Single Photon Emission Computed Tomography (SPECT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

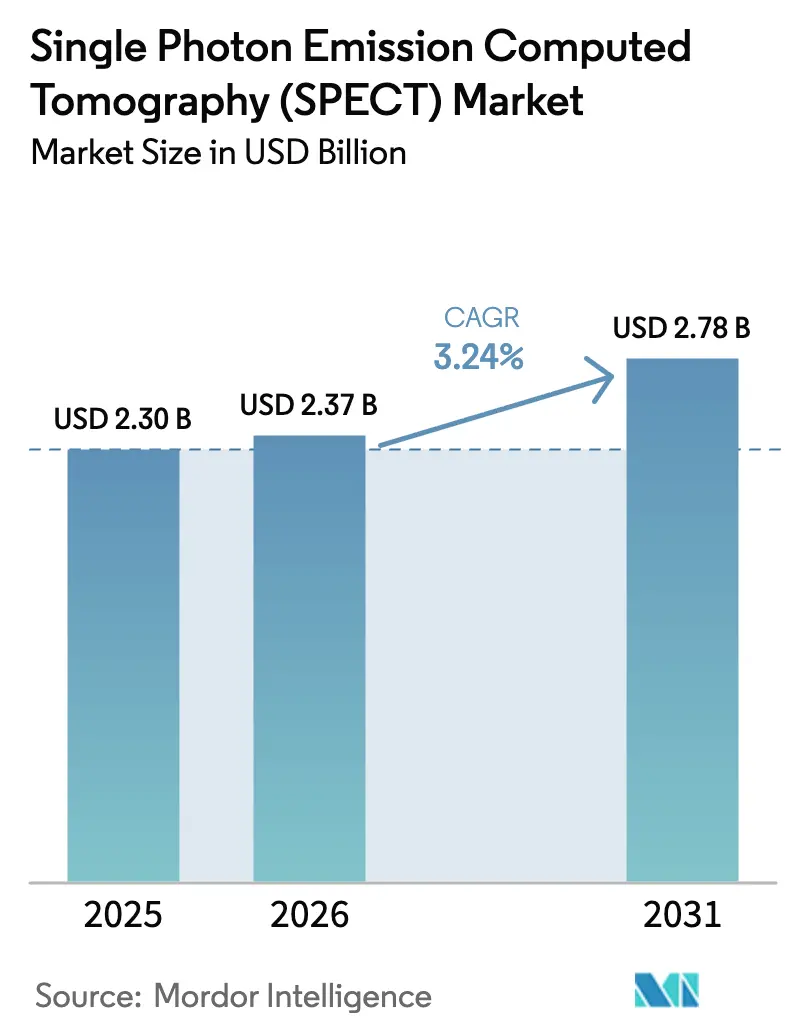

| Market Size (2026) | USD 2.37 Billion |

| Market Size (2031) | USD 2.78 Billion |

| Growth Rate (2026 - 2031) | 3.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

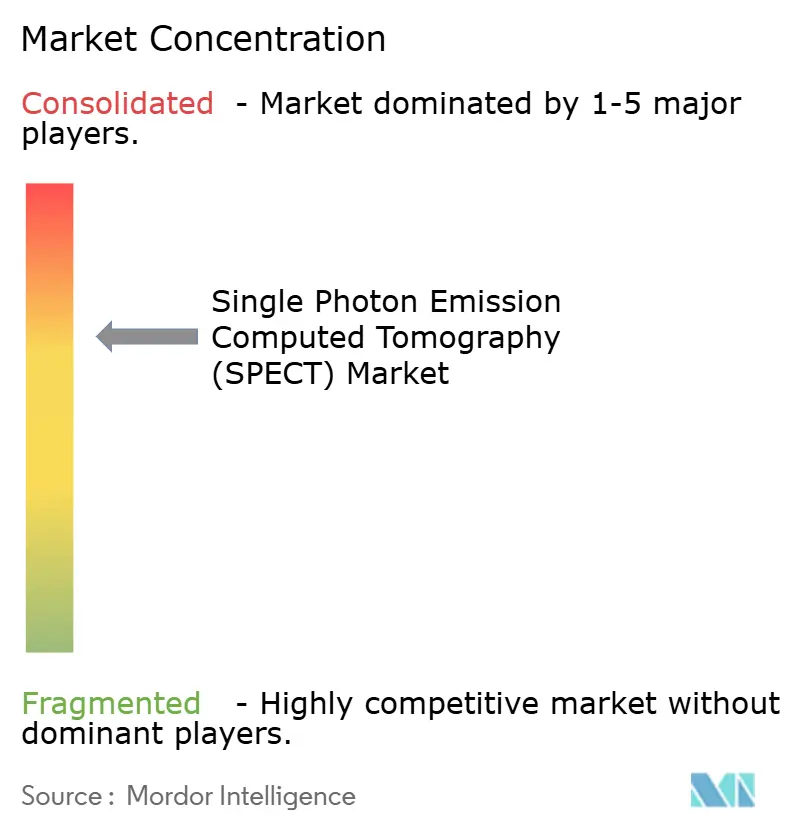

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single Photon Emission Computed Tomography (SPECT) Market Analysis by Mordor Intelligence

The Single Photon Emission Computed Tomography Market size was valued at USD 2.30 billion in 2025 and is estimated to grow from USD 2.37 billion in 2026 to reach USD 2.78 billion by 2031, at a CAGR of 3.24% during the forecast period (2026-2031).

Demand holds steady as oncology and cardiology workloads expand, hybrid SPECT/CT upgrades accelerate replacement cycles, and federal incentives bolster domestic molybdenum-99 production. Digital cadmium-zinc-telluride (CZT) detectors reduce 15-minute studies to 2 minutes, enhancing patient throughput and minimizing radiation exposure. Outpatient imaging networks capitalize on these gains to underprice hospital departments, while policy moves, such as the January 2026 CMS proposal for a USD 10 add-on payment for U.S.-sourced Mo-99, de-risk supply. Vendors respond with vertically integrated models that link radioisotope production, radiopharmacy logistics, and scanner sales, ensuring tracer availability and maximizing system utilization.

Key Report Takeaways

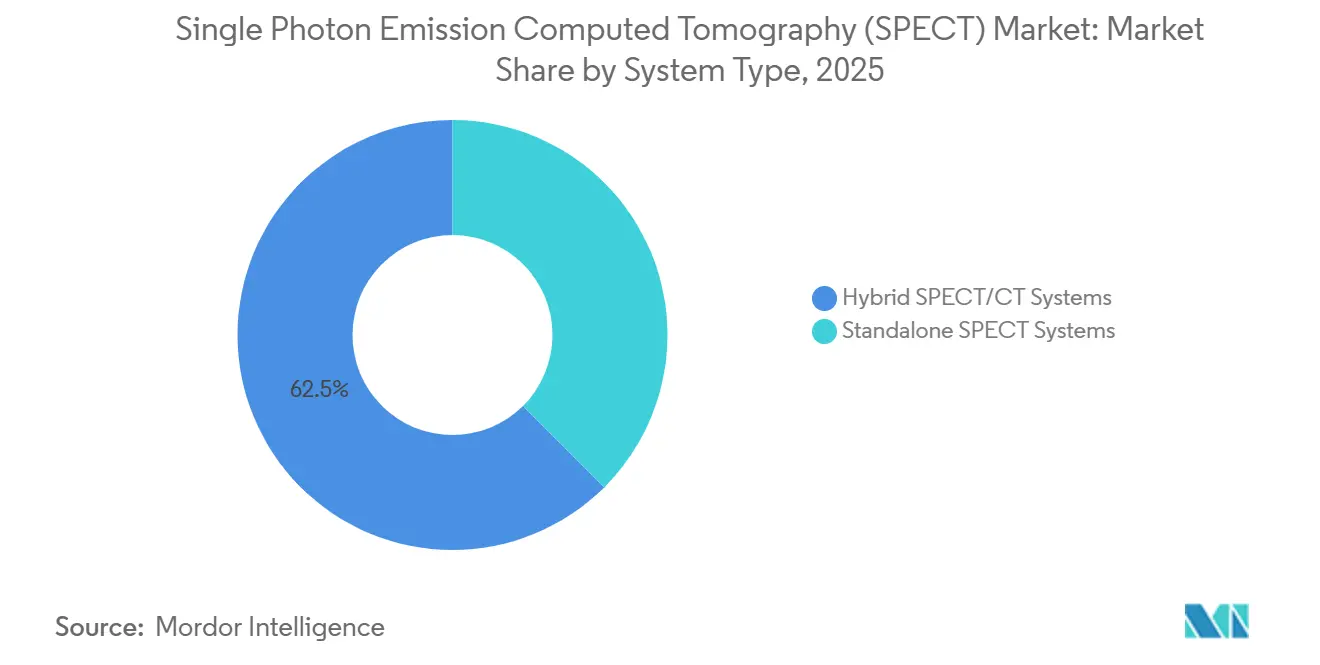

- By system type, hybrid SPECT/CT platforms led with a 62.46% revenue share in 2025; standalone gamma cameras are projected to trail, as hybrids grow at a 5.45% CAGR through 2031.

- By detector technology, sodium-iodide Anger cameras retained 63.56% of the Single-Photon Emission Computed Tomography market share in 2025, while digital CZT units are forecast to expand at a 5.67% CAGR through 2031.

- By application, oncology accounted for 42.45% of 2025 revenue; cardiology represents the fastest-growing segment, advancing at a 6.01% CAGR to 2031 as guideline updates deepen nuclear cardiology referral pools.

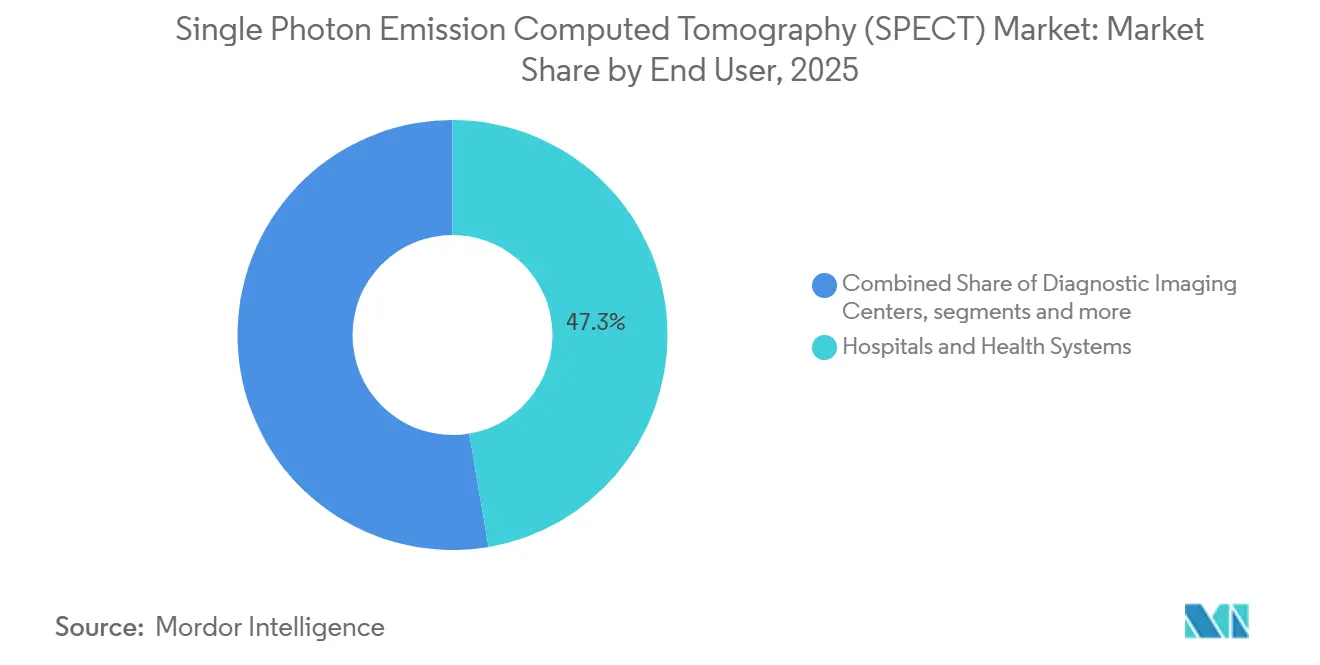

- By end user, hospitals commanded 47.32% of the revenue in 2025; diagnostic imaging centers are poised for a 6.54% CAGR through 2031, as two-minute CZT protocols increase daily study capacity.

- By radioisotope, technetium-99m accounts for 45.65% of the 2025 demand; iodine-123 is projected to grow at a 6.43% CAGR to 2031 as thyroid and movement-disorder imaging volumes increase.

- By geography, North America accounts for 42.23% of the 2025 demand; Asia-Pacific is projected to grow at a 4.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Single Photon Emission Computed Tomography (SPECT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden of Oncology and Cardiovascular Diseases | +1.2% | Global, peak intensity in North America & Europe | Long term (≥ 4 years) |

| Accelerating Adoption of Hybrid SPECT/CT Systems | +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Advancements in Digital CZT and AI-Enabled Reconstruction | +0.7% | North America & EU early adopters, APAC following | Medium term (2-4 years) |

| Strengthening Tc-99m Generator and Radiopharmacy Networks | +0.5% | Core markets in North America, EU, APAC | Short term (≤ 2 years) |

| Replacement and Upgrade Cycles of Legacy Gamma Cameras | +0.4% | Global, concentrated in North America & EU | Short term (≤ 2 years) |

| Expansion of Theranostics and Quantitative SPECT Workflows | +0.3% | North America & EU academic centers, APAC pilot sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Oncology and Cardiovascular Diseases

Global cancer incidence hit 20 million new cases in 2022 and is projected to surge 77% by 2050 as populations age[1]World Health Organization, “Cancer Tomorrow,” who.int. Parallel to this trend, cardiovascular disease caused 19.2 million deaths in 2023, keeping nuclear cardiology in high demand. SPECT remains the first-line gatekeeper: bone scans stage metastatic disease and myocardial-perfusion imaging triages revascularization candidates. The American Heart Association’s 2024 guideline reaffirmed SPECT for assessing myocardial viability, solidifying procedure volumes. Hospitals increasingly install hybrid SPECT/CT units to capture oncologic attenuation correction and coronary calcium scoring in a single visit, reinforcing system-replacement momentum.

Accelerating Adoption of Hybrid SPECT/CT Systems

Hybrid configurations accounted for 62.46% revenue in 2025 and will outpace standalone gamma cameras with a 5.45% CAGR to 2031. January 2025 joint guidelines from SNMMI, ASNC, and SCCT defined hybrid SPECT/CT as standard cardiac practice, mandating attenuation correction to curb false positives. GE HealthCare’s Aurora, cleared by the FDA in May 2025, uses a 75 cm bore and 40 mm crystal to trim scan time 30%, while Siemens’ Symbia Pro.specta ROI calculator shows payback in under three years for high-volume sites. Hospitals view hybrid adoption as future-proof, enabling theranostics dosimetry and quantitative SPECT imaging that standalone cameras cannot handle. Capital budgets pivot accordingly despite higher acquisition costs.

Advancements in Digital CZT and AI-Enabled Reconstruction

Digital CZT detectors held 36.44% share in 2025 yet are scheduled to grow fastest at 5.67% CAGR through 2031. GE HealthCare’s StarGuide GX, CE-marked in November 2025, marries dual-sided CZT arrays with NVIDIA acceleration, raising sensitivity 2.67-fold and enabling 1 mSv cardiac studies. Energy resolution improves from 10% in NaI systems to 5%-6% with CZT, sharpening lesion delineation and reducing equivocal reads. AI denoising engines such as Clarify DL compress acquisition time further, helping outpatient centers double daily throughput. Supply constraints at crystal manufacturers Kromek and Redlen, however, keep NaI cameras relevant for cost-sensitive buyers.

Strengthening Tc-99m Generator and Radiopharmacy Networks

Technetium-99m drives 45.65% of radioisotope revenue, and vendor vertical integration now safeguards supply. GE HealthCare’s December 2024 acquisition of Nihon Medi-Physics brought 13 radiopharmacies under its umbrella, guaranteeing tracer availability. The U.S. Department of Energy’s September 2025 USD 32 million grant to SHINE Technologies aids a domestic Mo-99 plant, while CMS proposes a USD 10 dose add-on for U.S.-made Mo-99 starting 2026. These measures lessen dependence on six aging research reactors that still produce 95% of global Mo-99, reducing supply-chain risk and supporting procedure stability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vulnerability of Mo-99/Tc-99m Global Supply Chain | -0.6% | Global, acute in EU & UK | Short term (≤ 2 years) |

| Capital Intensity and Budget Constraints for SPECT/CT Upgrades | -0.5% | North America & EU public hospitals, APAC tier-2 sites | Medium term (2-4 years) |

| Competitive Substitution from PET/CT in Oncology | -0.3% | North America & EU oncology centers | Medium term (2-4 years) |

| Limited Availability and Cost of Detector-Grade CZT | -0.2% | Global, supply concentrated in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vulnerability of Mo-99/Tc-99m Global Supply Chain

Six reactors generate 95% of the world’s Mo-99, making outages disruptive. When Curium’s European reactors paused in October 2024, United Kingdom clinics rationed doses, extending cardiac waitlists by weeks. Hospitals reverted to higher-dose thallium-201 protocols, highlighting a critical safety and efficiency setback. Reactor operators must also transition from highly enriched uranium targets to low-enriched fuel, temporarily lowering yields by about 20%, compounding supply tension. NorthStar’s RadioGenix provides a cyclotron-based alternative, yet current output covers only a fraction of demand. Until redundancy improves, the Single-Photon Emission Computed Tomography market remains exposed to isotope shocks.

Capital Intensity and Budget Constraints for SPECT/CT Upgrades

Hybrid SPECT/CT units cost USD 400,000–600,000, straining public-hospital budgets where competing modalities vie for funds. United Kingdom NHS replacement guidelines continue to prioritize CT and MRI, pushing nuclear-medicine upgrades down the queue[2]NHS England, “Capital Equipment Planning 2024,” england.nhs.uk. In India and Southeast Asia, 15-year-old Anger cameras still pass regulatory linearity checks, further delaying refresh cycles. PET/CT, though pricier, can siphon oncology budgets, undermining SPECT capital plans. Financing innovations, vendor leasing, and proven ROI calculators help, but capex constraints shave half a percentage point off forecast growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Hybrid Upgrades Prevail in Replacement Cycles

Hybrid SPECT/CT platforms captured 62.46% of 2025 revenue and are predicted to grow at a 5.45% CAGR through 2031. This dominance stems from integrated attenuation correction, anatomical registration, and theranostics capabilities that justify a 40% premium over standalone units. GE HealthCare’s Aurora, FDA-cleared in May 2025, trims acquisition time 30%, lifting daily myocardial-perfusion throughput to 20 patients. Siemens’ Symbia Pro.specta supports isotopes up to 588 keV, enabling Lu-177 post-therapy scans. Standalone gamma cameras survive in mobile fleets and rural settings where CT adds limited benefit. Digirad’s portable Ergo unit, priced under USD 250,000, fills this niche but lacks hybrid features essential for ACR oncology accreditation.

Hospitals view hybrid systems as strategic assets that future-proof nuclear-medicine departments. ROI calculators demonstrate breakeven in under three years when repeat studies drop 18% and same-day reporting accelerates billing cycles. Single-Photon Emission Computed Tomography market size for hybrid platforms is forecast to reach USD 1.9 billion by 2031, accounting for nearly 70% of total equipment revenue. As accreditation bodies tighten standards, the share gap between hybrid and standalone units will widen, reinforcing the former’s leadership within the Single-Photon Emission Computed Tomography market.

By Detector Technology: CZT Momentum Builds Despite NaI Incumbency

Sodium-iodide (NaI) cameras held 63.56% of 2025 revenue, yet CZT systems are advancing at the fastest clip. Full-ring CZT scanners provide 4-to-10-fold sensitivity and 5% energy resolution, enabling 1 mSv cardiac studies that rival PET dose levels[3]European Association of Nuclear Medicine, “CZT Adoption Survey,” eanm.org. Spectrum Dynamics’ Veriton-CT, a 360° CZT ring, halves scan times with organ-specific geometries but carries a USD 1 million-plus list price. Kaiser Permanente adopted CZT-based cardiac amyloidosis screening in April 2025, validating clinical differentiation in a large integrated network.

Cost and supply advantages keep NaI relevant, particularly in emerging markets. Still, Single-Photon Emission Computed Tomography market share migration favors CZT, projected to rise above 45% by 2031. AI denoising workflows amplify performance gains, making CZT the detector of choice for outpatient centers chasing productivity. Vendors hedge by dual-detector portfolios, but future R&D resources tilt toward semiconductor-based designs.

By Application: Cardiology Surges on Guideline Endorsements

Oncology contributed 42.45% of 2025 revenue, yet cardiology will expand fastest at a 6.01% CAGR through 2031. The 2024 American Heart Association update cemented SPECT’s role in ischemia assessment, and two-minute CZT protocols now enable same-day stress-rest exams. CMS pass-through codes for novel PET tracers paradoxically grow nuclear procedure volumes by broadening referral pipelines. Single-Photon Emission Computed Tomography market size for cardiology is projected to reach USD 1.3 billion by 2031, lifting its revenue share toward 45%. Oncology growth moderates as PET substitutes in tumor staging, but thyroid, neuroendocrine, and bone metastasis use cases preserve a sizeable floor.

Neurology, endocrine, and renal studies jointly form a stable mid-single-digit growth cohort, buoyed by aging demographics and evolving movement-disorder work-ups. As theranostic therapies proliferate, quantitative SPECT expands from academic centers into community hospitals, adding high-value post-therapy scans that raise average revenue per patient.

By End User: Imaging Centers Accelerate on Throughput Economics

Hospitals held 47.32% revenue in 2025, yet diagnostic imaging centers will grow at 6.54% CAGR as site-of-service migration gains momentum. Two-minute CZT studies allow centers to schedule 20 cardiac patients daily, versus 12 under NaI protocols, boosting scanner utilization 60%. Lower overhead lets centers undercut hospital outpatient departments by 15%-20% on commercial contracts. Specialty and academic sites advance steadily on theranostics research, but the fastest share growth accrues to independent networks aggregating payers and self-pay volumes. By 2031, imaging centers could account for nearly one-third of Single-Photon Emission Computed Tomography market revenue.

By Radioisotope: I-123 Climbs on Thyroid and Movement-Disorder Work-ups

Technetium-99m generators remain the backbone at 45.65% of 2025 revenue. Iodine-123 volumes are set for a 6.43% CAGR through 2031, fueled by thyroid-nodule evaluation and Parkinson’s disease diagnosis with DaTscan. Though I-123 costs 2-3 times more per dose, superior 159 keV photon energy yields clearer images and lower radiation. Alpha-emitters like Ra-223 introduce low-volume, high-value imaging for theranostic dosimetry, and hybrid SPECT/CT scanners now feature protocols aligned with these therapies. Single-Photon Emission Computed Tomography market share for I-123 is expected to reach 18% by 2031, reflecting broader adoption in endocrine and neuro applications.

Geography Analysis

North America generated 42.23% of 2025 revenue, buoyed by 15-20 million annual myocardial-perfusion studies and policy incentives supporting domestic Mo-99 supply. DOE’s USD 32 million grant to SHINE Technologies and CMS’s proposed USD 10 Mo-99 add-on de-risk isotope logistics, stabilizing procedure volumes. High installed bases temper growth, so the region advances at a moderate 3.5% CAGR through 2031 as hospitals stretch upgrade cycles to ten years. Nonetheless, hybrid SPECT/CT installations concentrate in bariatric-capable and theranostics-ready platforms such as GE’s Aurora.

Asia-Pacific will post the fastest 4.54% CAGR, propelled by China’s 1,200-plus PET/CT fleet that spurs downstream demand for lower-cost SPECT in tier-two cities and India’s mandated detector-linearity upgrades. United Imaging’s aggressively priced hybrid systems win provincial tenders, while Japanese centers maintain per-capita utilization near U.S. levels. Regulatory fragmentation slows cross-border equipment flows, yet International Atomic Energy Agency technical-cooperation projects in Southeast Asia expand nuclear-medicine access, seeding long-term growth.

Europe advances at 3.18% CAGR. Germany and France refresh fleets on seven-year cycles, but reactor maintenance at Belgium’s BR2 and the Netherlands’ Pallas periodically restricts isotope supply, causing utilization dips. Middle East-Africa and South America together deliver mid-single-digit growth as Gulf Cooperation Council hospital expansions and Brazil’s public procurement cycles lift installed bases. Site-of-service migration and private imaging centers gain traction in Gulf states offering bundled cardiac check-up packages.

Regulatory Landscape

SPECT and SPECT/CT systems are regulated as diagnostic medical devices, with the United States classifying emission computed tomography systems under 21 CFR 892.1200 (Class II) and requiring conformity to FDA quality and postmarket expectations. A major compliance inflection occurred in February 2026 when the FDA Quality Management System Regulation (QMSR) became effective, updating CGMP expectations and tightening quality system alignment for manufacturers selling into the US market.

Across Europe, SPECT/CT systems fall under the EU Medical Device Regulation (EU 2017/745), with transition requirements for legacy devices and timelines extending through end-2026 for certain classes. This raises the importance of Notified Body capacity and technical documentation readiness. In the United Kingdom, nuclear medicine practice is governed under Ionising Radiation (Medical Exposure) Regulations (IR(ME)R) guidance, with ARSAC-linked diagnostic reference level practices shaping administered-activity and protocol standardization. US state-level rules can also differentiate between CT used for attenuation correction versus independent diagnostic CT use, affecting facility compliance workflows for hybrid systems.

Value Chain Analysis

The SPECT value chain begins upstream with radioisotope production and processing, including Mo-99/Tc-99m supply and generator manufacturing, and extends to critical component suppliers for detectors such as detector-grade CZT materials and reconstruction software ecosystems. Midstream participants include imaging OEMs (GE HealthCare, Siemens Healthineers, Philips, Canon Medical Systems, United Imaging) and radiopharmacy and distribution networks (Cardinal Health, Curium, Jubilant Radiopharma) that compound and deliver short half-life tracers on tight schedules. Weather, transportation delays, and cross-border controls can directly disrupt daily imaging capacity.

Downstream demand is concentrated in hospitals and outpatient imaging centers, where scanner uptime and radiotracer availability translate into procedure volumes and reimbursement capture. Vertical integration is becoming more visible, with GE HealthCare completing its acquisition of Nihon Medi-Physics in December 2024 to expand radiopharmacy reach, and US reimbursement policy signaling supply-chain prioritization through CMS action tied to US-sourced Mo-99. These dynamics make isotopes and last-mile radiopharmacy logistics as decisive as hardware specifications for system utilization and replacement decisions.

Competitive Landscape

Five multinationals Siemens Healthineers, GE HealthCare, Philips, Canon Medical Systems, and United Imaging - control roughly 70% of global system sales, giving the Single-Photon Emission Computed Tomography market a moderate concentration profile. GE HealthCare’s 2024 acquisition of Nihon Medi-Physics illustrates a push toward vertical integration, ensuring tracer supply and lifting scanner utilization 15%-20%. Siemens Healthineers differentiates through software, publishing an ROI calculator that quantifies hybrid benefits and secures sales in budget-constrained systems.

Challengers include Spectrum Dynamics, whose Veriton-CT 360° CZT ring offers organ-specific imaging that halves scan times, and Digirad, which supplies portable gamma cameras for mobile fleets. United Imaging leverages Chinese subsidies to price hybrids 20-30% below Western incumbents, capturing share in cost-sensitive Asia-Pacific tenders. Legacy single-head vendors lacking hybrid portfolios risk obsolescence as ACR accreditation standards shift toward mandatory attenuation correction for oncology.

Vendor roadmaps center on AI reconstruction, theranostics workflows, and supply-chain resilience. Crystal manufacturers work to expand CZT capacity, while radiopharmacy acquisitions proliferate to lock in isotope access. The resulting ecosystem shapes purchasing criteria beyond hardware specifications, favoring players offering end-to-end solutions.

Single Photon Emission Computed Tomography (SPECT) Industry Leaders

Bracco Imaging

Curium

Cadinal Health Inc

NTP Radioisotopes SOC Ltd

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Quantitative SPECT and theranostics-linked workflows represent a clear whitespace where hybrid SPECT/CT and digital CZT platforms support use cases beyond conventional cardiology and bone imaging, particularly post-therapy imaging and voxel-level dosimetry. Clinical validation is also expanding around ring-shaped CZT SPECT/CT for radiopharmaceutical therapy monitoring, including published evidence on voxel-level 3D dosimetry for 177Lu therapies using a 360-degree digital CZT-SPECT/CT platform. This is helping providers standardize protocols and justify hybrid upgrades.

Regulatory clearances in 2026 reinforce competitive activity around higher-throughput digital SPECT/CT and software-enhanced reconstruction, widening choice for providers focused on dose and time reductions. FDA actions cited in 2026 include clearance activity for Spectrum Dynamics digital SPECT/CT families and Siemens Symbia Pro.specta system family updates, signaling continued platform refresh cycles among leading vendors. Alongside these system-level advances, isotope resilience programs and reimbursement signals tied to domestic Mo-99 sourcing create operational incentives for providers to invest in SPECT/CT utilization improvements, even as detector-grade CZT supply remains a practical constraint that sustains a mixed installed base of NaI and CZT systems across cost-sensitive settings.

Recent Industry Developments

- January 2026: SHINE Technologies completed the acquisition of Lantheus Holdings, Inc. SPECT business, including the North Billerica, Massachusetts manufacturing facility and a portfolio of established SPECT radiopharmaceuticals. The transaction strengthens SHINE's downstream footprint and adds manufacturing and distribution assets that can be paired with domestic isotope initiatives to support tracer availability for routine SPECT procedures.

- November 2025: GE HealthCare received CE Mark for StarGuide GX, a digital 4D SPECT/CT system built around dual-sided CZT detectors to improve sensitivity and support faster acquisitions. The milestone expands commercialization in Europe for digital CZT SPECT/CT and reinforces the shift toward higher-throughput platforms used for quantitative imaging and theranostics-related protocols.

- October 2024: GE HealthCare introduced Aurora, a new dual-head SPECT/CT system with AI-enabled reconstruction capabilities, at the European Association of Nuclear Medicine (EANM) 2024 Congress. The presentation highlighted ongoing replacement-cycle focus on hybrid platforms that combine workflow efficiency with features intended to expand clinical use beyond legacy gamma camera applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues earned from SPECT imaging systems and closely related configurations used to capture functional images in clinical and academic settings, including standalone SPECT and hybrid SPECT/CT installations, along with relevant technology types used inside the system.

Scope exclusions: We exclude PET-only systems, CT-only scanners, and general hospital imaging services that are not directly tied to SPECT procedure capability.

Segmentation Overview

- By System Type

- Standalone SPECT Systems

- Hybrid SPECT/CT Systems

- By Detector Technology

- NaI(Tl) Anger Cameras

- Solid-state Digital CZT SPECT

- By Application

- Cardiology

- Oncology

- Neurology

- Endocrine/Thyroid

- Other Applications

- By End-user

- Hospitals & Health Systems

- Diagnostic Imaging Centers

- Specialty & Academic Centers

- By Radioisotope

- Tc-99m

- Ra-223

- Ga-67

- I-123

- Other Radioisotopes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the installed base, procedure setting, and replacement cycle signals that typically steer demand for SPECT systems. We refer to public sources such as the World Health Organization, the World Bank, the US FDA device databases, the International Atomic Energy Agency (nuclear medicine resources), and peer reviewed clinical journals that track imaging utilization and modality shifts.

To keep assumptions realistic, we also review company annual reports, investor presentations, press releases, and hospital or academic center procurement notes where they are publicly available. In a few cases, paid subscriptions that track company financials, patents, and import export shipment records were used to confirm product launches, manufacturing footprints, and regional trade flow direction. These desk research sources are illustrative only, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were gathered through structured interviews and surveys with hospital imaging heads, nuclear medicine physicians, radiology administrators, distributors, and service providers across major regions. The goal was to correct desk assumptions where reported buying behavior differed, especially on replacement timing, the mix shift toward hybrid SPECT/CT and CZT based systems, and regional differences in budget approval cycles, before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 44% |

| Mid tier: 51% | Functional/Unit leaders: 30% | EMEA: 37% |

| Smaller Players: 20% | Managers: 58% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using top-down logic, where country level healthcare spend and nuclear medicine capacity signals were translated into an addressable demand pool for SPECT equipment, and then refined by adoption and replacement behavior. The totals were then corroborated with selective bottom-up checks using sampled system ASP ranges by configuration, distributor channel checks, and a practical roll-up of reported modality exposure in key end users, which helped adjust outliers.

Inputs that matter in this market include the installed base and average age of gamma cameras, the share of hybrid SPECT/CT in new purchases, typical replacement cycles by care setting, procedure mix trends across cardiology and oncology, and the pace of solid-state CZT penetration (since it impacts price points and upgrade intent). For forecasting, scenario analysis was used, and near-term demand was anchored to expert views on capital budgets, utilization recovery, and procurement lead times, before longer-term growth was smoothed through stable replacement driven demand. Where bottom-up data was thin for smaller countries, we used proxy ratios from similar healthcare systems and then rechecked them with regional interviews.

Data Validation & Update Cycle

Model outputs are checked against multiple independent signals, such as reported imaging equipment spending patterns, public procurement announcements, and consistency between implied ASPs and the technology mix assumed. When a variance looks too large, the underlying drivers are reopened, and follow-up calls are triggered to retest assumptions like replacement cycle, hybrid share, and price progression.

Before sign-off, the work goes through multi-step analyst review where calculations, currency conversions, and year alignment are rechecked, and the narrative is compared against the quantified outputs. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, reimbursement shifts, or a meaningful technology launch. Right before delivery, a final update pass is completed so clients receive the most current view available.

Mordor Intelligence's Single Photon Emission Computed Tomography Spect Market Size Compared Against Other Published Estimates

It is normal to see different published market sizes for SPECT because the studies do not always count the same products, years, and revenue pools, even when the market title looks identical. Differences also show up when one model leans heavily on shipment assumptions, while another is driven by procedure volume or by broad nuclear imaging spending.

The key gap drivers here are usually whether radiopharmaceutical revenues are included alongside equipment, whether PET and other nuclear imaging modalities are blended into the same number, how hybrid SPECT/CT upgrades are priced versus full system replacements, and how older base years are inflated into current dollars. Also, some estimates assume faster CZT adoption and higher ASP expansion without doing enough checks against what hospitals say they are actually buying in each region.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.30 B (2025) | |

| Global Consultancy A | USD 3.78 B (2023) | Uses an earlier base year and appears to capture a broader revenue pool that may bundle adjacent nuclear imaging equipment and related services, which lifts totals when rolled into a global figure. |

| Industry Publisher B | USD 3.56 B (2024) | The estimate is higher mainly because it likely counts additional revenue lines beyond system sales (such as wider modality scope or extended end-user coverage), and it assumes a faster value lift from hybrid configurations. |

The table shows that year alignment and what gets counted as SPECT related revenue are the biggest reasons the numbers spread out. When equipment revenues are kept tied to system configurations, detector technology mix, and end-user purchase behavior, the result stays closer to an install and replacement driven demand pool, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

How fast is the Single-Photon Emission Computed Tomography market expected to grow by 2031?

It is projected to expand from USD 2.37 billion in 2026 to USD 2.78 billion in 2031, marking a 3.24% CAGR.

Which system type leads revenue today?

Hybrid SPECT/CT platforms held 62.46% of revenue in 2025 and remain the preferred upgrade choice.

Why are imaging centers gaining share?

Two-minute CZT protocols let centers handle 20 cardiac exams daily, boosting utilization 60% and attracting referral business.

What is the biggest clinical growth area?

Cardiology studies are forecast to rise at a 6.01% CAGR through 2031 following guideline endorsements and faster scan times.

How does Mo-99 supply affect scanner demand?

Stable isotope availability underpins 80% of nuclear-medicine procedures, so domestic production incentives reduce downtime risk and support equipment utilization.

Which detector technology is gaining traction?

Digital CZT systems are growing at 5.67% CAGR on the back of 4-to-10-fold sensitivity gains and AI-assisted dose reduction.

Page last updated on: