Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

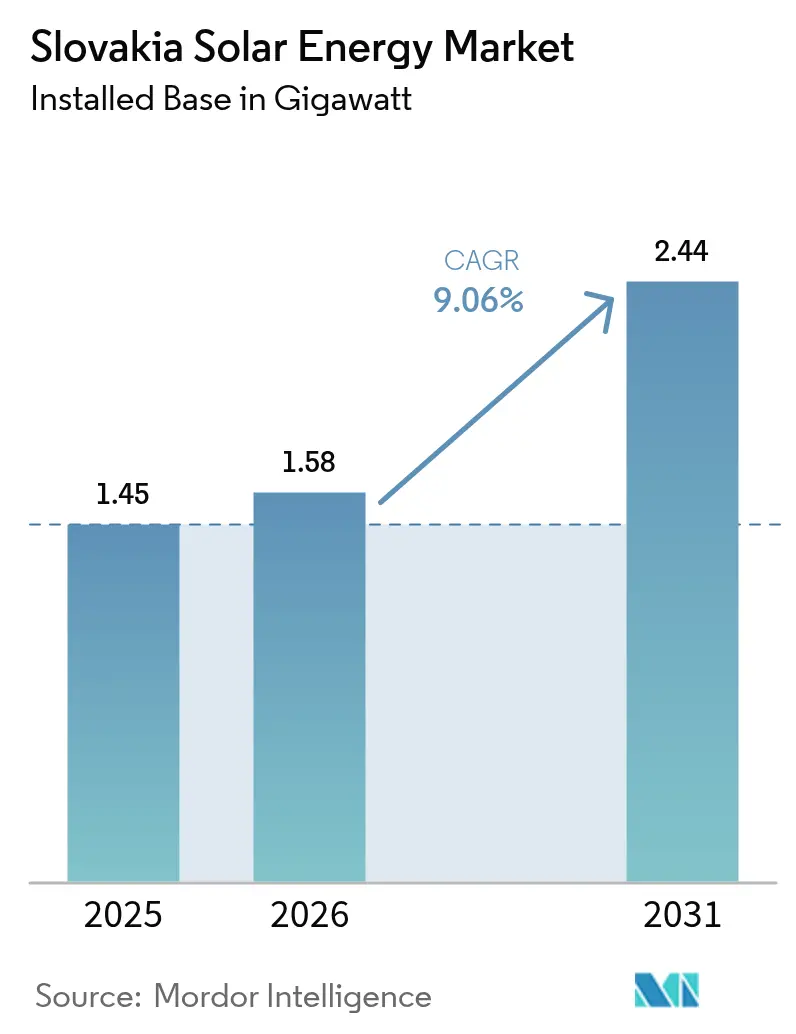

| Base Year Market Size (2025) | 1.45 gigawatt |

| Market Volume (2026) | 1.58 gigawatt |

| Market Volume (2031) | 2.44 gigawatt |

| Growth Rate (2026 - 2031) | 9.06% CAGR |

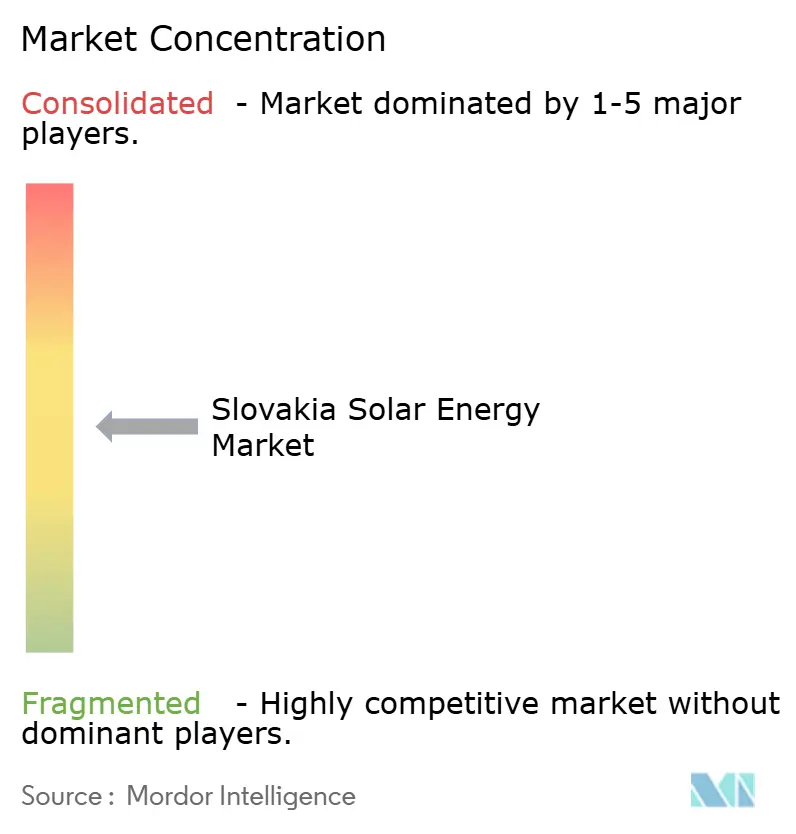

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Slovakia Solar Energy Market Analysis by Mordor Intelligence

Slovakia Solar Energy Market size in 2026 is estimated at 1.58 gigawatt, growing from 2025 value of 1.45 gigawatt with 2031 projections showing 2.44 gigawatt, growing at 9.06% CAGR over 2026-2031.

Momentum comes from rapid residential uptake, surging corporate power-purchase-agreement demand, and expanded state funding that together pushed annual additions to 274 MW in 2024.[1]pv Europe, “Central and Eastern Europe increasingly in the solar gigawatt class,” pveurope.eu Competitive intensity is rising as Energetický a průmyslový holding (EPH) assumes control of Slovenské elektrárne, heightening activity around hybrid solar-plus-storage projects and ancillary-service revenues. Negative wholesale electricity prices now occur dozens of times a year, improving arbitrage economics for battery-equipped plants and signaling the need for flexible grid solutions. The country’s updated National Energy and Climate Plan (NECP) raises renewable-electricity ambitions and introduces contract-for-difference support, flexible connection agreements, and electricity-sharing rules that collectively streamline solar deployment.

Key Report Takeaways

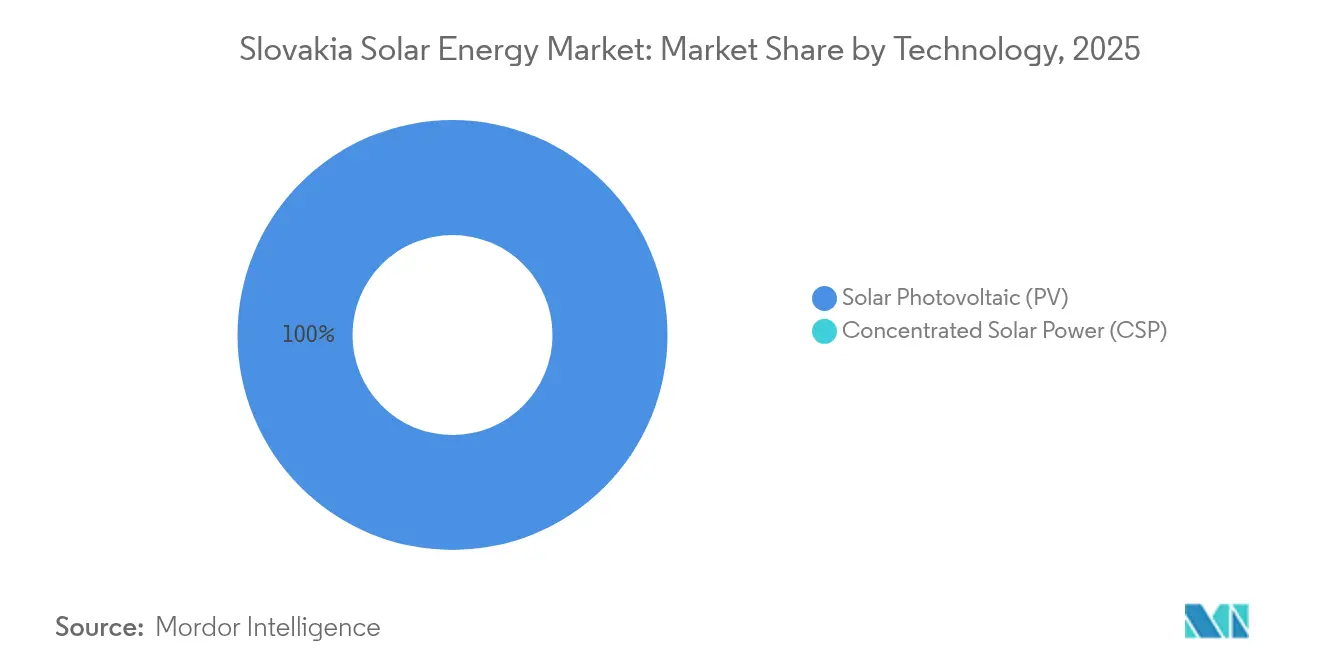

- By technology, solar photovoltaic captured 100.00% of the Slovakia solar energy market share in 2025.

- By grid type, on-grid systems held 68.12% of the Slovakia solar energy market size in 2025, while off-grid installations are projected to advance at a 14.33% CAGR through 2031.

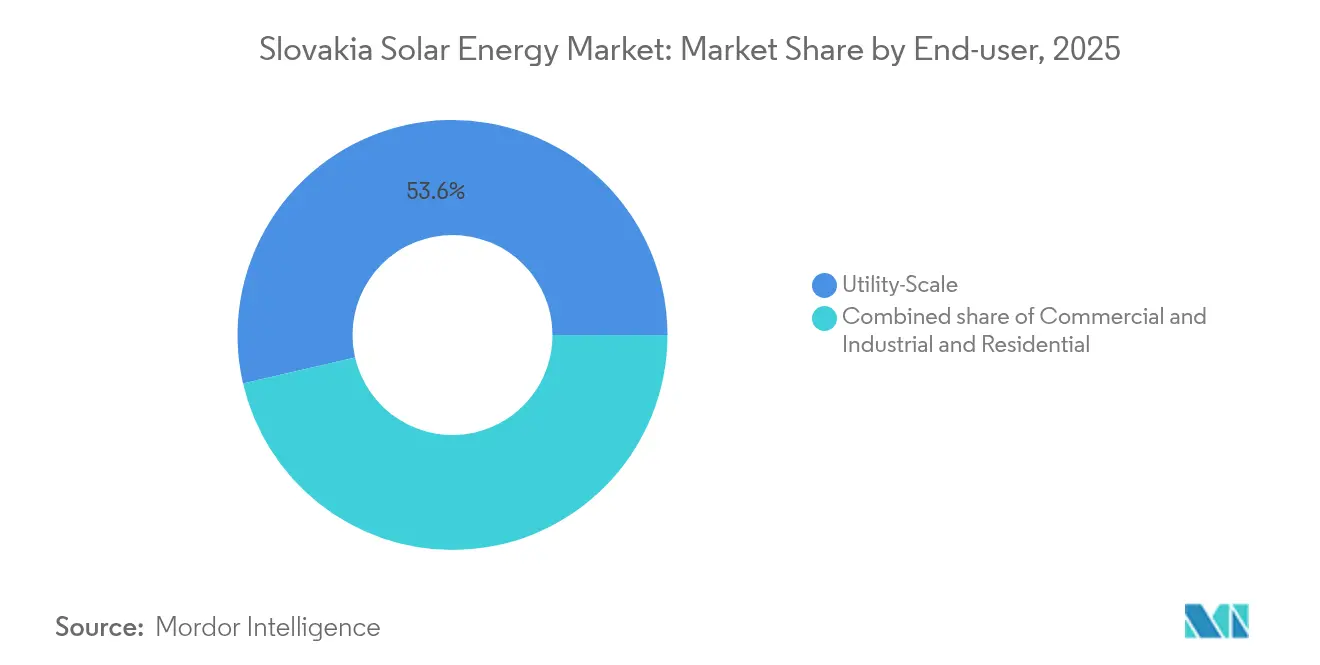

- By end-user, utility-scale projects accounted for 53.62% of the Slovakia solar energy market share in 2025, and commercial & industrial installations are poised to expand at an 17.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Slovakia Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU 2030 RES target alignment & Fit-for-55 compliance pressure | +2.0% | National, with early gains in Bratislava, Košice, Žilina regions | Medium term (2-4 years) |

| LCOE of utility-scale PV < wholesale power price parity since 2023 | +1.7% | National, concentrated in utility-scale segments | Short term (≤ 2 years) |

| Corporate PPAs from automotive OEMs (VW, Kia) driving green demand | +1.2% | Western Slovakia industrial corridors | Medium term (2-4 years) |

| Grid-balancing ancillary-service revenues unlocked after 2025 market redesign | +0.8% | National grid integration points | Medium term (2-4 years) |

| Agro-photovoltaic subsidy pilot for drought-prone regions from 2026 | +0.4% | Central and Eastern Slovakia agricultural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU 2030 RES Target Alignment & Fit-for-55 Compliance Pressure

EU rules now require Slovakia to lift the renewable-electricity share to 27.3% by 2030, up from 17.5% in 2022.[2]European Commission, “Slovakia – Final updated NECP 2021-2030,” commission.europa.eu National transposition is on track, and €4.3 billion in combined public and private investment has been earmarked for electricity and heating assets. The upcoming January 2026 legislation will introduce contract-for-difference payments, flexible grid-connection deals, and electricity sharing that collectively cut red tape for solar developers. Concurrently, the transmission operator SEPS is linked to the European MARI and PICASSO balancing platforms, allowing Slovak PV fleets to bid for regional ancillary-service revenues. These measures combine regulatory certainty with technical market access, accelerating large-scale project pipelines across all regions.

LCOE Below Wholesale Price Parity Since 2023

Utility-scale solar reached grid parity in 2023 and now consistently beats average day-ahead prices, making subsidy-free investment viable.[3]Slovak Innovation and Energy Agency, “Výsledky štatistického zisťovania o výrobe elektriny z obnoviteľných zdrojov energie za rok 2024,” siea.sk Negative power prices appeared 90 times in 2023 and have deepened to –EUR 202.70/MWh in May 2025, sharpening the arbitrage case for co-located storage. Slovenské elektrárne plans a 9 MWh battery at Mikšová hydro plant to exploit the spread between peaks and troughs. Tax changes effective 2025 lift the excise-duty exemption from 10 kW to 50 kW, cutting soft costs for small producers. Together, these factors spur new entrants, intensify competition, and reinforce cost-down trajectories for components.

Corporate PPAs From Automotive OEMs

Volkswagen and Kia anchor a 1-million-unit automotive base that now seeks low-carbon power for Scope 2 compliance, driving a new stream of long-term PPAs. Business-park developer CTP rolled out 1.26 MWp of rooftop PV across sites in Bratislava, Trnava, and Žilina under its “Off-grid 2025” program. Slovakia’s Act No. 363/2022 broadened guarantees-of-origin trading and simplified PPA structuring, letting corporates lock in 10–15-year energy-and-storage bundles. Automotive tier-one suppliers now replicate the model, feeding a second wave of rooftop and carport installations in Western Slovakia industrial zones. The predictable off-take profile these PPAs provide helps lenders reduce risk premiums on merchant solar farms.

Grid-Balancing Ancillary-Service Revenue Streams

SEPS joined the MARI and PICASSO platforms in January 2025, opening frequency-containment and automatic restoration markets to batteries as small as 1 MW. FUERGY’s 2.916 MWh Banská Bystrica system earns from both balancing and peak-shaving, with a payback claimed at 3.5 years even without grants. SEPS has meanwhile raised available connection capacity by 25%, reducing queue times and enabling more hybrids to qualify.[4]SEPS, “SEPS connected to PICASSO platform,” sepsas.sk Aggregators now bundle rooftop arrays and batteries into virtual power plants that can trade across borders, enriching revenue options and supporting grid resilience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Distribution-level hosting-capacity saturation in Western Slovakia | -1.3% | Western Slovakia distribution networks | Short term (≤ 2 years) |

| Stop-start nature of CAPEX subsidy schemes (Green Homes, Modernisation Fund) | -0.7% | National, affecting residential and C&I segments | Short term (≤ 2 years) |

| Farmland Protection Act limiting green-field solar >2 ha | -0.5% | National, primarily rural and agricultural zones | Medium term (2-4 years) |

| EPC labour shortage as installers migrate to higher-paying DACH markets | -0.4% | National, with acute impact in Western Slovakia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Distribution-Level Hosting-Capacity Saturation in Western Slovakia

Rapid commercial and industrial solar build-out in Western Slovakia now pushes some feeders close to voltage limits, delaying or denying new connection requests.[5]Energy Policy Institute, “Štúdia integrácie OZE do ES SR,” energypolicy.sk Project sponsors must often finance transformer upgrades or accept curtailment clauses, inflating capex and lengthening development cycles. Industrial clusters near Bratislava and Trnava feel the squeeze most, as automotive OEMs and their suppliers crowd the same substations. Regulators plan flexible-connection contracts starting in 2026, but until then, pipeline growth risks bottlenecks. Developers therefore prioritize brownfield sites with spare capacity or co-locate with storage to lower grid-impact scores. The constraint slows utility-scale momentum but simultaneously boosts demand for behind-the-meter and off-grid systems.

Stop-Start Nature of CAPEX Subsidy Schemes

Residential and small-commercial installers lean on grants such as “Zelená domácnostiam,” yet annual budgets often run dry mid-year, freezing order books for months. The Green for Businesses program follows a tender-window model that triggers bursts of demand followed by lulls, undermining supply-chain planning. Modernisation-Fund money must clear European Investment Bank checks, introducing further administrative delay. Experienced EPC crews migrate to Germany and Austria, where funding is steadier, leaving domestic projects understaffed and inflating wages. Until more predictable incentive calendars appear, small-scale uptake will remain sensitive to policy on-off cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar PV Maintains Total Market Control

Solar photovoltaic installations hold 100% of the Slovak solar energy market in 2025, leaving no room for concentrated solar power because irradiation conditions favor flat-plate modules. The segment expanded from 573 MW in 2022 to more than 1.11 GW by 2024, a trajectory expected to persist near a 9.05% CAGR through 2031. Slovak households now benefit from excise-duty exemptions up to 50 kW, accelerating rooftop adoption and encouraging energy-community projects that pool generation and storage. In parallel, large developers switch from feed-in tariffs to auction-indexed bonuses, improving price discovery and aligning with EU state-aid rules.

Component innovation underpins the segment’s dynamism. Photon Energy introduced Solinteg hybrid inverters expressly certified for Slovak grid codes, supporting plug-and-play battery pairing. Building-integrated options such as HybridHouse’s Solar Full Roof grow in appeal for urban retrofits where land is limited. Local manufacturer VONSCH supplies high-efficiency inverters tailored to off-grid mining and industrial niches, expanding domestic value capture. Such diversification reinforces resilience against import bottlenecks and positions Slovak firms within regional supply chains.

By Grid Type: On-Grid Dominance Faces a Fast-Growing Off-Grid Niche

On-grid arrays captured 68.12% of the Slovakia solar energy market size in 2025 on the strength of priority dispatch, net-metering rights, and access to ancillary-service income. Integration with MARI and PICASSO lets operators trade flexibility across borders, supporting earnings beyond simple energy sales. Yet hosting-capacity constraints in Western Slovakia and curtailment risk encourage hybrid designs that embed storage or bidirectional EV chargers to smooth export profiles.

Off-grid systems, though still a minority, are the fastest-growing slice at a forecast 14.33% CAGR. Farms, mountain resorts, and remote industrial sites adopt standalone kits to dodge grid delays and rising demand charges. Rekoser ships lithium-iron-phosphate battery packs optimized for Slovak temperature swings, while Megarevo delivers 2.5 MW/2.5 MWh containers that participate in demand-response once grid points become available. As legislation introduces flexible connection terms, some off-grid arrays may later upgrade to semi-autonomous status, monetizing surplus power without surrendering self-reliance.

By End-User: Utility-Scale Still Leads but C&I Growth Outpaces

Utility-scale plants held 53.62% of the Slovak solar energy market share in 2025, benefiting from economies of scale and the ability to shoulder grid-upgrade costs. Projects such as the 44.2 MW Veľký Blh park demonstrate how revenue stacking, merchant sales, balancing, and green certificates can support bankability. EPH-backed Slovenské elektrárne is layering a 9 MWh battery onto hydro assets to capture ancillary margins, signaling a broader tilt toward hybridization.

Commercial and industrial rooftops, however, grow the fastest at 17.92% CAGR, powered by automotive and logistics tenants chasing ESG targets. Companies such as CTP integrate solar, storage, and EV charging under turnkey energy-as-a-service agreements, lowering occupancy costs and improving carbon footprints. Amendments from April 2022 let prosumers export up to 1,000 MWh per year, enhancing revenue certainty for larger factories. Residential demand remains solid at 113.6 MW added in 2024, yet future volume hinges on more stable subsidy calendars and stronger domestic installer capacity.

Geography Analysis

Western Slovakia, anchored by Bratislava, Trnava, and Žilina, hosts 67.90% of on-grid capacity thanks to dense industrial load and robust transmission lines. Volkswagen and Kia factories source green power locally through long-term PPAs, ensuring bankable revenue streams for developers. Rooftop space within business parks offers a literal platform for expansion, though distribution feeders near saturation force some projects to add batteries or accept curtailment clauses.

Central Slovakia is emerging as a new utility-scale hub where land prices are lower, and transmission corridors still have headroom. Košice and surrounding districts attract energy-storage manufacturers like INO-HUB, whose €5.5 million battery plant in Kysucké Nové Mesto will underpin regional hybrid projects and create 90 skilled jobs. State plans for an agro-photovoltaic pilot in drought-prone northern counties add a future layer of demand, blending food security and energy diversification.

Eastern Slovakia, although lagging in installed wattage, enjoys unexploited sunlight potential and supportive municipal policies aimed at job creation. Local authorities court investors with expedited permitting on brownfield sites left by heavy industry, minimizing land-use conflict and shortening development cycles. Off-grid arrays tied to tourism lodges and forestry outposts show early promise, particularly where microgrids can back up critical services during winter storms. Transmission upgrades scheduled for 2027 will link new 110 kV nodes to Hungary and Poland, expanding cross-border trading options for future PV farms.

Regulatory Landscape

Slovakia's solar support and market access rules are anchored in Act No. 309/2009 Coll. on the promotion of renewable energy sources (as amended), with pricing and support parameters regulated by the Office for the Regulation of Network Industries (URSO). URSO sets regulated conditions for renewable-electricity support under instruments such as Decree No. 370/2023 Coll., covering how eligible generators receive support and how related regulated activities are carried out.

The policy direction highlighted for the study period focuses on updated rules taking effect in 2026, including transition provisions within Act 309/2009 that affect support conditions and installed-power thresholds, alongside Ministry of Economy-led legislative work on energy regulation tools (referenced alongside amendments to Act No. 251/2012 Coll. on Energy, with a July 1, 2026 effective date in government materials). At the same time, the Ministry of Economy has prepared scenarios for targeted energy assistance in 2026 pending government decision, reflecting a shift toward more structured and conditional support design rather than broad, open-ended subsidy access.

Competitive Landscape

The Slovak solar energy market commands a moderate concentration, with the top five developers and EPC players estimated to own just above 50% of active capacity. Slovenské elektrárne’s transfer into EPH’s portfolio adds financial muscle and hybrid-energy know-how from its 70-company European network. Photon Energy accelerates component localization through partnerships with inverter brand Solinteg, capturing both supply-chain savings and intellectual-property advantages.

Smart-storage specialist FUERGY demonstrates the value of software-defined assets; its Banská Bystrica installation stacks frequency containment fees on top of PV self-consumption, achieving rapid payback without subsidies. Domestic inverter maker VONSCH addresses niche off-grid and mining clients, helping anchor a local supply ecosystem. Foreign entrants like Janom Investments use Slovak engineering talent to scale regionally, underscoring labor competitiveness despite outbound migration.

Strategy now pivots on hybrid architecture, ancillary-service readiness, and digital O&M. Developers able to provide bundled solar-storage-EV packages or participate in cross-border balancing pools secure pricing power. Meanwhile, EPC firms invest in prefabricated mounting systems and drone-based inspections to slash labor hours and cope with workforce gaps. As agro-PV pilots near launch, multidisciplinary teams that mix horticulture, power electronics, and financing skills are poised to capture first-mover advantages.

Slovakia Solar Energy Industry Leaders

-

Slovenské elektrárne, A.S.

-

Západoslovenská energetika (ZSE)

-

Axpo Holding AG

-

CEZ Group – Slovak unit

-

Green Energy SK s.r.o.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunities concentrate on scaling hybrid PV-plus-storage and projects built for flexibility, where operators can monetize changing price signals and balancing-market access. Slovakia has already posted deep negative pricing (for example, -EUR 202.70/MWh in May 2025), and SEPS' participation in European balancing platforms (MARI and PICASSO) gives batteries a clearer route to stack revenues alongside solar generation, as seen in operational deployments such as FUERGY's Banská Bystrica battery system.

Distributed C&I and community-scale solar also provide room for incremental growth, supported by corporate decarbonization demand and the policy push to formalize electricity sharing. Recent capacity additions point to execution momentum in rooftops and smaller plants (274 MW added in 2024 and 243 MW in 2025, reaching 1,357 MW cumulative by end-2025), while the updated NECP target of 1,700 MW by 2030 keeps permitting, grid connection, and bankable offtake structures in focus. Programs and tenders that combine PV with batteries under Recovery and Resilience Plan-related calls, alongside enabling rules for energy communities, support capacity build-outs in constrained distribution zones where behind-the-meter consumption and managed export are valued.

Recent Industry Developments

- June 2026: Západoslovenská energetika (ZSE) commissioned a battery energy storage system near Jaslovské Bohunice, reported at around EUR 17 million of investment. The project strengthens local flexibility at a system node, supporting higher solar penetration where distribution and transmission constraints can limit new PV connections.

- October 2025: Enery acquired Project Lassie, a 34.6 MW operational solar portfolio in Slovakia from ContourGlobal. The transaction points to ongoing portfolio consolidation and gives the buyer a larger platform for optimizing operating assets, including potential hybridization and offtake structuring.

- November 2024: Slovakia linked to the European MARI and PICASSO balancing platforms, expanding routes for batteries and hybrid solar-plus-storage plants to access ancillary-service revenues. This integration improves the commercial case for co-located storage and aggregator-led virtual power plant participation alongside new PV builds.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Slovakia solar energy market is defined as the installed solar power base in Slovakia, tracked in gigawatts, and tied to grid connected and off grid deployment across end users.

Scope exclusions: This sizing excludes broader power market revenues, electricity retail tariffs, and unrelated renewable technologies outside solar.

Segmentation Overview

-

By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

-

By Grid Type

- On-Grid

- Off-Grid

-

By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

-

By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping Slovakia's solar deployment context using public energy statistics and policy documents, so the model remains anchored to what is actually built and connected. We relied on sources such as the International Energy Agency, IRENA statistics, Eurostat electricity and energy balances, and national releases from the Slovak Ministry of Economy and the national regulator.

To tighten assumptions, we also reviewed grid connection notices, auction and support scheme updates, and project level announcements from developer and utility websites, then compared them with annual reports and investor presentations. For cross-checking plant additions and ownership changes, a paid subscription focused on company financials and intelligence, plus a patent database for technology direction, were used selectively where public disclosures were thin. These desk sources are illustrative, and other public references were used for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary discussions were used to confirm what is being commissioned versus what is only permitted, and to sanity check solar timelines that can slip after permitting and grid interconnection. We spoke with EPC and O&M participants, developers, equipment distributors, and large C&I buyers, then validated the takeaways with policy and grid experts familiar with Slovakia's interconnection and support rules.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 14% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 17% | Managers: 51% | Americas: 25% |

Market-Sizing & Forecasting

The sizing logic starts with a top-down build where national installed solar capacity is reconstructed from official energy balances, grid connected additions, and commissioning cues, and then shaped to the study definition. Once that spine is set, selective bottom-up checks are run using sampled project pipelines, typical MW sizes by end user, and channel level views of equipment availability, then used to adjust obvious gaps.

Key inputs used in the model include annual MW additions, connection and permitting throughput, expected repowering or replacement activity, typical system sizing for residential and C&I rooftops, and the pace of utility scale buildouts where land and grid access permit. For forecasting, we used scenario analysis supported by expert views, because policy design, grid capacity, and financing conditions can shift the slope quickly even when the long term direction is stable. Where bottom-up signals were incomplete, the missing portion was filled using conservative adoption rates tied to confirmed connection capacity, then rechecked against the latest commissioning pattern.

Data Validation & Update Cycle

Model outputs were checked against independent indicators such as national power statistics, published capacity snapshots, and near-term pipeline signals, and then any large variance was investigated before sign-off. When a number looked out of line, the assumption behind it was revisited, and if needed, follow-up calls were triggered with the same respondent group to confirm what changed.

Each deliverable goes through a multi-step review so calculation logic, units, and definitions remain consistent from base year to forecast year. Reports are refreshed annually, with interim updates when material events occur, for example a major policy change or an unexpected connection bottleneck. Before delivery, a final analyst pass is done so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Slovakia Solar Energy Market Estimate Compared With Other Published Estimates

Published estimates for Slovakia solar energy do not always line up because teams measure different things and also pick different timing assumptions for what is counted as market progress. The biggest spread usually comes from whether the market is sized as installed capacity, revenues, or a mixed view that blends equipment, services, and generation value.

The main gap comes from unit choice, where Mordor Intelligence keeps the market strictly in installed capacity (GW), anchored to commissioned and grid-recognized additions, rather than translating the buildout into USD using varying system cost and subsidy assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.58 B (2026) | |

| Industry Research Publisher A | USD 1.10 B (2024) | This figure is reported in USD value terms, which can fold in equipment pricing and services, and it can also shift with currency timing and assumed system cost per MW rather than confirmed commissioned capacity. |

| Trade Journal B | USD 1.45 B (2025) | This type of estimate often aligns to pipeline and target announcements, and it may count permitted or planned projects earlier than commissioning, which can inflate the near-term market when grid connection is the limiting step. |

The table shows that most differences are explained by whether the market is treated as a capacity stock versus a value pool, and by how strictly commissioning timing is applied. By keeping inputs tied to observable build signals and then cross-checking with project and policy realities, the final number stays easy to trace and repeat when new capacity data arrives.

Key Questions Answered in the Report

How large is the Slovakia solar energy market in 2026?

Installed capacity will reach 1.58 GW in 2026.

What is the expected growth rate for Slovak solar through 2031?

Capacity is projected to rise at a 9.06% CAGR to reach 2.44 GW by 2031, outpacing the country’s official targets.

Which customer segment is expanding fastest?

Commercial and industrial rooftops are forecast to grow at an 17.92% CAGR as automotive and logistics firms lock in long-term PPAs.

Why are batteries becoming integral to new projects?

Negative power prices and SEPS’ participation in European balancing markets allow batteries to earn from both arbitrage and ancillary-service fees.

What regulatory shifts will matter most after 2025?

Contract-for-difference support, flexible grid-connection deals, and electricity-sharing rules scheduled for January 2026 will streamline permitting and cut project risk.

Where are grid bottlenecks most acute?

Western Slovakia’s distribution feeders around Bratislava and Trnava face the tightest hosting-capacity limits, slowing new connections until upgrades are complete.

Page last updated on: