Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

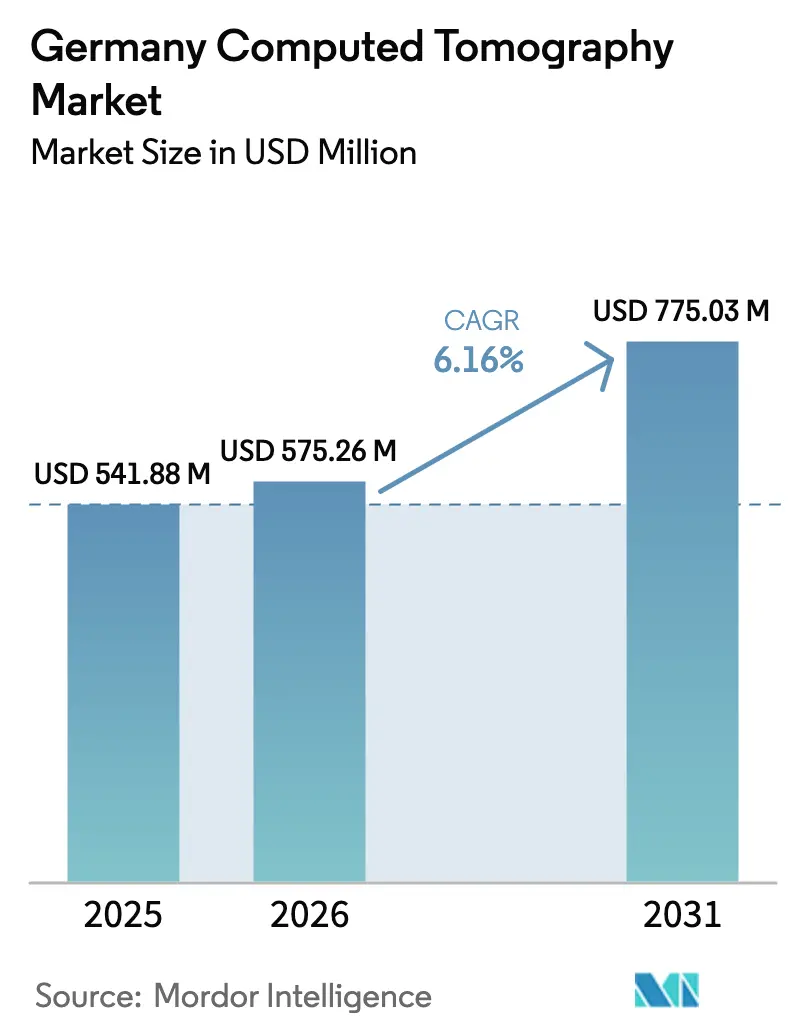

| Base Year Market Size (2025) | USD 541.88 Million |

| Market Size (2026) | USD 575.26 Million |

| Market Size (2031) | USD 775.03 Million |

| Growth Rate (2026 - 2031) | 6.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Computed Tomography Market Analysis by Mordor Intelligence

The Germany computed tomography market size is expected to grow from USD 541.88 million in 2025 to USD 575.26 million in 2026 and is forecast to reach USD 775.03 million by 2031 at 6.16% CAGR over 2026-2031. Growth stems from the country’s universal insurance coverage, a dense network of more than 1,900 hospitals, and rising demand for non-invasive diagnostics as the share of citizens aged 65 and above approaches 23% by 2030. Rapid product innovation—most notably photon-counting detectors and AI-enhanced reconstruction—reduces radiation dose by up to 45% while improving throughput, which appeals to hospitals grappling with staff shortages. Reimbursement reform in 2025 introduced GOP 34370 and 34371 for cardiac CT angiography, accelerating adoption in outpatient cardiology and radiology practices. Mobile CT programs such as Berlin’s STEMO ambulances cut stroke treatment times by 25 minutes, illustrating how point-of-care imaging reshapes acute neurology workflows. Regulatory rigor under the Medical Device Regulation (MDR) ensures patient safety but lengthens approval timelines, compelling vendors to invest early in clinical evidence generation.

Key Report Takeaways

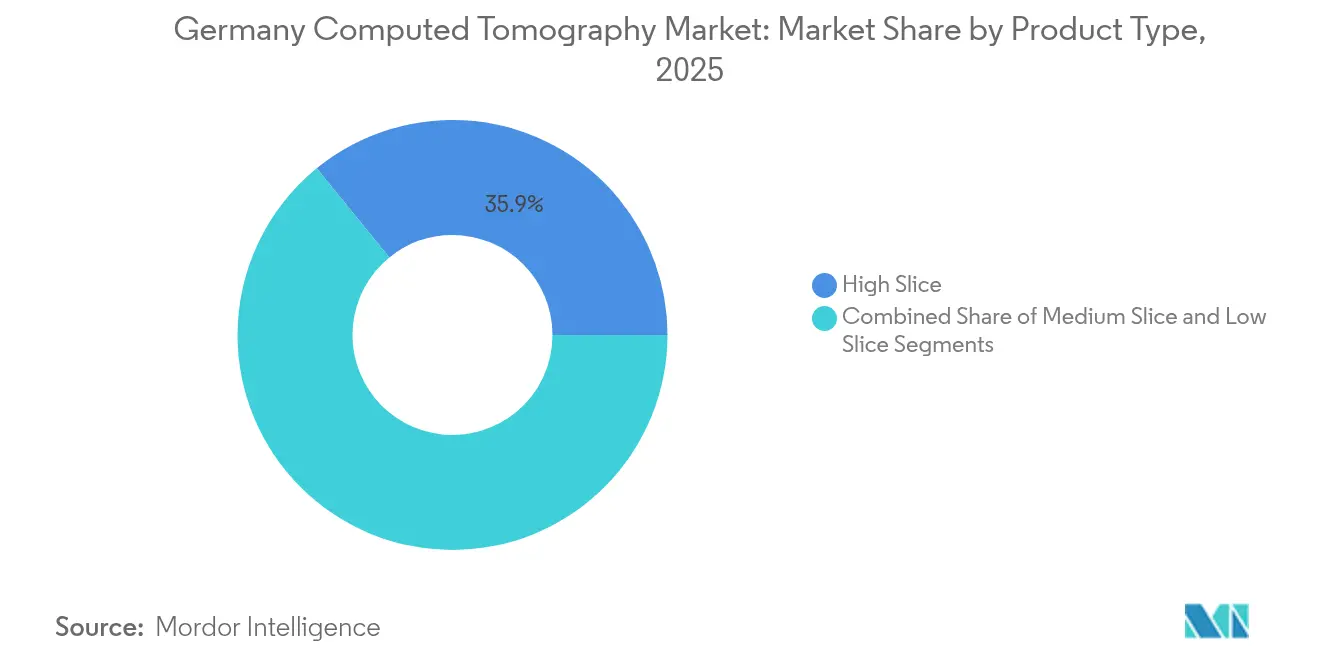

- By product type, High Slice systems led with 35.88% of Germany computed tomography market share in 2025, while Medium Slice systems are projected to expand at a 6.71% CAGR through 2031.

- By application, oncology accounted for a 31.78% share of the Germany computed tomography market size in 2025, whereas neurology is forecast to grow fastest at a 6.62% CAGR to 2031.

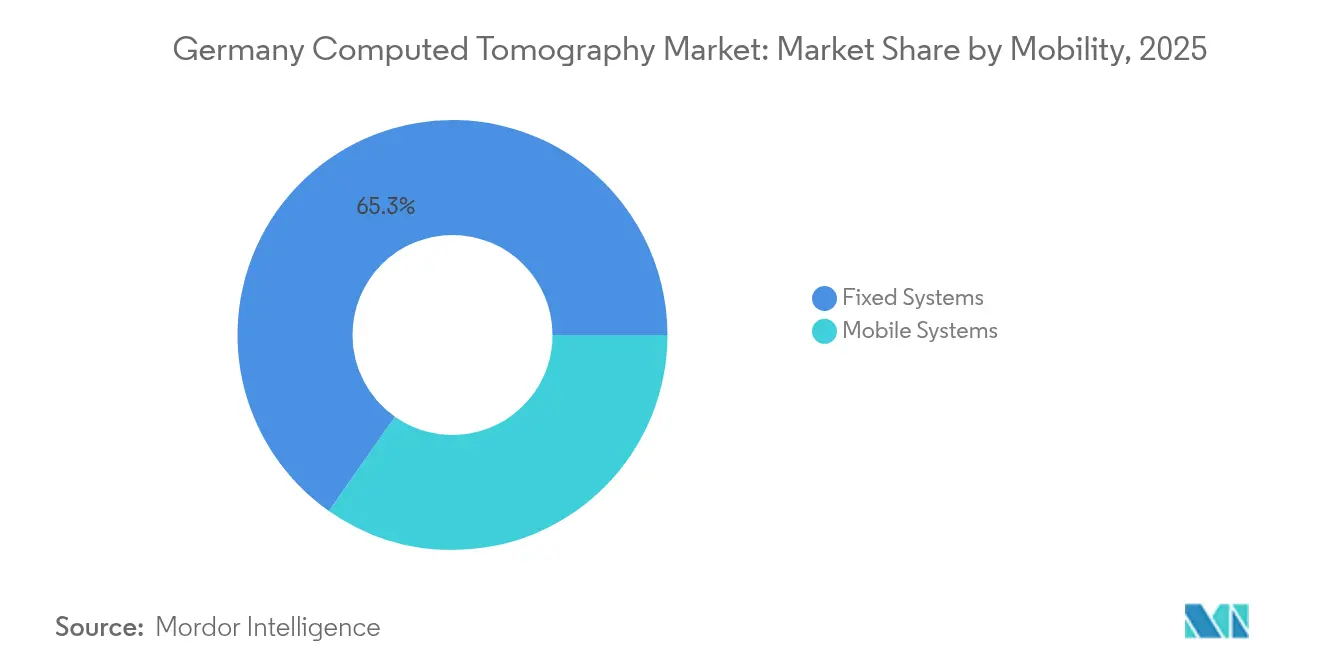

- By mobility, fixed scanners commanded 65.25% of the Germany computed tomography market size in 2025; mobile systems post the highest 6.90% CAGR between 2026-2031.

- By end user, hospitals generated 48.22% of revenue in 2025, while diagnostic imaging centers record the quickest expansion at a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Computed Tomography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic-disease burden & ageing population | +1.8% | National, higher intensity in rural and eastern states | Long term (≥ 4 years) |

| Continuous detector, AI & photon-counting breakthroughs | +1.2% | National, early adoption at university hospitals | Medium term (2-4 years) |

| Reimbursement of cardiac CT angiography from 2025 | +0.9% | National, immediate effect in outpatient settings | Short term (≤ 2 years) |

| Growth of low-dose lung-cancer screening programs | +0.7% | National, pilot activity in high-risk regions | Medium term (2-4 years) |

| Outpatient imaging platform roll-ups | +0.5% | Berlin, Munich, Hamburg | Short term (≤ 2 years) |

| Rural teleradiology demand | +0.4% | Brandenburg, Saxony, Saxony-Anhalt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic-Disease Burden & Ageing Population

Germany computed tomography market volumes climb steadily as 15.3 million residents live with cardiovascular disease and annual cancer incidence reaches 500,000 cases [1]Robert Koch-Institute, “Cancer in Germany 2023/2024,” rki.de. Each oncology patient undergoes an average of 4-6 scans during therapy, forming a predictable revenue stream for imaging providers. The demographic shift is more pronounced in sparsely populated eastern states where hospital consolidation raises concern over access. To maintain throughput amid staffing gaps, providers invest in automation tools that shorten exam times and standardize image quality. Hospitals use these efficiency gains to accommodate a growing share of chronic-care follow-ups without lengthening wait lists.

Continuous Detector, AI & Photon-Counting Breakthroughs

Photon-counting CT delivers sub-0.2 mm spatial resolution and 45% lower dose relative to conventional detectors [2]Siemens Healthineers, “NAEOTOM Alpha technical white paper,” siemens-healthineers.com. University Hospital Augsburg has already completed more than 8,000 clinical cases, validating spectral imaging benefits in complex cardiovascular and orthopedic evaluations. AI-based reconstruction drives a further 50-80% dose reduction while tripling daily scan capacity, helping radiology departments mitigate workforce shortages. As Germany computed tomography market participants bundle detectors, AI and workflow software, competitive focus shifts from hardware alone to integrated platforms that optimize room utilization.

Reimbursement of Cardiac CT Angiography from 2025

Statutory insurance now reimburses coronary CT angiography under GOP 34370, reducing economic barriers for non-invasive assessment of suspected coronary artery disease. Evidence shows the procedure costs EUR 98.60 against EUR 317.75 for invasive angiography, promising significant savings for payers. Early forecasts suggest 30-40% of diagnostic coronary angiographies could migrate to CT by 2030, infusing new momentum into the Germany computed tomography market. Outpatient cardiology practices plan equipment upgrades, while radiology societies publish training guidelines to preserve image quality and patient safety in rapidly expanding cardiac programs.

Growth of Low-Dose Lung-Cancer Screening Programs

Pilot studies evaluate national deployment of low-dose CT screening to curb lung-cancer mortality, which claimed 56,690 new cases in 2024. International clinical trials confirmed a 20% mortality drop among high-risk smokers, prompting German policymakers to outline eligibility criteria and funding models. Domestic research groups apply AI algorithms to filter noise and detect sub-centimeter nodules at radiation levels comparable to annual background exposure, addressing scepticism over cumulative dose [3]Plattform Lernende Systeme, “AI in lung cancer screening,” plattform-lernende-systeme.de . Scaling the program will require additional systems in regions with elevated smoking prevalence, buoying equipment sales over the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High scanner CAPEX & OPEX | -1.1% | Nationwide, acute at small community hospitals | Long term (≥ 4 years) |

| Stringent BfArM / CE-MDR approval timelines | -0.8% | Nationwide | Medium term (2-4 years) |

| Radiographer & radiologist workforce shortages | -0.7% | Nationwide, more pressing in rural facilities | Long term (≥ 4 years) |

| Oversupply in metro areas compressing scan prices | -0.4% | Berlin, Munich, Hamburg | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Scanner CAPEX & OPEX

A state-of-the-art 128-slice CT costs up to USD 3 million, and annual service contracts add 8-12% of purchase value. Under Germany’s diagnosis related group (DRG) financing, hospitals face fixed reimbursements that rarely cover high-end equipment lifecycle costs. Providers need a minimum of 1,065 scans per year to reach breakeven for a dedicated radiology unit, pushing smaller facilities toward teleradiology partnerships. Capital constraints slow uptake of photon-counting systems despite their clinical upside, reinforcing the preference for mid-range platforms that balance capability and cost.

Stringent BfArM / CE-MDR Approval Timelines

Class IIb and III CT devices must complete exhaustive conformity assessments, extending market entry by 12-18 months and inflating regulatory expenses. Post-market clinical follow-up and vigilance reporting add administrative burden, especially for smaller vendors. While the framework raises safety standards, it lowers agility, delaying the commercial impact of technological breakthroughs. Manufacturers pre-fund extensive clinical trials to secure early evidence, raising barriers for new entrants and tightening competition within the Germany computed tomography market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Medium Slice Systems Drive Growth

Medium Slice platforms capture buyers seeking advanced functionality at sustainable prices, and this category is forecast to grow at a 6.71% CAGR, outpacing the overall Germany computed tomography market. High Slice units retained a 35.88% Germany computed tomography market share in 2025 on the strength of premium cardiac and oncology applications. University hospitals prefer ≥256-slice or photon-counting scanners for ultra-high-resolution cases, whereas regional clinics migrate to 64-slice systems that cover most diagnostic pathways without exceeding budget ceilings.

Rapid detector improvements enable Medium Slice devices to deliver near-isotropic imaging and spectral post-processing once reserved for flagship models. This democratization aligns with procurement policies emphasizing value-based care. The Germany computed tomography market size for Medium Slice systems is projected to advanced steadily as outpatient imaging chains refurbish ageing fleets to meet cardiac CT reimbursement demand. Conversely, Low Slice scanners remain niche, serving emergency backups and small trauma centers where acquisition cost trumps advanced features.

By Application: Neurology Segment Accelerates

Neurology is projected to register a 6.62% CAGR, the fastest within the Germany computed tomography market, driven by nationwide stroke pathways and expanding endovascular therapy capacity. Berlin’s STEMO ambulances demonstrate how on-board CT raises thrombolysis rates above 30%, underscoring clinical and economic payoffs of pre-hospital imaging. Oncology preserved the largest 31.78% slice of Germany computed tomography market size in 2025 as comprehensive cancer centers rely on serial CT for staging, treatment planning and surveillance.

Cardiovascular imaging will benefit most directly from the 2025 reimbursement change. As payers encourage non-invasive coronary pathways, mid-tier hospitals invest in dual-source systems that deliver one-beat cardiac studies. Musculoskeletal and trauma indications remain steady, sustained by high road-traffic and workplace injury volumes. AI decision-support tools shorten neurological scan interpretation times, freeing radiologists to handle surging demand without sacrificing diagnostic accuracy.

By Mobility: Mobile Systems Transform Care Delivery

Fixed systems accounted for 65.25% of Germany computed tomography market size in 2025, yet mobile platforms are expected to post the highest 6.90% CAGR through 2031. Critical care teams deploy head-only systems beside ICU beds to reduce intra-hospital transfers that risk ventilator disconnections. Devices such as SOMATOM On.site deliver diagnostic-grade images in 20 minutes and integrate seamlessly with hospital PACS networks. Rural hospitals use trailer-mounted scanners on rotation schedules to guarantee weekly access without full-time staffing, a model supported by federal telemedicine grants.

Continuous software updates improve image quality and radiation dose on mobile units, reinforcing their suitability for stroke, trauma and pediatrics. As workforce constraints intensify, health systems treat mobile CT as a multiplier that spreads specialist capacity across multiple sites, sustaining the Germany computed tomography market momentum in underserved regions.

By End User: Diagnostic Centers Lead Expansion

Hospitals commanded 48.22% of 2025 revenue due to comprehensive inpatient and emergency case-mix needs. However, diagnostic centers are projected to expand fastest at a 6.78% CAGR as private equity consolidates small practices into scalable outpatient platforms. These groups negotiate equipment volume discounts and standardize AI-enabled workflows that lift daily scan counts above hospital averages.

Legislation governing Medical Treatment Centers (MVZ) clarifies licensing, spurring new builds near large employers for convenient screening services. Public insurers increasingly steer non-acute referrals to outpatient providers to contain costs, reinforcing volume migration. In response, hospital managers position themselves as tertiary centers for complex cardiology, oncology and trauma, focusing capital budgets on premium High Slice or photon-counting technology that secures referral loyalty within the Germany computed tomography market.

Geography Analysis

Market demand clusters in Bavaria, Baden-Württemberg and North Rhine-Westphalia, where dense populations and robust economies support early adoption of photon-counting and AI-augmented scanners. Bavaria’s hospital plan prioritizes replacement of ageing systems with dual-energy or spectral models, sustaining supplier order pipelines. Berlin and Hamburg deploy mobile stroke units featuring CT to reduce door-to-needle times, expanding neurology volumes outside traditional emergency departments.

Eastern states such as Brandenburg and Saxony modernize infrastructure funded by federal-state programs that target legacy equipment dating from the 1990s upgrade wave. These facilities often adopt Medium Slice systems paired with teleradiology contracts to offset limited on-site radiologist availability. Teleradiology networks link more than 30 sites, demonstrating how cloud-based reporting expands specialist reach and stabilizes scan demand in low-density regions.

Oversupply pressures appear in urban corridors where scan prices trend downward as new outpatient chains enter the Germany computed tomography market. Providers counter by differentiating through dose reduction protocols and subspecialty services such as cardiac CT or spectral oncology imaging. National reimbursement uniformity ensures consistent revenue per scan, yet operational efficiency dictates profitability, reinforcing regional competition based on workflow productivity rather than pricing variance.

Competitive Landscape

The Germany computed tomography market is moderately fragemented, with Siemens Healthineers, GE HealthCare, Philips and Canon Medical Systems controlling the majority of installed units. Siemens leverages its Forchheim production hub and first-to-market photon-counting portfolio to preserve domestic leadership. GE HealthCare focuses on AI-driven cardiac workflows, exemplified by the Revolution Vibe launch that targets new CCTA reimbursement. Philips emphasizes iterative reconstruction and dose management in its CT 5300, appealing to providers seeking radiation stewardship. Canon differentiates through detector coverage combined with aquilion spectral imaging that reduces contrast dose for renal-compromised patients.

Strategic activity centers on partnerships that embed AI algorithms into scanners at the point of acquisition. NEXUS/CHILI’s alliance with deepc distributes an FDA-cleared algorithm marketplace to more than 500 German hospitals, simplifying integration and support. Vendors also invest in service contracts offering uptime guarantees that alleviate staffing shortages for in-house biomedical engineers. Patent filings exceed 500 for photon-counting detector innovations, indicating sustained R&D despite regulatory headwinds.

Providers explore mobile CT fleet leasing and usage-based pricing that lower capital barriers, an emerging business model that could reshape competitive dynamics. Domestic startups develop thin-slice reconstruction software that interfaces with legacy hardware, allowing older units to meet modern image-quality expectations and extending system lifespan.

Germany Computed Tomography Industry Leaders

GE Healthcare

Koninklijke Philips NV

Canon Medical Systems Corporation

Siemens Healthineers AG

Fujifilm Holdings Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare introduced Revolution Vibe with Unlimited One-Beat Cardiac imaging and embedded AI to capture the expanding CCTA segment in Germany.

- October 2024: GE HealthCare partnered with University Medicine Essen to establish a Theranostics Center of Excellence focused on personalized oncology pathways.

- February 2024: Philips debuted the AI-enabled CT 5300 featuring Nanopanel Precise detectors, delivering lower dose and enhanced workflow performance across European installations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, prepared by Mordor Intelligence analysts, defines the German computed tomography market as revenues from new, medical-grade CT scanner hardware, low-, mid-, and high-slice systems installed in hospitals, diagnostic imaging centers, and certified mobile units. The scope captures purchase price only; service contracts, contrast agents, and refurbished or rental systems are omitted.

Industrial nondestructive testing CT and radiation therapy simulation CT equipment are outside this assessment.

Segmentation Overview

- By Product Type

- Low Slice

- Medium Slice

- High Slice

- By Application

- Oncology

- Neurology

- Cardiovascular

- Musculoskeletal

- Other Applications

- By Mobility

- Fixed Systems

- Mobile Systems

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Others

Detailed Research Methodology and Data Validation

Primary Research

We interviewed radiology department heads, procurement leads at university and regional hospitals, imaging center owners, and local distributors across seven Bundesländer. These discussions validated average selling prices, replacement cycles, and the timing of cardiac CT angiography uptake after 2025 reimbursement, then reconciled any data gaps uncovered in secondary work.

Desk Research

We began with publicly available German sources such as Destatis hospital equipment counts, G-BA reimbursement catalog updates, the Federal Office for Radiation Protection dose audit data, and OECD Health Statistics to size procedure demand. Trade bodies like the German Radiological Society and Europe's COCIR supplied shipment trends, while peer-reviewed papers in European Radiology clarified adoption rates for photon-counting scanners. Company filings and investor decks, complemented by D&B Hoovers and Dow Jones Factiva, helped us benchmark vendor revenues and installed base churn. All items listed illustrate the wider set of documents reviewed; many additional publications informed data cleaning, validation, and scope decisions.

Market-Sizing & Forecasting

A top-down model converts national installed base counts and typical seven-year replacement curves into annual unit demand, which is multiplied by blended ASPs gathered from channel checks. Supplier roll-ups on selected tenders act as a bottom-up cross-check before totals are frozen. Key variables like 65+ population growth, oncology and cardiac CT procedure volumes, slice mix shift toward >=128 detectors, ASP erosion, and photon-counting penetration feed a multivariate regression that projects values to 2030. Where hospital-level data were missing, we imputed figures using weighted averages from matched facilities of similar size.

Data Validation & Update Cycle

Analysts triangulate outputs against import data, vendor earnings, and DRG scan volumes, flagging anomalies for senior review. Reports refresh each year, and we trigger interim revisions if regulatory or reimbursement changes materially alter any input; a final freshness check precedes client delivery.

Why Mordor's Germany Computed Tomography Baseline Commands Confidence

Published numbers often diverge because firms pick different device classes, price assumptions, or refresh cadences. We note that slice coverage, inclusion of service revenue, and currency timing create the widest swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 541.9 M (2025) | Mordor Intelligence | - |

| USD 205.5 M (2023) | Regional Consultancy A | Narrow slice definition and exclusion of mobile units; older base year not inflation adjusted |

| USD 1.98 B (2024) | Industry Databook B | Bundles service contracts, simulators, and refurb sales into hardware total; relies on budgeted CAPEX rather than actual shipments |

The comparison shows how scope inflation or contraction can skew values by more than threefold. By anchoring on verified shipments, clearly stated device classes, and an annually refreshed model, Mordor delivers a balanced, transparent baseline that decision makers can retrace and reproduce with confidence.

Key Questions Answered in the Report

What is the current value of the Germany computed tomography market?

The market is valued at USD 575.26 million in 2026 and is set to reach USD 775.03 million by 2031.

Which application segment contributes the largest revenue?

Oncology holds the leading 31.78% share owing to Germany’s extensive cancer screening and treatment infrastructure.

Why are Medium Slice CT systems growing faster than other product types?

They balance advanced imaging capability with lower acquisition cost, matching budget priorities of community hospitals and outpatient centers.

How will reimbursement changes affect cardiac imaging volumes?

New GOP codes introduced in 2025 enable full statutory insurance coverage for coronary CT angiography, potentially shifting up to 40% of diagnostic coronary cases from invasive to non-invasive CT.

What is driving interest in mobile CT scanners?

Mobile units reduce patient transport risks, support stroke ambulances and ICU imaging, and address staff shortages by bringing the scanner to the bedside.

How stringent are regulatory requirements for new CT technology in Germany?

Class IIb and III CT devices must undergo lengthy conformity assessments under the MDR, extending market entry by up to 18 months and increasing compliance costs for manufacturers.

Page last updated on: