South Korea Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

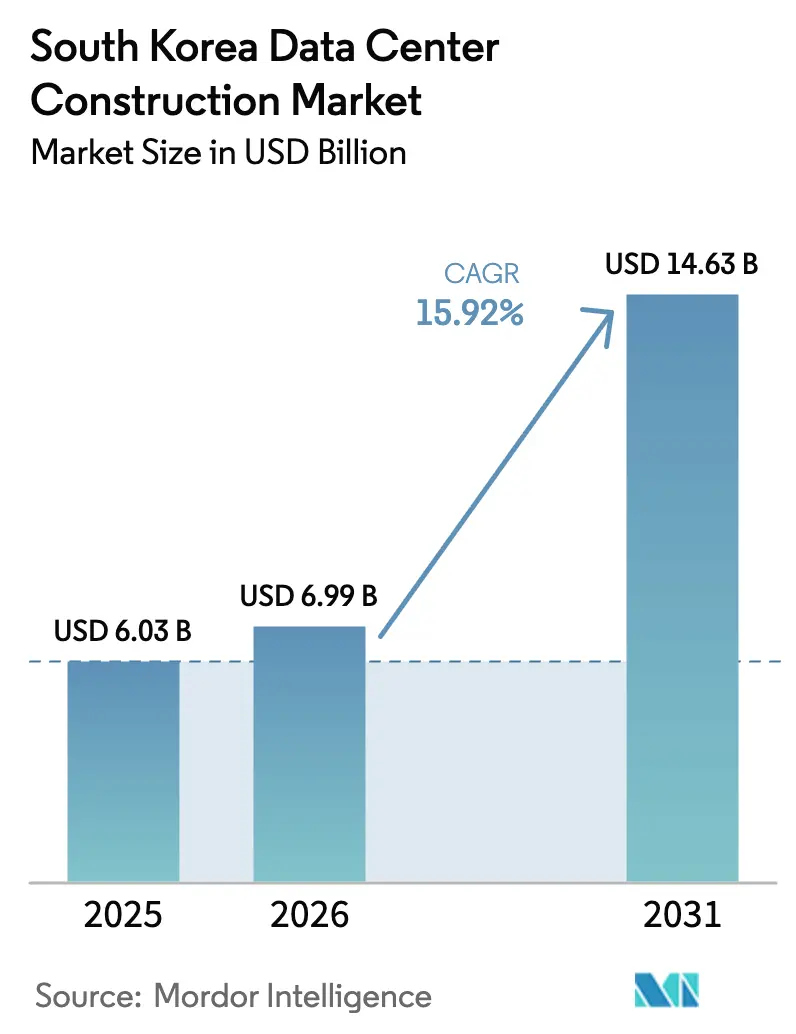

| Base Year Market Size (2025) | USD 6.03 Billion |

| Market Size (2026) | USD 6.99 Billion |

| Market Size (2031) | USD 14.63 Billion |

| Growth Rate (2026 - 2031) | 15.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Data Center Construction Market Analysis by Mordor Intelligence

The South Korea data center construction market size was valued at USD 6.03 billion in 2025 and estimated to grow from USD 6.99 billion in 2026 to reach USD 14.63 billion by 2031, at a CAGR of 15.92% during the forecast period (2026-2031). This rapid expansion anchors South Korea’s ambition to become the primary digital infrastructure hub of Northeast Asia, supported by hyperscale capital spending, sovereign AI initiatives, and accommodative infrastructure policies. Intensifying GPU deployments, surging transformer orders, and sustained cloud-migration waves are lifting power-density benchmarks well beyond historical norms. Construction majors are shifting toward liquid-cooling expertise, while pension funds recycle long-duration capital into wholesale colocation shells. Secondary provinces are leveraging lower land costs and renewable resources to attract mega-campus projects, easing congestion in Greater Seoul. These intersecting vectors collectively propel the South Korea data center construction market toward double-digit annual growth and higher project complexity.

Key Report Takeaways

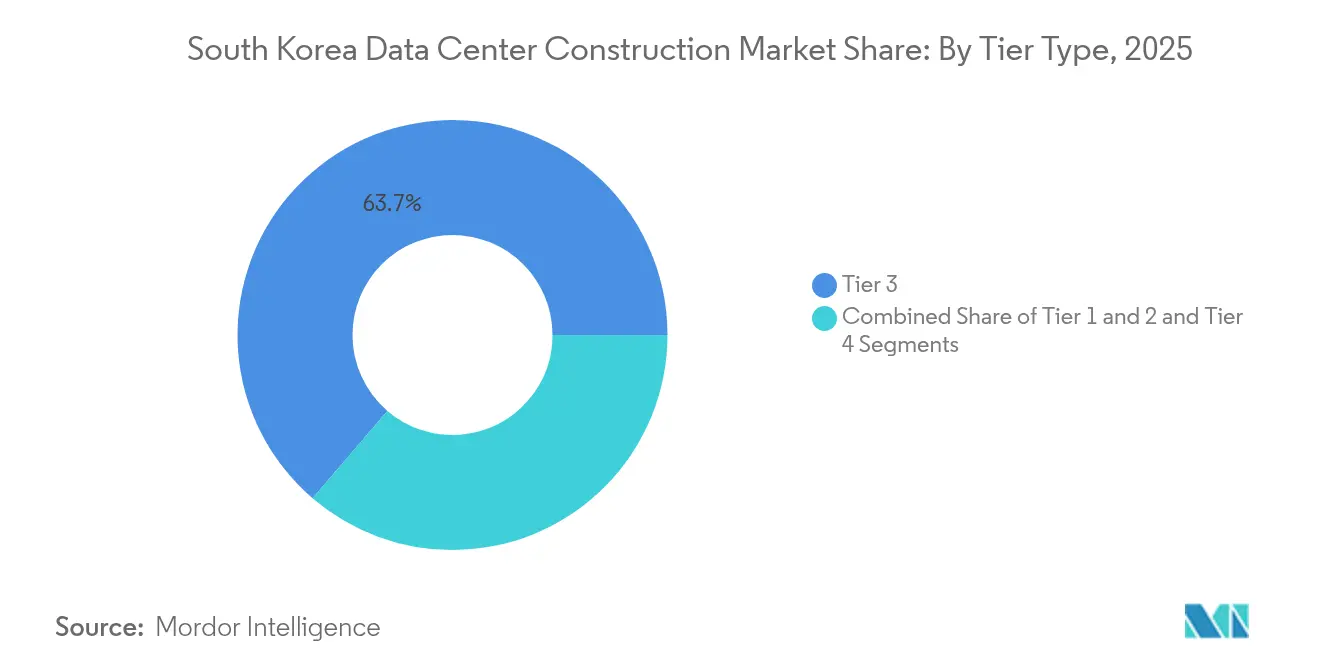

- By tier type, Tier 3 facilities held 63.72% of the South Korea data center construction market share in 2025; Tier 4 facilities are forecast to expand at a 16.88% CAGR through 2031.

- By data-center type, colocation services led with 53.35% revenue share in 2025, while hyperscaler self-builds are projected to grow at an 18.35% CAGR to 2031.

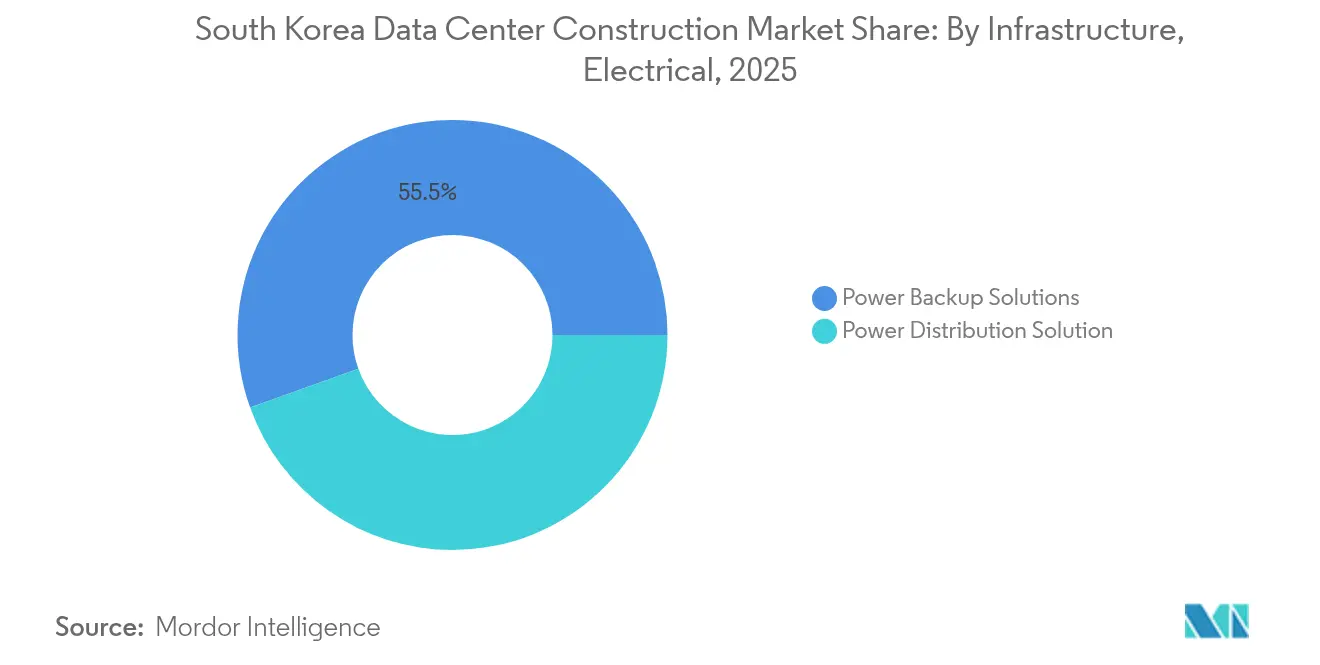

- By electrical infrastructure, power-backup solutions accounted for 55.48% share of the South Korea data center construction market size in 2025; power-distribution solutions are advancing at a 18.92% CAGR.

- By mechanical infrastructure, cooling systems commanded 41.92% share of the South Korea data center construction market size in 2025, with servers and storage infrastructure rising at a 15.78% CAGR.

- By geography, the Greater Seoul corridor retained an estimated 67.15% share of the South Korea data center construction market size in 2025, yet Jeollanam-do is pacing the fastest capacity additions at 23.05% CAGR on the back of the 3 GW AI hub commitment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscale and AI-led investments (2025-) | +4.2% | National, concentrated in Greater Seoul and Jeollanam-do | Medium term (2-4 years) |

| Government plan for 3 GW "mega" AI data hub in Jeollanam-do | +3.8% | Regional, with national spillover effects | Long term (≥ 4 years) |

| Cloud-migration wave by chaebol subsidiaries | +2.9% | National, with Seoul metropolitan area focus | Short term (≤ 2 years) |

| 5G/Private-5G edge-compute build-outs | +2.1% | National, prioritizing urban centers | Medium term (2-4 years) |

| Under-reported: Hydrogen-fuel-cell micro-grids for Seoul DCs | +1.4% | Seoul metropolitan area | Long term (≥ 4 years) |

| Under-reported: Capital-recycling by Korean pension funds into DC real-estate | +1.8% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in hyperscale and AI-led investments drive market transformation

Hyperscale operators and domestic conglomerates are jointly underwriting record-size campuses designed around GPU-dense clusters. SK Group’s USD 4 billion alliance with AWS in Ulsan will scale from 41 MW in 2027 to 103 MW by early 2029, illustrating phased power-envelope planning for AI inference loads. Samsung Electronics likewise finalized its Hwaseong HPC Center after investing KRW 1.5 trillion (USD 1.13 billion) to house 116,000 servers, reinforcing sovereign AI objectives.[1]Yoon-Seok Kim, “Samsung Completes Hwaseong HPC Campus,” Maeil Business Newspaper, mk.co.kr Upstream, HD Hyundai Electric has allocated USD 274 million to expand transformer output by 30% as domestic utilities race to fulfill data-center interconnect requests. These capital flows reposition the South Korea data center construction market as a preferred launchpad for regionwide AI workloads, stimulating specialized construction demand across electrical, mechanical, and security subsystems.

Government’s 3 GW AI data-hub initiative reshapes regional development

Jeollanam-do’s preliminary accord with Stock Farm Road calls for a USD 35 billion, 3-gigawatt campus that begins ground-breaking in winter 2025 and wraps by 2028.[2]Isabelle Gallagher, “Jeollanam-do Signs 3 GW Data-Hub Deal,” Capacity Media, capacitymedia.com The megaproject alleviates grid congestion in Pangyo and Songdo while creating 10,000 direct jobs and USD 3.5 billion in early-stage revenue. State support—expedited permitting, sub-station upgrades, and tax credits—signals a durable political commitment to disperse capacity beyond Seoul. Consequently, the South Korea data center construction market is witnessing a geographic re-weighting as land-hungry hyperscalers secure multi-hectare plots in secondary provinces where renewable energy pipelines are deeper and land prices are one-third of capital-area averages.

Chaebol cloud-migration accelerates enterprise infrastructure demand

Stacks blending colocation cages, native cloud, and private cores. The managed-services segment cleared KRW 7 trillion (USD 5.3 billion) in 2024 turnover, buoyed by CJ OliveNetworks and KT’s service expansions. Samsung SDS is spending KRW 21.5 billion to stand up an AI-centric facility at Gumi that will interlink directly with semiconductor production lines. This enterprise refactoring fuels rack-density upgrades, propelling the South Korea data center construction market toward higher average power allotments per square meter.

5G and private-5G networks drive edge-computing infrastructure

NAVER Cloud’s private 4.7 GHz network at Hoban Construction’s site covers 40,000 m², enabling autonomous drones and wearable safety gear. As manufacturing and logistics facilities replicate the model, demand shifts toward micro-modular data centers positioned inside industrial campuses. Contractors therefore bundle telecom shelters, battery arrays, and liquid-to-chip cooling kits in a single mobilization cycle, enlarging the serviceable obtainable market for the South Korea data center construction market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-connection bottlenecks around Greater-Seoul | -2.8% | Greater Seoul metropolitan area | Short term (≤ 2 years) |

| Public opposition on power-intensive projects | -1.9% | National, concentrated in urban areas | Medium term (2-4 years) |

| Escalating land-prices in Pangyo and Songdo tech-valleys | -1.6% | Pangyo and Songdo tech valleys | Short term (≤ 2 years) |

| Under-reported: MoEF tax-incentive sunset for DC cooling equipment (2027) | -1.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-connection bottlenecks constrain Seoul-metropolitan expansion

Electric demand from AI clusters is projected to double by decade-end, outpacing grid-reinforcement budgets at financially stressed KEPCO. Developers now face multi-year waits for 154 kV tie-ins, inflating project schedules and carrying costs. The 11th Basic Plan for Electricity envisions 121.9 GW of renewables by 2038, yet analysts cite a shortfall relative to data-center power trajectories.[3]Simon Nicholas, “Korea’s Grid Faces Data-Center Crunch,” IEEFA, ieefa.org As a result, operators pivot to Jeollanam-do and Ulsan, where interconnection queues are shorter and LNG-cold-energy synergies exist, thereby redefining site-selection heuristics in the South Korea data center construction market.

Public opposition emerges as significant development risk

Community groups halted a Seoul data-center build in January 2025 over energy-consumption worries. National carbon-reduction pledges—40% below 2018 baselines by 2030—catalyze scrutiny of water usage and Scope 2 emissions. Developers counter with district-heating tie-ins, on-site solar roofs, and hydrogen-fuel-cell pilots, yet permitting timelines are lengthening, raising the non-technical risk profile inside the South Korea data center construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Mission-Critical Infrastructure Drives Premium Demand

Tier 3 facilities represent the backbone of domestic fintech, cable-TV billing, and public-sector workloads, capturing 63.72% of the South Korea data center construction market share in 2025. Their concurrent-maintainability architecture aligns with local uptime regulations. As hyperscalers deploy multi-cluster AI farms, demand tilts toward Tier 4, which is expanding at a 16.88% CAGR and is forecast to absorb an additional 400 MW by 2030. The South Korea data center construction market size for Tier 4 builds is projected to swell to USD 4.88 billion by 2031. Construction majors are retooling supply chains to source 2N transformers and chilled-water ring loops, while facilities management firms adopt digital twins for predictive maintenance. Lower-tier builds still serve dev-test sandboxes and edge POPs, but their relative importance is receding.

Rising availability SLAs push Korean insurers and banks to migrate core ledgers into Tier 3+ footprints. Samsung C&T pilots submerged-server tanks to achieve PUE targets below 1.15, thereby meeting both redundancy and energy benchmarks. With demand high, some operators pre-sell capacity two years prior to go-live, locking in power tariffs amid inflationary pressures. Market observers expect Tier 4 rack densities to breach 40 kW by 2027, underscoring a power-first design ethos inside the South Korea data center construction market.

By Data Center Type: Hyperscaler Self-Build Momentum Accelerates

Colocation suites commanded 53.35% of 2025 revenue after onboarding hundreds of mid-cap enterprises facing capex constraints. However, hyperscalers prefer proprietary campus designs, pushing the self-build slice toward an 18.35% CAGR. The South Korea data center construction market size attached to hyperscaler projects is forecast at USD 7.64 billion in 2031. Design-build contractors must therefore integrate liquid-immersion cooling, 3 MW power blocks, and 48 V DC busways. Edge micro-sites, while growing, remain below 5% share.

SK-AWS Ulsan’s 60,000-GPU phase alone commands more concrete than twelve average colocation builds combined, illustrating the scale differential. Contractors are incorporating LNG cold-energy exchangers and seawater intake tunnels to hit operating-cost targets. Concurrently, enterprise CIOs negotiate hybrid burst pathways, ensuring colocation demand stays resilient. This dual-track demand keeps the South Korea data center construction market pluralistic even as hyperscalers scale vertically.

By Electrical Infrastructure: Power-Distribution Innovation Leads Growth

Backup systems (UPS, generators) held 55.48% share of electrical spend in 2025, reflecting high-availability mandates. Yet AI racks draw peak loads beyond 70 kW, compelling a pivot toward advanced switchgear and solid-state transformers, the fastest-growing sub-segment at 18.92% CAGR. The South Korea data center construction industry benefits from local supply depth: LS Electric ships busduct assemblies to Memphis for xAI facilities, showing export competitiveness.

HD Hyundai Electric’s added 30% transformer capacity enabling shorter lead times for domestic builds. Meanwhile, Hyosung Heavy scales Memphis plant output to 200 units by 2026, hedging against currency swings and US tariff risks. Intelligent PDUs with embedded analytics now ship standard, giving operators real-time phase-imbalance alerts. Collectively, these shifts elevate electrical capex intensity per megawatt, bolstering revenue visibility across the South Korea data center construction market.

By Mechanical Infrastructure: Cooling Innovation Addresses AI Demands

Cooling systems commanded 41.92% expenditure in 2025, with chilled-water loops and rear-door heat exchangers dominant. GPU clusters push inlet temperatures upward, accelerating adoption of direct-to-chip liquid cooling. Servers and storage cabinets, the fastest-growing slice at 15.78% CAGR, embed copper cold-plates to dissipate 800 W chips. This dynamic raises overall mechanical-to-electrical spend ratios within the South Korea data center construction market.

Samsung C&T’s underwater-cooling proof-of-concept aims to route coolant through coastal pipelines for free-cooling potential of 5 °C seawater. Rack vendors are standardizing 48U form factors that accept 1.5-inch coolant quick connects, shortening install cycles. Fire-suppression systems integrate early smoke aspirating detection due to liquid-cooling condensation risk. These mechanical innovations sharpen Korea’s value proposition versus land-constrained peers such as Singapore.

Geography Analysis

Greater Seoul retained roughly 67.15% of installed IT load in 2025, but grid queues and land inflation—KRW 30,000-50,000 per m²—are eroding its dominance. The South Korea data center construction market size for capital-area builds is projected to plateau by 2027. Grid-approved capacity is rationed, forcing some developers to consider onsite gas turbines. Municipalities are tightening zoning around Pangyo Techno Valley, adding procedural friction. Despite these obstacles, investors still prize the metro’s dense fiber rings and enterprise adjacency, ensuring a pipeline of brownfield reconversions within industrial parks.

Jeollanam-do’s 3 GW blueprint repositions the southwest as the country’s largest future power sink. Land prices under USD 150 per m² and ample renewable potential offer a compelling math for hyperscalers. Ulsan, armed with LNG import terminals, has emerged as a cold-energy hub, enabling SK-AWS to deploy heat-recovery chillers at scale. Busan pursues subsea-cable landing proximity to cultivate disaster-recovery nodes, while Daegu markets geothermal cooling advantages. Collectively, these initiatives diversify the South Korea data center construction market footprint.

Regional governments bundle workforce grants, tax holidays, and expedited 154 kV tap-lines, slashing greenfield timelines by nine months on average. Telecom carriers extend dark-fiber backbones, mitigating latency penalties for workloads replicated into Seoul. As more capacity surfaces in periphery provinces, colocation prices in Songdo have shown early signs of moderation. Investors forecast that by 2031, non-Seoul regions may collectively hold 45.60% of national IT load, underscoring structural realignment within the South Korea data center construction market.

Competitive Landscape

Fragmentation persists, with the top five builders holding roughly 46% combined 2024 revenue. Samsung C&T, Hyundai E&C, and GS E&C leverage multibillion-dollar balance sheets to guarantee bonded schedules but increasingly partner with niche engineering firms for liquid-cooling and DC-bus retrofits. International developers—NTT GDC, DCI Data Centers, and Equinix—expand via JV structures that de-risk local compliance. Start-ups focused on modular edge pods capture industrial IoT demand along shipping corridors. This multiplicity sustains a vibrant South Korea data center construction market.

Technology partnerships distinguish bids. Samsung C&T’s 2024 MOU with Shell Energy explores hydrogen-fuel-cell power plants to secure off-grid redundancy, a tactic resonating with municipalities eyeing decarbonization targets. GS E&C co-develops digital twins with Dassault Systèmes to compress commissioning cycles by 20%. Such differentiators win premium margins, especially.

South Korea Data Center Construction Industry Leaders

Samsung CandT Corporation

Hyundai Engineering and Construction

DL EandC (Daelim)

GS Engineering and Construction

SK ecoplant

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SK Group and AWS unveiled a USD 4 billion plan for a 60,000-GPU AI data center in Ulsan, ramping from 41 MW in 2027 to 103 MW in 2029.

- June 2025: LG Energy Solution began mass-producing 17 GWh of LFP batteries in Michigan to serve AI-driven data-center storage needs.

- March 2025: HD Hyundai Electric committed USD 274 million to raise transformer capacity by 30% at Alabama and Ulsan plants.

- March 2025: Hyosung Heavy Industries announced plans to lift Memphis transformer output above 250 units by 2027.

