Single-Use Bioprocessing Probes And Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

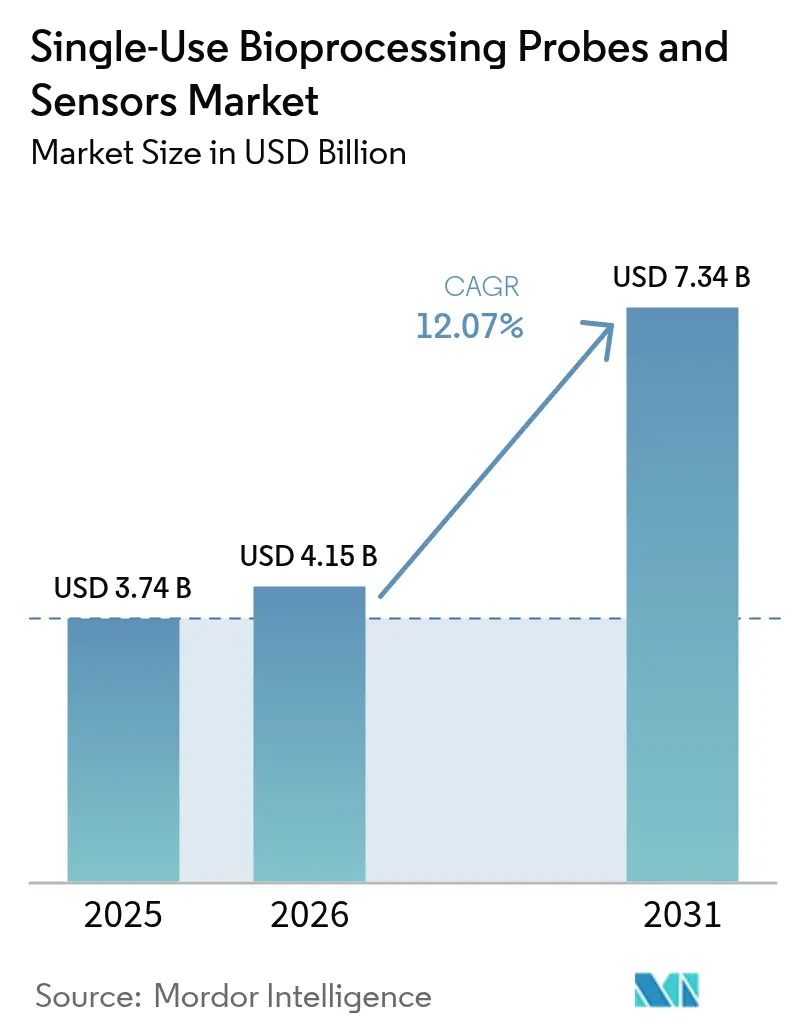

| Market Size (2026) | USD 4.15 Billion |

| Market Size (2031) | USD 7.34 Billion |

| Growth Rate (2026 - 2031) | 12.07% CAGR |

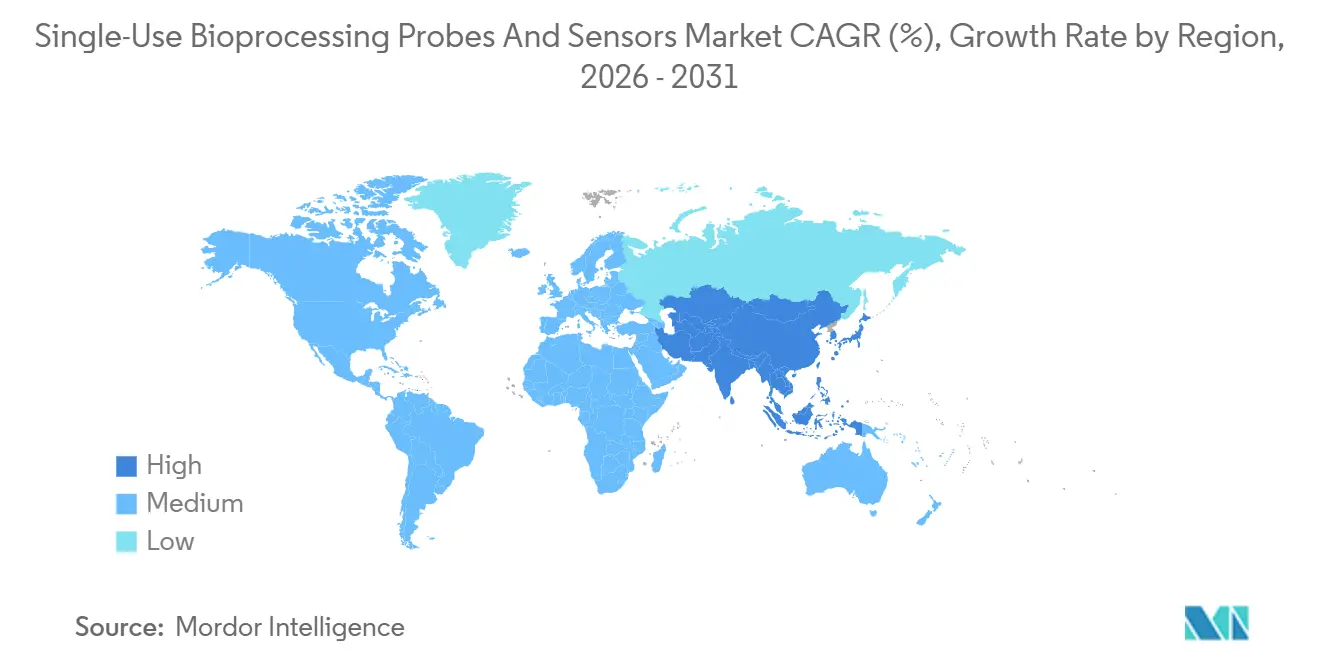

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

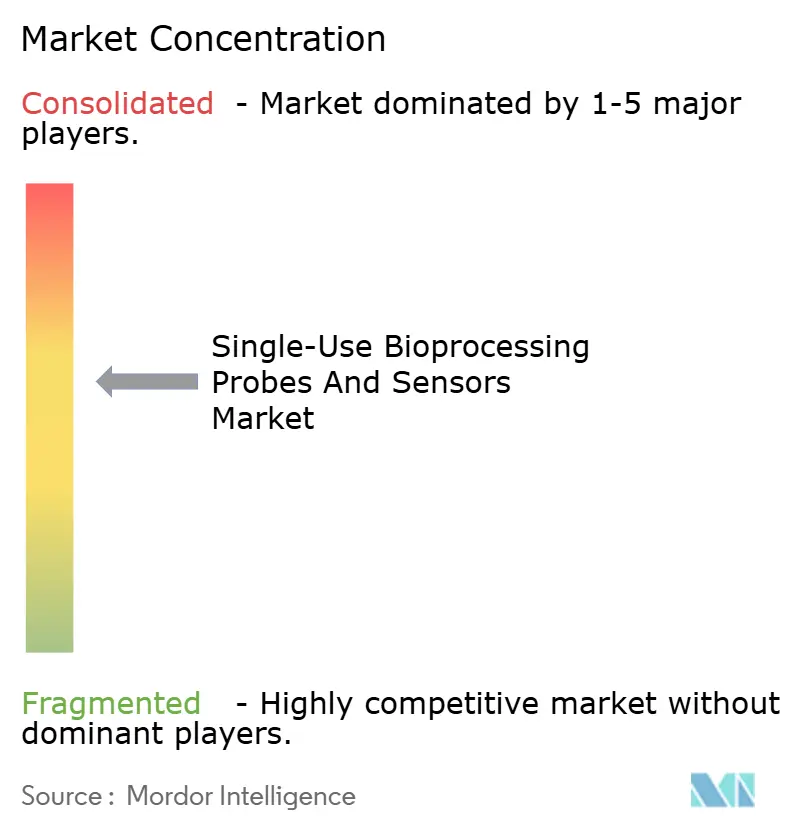

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single-Use Bioprocessing Probes And Sensors Market Analysis by Mordor Intelligence

The Single-Use Bioprocessing Probes And Sensors Market size is expected to increase from USD 3.74 billion in 2025 to USD 4.15 billion in 2026 and reach USD 7.34 billion by 2031, growing at a CAGR of 12.07% over 2026-2031.

Contract manufacturers drive early adoption because disposables remove cross-contamination risk and shrink changeover time, an advantage when a single suite must pivot across multiple clients in a week. Optical technologies, especially Raman and near-infrared spectroscopy, are rising because they deliver real-time metabolite data without sampling, cutting offline testing by nearly half. At the same time, sterilization compatibility is shifting toward X-ray and e-beam formats that preserve optical-fiber integrity. Policy moves such as the U.S. Inflation Reduction Act and the EU Critical Raw Materials Act are nudging suppliers to localize polymer and sensor assembly, compressing lead times from 16 weeks to 8 weeks and insulating margins from currency swings.[1]European Commission, “Critical Raw Materials Act,” ec.europa.eu

Key Report Takeaways

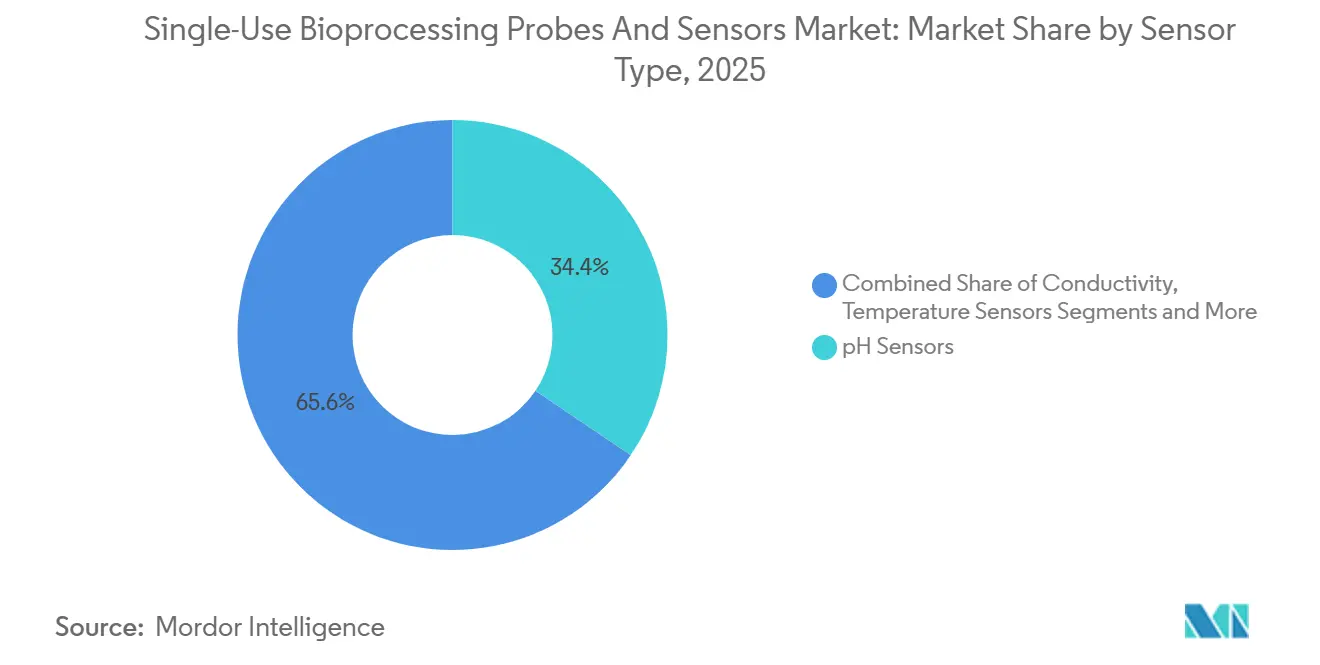

- By sensor type, pH devices held 34.43% of the single-use bioprocessing probes and sensors market share in 2025, while optical and multi-parameter sensors are advancing at a 15.23% CAGR through 2031.

- By detection technology, electrochemical methods led with 56.13% share in 2025; optical approaches are forecast to climb at 14.89% CAGR to 2031.

- By application, upstream operations captured 59.55% share of the 2025 single-use bioprocessing probes and sensors market size, whereas quality-control workflows are projected to grow at 14.05% CAGR.

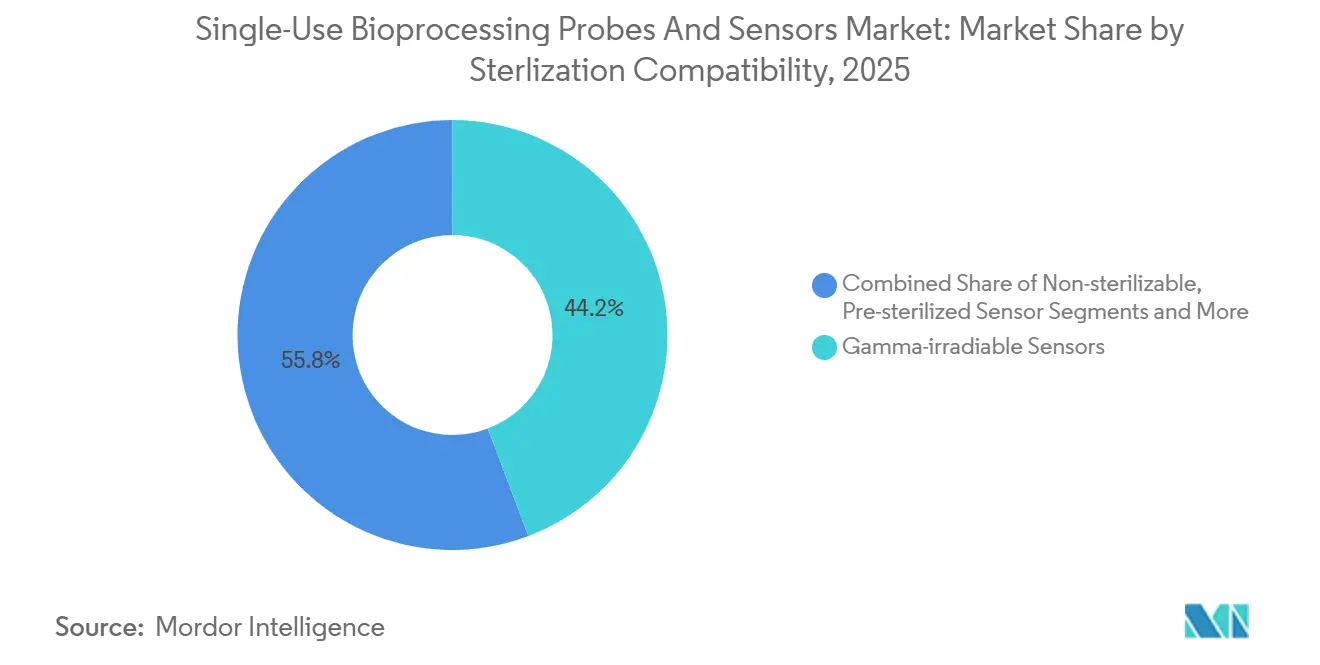

- By sterilization compatibility, gamma-irradiable formats led with 44.25% share in 2025; X-ray and e-beam-ready devices are the fastest movers at 16.14% CAGR.

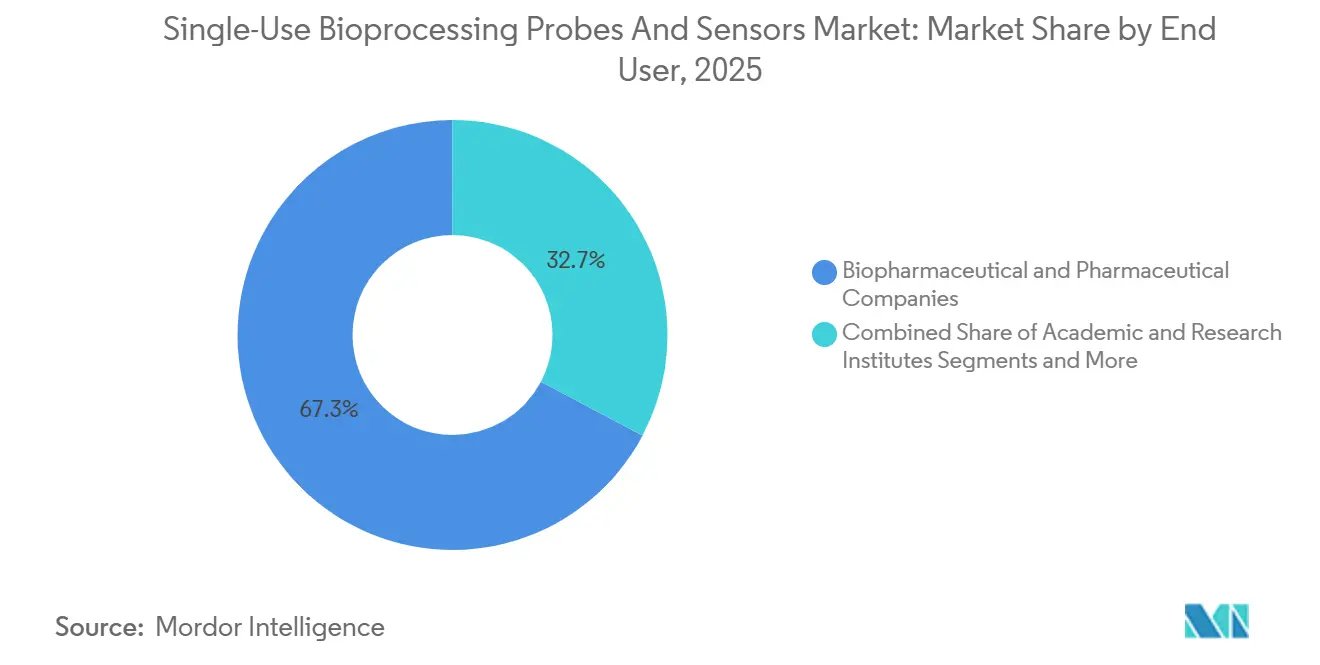

- By end user, biopharma and pharma companies represented 67.26% of 2025 demand, while academic and research institutes are expanding at 15.83% CAGR to 2031.

- By geography, North America held 37.82% of revenue in 2025, but Asia-Pacific is set to post the quickest growth at a 14.77% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Single-Use Bioprocessing Probes And Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Single-Use Technologies in Biologics Manufacturing | +2.8% | Global, with concentration in North America and Western Europe | Medium term (2–4 years) |

| Expanding Pipeline of Cell & Gene Therapies Demanding Flexible Monitoring | +2.3% | North America, Asia-Pacific (China, Singapore, South Korea) | Long term (≥ 4 years) |

| Growth of CMOs/CDMOs Accelerating Disposable-Probe Procurement | +2.1% | Global, strongest in North America and emerging in Asia-Pacific | Short term (≤ 2 years) |

| Standardization of Single-Use Sensor Formats by Industry Consortia | +1.5% | Global, led by BPSA and ISPE working groups | Medium term (2–4 years) |

| Integration of Disposable Sensors with Digital Twins & Real-Time Analytics | +1.9% | North America, Europe, select Asia-Pacific hubs | Medium term (2–4 years) |

| Tariff-Driven Regionalization of Sensor Supply Chains | +1.2% | North America, Europe, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Single-Use Technologies in Biologics Manufacturing

Biologics pipelines are shifting to single-use systems because fixed stainless infrastructure cannot flex with rising molecule diversity. Pfizer noted that 60% of its clinical biologics used disposables in 2025, up from 38% in 2022, and predicts single-use sensors will command 75% of its process-analytics spend by 2028. Facilities producing antibody–drug conjugates prefer disposables because surfaces must be discarded to eliminate cytotoxic residue. Pre-calibrated, irradiated sensors align with this model and compress changeovers from five days to less than 24 hours. FDA’s 2024 continuous-manufacturing guidance legitimized factory calibration, erasing a compliance roadblock that once favored reusable probes.[2]U.S. Food and Drug Administration, “Guidance for Continuous Manufacturing,” fda.gov

Expanding Pipeline of Cell & Gene Therapies Demanding Flexible Monitoring

Autologous CAR-T manufacturing runs patient-specific batches in parallel, each needing separate pH and dissolved-oxygen monitoring. Novartis reported deploying 340 single-use sensor sets per month across its facilities in 2025, nearly triple 2023 volume. Installing reusable probes in every vessel would lock in USD 1.2 million in capital per suite, versus a monthly USD 85,000 consumables bill with no validation labor. Viral-vector producers add complexity because adherent cultures demand distributed sensing that wired probes cannot supply, but wireless disposables manage with ease.

Growth of CMOs/CDMOs Accelerating Disposable-Probe Procurement

Multi-client plants cannot afford downtime to clean and re-qualify hardware between campaigns. Lonza stated that 82% of its mammalian-cell campaigns used disposable probes in 2025, versus 54% in 2023, standardizing on gamma-irradiated formats for inventory simplicity. Samsung Biologics’ newest facility was designed without reusable ports, saving 8% in construction expense and stripping calibration steps from batch records.

Standardization of Single-Use Sensor Formats by Industry Consortia

In March 2025, the BioProcess Systems Alliance introduced the SU-200 connector that lets any compliant sensor plug into any controller, and 14 suppliers committed to ship compatible units by 2027.[3]BioProcess Systems Alliance, “SU-200 Connector Standard,” bioprocesssystemsalliance.com Merck cut sensor-qualification time from nine months to four months after adopting the standard, signaling faster upgrade cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Per-Unit Cost Versus Reusable Probes | -1.4% | Global, most acute in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Environmental Concerns over Single-Use Plastic Waste | -0.9% | Europe, North America, spreading to Asia-Pacific | Medium term (2–4 years) |

| Supply-Chain Volatility of Medical-Grade Polymers & Optical Components | -1.1% | Global, with acute shortages in optical-component supply | Short term (≤ 2 years) |

| Calibration-Data Integrity Challenges in GMP Audits | -0.7% | Global, particularly in facilities undergoing first-time inspections | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Per-Unit Cost Versus Reusable Probes

A single-use dissolved-oxygen sensor costs USD 180–280 per batch, while a reusable unit amortizes at USD 12 per batch after the USD 3,200 upfront spend. Continuous facilities such as Genentech’s Vacaville site would incur a USD 9 million annual penalty by going disposable. Raw material inflation pushed cyclic olefin copolymer prices up 18% in 2025, widening the gap.

Environmental Concerns over Single-Use Plastic Waste

EMA’s December 2025 draft guidance mandates life-cycle assessments for disposable components, and early models show single-use sensors carry four-to-six times the carbon footprint of reusable alternatives. AstraZeneca aims to pare plastic waste 30% by 2028 and has launched take-back pilots with leading vendors. California’s Assembly Bill 1200 adds USD 8–12 compliance costs per sensor under extended-producer-responsibility rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: pH Dominance Meets Optical Disruption

pH sensors held 34.43% of 2025 revenue within the single-use bioprocessing probes and sensors market, reflecting universal demand from seed train through formulation. Optical and multi-parameter devices are rising at a 15.23% CAGR as manufacturers fold multiple readings into fewer ports, reducing hardware cost and validation burden. Traditional glass electrodes foul in high-density perfusion cultures, so fluorescent optical pH alternatives are gaining ground. Dissolved-oxygen sensors remain vital for aerobic mammalian cultures, with integration into lactate probes to complete metabolic profiles. Flow and pressure sensors are shaking up downstream chromatography as magnetically levitated designs eliminate seals that shed particles.

The single-use bioprocessing probes and sensors market size for tri-parameter devices is projected to expand swiftly following Sartorius’ 2025 release of a combined pH-DO-temperature probe that trims port count and slash costs 22%. Pressure-sensor innovation includes burst-disc integration, preventing bag rupture during high-flow filtration, and capacitance probes now correlate 95% with offline viable-cell counts, supporting real-time cell-density control.

By Detection Technology: Electrochemical Incumbency Faces Optical Ascent

Electrochemical devices delivered 56.13% of 2025 revenue, but optical formats are slated for 14.89% CAGR because they offer non-invasive, multi-analyte monitoring. Raman spectroscopy measures glucose, lactate, ammonia, and glutamine simultaneously, eliminating 40-60 offline samples per batch and trimming technician hours. Hamilton’s 2025 study showed Raman cut titer variability by 14% in 12 validation batches. Near-infrared sensors, meanwhile, track protein concentration during ultrafiltration to avoid contamination from manual sampling.

Optical hardware costs USD 80,000–120,000 versus USD 8,000 for electrochemical suites, yet the labor savings and tighter control tilt total cost of ownership. ISFET pH sensors represent a hybrid, offering small form factor with electrochemical simplicity, and Endress+Hauser shipped the first gamma-sterilizable model in 2025.

By Sterilization Compatibility: Gamma Leadership, X-ray Momentum

Gamma-compatible units owned 44.25% of 2025 share, but X-ray and e-beam alternatives are forecast to post 16.14% CAGR through 2031. X-ray sterilization achieves sterility assurance levels in under 10 minutes without degrading optical fibers, making it the method of choice for Raman and NIR devices. Sterigenics added X-ray lines in Illinois and California in 2025 to serve this swelling demand.

Electrochemical sensors remain gamma-friendly and cheaper to sterilize at USD 15–20 per unit, whereas X-ray adds USD 25–35. ISO 11137’s 2024 amendment now supports X-ray dose mapping, but many SOPs still cite gamma data, creating paperwork for early adopters.

By Application: Upstream Dominance, Quality-Control Surge

Upstream bioprocessing contributed 59.55% of 2025 revenue as each batch consumes three-to-five sensors, with perfusion runs needing mid-campaign replacements. Optical Raman units priced at USD 1,200–1,800 per set in downstream chromatography now enable real-time protein detection, shrinking offline QC. Quality-control deployments are accelerating at 14.05% CAGR after FDA endorsed real-time release testing in 2024.

Thermo Fisher logged a 28% year-over-year rise in QC-oriented sensor sales during Q3 2025, led by inline endotoxin products that avert post-run LAL assays. Eppendorf’s wireless pH probe eliminates cable penetrations, lowering leak risk and simplifying bag assembly.

By End User: Biopharma Anchors Demand, Academia Accelerates

Biopharma and pharma firms accounted for 67.26% of 2025 demand, leveraging volume to secure 15–20% discounts. Academic and research institutes, however, are expanding at 15.83% CAGR as university spin-outs adopt single-use systems to avoid capital outlays for autoclaves and cleaning validation. North American and European firms favor premium optical hardware, while Indian and Chinese plants often specify lower-cost electrochemical formats.

CMOs lead in intensity; Samsung Biologics sources 90% electrochemical sensors for cost-sensitive biosimilar runs. Academic partnerships, such as UC Berkeley’s work with Polestar Technologies on a USD 50 lactate probe, aim to bend cost curves further.

Geography Analysis

North America held 37.82% of 2025 revenue thanks to concentrated CMO capacity in Massachusetts, North Carolina, and California. FDA approvals of 12 cell therapies in 2025 triggered rapid build-outs, with each new product demanding up to USD 4 million in annual sensor consumption. Domestic-content incentives now pull assembly into South Carolina, trimming delivery times to six weeks.

Asia-Pacific is forecast to post a 14.77% CAGR through 2031 on the back of China’s USD 12 billion biomanufacturing push and Singapore’s emergence as a hub for regional cell-therapy trials. Autobio Diagnostics and Mindray Medical launched competitively priced gamma-sterilizable sensors in 2025 that undercut imports by up to 40%, accelerating local uptake. Lonza, Thermo Fisher, and Merck operate GMP complexes in Singapore that mirror Western sensor specifications, creating demand for premium optical devices.

Europe faces sustainability headwinds. EMA’s draft mandate for life-cycle assessments is steering some projects back toward reusable probes. Sartorius introduced a sensor take-back scheme in 2025 that recovers electronics for refurbishment, slicing environmental impact by 40%. Elsewhere, GCC states are funding biotech parks, and Brazil’s vaccine expansion is fueling modest sensor demand anchored in electrochemical formats.

Regulatory Landscape

Single-use bioprocessing probes and sensors need GMP-aligned qualification, validation, and data integrity, with particular attention to materials compatibility for direct product-contact components. In the United States, USP General Chapter 665 became mandatory on May 1, 2026 for plastic components and systems used in manufacturing drug substances and products, and USP 1665 is commonly used as the companion risk assessment framework to structure extractables characterization and documentation packages.

In Europe, EMA validation and sterilization frameworks influence adoption and documentation for pre-calibrated, pre-sterilized sensors in SUS assemblies. EMA has also launched a workstream to revise EudraLex Volume 4 Annex 15 (Qualification and Validation), with consultations through mid-2026, reinforcing demand for standardized qualification evidence, lot traceability, and electronic records controls for computerized systems supporting PAT and real-time monitoring (cGMP and 21 CFR Part 11 aligned).

Value Chain Analysis

The value chain runs from specialized raw-material and sensing-element suppliers, including medical-grade polymers, pH/DO membranes, optical dyes, and MEMS dies and ASICs, through cleanroom assembly and calibration. After that, sterilization qualification and distribution take place either as standalone sensors or as part of single-use assemblies and bioreactor platforms.

Bioprocess OEMs and integrators, such as skids, controllers, single-use bioreactors, and bags and tubing sets, are key channel partners that bundle probes and sensors into validated workflows for biopharma manufacturers and CDMOs that require rapid changeover and tight contamination control. Bottlenecks tend to cluster around availability of high-purity polymers and optical components, ISO 13485-grade manufacturing controls, and additional lead time driven by pre-calibration and irradiation compatibility (gamma, X-ray, e-beam), plus lot-level documentation needed for GMP audits. As a result, end users often hold added safety stock, while suppliers regionalize assembly and sterilization steps to shorten replenishment cycles and reduce cross-border logistics exposure, particularly for higher-value optical and multi-parameter sensor configurations.

Competitive Landscape

The single-use bioprocessing probes and sensors market has a moderate concentration profile. Commodity pH and dissolved-oxygen probes leave room for nimble firms such as Broadley-James and PendoTECH to gain share through rapid delivery and flexible order sizes. Multi-parameter optical sensors and wireless units remain under-penetrated, representing less than 10% of installed bioreactors, so disruptive entrants like Polestar Technologies can open price gaps with injection-molded housings that shave 40% off unit costs.

Technology integration is the key battleground. Emerson filed a 2025 U.S. patent for embedding machine-learning drift detection directly into sensor firmware, locking in customers who rely on accumulated historical data. The SU-200 standard, meanwhile, pressures suppliers to pick between open connectivity and proprietary ecosystems, a choice that will shape margins through 2031. New entrants must still clear ISO 13485 and FDA Part 820 hurdles, which require sizable investments in quality systems, limiting fragmentation at the high end.

Single-Use Bioprocessing Probes And Sensors Industry Leaders

Thermo Fisher Scientific Inc.

Sartorius AG

Danaher

Hamilton Company

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven documentation and materials characterization create opportunities for suppliers that package single-use probes and sensors with extractables support, lot traceability, and ready-to-use qualification artifacts. The May 2026 effective date for USP 665 raises the value of standardized material-change control and risk assessment playbooks, which are often aligned to USP 1665, especially for CDMOs running multi-client suites where sensor substitution and changeovers are frequent.

The technology gap is also widening for integrated in-line analytics that cut manual sampling across upstream and downstream steps, with optical and multi-analyte approaches supporting real-time readouts without breaching sterile boundaries. In June 2026, Fujifilm and HORIBA announced a co-development of a high-sensitivity inline Raman measurement system aimed at continuous real-time monitoring across cell culture and purification, reflecting ongoing investment in advanced PAT for bioprocess control. At the platform level, embedded sensing concepts demonstrated publicly in 2026, including pH, DO, and metabolite sensing within disposable components, support demand for sensor-to-software interoperability and standardized connector ecosystems, including BPSA-led efforts.

Recent Industry Developments

- July 2026: Hamilton obtained North American Ex approvals (CSA, UL, and FM standards) for its VisiFerm mA and VisiTrace mA dissolved oxygen sensors. The certifications expand deployment options for bioprocess monitoring in hazardous environments where compliance constraints can limit instrumentation choices. This supports broader plant standardization for oxygen measurement.

- June 2026: Merck KGaA (Darmstadt, Germany) agreed to acquire Bio-Techne for USD 11.3 billion to strengthen its life science tools and analytical technologies portfolio. The deal underscores consolidation around upstream-to-analytics workflows and can shift competitive positioning for suppliers that bundle sensors with broader bioprocess and QC toolchains.

- November 2025: Aber Instruments and Sartorius extended integration of the BioPAT Viamass biomass sensor into Ambr 250 single-use vessels. The integration broadens PAT coverage for scale-down and high-throughput development workflows. It also tightens the link between automated bioreactor platforms and real-time sensing for process optimization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We size the market for disposable probes and sensors that are installed into single-use bioprocess containers and assemblies to monitor process conditions during biomanufacturing, including upstream and downstream steps. Revenues are counted at the point of sale for these measurement devices used for parameters like pH and dissolved oxygen.

Scope exclusions: We exclude reusable or fixed stainless-steel instrumentation, general lab analyzers that are not single-use inline sensors, and broader single-use consumables like bags and tubing unless sold as a sensor or probe.

Segmentation Overview

- By Sensor Type

- pH Sensors

- Dissolved Oxygen Sensors

- Conductivity Sensors

- Temperature Sensors

- Pressure Sensors

- Flow Sensors & Meters

- By Detection Technology

- Optical (fluorescence, Raman, NIR)

- Electrochemical (potentiometric, amperometric, ISFET)

- Capacitive / Piezo-resistive

- Other / Hybrid

- By Sterilization Compatibility

- Gamma-irradiable Sensors

- X-ray / E-beam–sterilizable Sensors

- Autoclavable / Steam-in-Place Sensors

- Non-sterilizable, Pre-sterilized Sensors

- By Application

- Upstream Bioprocessing

- Downstream Bioprocessing

- Quality Control & Assurance

- Research & Development

- By End User

- Biopharmaceutical & Pharmaceutical Companies

- Contract Manufacturing & Development Organizations (CMOs/CDMOs)

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where these sensors sit inside bioprocessing, and then linking demand to biopharma production intensity and single-use adoption. We referred to public sources such as the US FDA biologics and approvals information, European Medicines Agency product and guidance pages, US International Trade Commission trade statistics, and OECD health and industry indicators to set context on manufacturing activity and cross-border flows.

To round out the picture, we also leaned on sources such as ISPE guidance and education resources, peer-reviewed articles indexed in PubMed that discuss inline monitoring and single-use validation practices, and association or conference publications that track bioprocessing trends. Company annual reports, investor presentations, and reputable press were used to cross-check product positioning and timing of capacity expansions, and a paid subscription for company financials and news supported consistency checks on reported revenue context. The sources named above are illustrative only, and many other public references were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on turning the scope into a practical demand model, and then pressure-testing pricing and usage assumptions with people who buy, specify, and use these sensors. We spoke with a mix of bioprocess engineers, quality teams, manufacturing leadership, and supplier-side product managers across major producing regions so our adoption and replacement assumptions match real run rates and validation practices.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 19% | APAC: 43% |

| Mid tier: 50% | Functional/Unit leaders: 34% | EMEA: 32% |

| Smaller Players: 21% | Managers: 47% | Americas: 25% |

Market-Sizing & Forecasting

For the core model, we used the top-down and bottom-up mix where biomanufacturing activity and single-use penetration are translated into the number of measurement points per process and the expected consumption of single-use sensors. The demand pool was then adjusted by typical batch frequency, scale of production, and where inline monitoring is required in upstream, downstream, and supporting steps.

To keep the totals realistic, the outputs were corroborated with selective bottom-up approximations, such as sampled average selling price ranges by sensor type and a roll-up of supplier revenue disclosures where available, followed by channel checks shared in interviews. Inputs that mattered most included single-use system deployment in production suites, number of lots and changeovers, sensor replacement rate per batch, sterilization compatibility preferences (for example gamma-ready formats), and ASP progression as volumes scale.

Forecasts were built using scenario analysis, where biologics manufacturing expansion, regional capacity additions, and single-use adoption rates were varied within ranges validated by experts. Where direct volume indicators were missing for smaller countries, we used proxies such as biologics pipeline activity and installed biomanufacturing capacity, and then normalized results back to the regional totals.

Data Validation & Update Cycle

We validate the model by checking whether implied sensor demand lines up with independent signals, such as biologics manufacturing capacity growth, single-use system adoption narratives, and reported production expansions. Outliers are investigated by revisiting assumptions on monitoring points, replacement rates, and pricing, and then re-checking them through follow-up questions with industry contacts.

Before sign-off, the work is reviewed in steps so calculations, currency handling, and year mapping are consistent across regions and the global roll-up. The report is refreshed annually, and interim updates are triggered when material events occur, such as major facility announcements or meaningful shifts in biologics production activity. Just before delivery, a final analyst pass is done so clients receive the most current view available.

Mordor Intelligence's Single Use Bioprocessing Probes and Sensors Market Size Compared With Other Published Estimates

Published market values for this space can look far apart because the product boundary is not always consistent, and the assumed usage rate per batch also changes the math quickly. Differences in which years are treated as the current baseline, plus how inflation and currency conversion are handled, also create visible gaps.

The table shows a wide spread mainly because some estimates fold this topic into a narrower device-only count or, on the other end, into broader single-use bioprocessing consumables. In Mordor Intelligence's model, only single-use probes and sensors intended for preinstallation into bioprocessing containers are counted, and volumes are tied to monitoring points in upstream and downstream workflows rather than to total single-use assemblies shipped.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.74 B (2025) | |

| Trade Publisher A | USD 2.81 B (2023) | Uses an earlier base year and appears closer to a probes-focused view, which can undercount newer single-use sensor formats and later-stage adoption in large-scale facilities. |

| Syndicated Report B | USD 0.88 B (2024) | Looks aligned to a narrow manufacturer-shipment definition and lower assumed usage per batch, which can omit replacement demand and broader inline monitoring points across workflows. |

Taken together, the comparison suggests that scope and the usage logic drive more variance than the core growth direction. By anchoring demand to process monitoring points, replacement behavior, and realistic ASP bands validated in interviews, the final estimate stays traceable to clear steps that can be re-checked as adoption and production footprints change.

Key Questions Answered in the Report

What drives rapid uptake of disposables in bioprocess monitoring?

Demand for flexible, contamination-free campaigns plus FDA acceptance of factory-calibrated sensors accelerate adoption, especially at CMOs handling many products.

Which detection technology is gaining fastest traction?

Optical methods, notably Raman and NIR spectroscopy, are growing around 14.9% CAGR because they provide multi-analyte, real-time data without sampling.

How do single-use sensors affect operating costs?

They cut changeover labor and validation time but raise per-batch sensor spend; breakeven versus reusable probes sits near 40 batches per year.

Why are X-ray-compatible probes emerging?

X-ray sterilization achieves sterility in minutes without degrading optical fibers, essential for advanced Raman and NIR sensors.

Which region will add the most new demand by 2031?

Asia-Pacific, led by Chinese and Singaporean investments, is projected to register the highest regional CAGR at 14.77%.

Page last updated on: