Sleep Tech Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.74 Billion |

| Market Size (2031) | USD 79.88 Billion |

| Growth Rate (2026 - 2031) | 18.12% CAGR |

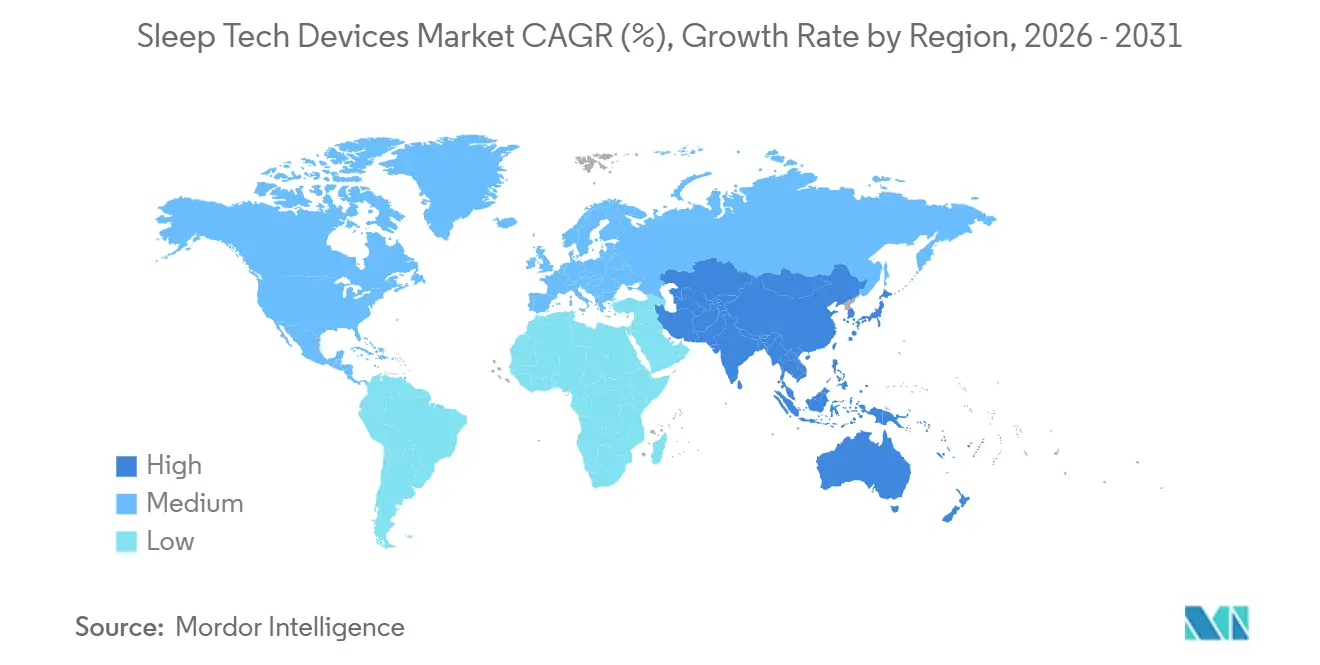

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

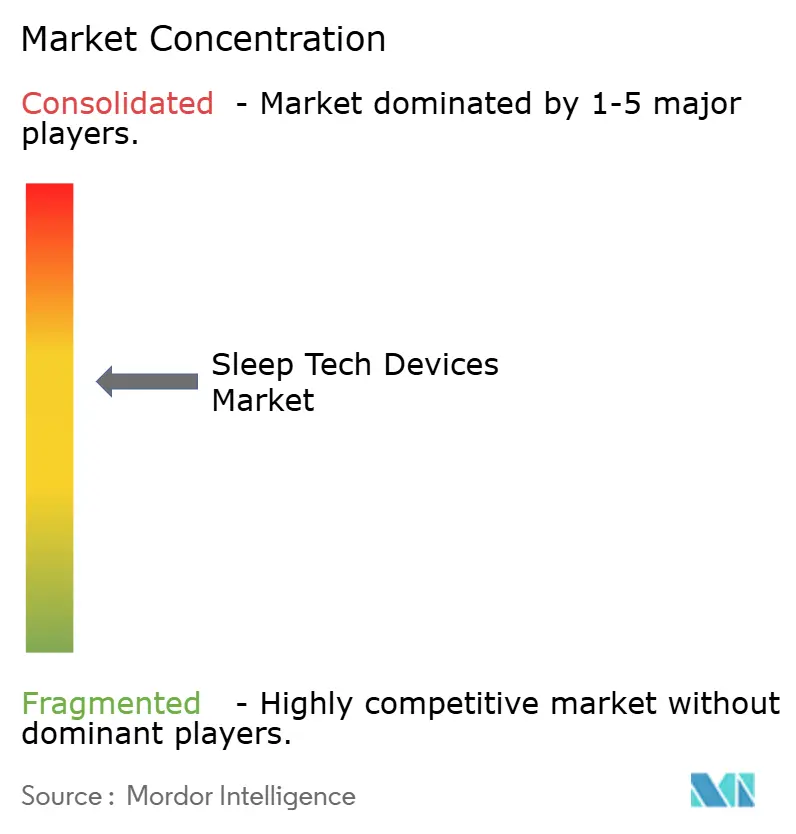

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sleep Tech Devices Market Analysis by Mordor Intelligence

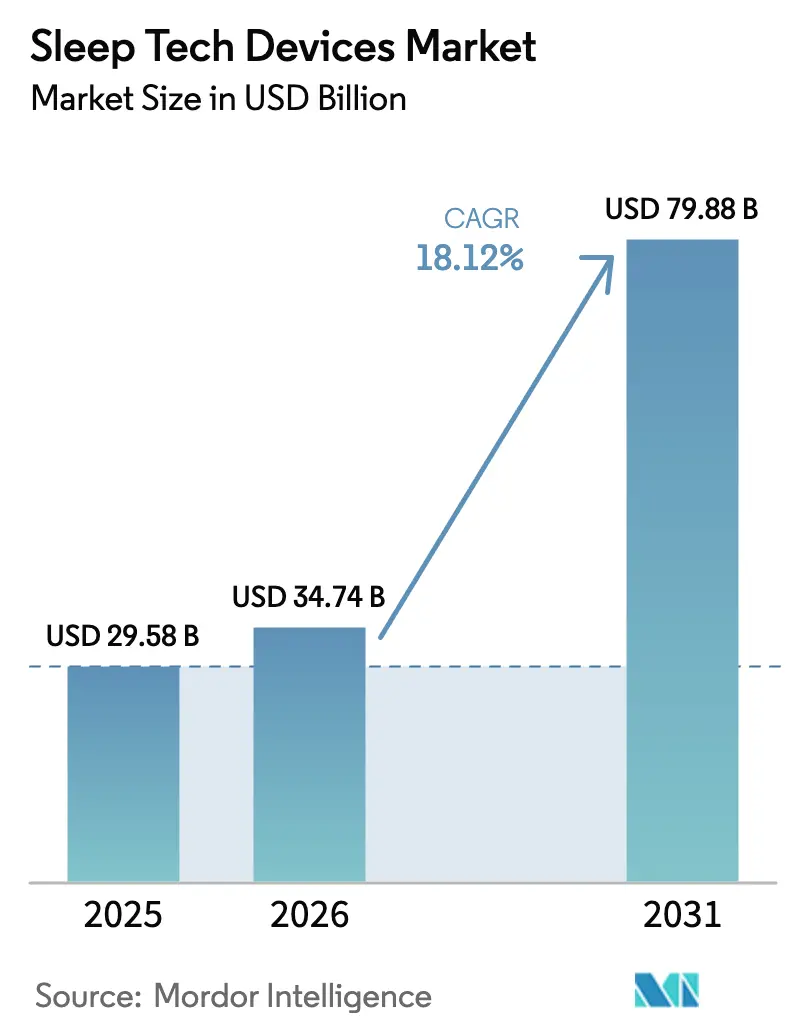

The Sleep Tech Devices Market size is projected to be USD 29.58 billion in 2025, USD 34.74 billion in 2026, and reach USD 79.88 billion by 2031, growing at a CAGR of 18.12% from 2026 to 2031.

This growth reflects a significant transition from clinic-centric diagnostics to connected, at-home solutions that integrate hardware with subscription-based analytics. Wearable devices are driving value creation, supported by FDA clearances that have elevated products like the Apple Watch Series 10 and Samsung Galaxy Watch7 from wellness trackers to reimbursable diagnostic tools. Regulatory advancements, such as the European Union's Medical Device Regulation and expanded Medicare coverage for home testing, are expediting market entry for new players. Additionally, Edge AI chips, such as the SleepViT ASIC designs, operate on just 0.56 milliwatts, enabling real-time device inference while reducing recurring cloud costs. However, inconsistent enforcement of data privacy regulations under HIPAA and GDPR presents challenges, requiring brands to adapt their go-to-market strategies to align with jurisdiction-specific requirements.

Key Report Takeaways

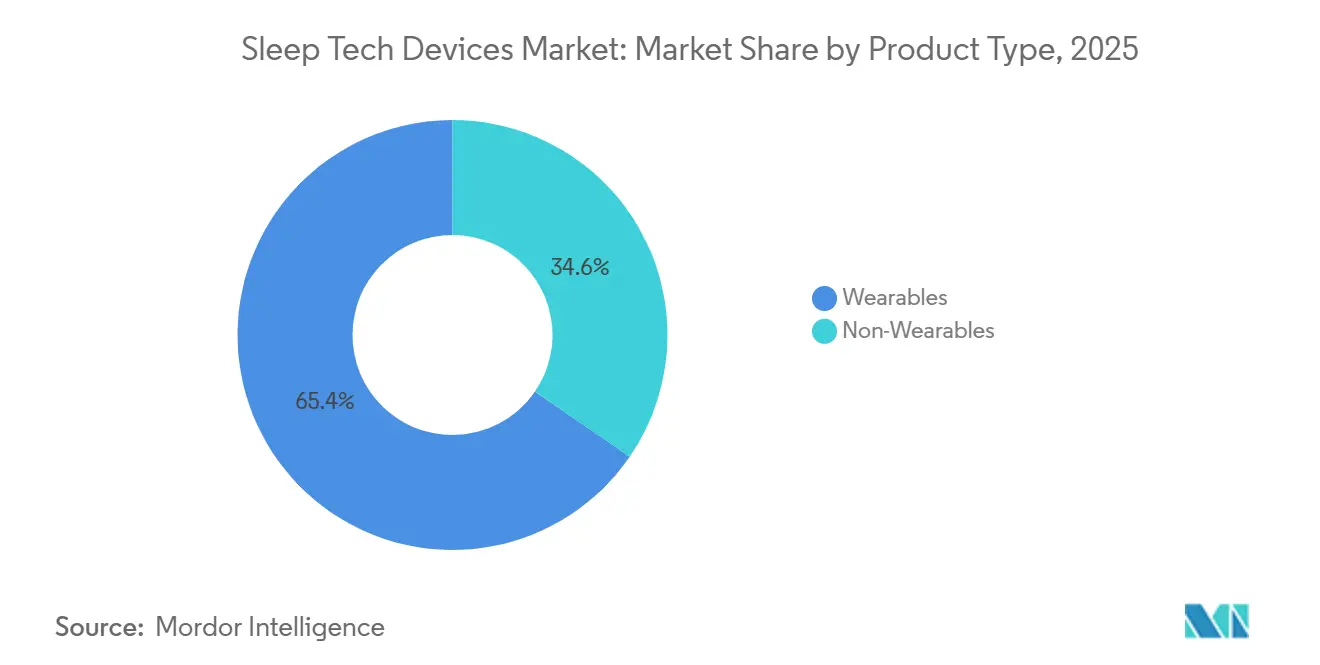

- By product type, wearables led the sleep tech devices market with a 65.43% share in 2025, and the segment is projected to grow at a 20.43% CAGR through 2031.

- By application, insomnia captured 42.45% of the revenue in 2025; narcolepsy devices are projected to record the highest CAGR at 20.55% from 2026 to 2031.

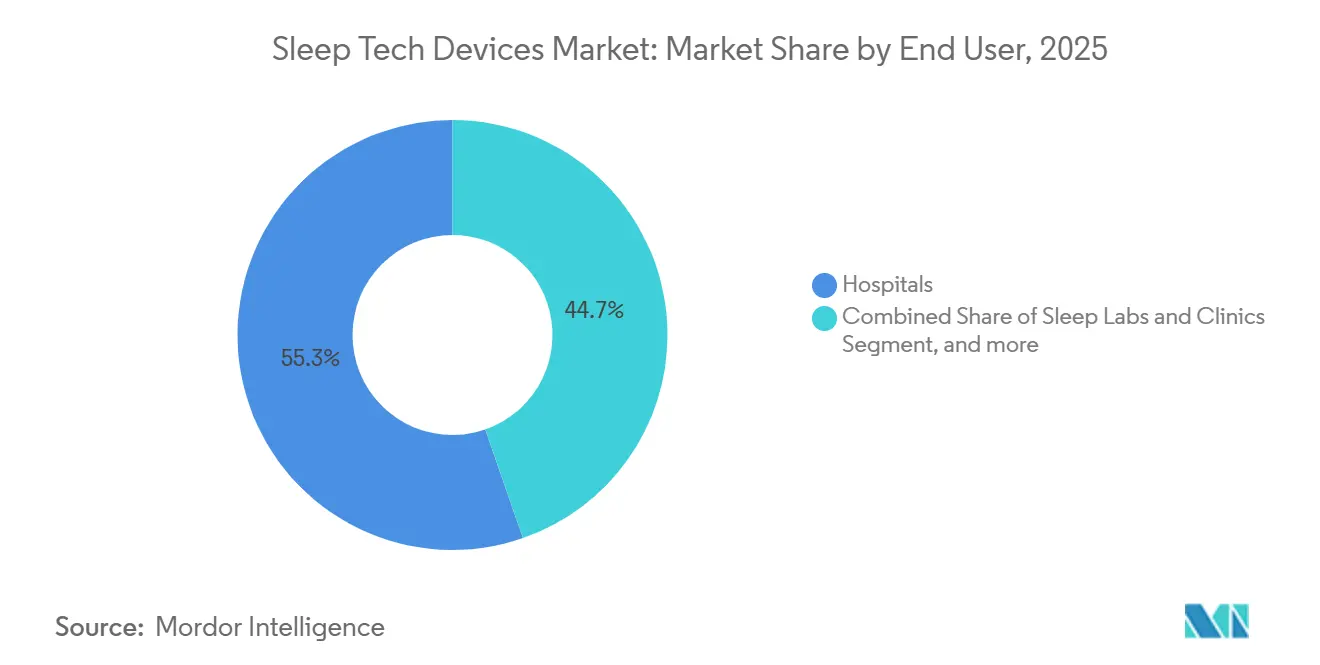

- By end user, hospitals held 55.32% of revenue in 2025, whereas home care settings are advancing at a 21.56% CAGR.

- By distribution channel, offline retail accounted for 41.45% of sales in 2025, while direct-to-consumer e-commerce is projected to post a 21.45% CAGR.

- By geography, North America led with 42.87% share in 2025, while Asia-Pacific is pacing at a 19.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sleep Tech Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence of Sleep Disorders | +4.2% | Global, especially North America and Asia-Pacific cities | Medium term (2-4 years) |

| Technological Advancements in Wearables, Sensors & AI | +5.1% | North America, Europe, Asia-Pacific tech hubs | Short term (≤ 2 years) |

| Growing Adoption of Smart-Home Ecosystems for Sleep Optimization | +2.8% | North America, Europe, early Middle East spillover | Medium term (2-4 years) |

| Regulatory Support for Home Sleep Testing & Reimbursement Expansion | +3.4% | North America, Europe, gradual Asia-Pacific uptake | Long term (≥ 4 years) |

| Integration of Sleep Data into Insurance Wellness Programs | +1.9% | North America, pilots in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Edge AI Chips Enabling Real-Time, On-Device Sleep Analytics | +2.3% | Global, led by U.S. and Asia-Pacific fabs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Sleep Disorders

An estimated 852 million adults reported experiencing insomnia symptoms in 2024, representing 16.2% of the global adult population[1]Nature Communications, “Global Burden of Sleep Apnea 2024,” nature.com. Obstructive sleep apnea diagnoses reached 936 million, yet 80% remain undiagnosed because clinic capacity cannot meet demand. In the United States, 36% of adults disclosed a diagnosed sleep disorder in 2024, underscoring a care gap that home testing can fill. FDA approval of Wakix for pediatric narcolepsy broadened the treated population, elevating demand for monitoring wearables in younger cohorts. Aging populations and rising obesity rates, notably in India and China, further intensify the worldwide incidence of sleep-disordered breathing.

Technological Advancements in Wearables, Sensors & AI

The Oura Ring Generation 4 reduced motion artifacts by 30% compared to its earlier model and introduced Advisor AI for personalized coaching. The Apple Watch Series 10 detects sleep apnea with a sensitivity above 85% using accelerometer and heart rate data. SleepViT’s ultra-low-power ASIC executes sleep-stage classification locally, minimizing latency and cloud fees[2]IEEE, “SleepViT: Ultra-Low-Power ASIC for Wearable Sleep Analytics,” ieee.org. Samsung Galaxy Watch7 raised sleep-stage concordance to 78%, narrowing the gap with clinical actigraphy. These improvements narrow the performance gap between consumer wearables and lab-grade devices, fostering physician endorsement and insurance reimbursement.

Growing Adoption of Smart-Home Ecosystems for Sleep Optimization

The Matter protocol, supported by Apple, Google, and Samsung, unifies smart-home devices so that temperature, lighting, and sound adjust to biometric cues in real-time. The Google Nest Hub utilizes Soli radar to gather contactless respiratory signals, achieving 92% accuracy compared to pulse oximetry. Withings Sleep Mat offers under-mattress sensing for users who prefer not to wear devices during the night. Circadian-aligned lighting systems that shift from 2,700 Kelvin at night to 5,500 Kelvin in the morning cut sleep-onset latency by 19% in peer-reviewed trials. As ecosystems converge, platform owners consolidate value while standalone trackers face interoperability headwinds.

Regulatory Support for Home Sleep Testing & Reimbursement Expansion

The FDA cleared ResMed’s NightOwl in April 2025, a USD 149 disposable home test that operates at one-third the cost of polysomnography. The United Kingdom’s NICE endorsed six home tests in December 2024, including AcuPebble SA100 priced at GBP 40 to GBP 60 per use, legitimizing lower-cost diagnostics. The American Academy of Sleep Medicine published technical guidance in 2024 supporting Type III home tests with up to seven channels. Medicare raised reimbursement for home testing to 80% of the allowable amount in 2025, removing a major adoption hurdle for seniors. This policy momentum compresses the path from symptom recognition to treatment initiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Sleep Tech Devices | -2.7% | Global, acute in emerging economies | Medium term (2-4 years) |

| Data Privacy and Security Concerns | -1.8% | Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Lack of Standardized Clinical Validation Protocols | -1.5% | Worldwide | Long term (≥ 4 years) |

| Supply-Chain Volatility in Sensor Components | -1.3% | Global, centered in Asia-Pacific fabs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Sleep Tech Devices

Eight Sleep’s Pod 4 Ultra retails for between USD 2,000 and USD 3,000, positioning it as a luxury purchase rather than a mass-market health tool. Sleep Number’s Climate360 bed ranges from USD 10,000 to USD 13,500, which limits its uptake to households in the highest income decile. The Oura Ring costs between USD 299 and USD 399 and requires a monthly subscription of USD 5.99 for premium analytics, which raises the total first-year ownership cost above USD 370. CPAP therapy can exceed USD 3,000 when diagnostic polysomnography is needed, delaying initiation for uninsured users. Subscription models heighten affordability concerns, especially in markets where the annual per-capita healthcare expenditure is below USD 200.

Data Privacy and Security Concerns

GDPR classifies sleep metrics as sensitive data that require explicit user consent, resulting in granular permission flows that may hinder feature adoption[3]European Commission, “General Data Protection Regulation,” gdpr.eu. HIPAA applies inconsistently to wellness devices, creating gray zones that insurers exploit when underwriting policies based on biometric data. A 2024 consumer survey found that 62% of respondents were reluctant to share their sleep data with third parties, citing concerns about discriminatory pricing. Independent penetration testing revealed firmware vulnerabilities in nine of the fifteen most popular wearables, allowing for unauthorized biometric access. GDPR fines can reach 4% of global revenue, and HIPAA breaches cost up to $50,000 per compromised record, prompting manufacturers to adopt conservative data-handling practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wearables Dominate Through Subscription Monetization

Wearables accounted for 65.43% of 2025 revenue, with the segment on track to grow at 20.43% through 2031, as edge analytics and large installed bases reinforce network effects. Oura generated USD 500 million in revenue in 2024 and converted more than 30% of owners into monthly subscribers, a model that lifts margins beyond hardware sales. Apple Watch Series 10 capitalizes on over 200 million active devices, transforming existing users into sleep-apnea patients without incremental bill-of-materials costs. The Samsung Galaxy Watch7 improved sleep-stage accuracy by 12 percentage points over the prior model, bringing the device closer to clinical relevance.

Non-wearables cater to consumers who prefer passive or environmentally friendly interventions. Eight Sleep’s Pod 4 Ultra delivers 32% gains in self-reported sleep quality via dual-zone thermal control. Sleep Number’s Climate360 integrates responsive air chambers at price points beyond USD 10,000, catering to affluent wellness adopters. ResMed’s NightOwl disposable test democratizes diagnostics at USD 149, capturing users who avoid lab studies. The Withings Sleep Mat offers under-mattress sensing but lacks multi-sensor fidelity, which limits its clinical use.

By Application: Insomnia Leads, Narcolepsy Accelerates

Insomnia accounted for 42.45% of application revenue in 2025, as cognitive behavioral therapy modules embedded in wearables gained traction. Apple’s breathing-exercise sequences reduced sleep-onset latency by 12 minutes in trials, highlighting the convergence of mental health. CPAP and related sleep-apnea devices target a diagnosed base of 936 million, yet most cases remain untreated, leaving a vast diagnostic pool. ResMed’s AirSense 11 utilizes adaptive algorithms that reduce abandonment by 18% compared to fixed-pressure systems.

Narcolepsy devices are advancing at a 20.55% CAGR, the fastest-growing segment, driven by FDA approvals that now include pediatric patients aged six and above. LUMRYZ extended-release sodium oxybate gained clearance in September 2024, with wearables offering objective adherence metrics. Restless-leg monitoring through accelerometers generates an ancillary revenue stream as limb-movement data are validated for clinical decision-making. As real-time data becomes accessible, treatment can shift from episodic office visits to continuous titration.

By End User: Homecare Settings Surge

Hospitals accounted for 55.32% of revenue in 2025, as polysomnography and surgical interventions continue to originate in inpatient settings. However, home care settings are expected to enjoy a 21.56% CAGR as Medicare reimbursement improves and cloud platforms transmit CPAP adherence data directly to clinicians. ResMed’s AirView platform reduced therapy abandonment by 22% compared to quarterly check-ups, demonstrating the efficacy of remote monitoring.

Sleep labs are facing shrinking volumes after the AASM guidelines allowed Type III home testing for moderate-risk patients. Employer wellness programs, such as UnitedHealthcare Motion, pay members up to USD 1,500 per year for meeting sleep targets and integrating devices into productivity strategies. The migration from hospital to home aligns with broader value-based care models that reward outcomes rather than service intensity.

By Distribution Channel: E-Commerce Gains Share

Offline retail accounted for 41.45% of 2025 sales, driven by consultative selling that eases buyers into high-ticket purchases. Best Buy’s partnership with Oura lets shoppers verify ring sizing in more than 850 U.S. outlets. Durable-equipment suppliers bundle insurance pre-authorizations with CPAP sales, sustaining brick-and-mortar relevance.

Direct-to-consumer e-commerce is projected to rise at 21.45% through 2031, as brands capture full margins and mine first-party data. Eight Sleep’s Plus plan generates USD 24 monthly per user, adding recurring revenue on top of a USD 2,000 base product. Amazon processed over 40 million sleep-related orders in 2024, utilizing Prime logistics to reduce delivery friction. For wearables priced below USD 400, online convenience outweighs showroom experiences, steering share away from physical channels.

Geography Analysis

North America retained 42.87% of revenue in 2025 as high insurance coverage and early FDA clearances fostered adoption. ResMed generated USD 2.3 billion in 2024 Americas revenue, reflecting robust CPAP uptake and growth in cloud subscriptions. Canada expanded provincial reimbursement for home testing, extending access beyond urban sleep labs.

The Asia-Pacific region records the fastest trajectory, with a 19.43% CAGR. China’s sleep tech devices market surpassed USD 1.2 billion in 2024, driven by e-commerce penetration exceeding 50% and the government's emphasis on preventive health. India’s market, estimated at USD 300 million in 2024, benefits from a shift to local manufacturing that lowers average retail prices. Xiaomi’s Mi Band 8 Pro, selling for USD 50, democratizes tracking for cost-sensitive buyers. Huawei captured a 15% share of China’s wearables segment by integrating TruSleep algorithms into the Watch GT 4.

Europe’s growth lags due to GDPR compliance costs and country-specific reimbursement hurdles. NICE guidance in the United Kingdom approved six home tests priced well below lab studies, signaling payer openness to lower-cost diagnostics. Germany’s statutory insurance now funds CE-marked wearables for insomnia, provided there is evidence of equivalence to CBT-I. The Middle East and Africa, while smaller, are expanding in double digits as Gulf states invest in digital health strategies. South America’s adoption trails because average device prices equal more than 20% of monthly household income, restricting uptake to affluent urban users.

Competitive Landscape

Competition is intensifying as consumer electronics leaders exploit their installed bases to layer medical features onto mainstream devices. ResMed and Philips still command about 60% of the therapeutic hardware space yet increasingly contend with wearables that claim diagnostic-grade accuracy. Apple’s September 2024 clearance enables it to target 936 million potential sleep apnea users through its existing smartwatch ecosystem. Oura, a private firm, scaled revenue to USD 500 million in 2024 by combining hardware margins with a subscription share above 30%.

Eight Sleep employs a hardware-as-a-service model, charging monthly fees to deliver continuous firmware upgrades and concierge support, thereby insulating itself from the commoditization of hardware. Qualcomm amassed a dozen 2024 patents covering low-power neural processors that underpin next-generation wearables, while Google advances Soli radar for contactless monitoring. Smaller innovators such as Dreem SAS secure high-grade EEG accuracy but struggle with distribution scale, revealing a barrier for clinically focused startups.

White-space opportunities lie in pediatric monitoring and sub-USD 100 wearables optimized for offline analytics in emerging markets. As reimbursement frameworks mature and regulators close the gap between wellness and medical devices, incumbents with silicon design capabilities and cloud platforms will likely consolidate their share.

Sleep Tech Devices Industry Leaders

Casper

Compumedics Limited

Huawei Technologies Co., Ltd.

Nihon Kohden Corporation

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SleepRes, Inc. received FDA 510(k) clearance for its Kricket PAP device, powered by Kairos Positive Airway Pressure (KPAP). The device treats obstructive sleep apnea (OSA) in patients over 66 pounds. It is suitable for use at home, hospitals, and sleep centers.

- January 2026: LumiMind launched LumiSleep at CES 2026 in Las Vegas, a groundbreaking sleep device utilizing millisecond real-time EEG modulation and personalized sound. The device aims to guide the brain into its natural Sleep Onset Pattern through non-invasive, at-home neural guidance. LumiSleep is set for official release in the first half of 2026.

- September 2025: Somnee launched its next-generation AI-powered smart sleep headband. The device is designed to help users fall asleep faster, achieve deeper recovery, and optimize overall sleep performance. It leverages advanced AI technology to personalize sleep insights and improve sleep quality.

Global Sleep Tech Devices Market Report Scope

As per the scope of the report, sleep tech devices are designed to monitor and improve the outcome in patients with sleep disorders such as sleep apnea, insomnia, narcolepsy, etc.

The Sleep Tech Devices Market is Segmented by Product Type (Wearables and Non-Wearables), Application (Insomnia, Obstructive Sleep Apnea, Narcolepsy, and Restless Leg Syndrome & Other Disorders), End User (Hospitals, Sleep Labs & Clinics, Homecare Settings, and Wellness Centers & Corporate Programs), Distribution Channel (Online E-Commerce & D2C, and Offline Retail & Specialty Stores), and Geography (North America, Europe, Asia-Pacific, Middle East And Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Wearables | Smart Watches & Bands |

| Smart Rings | |

| Other Wearable Devices | |

| Non-Wearables | Sleep Monitors (Under-Mattress / Bedside) |

| Smart Beds & Mattresses | |

| Other Non-Wearable Devices |

| Insomnia |

| Obstructive Sleep Apnea |

| Narcolepsy |

| Restless Leg Syndrome & Other Disorders |

| Hospitals |

| Sleep Labs & Clinics |

| Homecare Settings |

| Wellness Centers & Corporate Programs |

| Online (E-Commerce & D2C) |

| Offline Retail & Specialty Stores |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | GCC | |

| Rest Of South America | Turkey | |

| By Product Type | Wearables | Smart Watches & Bands | |

| Smart Rings | |||

| Other Wearable Devices | |||

| Non-Wearables | Sleep Monitors (Under-Mattress / Bedside) | ||

| Smart Beds & Mattresses | |||

| Other Non-Wearable Devices | |||

| By Application | Insomnia | ||

| Obstructive Sleep Apnea | |||

| Narcolepsy | |||

| Restless Leg Syndrome & Other Disorders | |||

| By End User | Hospitals | ||

| Sleep Labs & Clinics | |||

| Homecare Settings | |||

| Wellness Centers & Corporate Programs | |||

| By Distribution Channel | Online (E-Commerce & D2C) | ||

| Offline Retail & Specialty Stores | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest Of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest Of Asia-Pacific | |||

| Middle East And Africa | GCC | ||

| South Africa | |||

| Rest Of Middle East And Africa | |||

| South America | Brazil | ||

| Argentina | GCC | ||

| Rest Of South America | Turkey | ||

Key Questions Answered in the Report

What is the current valuation of the sleep tech devices market?

The sleep tech devices market size reached USD 34.74 billion in 2026 and is projected to climb to USD 79.88 billion by 2031.

Which product category holds the largest revenue share?

Wearables lead the field, accounting for 65.43% of 2025 revenue thanks to their continuous monitoring and subscription models.

Which region is expected to expand fastest through 2031?

Asia-Pacific posts the quickest growth with a forecast 19.43% CAGR, driven by urbanization and rising middle-class spending.

How are regulatory changes influencing adoption?

FDA and Medicare decisions that reimburse home sleep tests at higher rates reduce barriers and accelerate at-home diagnostics.

What factors limit mass-market penetration?

High device prices and persistent data-privacy concerns continue to constrain uptake, especially in emerging economies.

Which application segment is growing most rapidly?

Devices aimed at managing narcolepsy show the highest growth, projecting a 20.55% CAGR as pediatric approvals widen the user base.

Page last updated on: