Situational Awareness Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

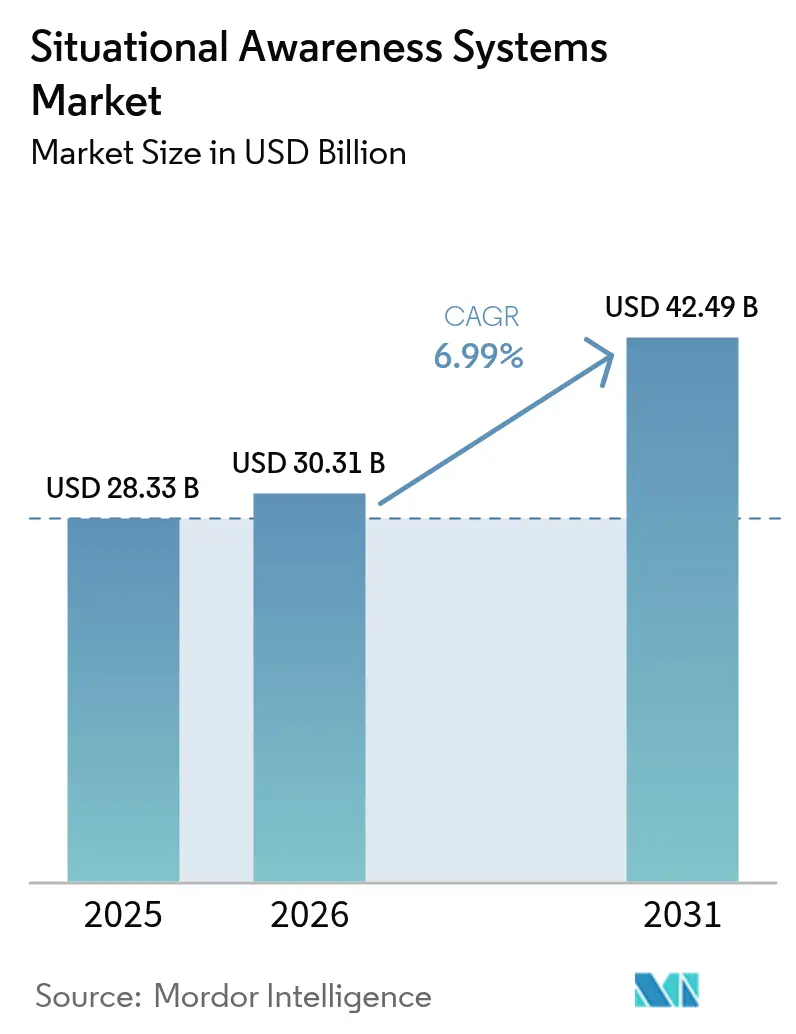

| Market Size (2026) | USD 30.31 Billion |

| Market Size (2031) | USD 42.49 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

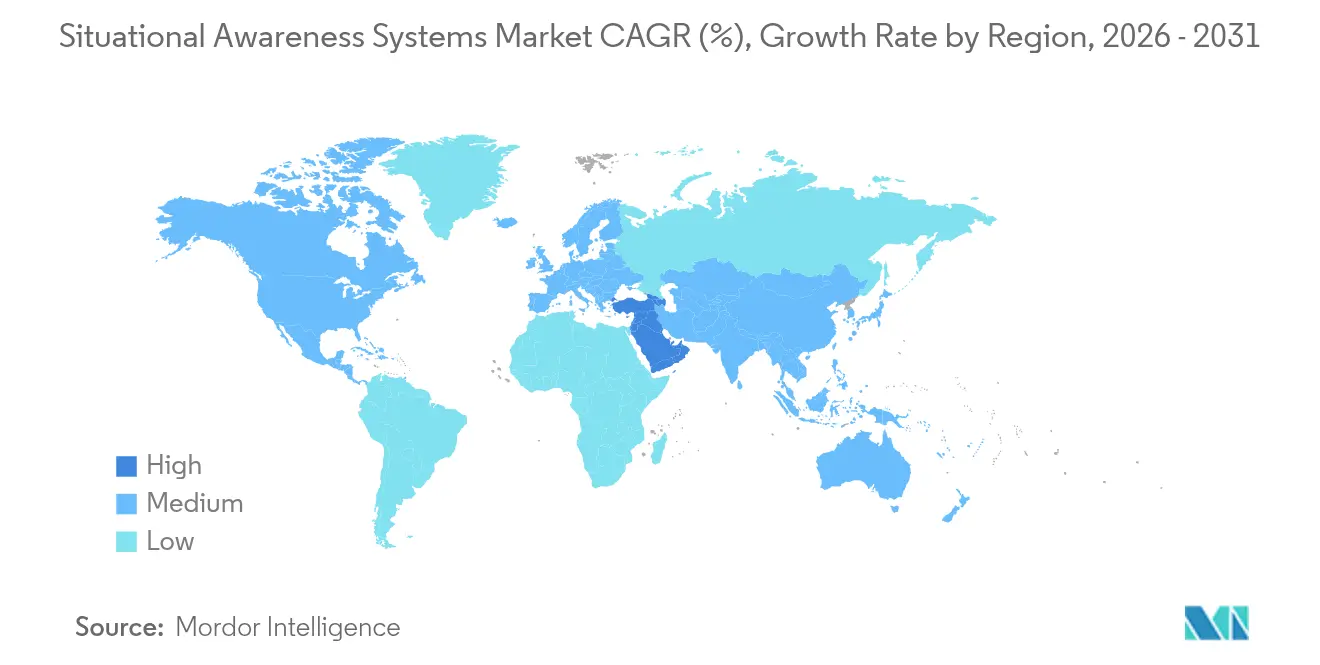

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Situational Awareness Systems Market Analysis by Mordor Intelligence

The situational awareness systems market size was valued at USD 28.33 billion in 2025 and estimated to grow from USD 30.31 billion in 2026 to reach USD 42.49 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031). Demand is accelerating as defense ministries invest in AI-enabled sensor fusion, CubeSat constellations, and open-architecture command platforms that support multi-domain operations. NATO interoperability mandates, QUAD security cooperation, and the rise of smart-city security programs are broadening the user base beyond the military. Asia-Pacific dominates current revenues, while Gulf countries allocate record budgets to counter regional threats. At the platform level, land systems remain the largest revenue contributors, but air and space segments are where double-digit growth pipelines are forming. Component suppliers are shifting toward software-defined upgrades, allowing operators to refresh capability without expensive hardware swaps. Competitive intensity is rising as large integrators seek partnerships with AI specialists to defend their share against software-centric entrants.

Key Report Takeaways

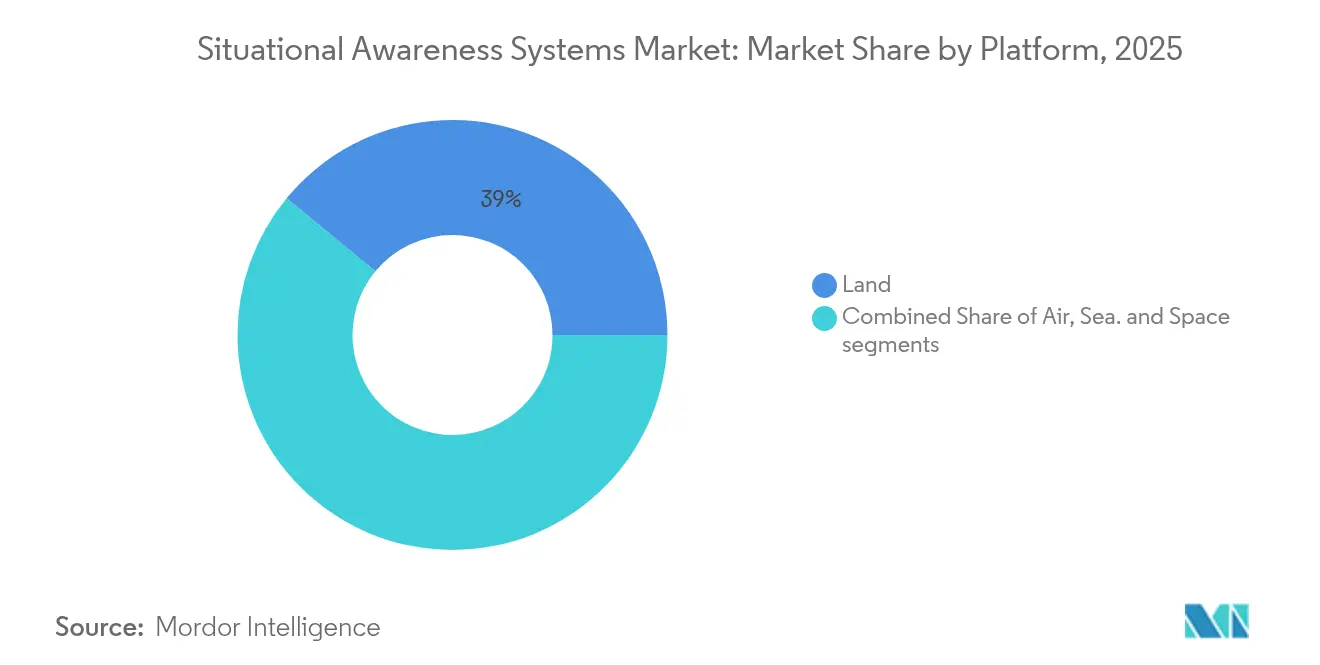

- By platform, land systems led with a 39.02% market share of situational awareness systems in 2025; air platforms are forecasted to post the fastest growth rate of 8.05% through 2031.

- By type, command and control solutions accounted for 29.05% of 2025 revenue, while optronics and EO/IR technologies are expected to expand at an 7.86% CAGR through 2031.

- By component, processing and computing units held a 33.74% share of the situational awareness systems market size in 2025; software is projected to grow at a 7.62% CAGR over the 2026-2031 period.

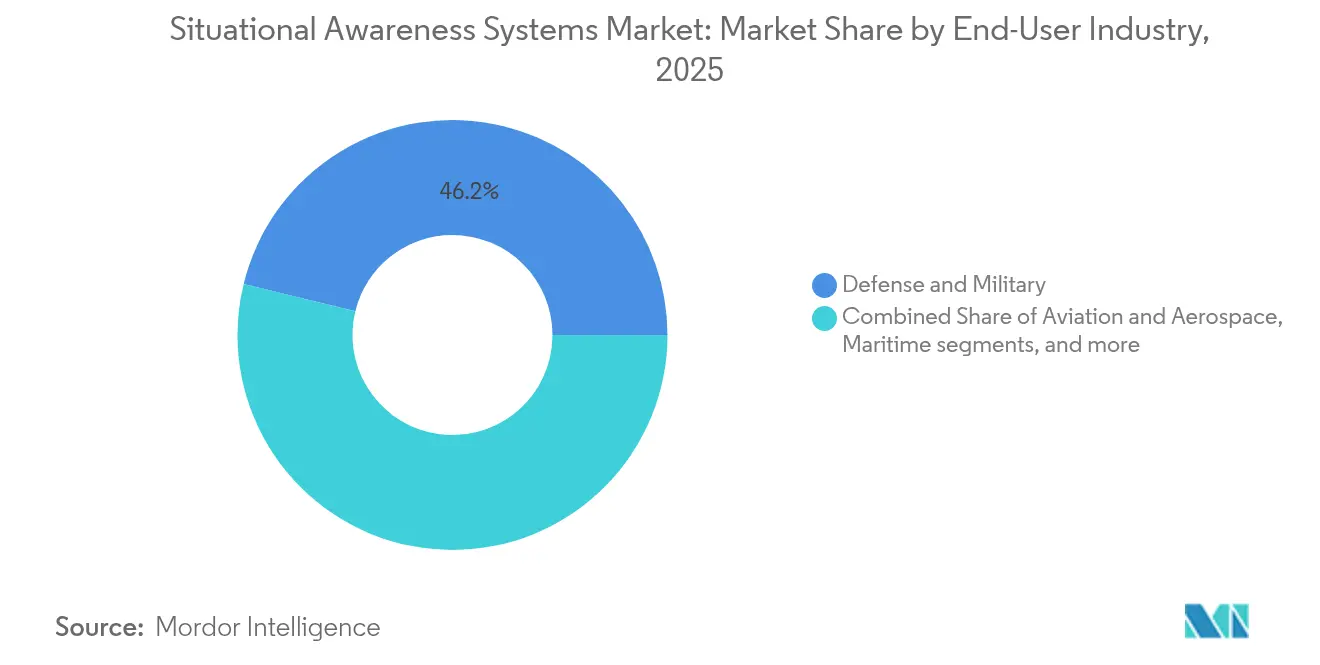

- By end-user, the defense segment maintained a 46.18% share in 2025, while aviation and aerospace applications are advancing at an 7.98% CAGR.

- By application, C4ISR and battle management represented 40.66% of 2025 revenue; security and surveillance use cases are anticipated to grow at a 9.05% CAGR.

- By geography, the Asia-Pacific captured 38.12% of global revenue in 2025, and the Middle East is poised for the fastest growth, with a 10.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Situational Awareness Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating defense modernization budgets | +1.8% | Global (strongest in APAC and North America) | Medium term (2-4 years) |

| Surge in autonomous and remotely-piloted platforms | +1.5% | Global (led by North America and Europe) | Short term (≤ 2 years) |

| Dual-use demand from critical infrastructure and smart-city security | +1.2% | North America and EU; expanding to APAC cities | Long term (≥ 4 years) |

| NATO and QUAD interoperability mandates | +0.9% | North America, Europe, APAC allies | Medium term (2-4 years) |

| Proliferation of CubeSat space-based sensing constellations | +0.8% | Global (early deployment in North America) | Long term (≥ 4 years) |

| AI-driven sensor-fusion reducing operator cognitive load | +0.7% | Global (tech-advanced markets first) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Defense Modernization Budgets

Global procurement cycles are shifting toward systems that can integrate data from air, land, sea, and space on a single platform. The US Department of Defense FY2025 request boosts funding for AI-enabled command nodes, while Asia-Pacific governments channel rising budgets into indigenous solutions that lessen foreign dependency. Lockheed Martin reported USD 18 billion in Q1 2025 sales, underpinned by integrated sensor packages embedded in missile and fire-control programs. Higher spending aligns with sovereign capability goals, creating consistent demand for modular, upgradeable situational awareness architectures.

Surge in Autonomous and Remotely-Piloted Platforms

The tri-service adoption of unmanned aircraft, ground vehicles, and maritime drones creates new requirements for onboard processing that can classify and prioritize threats without continuous human oversight. Boeing’s involvement in the Next Generation Air Dominance program underscores the development of sixth-generation fighter roadmaps, which center on AI-driven autonomy and adaptive engines.[1]Boeing, “Next Generation Air Dominance Program Update,” boeing.com RTX successfully flight-tested machine-learning radar-warning receivers that retrofit legacy fighters with cognitive threat prioritization.[2]RTX, “Machine-Learning Radar Warning Receiver Demonstration,” rtx.com The same logic underpins counter-UAS solutions, such as Honeywell’s modular Reveal and Intercept package, which integrates EO/IR sensors with RF detectors to neutralize drone swarms.

Dual-Use Demand from Critical Infrastructure and Smart-City Security

Critical infrastructure operators utilize defense-grade sensor fusion to monitor pipelines, ports, and power grids, while municipalities integrate command-center technology into their traffic and public safety platforms. The US Naval Information Warfare Center’s USD 125 million SeaVision deployment for India demonstrates maritime surveillance tools migrating into civilian vessel-tracking roles. Europe’s MARSUR III program enables 20 nations to share maritime data between defense and coast-guard users, underscoring a multi-mission value proposition.[3]European Defence Agency, “MARSUR III Project Overview,” eda.europa.eu

NATO and QUAD Interoperability Mandates

Alliance doctrines prescribe seamless data sharing across heterogeneous fleets. The Global Combat Air Programme, which links the UK, Japan, and Italy, requires common avionics standards and synchronized production workflows. Thales is coordinating the EISNET consortium of 23 partners to establish uniform Integrated Air and Missile Defence interfaces across Europe. Vendors that can certify their products against these open standards secure long-term export pathways.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and lifecycle costs | –1.3% | Global (especially smaller defense budgets) | Medium term (2-4 years) |

| Cyber-security vulnerabilities in network-centric ops | –0.8% | Global (heightened concern in NATO nations) | Short term (≤ 2 years) |

| RF-spectrum congestion causing sensor interference | –0.6% | Global (acute in dense urban and contested areas) | Medium term (2-4 years) |

| Tightening export controls on advanced imaging sensors | –0.5% | Global (notably affects international trade) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Lifecycle Costs

The total cost of ownership extends well beyond initial procurement, encompassing operator training, sovereign crypto modules, software sustainment, and mid-life sensor refresh. Smaller defense budgets often defer or pool purchases, prompting the development of joint frameworks, such as NATO Support and Procurement Agency agreements. Software-intensive architectures incur recurring cyber-compliance expenses that can exceed hardware outlays over a 20-year lifespan.

Cyber-Security Vulnerabilities in Network-Centric Operations

The same connectivity that enables real-time domain awareness creates lucrative attack surfaces. Adversaries target unsecured data links and unpatched mission computers to disrupt decision-making processes. Governments now demand zero-trust architectures, post-quantum encryption, and secure supply-chain attestations before fielding new situational awareness suites. Integrators that pre-build cryptographic agility and cyber-resilience into their platforms gain procurement preference.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Land Dominance Drives Multi-Domain Integration

Land platforms controlled 39.02% of situational awareness systems market revenue in 2025, underpinned by mobile command centers and armored vehicle electronics. Integrated battle-management networks fuse feeds from ground radars, acoustic sensors, and dismounted soldier systems into a common operating picture. However, air platforms are pacing future growth at an 8.05% CAGR as next-generation fighters and Group 5 drones standardize panoramic sensor suites. The market size of situational awareness systems for air platforms is expected to grow rapidly, driven by the need to operate within contested airspace with degraded GPS. CubeSats increasingly extend ground forces' horizons, tying into handheld terminals that have supplanted legacy line-of-sight radios.

Space assets form the youngest but most disruptive layer. Persistent low-earth-orbit constellations beam tactical data straight to edge processors, closing observe-orient-decide loops from minutes to seconds. Sea platforms continue to invest in surface-ship air-defense sensors, while harbor security projects adopt unmanned surface vessels for autonomous patrol. Collectively, multi-domain integration favors open middleware that allows operators to reconfigure sensors across theaters without requiring the rewriting of core code. Proprietary stovepipes are losing ground to modular plug-and-play frameworks demanded by coalition planners.

By Type: Command Systems Lead While Optronics Accelerate

Command and control hubs generated 29.05% of 2025 revenue, underscoring their status as the orchestrating nerve center for every sensor node. These systems translate diverse inputs, such as radar tracks, AIS ship data, and electronic support measures, into actionable tasks. Running advanced algorithms at the edge within the next five years will lift their share of the situational awareness systems market size for C2 suites.

Optronics and EO/IR technologies, though smaller today, are expanding at an 7.86% CAGR as resolution, night-vision range, and thermal sensitivity improve. RTX’s RAIVEN family achieves five-fold detection range gains by coupling hyperspectral, lidar, and AI filtering in one gimbal. Radar remains indispensable for all-weather detection, yet the gap between radio-frequency and optical sensing narrows as software combines cues. SONAR retains its niche in submarine tracking, whereas vehicle ADAS kits borrow military heritage to assist convoy autonomy in low-visibility environments. The situational awareness systems market now favors sensor diversity over single-modality supremacy.

By Component: Processing Power Drives Software Innovation

Processing and computing units captured 33.74% of the revenue in 2025, reflecting insatiable demand for GPUs and real-time signal processors capable of processing multispectral feeds. Edge computing eliminates satellite latency and ensures commanders receive coherent tracks even when data links drop. Software, meanwhile, is the fastest riser, with a 7.62% CAGR, as containerized microservices allow users to add AI upgrades through cloud-style updates rather than depot visits.

Sensors and antennas continue to shrink, benefiting small-form-factor Group 1 drones that relay ISR data to truck-mounted fire-direction centers. Displays evolve from fixed multifunction units to helmet-mounted augmented-reality overlays. Universal Avionics’ ClearVision system, selected by Boom Supersonic, overlays symbology onto the pilot’s field of view during low-visibility departure. Networking hardware now embeds mobile ad-hoc waveforms, automatically forming secure meshes within jammed environments.

By End-User Industry: Defense Leads While Aviation Accelerates

Defense ministries constituted 46.18% of 2025 spending, continuing to anchor the situational awareness systems market. Live-synthetic training and contested-space readiness ensure procurement remains robust, even amid budget scrutiny. Yet, commercial aviation and spaceflight are projected to grow at the fastest 7.98% CAGR as regulators adopt military-grade traffic-collision algorithms for crowded urban air-mobility corridors.

Homeland security agencies integrate border-surveillance towers, coastal radar, and AI-enabled video analytics to safeguard critical infrastructure. Maritime operators adopt unmanned surface vehicles equipped with ISR masts to patrol offshore energy installations. Emergency-management entities deploy ruggedized command tablets that run the same decision tools once reserved for theater commanders. The situational awareness systems industry benefits from certifications such as DO-178C, which expedite the adoption of dual-use systems.

By Application: C4ISR Dominance Meets Surveillance Growth

C4ISR and battle-management accounts for 40.66% of 2025 spending, cementing its role as the digital backbone of modern joint forces. The situational awareness systems market share for C4ISR platforms remains high as commanders prioritize fused sensor mosaics and automated course-of-action recommendations.

Security and surveillance is the breakout growth engine, with a 9.05% CAGR. City authorities in Europe and North America deploy integrated dashboards that combine traffic cameras, license-plate readers, and chemical sensor alerts. Disaster-response teams, meanwhile, leverage satellite imagery fed through AI classifiers to allocate relief assets minutes after a cyclone. Navigation and traffic-control applications incorporate GNSS-independent inertial sensors to maintain air lanes during GNSS jamming. Simulation software streamlines training cycles by replicating exact sensor behaviors, enabling crews to rehearse emerging threat scenarios before deployment.

Geography Analysis

The Asia-Pacific region held 38.12% of global revenue in 2025, as China, India, Japan, South Korea, and Australia executed overlapping modernization roadmaps. Indigenous sensor fabrication programs receive preferential financing, while foreign suppliers secure contracts through offset and technology-transfer clauses. India’s Defense Acquisition Procedure streamlines approval for imported radio-frequency chips that feed into locally assembled command modules. Japanese participation in the Global Combat Air Programme aligns its next-generation fighter cockpit with European human-machine interface standards, enabling the establishment of shared supply chains.

The Middle East is forecasted to deliver a 10.18% CAGR to 2031. Saudi Arabia’s Vision 2030 requires 50% domestic content in new situational awareness suites, steering integrators such as Thales toward local joint ventures. UAE air forces embed CubeSat downlinks into pilot helmets for real-time maritime situational pictures over the Strait of Hormuz. Israel continues to export software-centric sensor fusion, often bundled with active cyber-defense layers specifically tuned for desert environments that are susceptible to thermal clutter.

North America maintains technology leadership through sustained US DoD outlays. The Pentagon’s Joint All-Domain Command and Control (JADC2) initiative finances open-standards middleware that primes the US for export wins. Canada upgrades Arctic surveillance radars to track hypersonic glide vehicles. Europe emphasizes interoperability: the EISNET consortium classifies threat libraries so that German, French, and Italian missile defense operators interpret sensor cues identically. Africa and South America remain emerging adopters; Colombia’s coastal radar overhaul and Nigeria’s pipeline-monitoring drone program illustrate how civil-security missions often precede full defense adoption.

Competitive Landscape

In the situational awareness systems market, a handful of major players dominate, yet niche specialists still find their footing. Companies like Lockheed Martin Corporation, RTX Corporation, and BAE Systems plc are not just selling products; they're enhancing their offerings. For instance, Lockheed Martin's F-35 Tech Refresh 3 not only upgrades processors but also paves the way for future AI capabilities. Meanwhile, RTX showcases its strategy by integrating cognitive electronic support measures into current radar pods, highlighting the lucrative potential of their established installations.

Mid-tier challengers, such as L3Harris, Saab, and Leonardo, differentiate through open-architecture kits that retrofit aging fleets. Saab's Giraffe 1X radar integrates with third-party command software via NATO-compliant data models, shortening deployment timelines for small nations. Meanwhile, technology disruptors focus on AI inference engines that combine disparate sensor feeds on handheld devices. California-based Palantir and UK-based Adarga license machine learning algorithms to defense ministries that prefer commercial refresh cycles.

Partnerships between hardware and software specialists are proliferating. Honeywell teams with Shield AI to embed autonomy in perimeter-security drones; Airbus pairs with Helsing to inject AI air-combat maneuver libraries into manned-unmanned teaming concepts. Vendors that can certify their products as cyber-hardened and export-compliant, utilizing open standards, gain bidding advantages as governments strive to avoid vendor lock-in.

Situational Awareness Systems Industry Leaders

Lockheed Martin Corporation

RTX Corporation

Northrop Grumman Corporation

Honeywell International Inc.

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lockheed Martin received a USD 1 billion contract to advance US hypersonic weapon systems, incorporating enhanced situational awareness capabilities.

- May 2025: The US Naval Information Warfare Center launched a USD 125 million initiative to expand India’s maritime domain awareness through SeaVision analytics.

- April 2025: 3dB Labs secured a USD 6.1-million contract with the US Army to create and showcase an electromagnetic spectrum situational awareness system tailored for combat units.

- April 2025: NATO selected Thales to implement the third phase of its NCOP (NATO Common Operational Picture) initiative, dubbed “NCOP-BMD”. The NCOP aims to furnish NATO commanders with a cohesive, real-time overview of operational theaters and emerging threats, thereby enhancing the situational awareness of joint forces.

Global Situational Awareness Systems Market Report Scope

The study assimilates data on situational awareness systems used by security forces, military, and other agencies involved in coordinated activities for various security and support operations. Furthermore, innovations in terms of the situational awareness system and the development of newer related technologies are also discussed in the report.

The situational awareness systems market is segmented by platform, type, and geography. By platform, the market has been segmented into air, land, sea, and space. By type, the market has been segmented into command and control, RADAR, SONAR, optronics, and vehicle situational awareness systems. The report also covers the market sizes and forecasts for the market across major regions. For each segment, the market sizing and forecasts have been done based on value (USD billion).

| Air |

| Land |

| Sea |

| Space |

| Command and Control Systems |

| RADAR |

| SONAR |

| Optronics and EO/IR |

| Vehicle SAS/ADAS |

| Sensors and Antennas |

| Displays and HUDs |

| Processing/Computing Units |

| Communications and Networking Hardware |

| Software |

| Defense and Military |

| Homeland Security and Public Safety |

| Aviation and Aerospace |

| Maritime |

| C4ISR and Battle Management |

| Security and Surveillance |

| Disaster Response and Emergency Management |

| Navigation and Traffic Control |

| Environmental/Weather Monitoring |

| Training and Simulation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Air | ||

| Land | |||

| Sea | |||

| Space | |||

| By Type | Command and Control Systems | ||

| RADAR | |||

| SONAR | |||

| Optronics and EO/IR | |||

| Vehicle SAS/ADAS | |||

| By Component | Sensors and Antennas | ||

| Displays and HUDs | |||

| Processing/Computing Units | |||

| Communications and Networking Hardware | |||

| Software | |||

| By End-User Industry | Defense and Military | ||

| Homeland Security and Public Safety | |||

| Aviation and Aerospace | |||

| Maritime | |||

| By Application | C4ISR and Battle Management | ||

| Security and Surveillance | |||

| Disaster Response and Emergency Management | |||

| Navigation and Traffic Control | |||

| Environmental/Weather Monitoring | |||

| Training and Simulation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the situational awareness systems market?

The market is valued at USD 30.31 billion in 2026 and is projected to reach USD 42.49 billion by 2031, advancing at a 6.99% CAGR. .

Which region generates the highest revenue?

Asia-Pacific contributes 38.12% of global revenue thanks to sustained modernization initiatives across China, India, Japan, and South Korea.

Which platform category is growing fastest?

Air platforms are forecasted to expand at an 8.05% CAGR as next-generation fighters and unmanned aerial systems demand advanced sensor fusion.

What is the leading application segment?

C4ISR and battle-management systems hold 40.66% of revenue, reflecting their centrality to joint operations.

How are software solutions impacting the market?

Software is the fastest-growing component at 7.62% CAGR because containerized updates let operators add AI capabilities without hardware replacement.

What is the main restraint to wider adoption?

High acquisition and lifecycle costs continue to limit uptake among smaller defense budgets, as ongoing cyber-security and software sustainment expenses elevate total ownership costs.

Page last updated on: