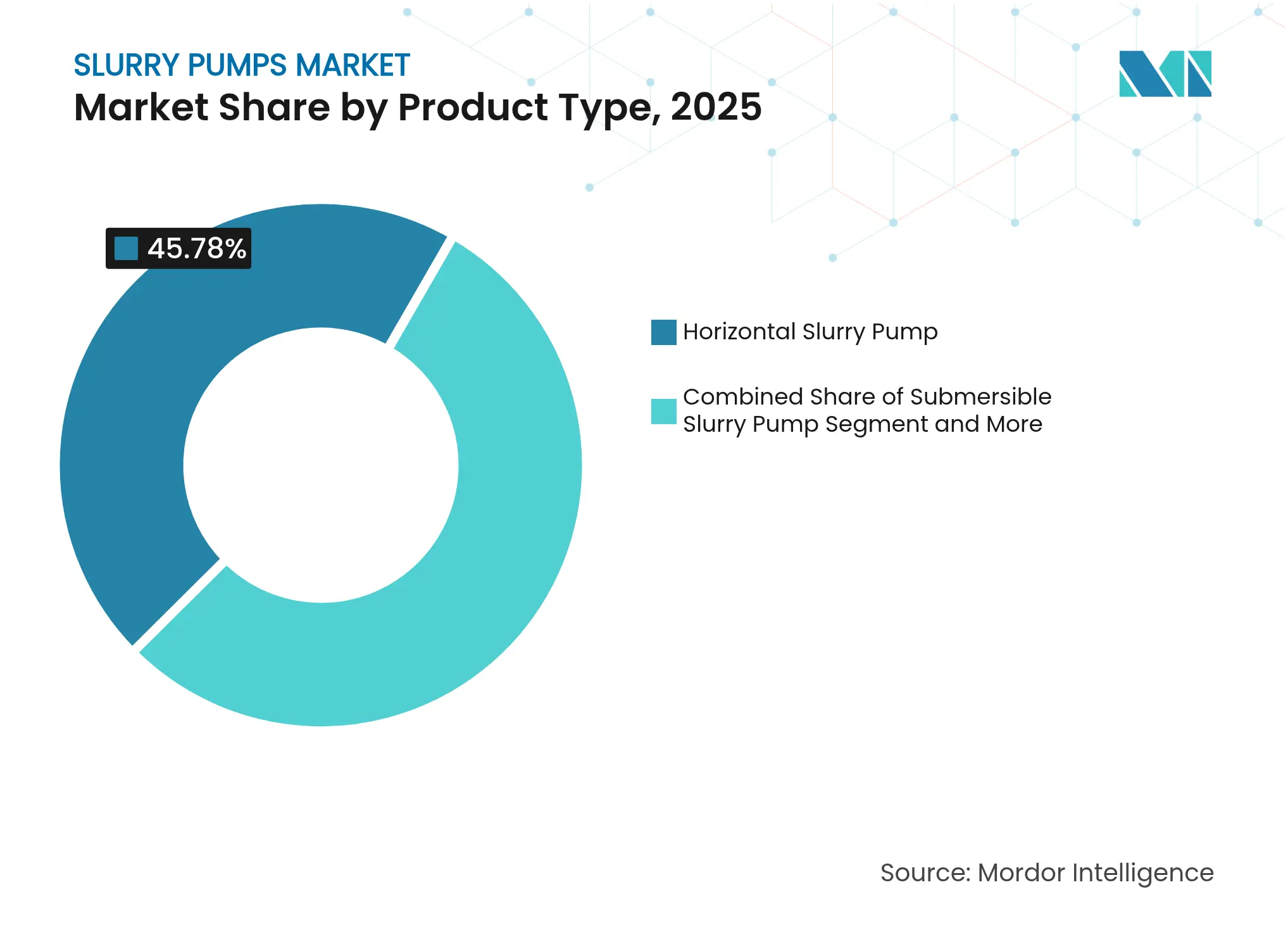

By Product Type: Horizontal Designs Sustain Leadership

Horizontal pumps represented 45.78% of the slurry pumps market in 2025 due to their serviceability and flexible mounting. Submersible units, while smaller in installed base, climbed at an 8.45% CAGR as underground mines and confined construction sites prioritized space efficiency. The slurry pumps market size for horizontal pumps is projected to grow steadily, supported by aftermarket parts demand for the ubiquitous Warman AH and comparable designs. Submersibles appealed where surface equipment racks are impractical, boosting demand for IP68-rated motors and abrasion-proof coatings. Vertical sump pumps retained a niche in sumps and under-screen applications, while centrifugal agitator models served chemical mixing duties. Dewatering variants gained share in urban tunneling projects that require continuous water removal during excavation.

Reliability, low vibration, and ease of bearing replacement kept horizontals in first place. OEMs introduced computational-fluid-dynamics optimized volutes that cut power draw by up to 6%, helping users meet corporate decarbonization targets. Submersible suppliers focused on leak-proof cable entries and double-mechanical seals to extend runtime. Digital twin selection tools now profile pump curves against slurry rheology, reducing oversizing and lifecycle energy cost. Equipment buyers increasingly specify remote monitoring packages as standard, transforming hardware procurement into connected-asset programs within the wider slurry pumps market.

Note: Segment shares of all individual segments available upon report purchase

By Power Source: Electric Dominance Meets Solar Upswing

Electric drives accounted for 70.92% share as plants embraced variable-frequency inverters that match pump speed to process requirements, trimming electricity bills. Solar arrays, while small in absolute terms, posted a 13.62% CAGR as ranchers, wastewater lagoons, and off-grid mines leveraged falling photovoltaic costs. The slurry pumps market size for solar configurations remains modest but strategic because each deployment displaces diesel, aligning with emission targets. Hydraulic drives persisted where mobile carriers need direct engine coupling, and pneumatic packages met explosion-proof codes in solvent handling areas.

Energy efficiency laws in the European Union and United States obligated large pumps to meet higher minimum-energy-performance standards, triggering retrofit activity. Solar kits such as the RPS 800 supplied up to 3,200 gallons per day without grid connection, illustrating commercialization beyond pilot. The UK Slurry Infrastructure Grant reimbursed electric transfer pumps, softening upfront cost for farmers. Hybrid systems that pair solar with lithium-ion storage extended run time into evenings, accelerating field trials across remote South American exploration camps.

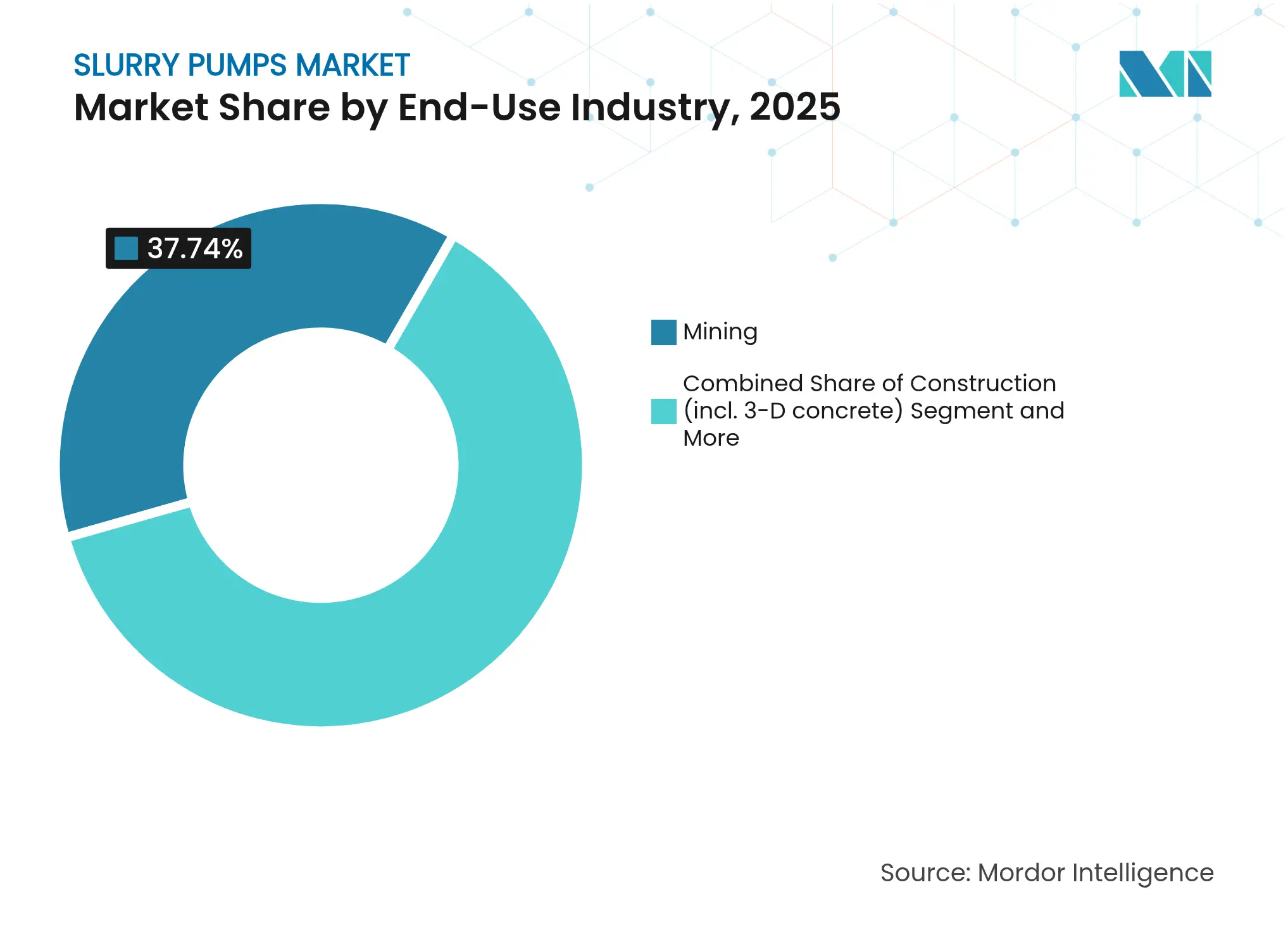

By End-Use Industry: Mining Still Commands, Construction Surges

Mining kept 37.74% share, anchored by ore-handling and tailings duties that run 24/7. Yet construction’s 12.55% CAGR highlighted the speed at which 3-D printing, shotcrete, and tunnel linings will reshape demand. The slurry pumps market share of mining is projected to decline mildly in proportional terms but remain the largest revenue pool through 2031. Oil-and-gas brownfield upgrades, wastewater expansions in megacities, and gradual agricultural mechanization all contributed steady incremental volume. Chemical processors sought alloyed wet-ends to survive aggressive slurries, lifting average selling price.

Mining operators prioritized uptime and remote diagnostics, deploying 5G-connected vibration sensors that plug into enterprise asset-management software. Construction contractors valued lightweight mobile skid packages that can be craned into dense urban sites. Wastewater boards selected progressive-cavity designs for primary sludge, citing reduced clogging versus screw pumps. Agriculture benefited from subsidies that cover pump and separator purchase, elevating nutrient-recycling capability at dairy farms.

Note: Segment shares of all individual segments available upon report purchase

By Liner Material: High-Chrome Reliability Faces Composite Gains

High-chrome iron maintained 54.92% share as the traditional workhorse for abrasives. Composite liners—polymer and ceramic blends—grew at 8.74% CAGR, appealing to operators who incorporate chemical resistance in lifecycle costing. The slurry pumps market size tied to high-chrome liners is expected to plateau as availability concerns and price volatility push buyers to hybrid strategies. Rubber compounds retained relevance where particle size is small, while duplex stainless options addressed corrosive, low-solids flows.

Research confirmed HVOF-sprayed Cr3C2-NiCr coatings delivered low porosity and high hardness on cast-iron substrates, prolonging wear life at a premium cost. Tungsten-carbide overlays offered mid-range performance gains for mines that could not wait for new foundry capacity. Procurement teams started scoring bids on total cost of ownership metrics that capture energy draw, liner life, and downtime risk rather than on lowest upfront price alone. Vendors responded with modular cartridge systems that shorten liner change-out time, further influencing material decisions across the slurry pumps market.

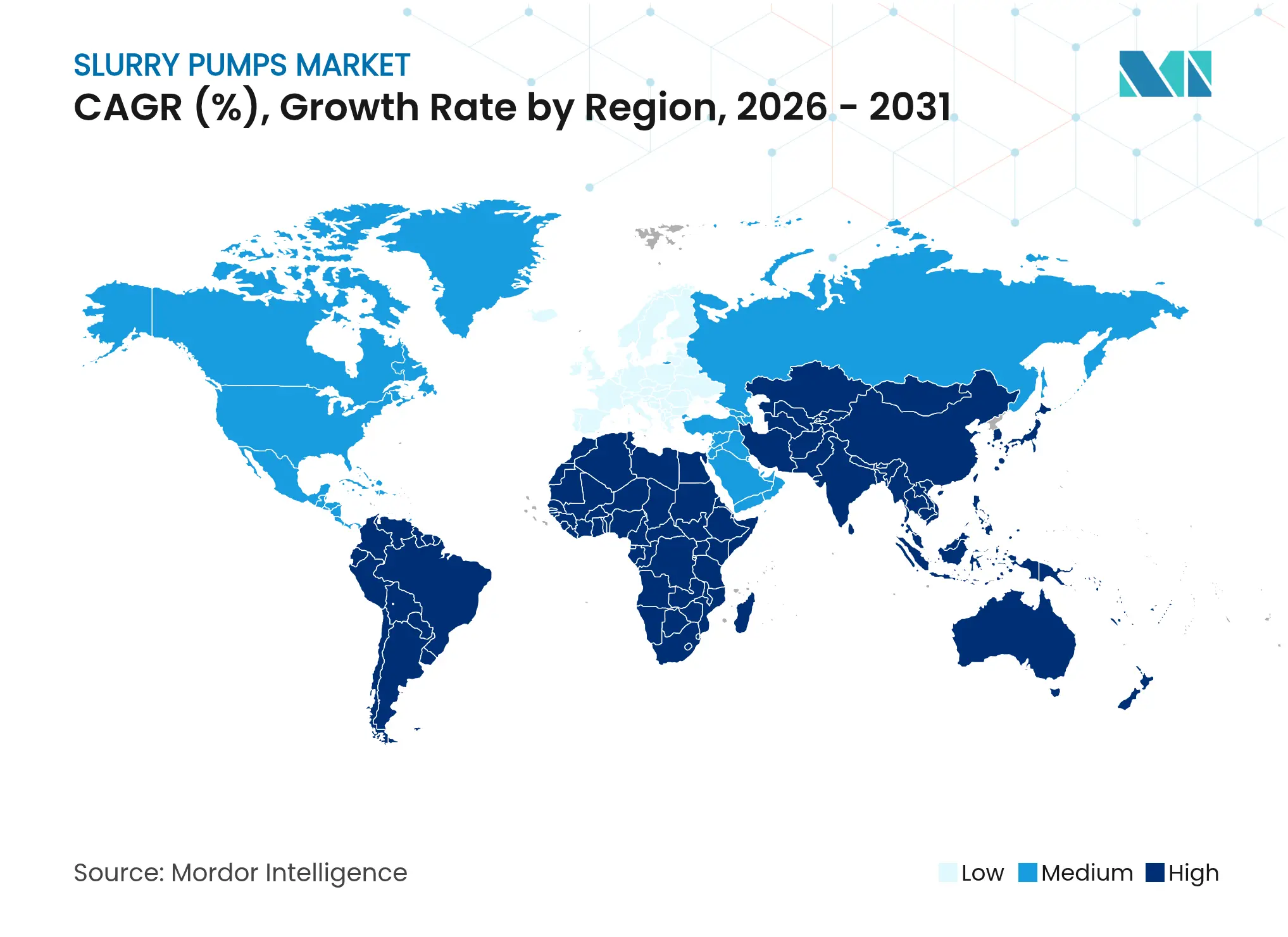

Asia-Pacific dominated with a 43.86% stake owing to China’s continued quota increases for rare-earths and sizable greenfield projects across Indonesia and Australia. Regional CAGR of 6.45% through 2031 outpaced other continents as governments prioritized resource security and infrastructure upgrades. Chinese OEMs gained share by co-locating casting, machining, and assembly plants, trimming lead time for domestic customers and exporting competitively priced units. Japanese and Korean EPC contractors specified premium European pumps on flagship refinery turnarounds, sustaining a market tier for high-margin products.

North America’s demand rose on oil-sands debottlenecking, critical-minerals incentives in the United States, and water reclamation plant upgrades. Canadian Natural Resources lifted upgrader throughput to 600,000 barrels per day, requiring additional slurry lines for coarse tailings. Municipal wastewater utilities placed multi-year blanket orders that bundle sensors and cloud analytics, demonstrating the region’s pivot toward digital lifecycle contracts within the slurry pumps market.

Europe emphasized decarbonization and circular-economy goals, which encouraged retrofits to higher efficiency drives and advanced seal systems that prevent leakage of hazardous slurries. Regulatory scrutiny over energy intensity forced plants to replace oversized legacy pumps. Manufacturers relied on service hubs in Germany and the Netherlands to deliver rapid rebuilds, reinforcing customer stickiness.

South America, led by copper and lithium hubs in Chile and Argentina, provided stable base-metal demand while grappling with water scarcity that compelled adoption of high-pressure thickened-tailings systems. Middle East and Africa recorded steady growth as desalination projects, phosphate mining, and infrastructure corridors implemented high-solids transport solutions. Across all emerging regions, concessional financing from multilateral banks often specified stringent sustainability criteria, pushing buyers toward electrically driven and solar-hybrid units.

Market Concentration

The slurry pumps market exhibited moderate concentration. Weir Group retained close to a 50% hold in high-performance mining pumps, leveraging the Warman and GEHO brands plus a global rebuild center footprint that captured aftermarket margin. Flowserve’s Pumps Division posted USD 816.4 million in Q4 2024 bookings, underpinned by chem-energy orders and service contracts that bundled asset-performance software.[4]Flowserve Corporation, “Fourth Quarter and Full-Year Results,” flowserve.com Sulzer invested CHF 10 million in South Carolina submersible lines to comply with Build America Buy America mandates, securing municipal projects.

Digitalization became a core differentiator. Vendors embedded IoT gateways that stream operating data to AI platforms capable of predicting wear patterns. Several OEMs piloted subscription models where customers pay per ton of slurry moved, aligning service revenue with operational uptime. Patent filings for magnetically suspended pumps indicated exploration of seal-less designs that eliminate common failure modes.

Regional manufacturers defended share by focusing on price-sensitive segments and offering local language support. Chinese firms such as Shanghai Electric scaled vertically integrated coastal plants, decreasing dependency on imported alloys. Indian and Brazilian assemblers partnered with European licensors to offer hybrid material options suited to their domestic mining conditions. Market entrants targeting renewable-energy slurry, such as geothermal brines and battery-recycling leachate, leveraged composite liners and energy-efficient magnetic drives to bypass incumbent specification lists.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Slurry pumps, engineered to transport a blend of solid particles and liquids, operate effectively even in demanding conditions. Predominantly utilized in sectors like mining, construction, agriculture, and wastewater treatment, these pumps adeptly move materials ranging from sand and gravel to minerals and chemicals in a fluid state. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The slurry pumps market is segmented by type (Horizontal Slurry Pump and Vertical Slurry Pump), by power source (Electric, Hydraulic, Pneumatic, Solar and Diesel), by end-use industry (Mining, Chemical, Wastewater Treatment, Construction, Oil & Gas, Agriculture and Other Industries) and by geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Market Potential for Solid-State Transformers

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.