- February 2025: Stock Farm Road signed a preliminary pact with Jeollanam-do to build a 3 GW, USD 35 billion AI campus.

- January 2025: LS Electric secured a distribution-board contract for Elon Musk’s xAI data centers in Memphis.

- December 2024: Samsung SDS disclosed a KRW 21.5 billion AI-focused data center at Samsung’s Gumi plant.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines South Korea's data center construction market as all capital outlays dedicated to planning, engineering, and erecting new green or brownfield facilities that house compute, network, power, and cooling plant. Renovation, routine fit-outs, and ongoing operations are left outside the scope.

Scope exclusion: Minor retrofit and facilities management spend is not modeled.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with EPC project managers, MEP engineers, utility planners, and colocation procurement leads across Seoul, Busan, and Jeollanam-do. These interviews verify build cost per megawatt, lead times, and tier migration intentions that secondary data cannot fully capture.

Desk Research

We start with public sources such as the Ministry of Science and ICT statistical yearbooks, MOLIT building permit filings, Korea Customs Service shipment logs, and Korea Data Center Council white papers that track capacity pipelines. Academic journals on liquid cooling and patent filings refine technology cost curves. To tighten revenue bands, we consult D&B Hoovers for contractor financials and Dow Jones Factiva for project news. The sources named illustrate our wider desk work and are not exhaustive.

Market-Sizing & Forecasting

A top-down build links national IT load additions with average cost per MW, which is then filtered through tier mix, regional incentives, and rack density drift before selective bottom-up contractor roll-ups fine-tune totals. Inputs include approved power capacity, average PUE, GPU deployment ratios, steel price indices, and exchange rate trends. Five-year views deploy multivariate regression blended with scenario analysis to reflect policy or currency shocks.

Data Validation & Update Cycle

Outputs pass variance checks against independent capacity trackers; anomalies trigger fresh stakeholder calls before sign-off. We refresh models annually and issue interim updates for major project announcements.

Why Mordor's South Korea Data Center Construction Baseline Earns Trust

Published estimates often diverge because firms pick different cost baskets, capacity proxies, and refresh dates. Our disciplined scoping and yearly audit keep the baseline steady.

Other publishers may fold in retrofit capex, omit Tier 4 builds, or escalate spend using global multipliers rather than local curves, whereas Mordor updates figures with live project data. Public estimates span USD 5.54 billion to USD 1.14 billion for 2024, underscoring the need for clarity.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.03 B (2025) | Mordor Intelligence | - |

| USD 5.54 B (2024) | Regional Consultancy A | Retrofit spend partly included |

| USD 5.25 B (2024) | Global Consultancy B | Uses global cost per MW multiplier |

| USD 1.14 B (2024) | Trade Journal C | Mechanical systems only |

The comparison shows our 2025 figure sits between retrofit heavy totals and narrow infrastructure only counts, giving decision makers a balanced, transparent baseline that is traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the South Korea data center construction market?

The market is valued at USD 6.99 billion in 2026 and is projected to reach USD 14.63 billion by 2031.

Which segment is growing fastest within the South Korea data center construction market?

Hyperscaler self-build deployments are expanding at an 18.35% CAGR, reflecting cloud providers’ preference for custom, AI-ready campuses.

Why are secondary provinces attracting new data centers?

Regions like Jeollanam-do and Ulsan offer lower land costs, available grid capacity, and government incentives, relieving congestion in Greater Seoul.

How are power-grid constraints affecting project timelines?

Interconnection queues around Seoul can delay large projects by several years, pushing developers to seek sites with ready access to transmission capacity.

What cooling innovations are being adopted for AI workloads?

Direct-to-chip liquid cooling, LNG cold-energy exchanges, and experimental underwater loops are emerging to manage high-density GPU clusters.

How concentrated is the competitive landscape?

The top five construction firms hold about 46% of market revenue, indicating moderate concentration with room for specialized entrants.

Page last updated on: