Signals Intelligence (SIGINT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.63 Billion |

| Market Size (2031) | USD 26.34 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Signals Intelligence (SIGINT) Market Analysis by Mordor Intelligence

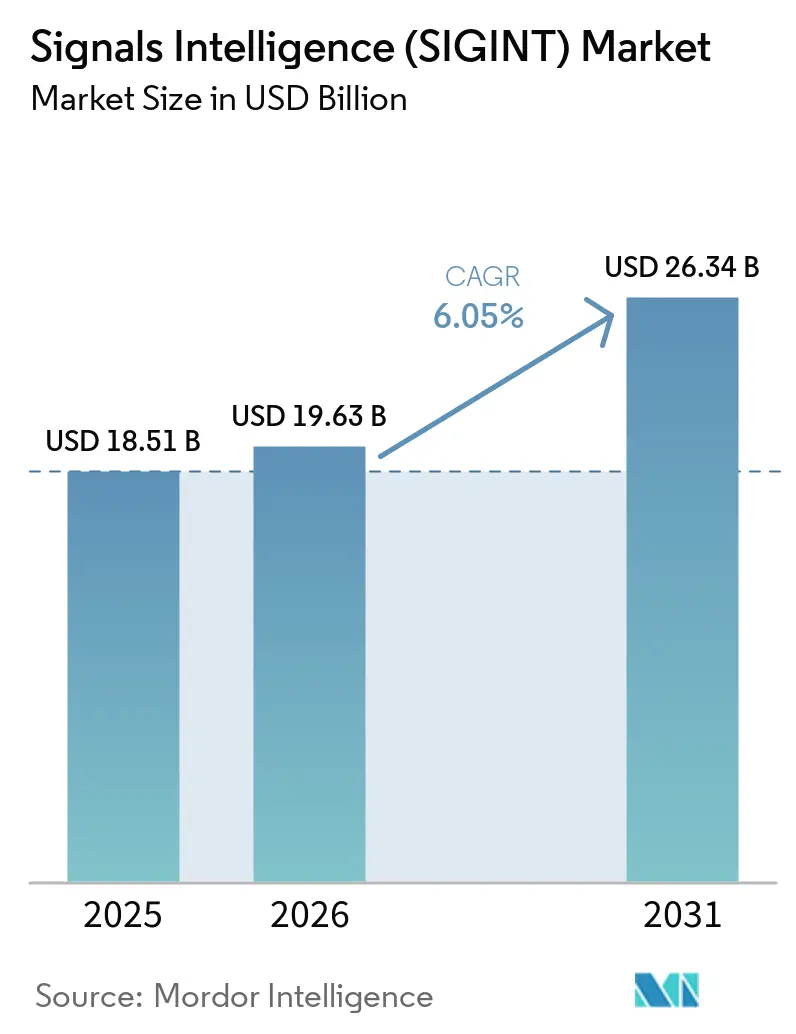

The Signals Intelligence Market size was valued at USD 18.51 billion in 2025 and estimated to grow from USD 19.63 billion in 2026 to reach USD 26.34 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031).

Accelerating defense outlays across NATO members and key Asia Pacific powers, rapid advances in software-defined radios, and the growing need to monitor proliferating Low Earth Orbit (LEO) satellites underpin this outlook. Cross-domain fusion initiatives, such as NATO’s shift toward multi-domain operations, are steering procurement toward open-architecture platforms that can ingest data from air, land, sea, space, and cyber sensors. At the same time, artificial intelligence-driven analytics are shortening decision-making cycles, while commercial constellation operators are lowering the barrier to strategic space coverage for mid-tier militaries. Persistent challenges include spectrum congestion, end-to-end encryption that blunts traditional collection techniques, and export-control revisions that restrict technology transfers. Even so, the signals intelligence market continues to attract new entrants ranging from satellite start-ups to cybersecurity specialists.

Key Report Takeaways

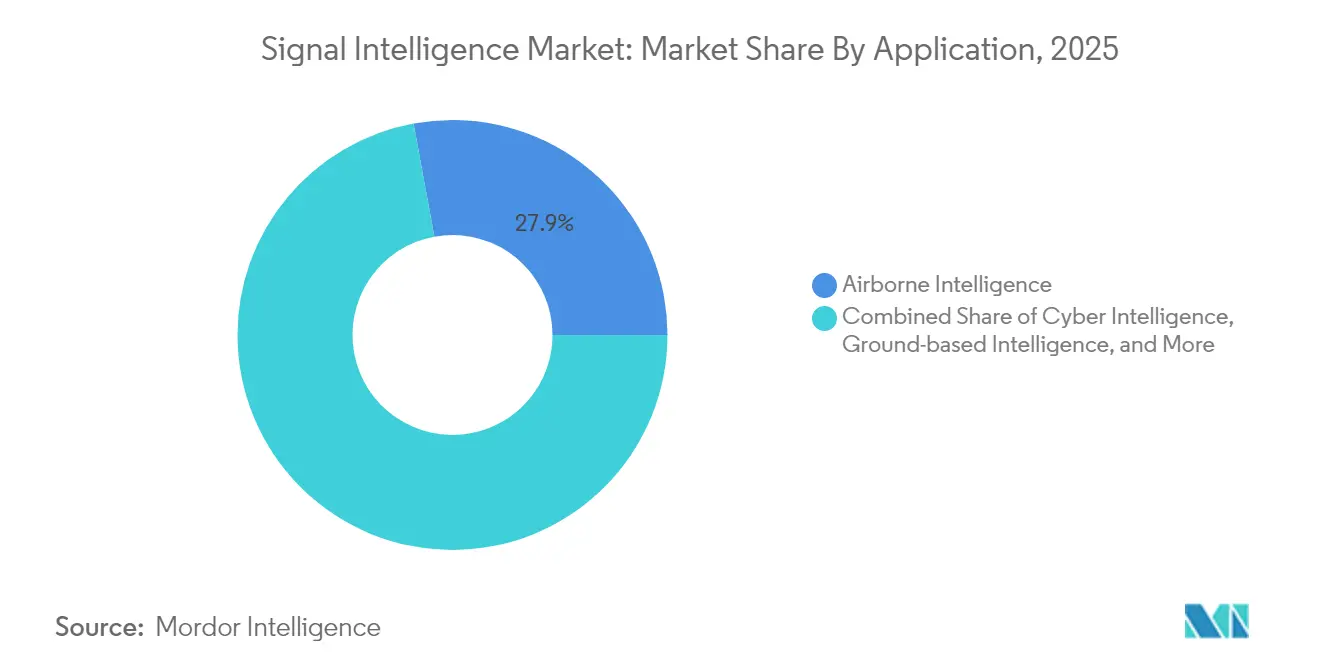

- By application, Space Intelligence commanded 27.84% of the signals intelligence market share in 2025, while its 7.09% CAGR makes it the fastest-growing segment to 2031.

- By type, Foreign Instrumentation Signals (FISINT) grew at 7.74% CAGR, outpacing Electronic Intelligence (ELINT), which retained the largest 51.35% revenue share in 2025.

- By platform, airborne systems held 32.45% revenue in 2025, whereas space platforms are forecast to expand at an 7.68% CAGR through 2031.

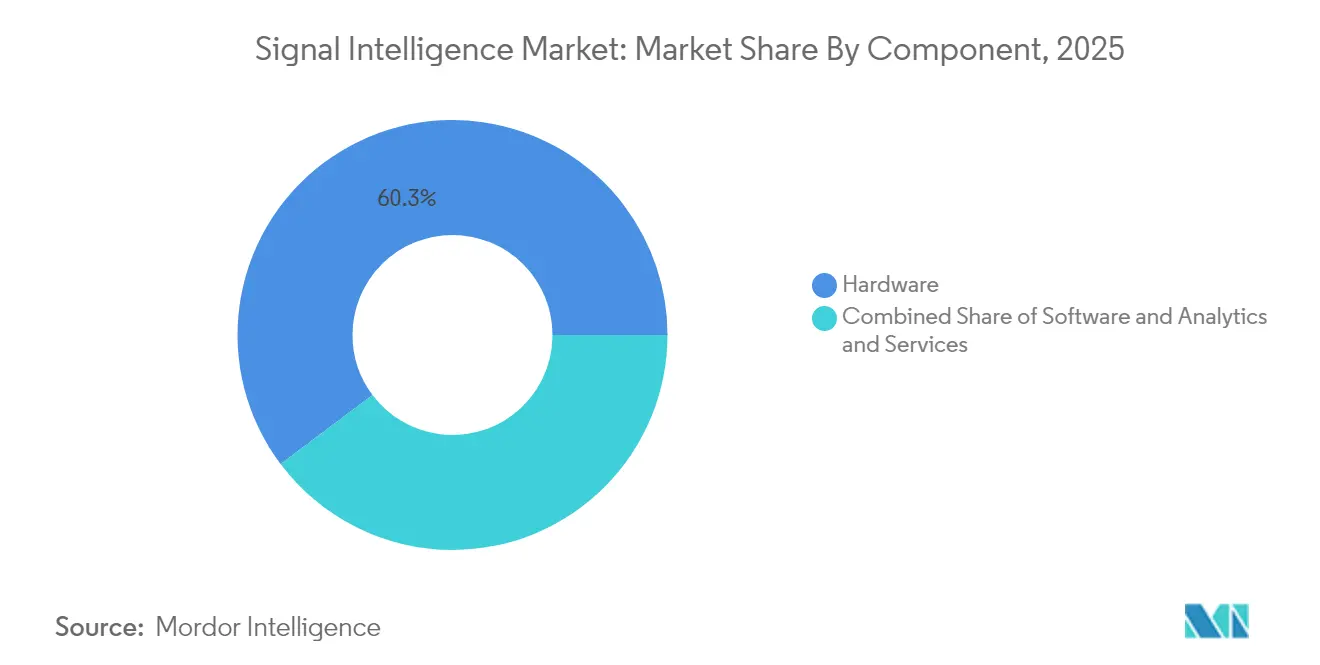

- By component, hardware accounted for 60.25% of the signals intelligence market size in 2025, but software and analytics lead growth at 6.92% CAGR.

- By end-user, defense forces retained 71.10% revenue in 2025, while commercial space and telecom providers are set to post an 7.95% CAGR to 2031.

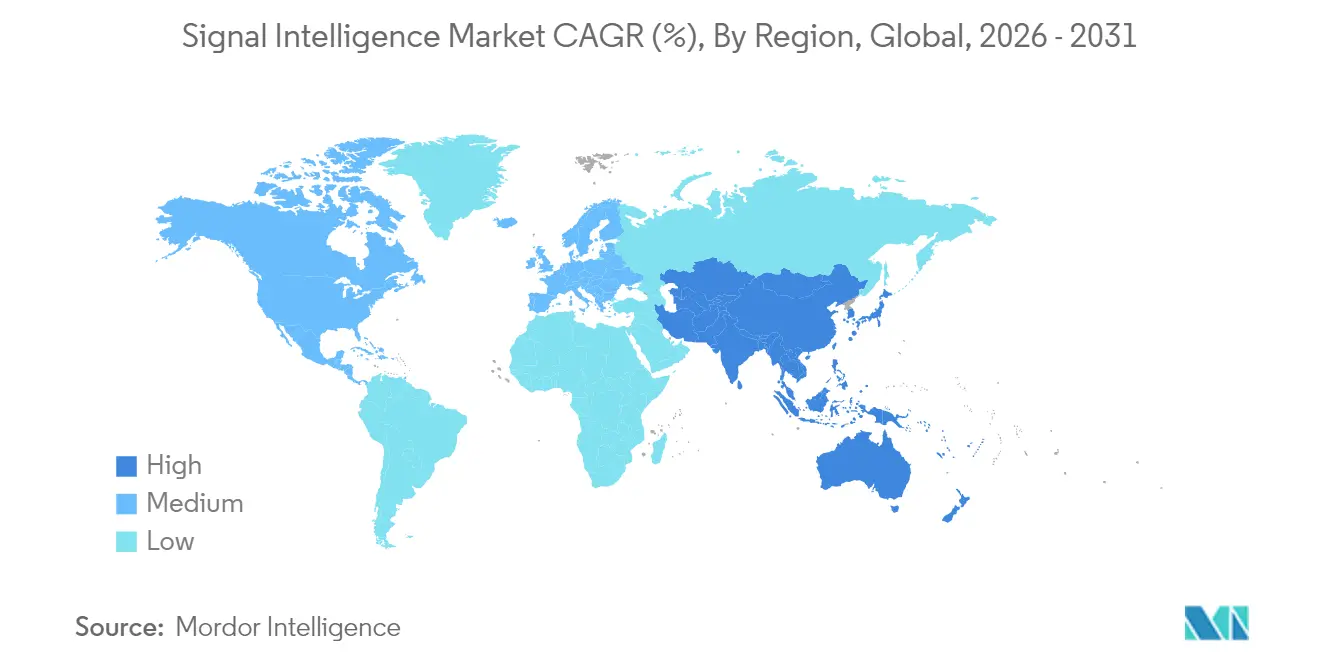

- Regionally, Asia Pacific recorded the fastest 8.15% CAGR, driven by Japan’s USD 59 billion defense budget and India’s new space-based networks.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Signals Intelligence (SIGINT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI/ML-enabled automated signal-processing efficiencies | 1.50% | United States, EU, Japan, South Korea | Medium term (2-4 years) |

| Multi-domain operations driving cross-platform SIGINT fusion | 1.80% | NATO states, AUKUS partners, key APAC allies | Long term (≥4 years) |

| Global defense budget expansion across NATO and APAC | 2.10% | North America, Europe, Asia Pacific | Short term (≤2 years) |

| Commercial LEO mega-constellations creating new intercept layers | 1.30% | Worldwide, with priority over contested oceans and border regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

AI/ML-Enabled Automated Signal Processing Efficiencies

Project Linchpin is creating a centralized AI ecosystem for the U.S. Army, delivering near-real-time insights that were previously human-intensive. The National Geospatial-Intelligence Agency now circulates AI-generated products, cutting analyst workloads and accelerating tasking cycles. Contractors are investing accordingly; General Atomics acquired North Point Defense in March 2025 to secure proprietary algorithms for autonomous signal processing[1]General Atomics, “GA-ASI Completes Acquisition of North Point Defense,” ga.com. DoD AI spending grew from USD 600 million in 2016 to USD 1.8 billion in 2024 across 685 projects. Beyond speed, AI augments resilience by flagging spoofing and jamming attempts that evade rule-based filters.

Multi-Domain Operations Driving Cross-Platform SIGINT Fusion

NATO earmarked EUR 32 million in 2024 for a service-oriented architecture that links airborne early-warning, cyber, and maritime sensors into a single intelligence backbone. The U.S. Fish Hook Undersea Defence Line integrates submarine, surface, and aerial collectors across the Pacific, proving the need for ocean-to-space coverage. In parallel, OneWeb and Eutelsat validated multi-orbit terminals that hand off between GEO and LEO links during NATO exercises. Japan’s 2024 surveillance satellite launches support regional monitoring and humanitarian assistance, underscoring dual-use expectations. New data-standard mandates such as STANAG 4774/4778 force vendors to deliver interoperability from day one.

Global Defense-Budget Expansion Across NATO and APAC

Japan increased defense spending by 9.4% to USD 59 billion for FY 2025, prioritizing intelligence upgrades. NATO’s 2025-2029 Common Funding Plan emphasizes ISR as a core pillar, accelerating joint procurement. India allocated USD 2 billion to acquire 12 extra-large unmanned underwater vehicles (XLUUVs) with integrated SIGINT payloads. The U.S. intelligence topline neared USD 100 billion in FY 2023, split between National and Military Intelligence Programs. Yet GAO warns that semiconductor supply delays could push key space programs beyond schedule, tempering near-term fielding

Commercial LEO Mega-Constellations Creating New Intercept Layers

SpaceX’s Starshield secured USD 2 billion from the National Reconnaissance Office for 21 classified satellites, giving the U.S. proliferated global coverage by 2025. HawkEye 360 teamed with Lockheed Martin to fly a 21-satellite RF-mapping network that already serves UAE customers. China’s Qianshao and Yaogan fleets extend naval geolocation reach into the Indian Ocean, forcing neighbors to adopt counter-collection measures. Russian hackers routinely probe Starlink terminals with spoofing and jamming, exposing the cybersecurity demands of space infrastructure. The upshot is that the signals intelligence market must now factor orbital resilience and cyber-hardening into every procurement brief.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum congestion & end-to-end encryption | −1.1% | Dense urban, privacy-focused regions | Long term (≥4 years) |

| Cyber-physical vulnerabilities at ground sites | −0.6% | Contested theaters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Spectrum Congestion and End-to-End Encryption Challenges

Meta activated default end-to-end encryption for over 1 billion Messenger users in 2024, closing a vast data stream that intelligence agencies once exploited. The Hudson Institute argues that limited U.S. spectrum access could erode tactical options versus well-resourced adversaries. CSIS finds that spectrum availability correlates directly with national security innovation. Agencies respond by increasing cyber insertion and partnering with telecom operators for lawful access, but the margin for traditional over-the-air intercept keeps shrinking.

Cyber-Physical Vulnerabilities at SIGINT Ground Stations

RAND research shows wide disparities in cybersecurity controls across commercial and military satellite ground sites, leaving doors open to state-sponsored intrusion. The U.S. Space Force, therefore, designates cyber defense as a cornerstone of mission assurance, launching red-team campaigns against its own gateways. Russia’s offensive toolset ranges from DDoS to supply-chain attacks that target firmware in modems connected to ground terminals. India’s new Joint Doctrine for Cyberspace Operations mandates indigenous operating systems to shrink foreign attack surfaces. Investment is thus shifting toward zero-trust architectures and encrypted telemetry links.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Space Intelligence Drives Next-Generation Capabilities

Space Intelligence held 27.84% of the signals intelligence market share in 2025 and is forecast at a 7.09% CAGR through 2031. This slice of the signals intelligence market gains momentum from proliferated LEO constellations that promise persistent coverage even under kinetic attack. The National Reconnaissance Office’s USD 2 billion Starshield contract underscores how sovereign buyers prioritize orbital resilience for strategic awareness. Parallel civilian ventures, such as HawkEye 360’s RF-mapping service, entice mid-tier militaries that cannot fund sovereign satellites yet require fast cueing.

Airborne Intelligence still captures 27.90% revenue in 2025, supported by NATO’s order of six Boeing Wedgetail AEW&C jets, while Japan’s dedicated surveillance satellites demonstrate complementary roles for space and air sensors. Ground-based nodes confront increasing cyber-physical risk, prompting hardened shelters and redundant routing. Naval programs benefit from India’s USD 2 billion XLUUV procurement, marrying underwater stealth with satellite backhaul. Cyber Intelligence continues to grow as pervasive encryption pushes analysts toward endpoint exploitation. Lawful interception tools face regulatory headwinds, yet remain crucial for domestic security operations.

By Type: FISINT Emerges as Fastest-Growing Segment

Electronic Intelligence dominates the signals intelligence market with a 51.35% 2025 share, given its centrality in radar monitoring and electronic-order-of-battle mapping. However, FISINT is pacing an 7.74% CAGR as militaries seek telemetry from missile tests and space launch vehicles. China’s Yaogan clusters combine ELINT and synthetic-aperture radar, creating highly granular maritime awareness that nudges regional rivals to invest in comparable FISINT capabilities.

Communications Intelligence remains indispensable for diplomatic monitoring but is hampered by end-to-end encryption that hides voice and text payloads. Consequently, technical disciplines such as ELINT and FISINT supply alternative signatures that evade encryption barriers. Historical growth curves confirm that the signals intelligence industry shifts budget from manpower-intensive voice translation to high-throughput digital demodulation systems that feed AI analytics. This realignment favors vendors offering automated decoding, bit-level parsing, and integrated mission data files.

By Platform: Space Systems Accelerate While Airborne Leads Revenue

Airborne assets controlled 32.45% revenue in 2025 because of their deployability and enduring upgrade pipeline. Yet space systems show an 7.68% CAGR, the fastest within the signals intelligence market, as commercial launch cost lows make multi-plane constellations viable. The U.S. Army’s theater-level programs emphasize ground collectors for tactical cues, but commanders increasingly rely on LEO feeds to confirm contacts.

Naval platforms integrate SIGINT masts and UUV payloads, reflecting the shift toward autonomous blue-water surveillance. Unmanned air and surface vehicles extend dwell times and reduce crew risk, while portable man-pack solutions benefit from affordable SDR modules. Supply-chain chokepoints for advanced chips pose headaches for hardware planners, elevating the value of software-defined upgrades that can port across CPU generations without board redesign.

By Component: Software and Analytics Capture New Value Pools

Hardware still accounts for 60.25% of the signals intelligence market size, covering antennas, receivers, and SDR boards. Yet software and analytics will grow 6.92% annually, driven by machine-learning pipelines that distill petabytes of I/Q samples into geolocated alerts. NGA’s automated imagery-to-signal correlation workflow proves that mature AI can bypass several analyst review layers.

Service providers offer lifecycle integration, training, and MRO, ensuring that complex platforms deliver intended performance. Semiconductor shortages underline why software-centric roadmaps are attractive: features can roll out via secure patches without waiting for foundry capacity. Meanwhile, the convergence of hardware and software through open-architecture SDR frameworks empowers users to retask radios from COMINT to ELINT with a firmware change, fostering mission agility.

By End-user: Commercial Entrants Disrupt Traditional Procurement

Defense organizations retained 71.10% of 2025 revenue, yet commercial space and telecom operators will outpace the wider signals intelligence market at an 7.95% CAGR. HawkEye 360 exemplifies dual-use growth by selling maritime RF tracking to both navies and insurers. Homeland security agencies need new lawful access solutions as encryption spreads, while critical-infrastructure players deploy RF sensors to spot spoofing and jamming around power grids.

Regulatory adjustments, such as the U.S. BIS waiver on select spacecraft exports to AUKUS partners, ease international program formation. In parallel, dual-use megaconstellations like Starshield blur lines between military and commercial service provisioning. The signals intelligence industry, therefore, sees venture-backed newcomers bidding head-to-head with legacy primes for orbital task orders, intensifying price competition and innovation velocity.

Geography Analysis

North America held 41.60% revenue in 2025, bolstered by the nearly USD 100 billion U.S. intelligence budget and the National Reconnaissance Office’s large-scale Starshield investment. General Atomics’ purchase of North Point Defense shows how domestic primes deepen AI portfolios to defend leadership positions. Supply-chain risk remains a strategic worry because Taiwan still dominates advanced node semiconductor fabrication, highlighting a geopolitical Achilles’ heel.

Asia Pacific posts the fastest 8.15% CAGR, propelled by Japan's defense allocation of USD 59 billion in FY 2025 and India's push for sovereign space intelligence infrastructure. China’s expanding Yaogan and Qianshao constellations raise the intelligence baseline, compelling neighbors to counter-invest. India’s USD 2 billion XLUUV program illustrates maritime focus, while South Korea and Australia accelerate joint AUKUS initiatives to safeguard sea-lanes. Historical spending patterns show a pivot from platform acquisition to data-centric architectures that feed joint commands in near real time.

Europe records steady mid-single-digit growth as NATO harmonizes ISR requirements and the European Commission funds secure satellite connectivity. The EUR 32 million NATO command-and-control upgrade triggers demand for interoperable SIGINT nodes afcea.org. AUKUS export-control waivers accelerate UK collaboration with U.S. integrators, lowering program lead times. Elsewhere, the Middle East and Africa maintain moderate growth anchored in border security, while South American budgets lag amid fiscal constraints and limited access to high-end electronics.

Competitive Landscape

Market consolidation is gathering pace as leading primes acquire niche software and analytics firms to keep pace with AI-centric demand. General Atomics’ March 2025 takeover of North Point Defense aligns with this strategy, embedding autonomous analytics into its MQ and Orbital Test Vehicle lines. In April 2025, Leidos secured a USD 390 million NSA award covering engineering, analysis, and reporting, reflecting the appetite for turnkey platforms that bundle analytics with hardware.

Commercial entrants inject new competitive dynamics into the signals intelligence market. SpaceX’s Starshield, financed by an NRO contract, positions a private company as a frontline defense supplier. HawkEye 360 illustrates how venture-funded constellations can provide RF geolocation for state and commercial customers alike. Traditional contractors respond by partnering or buying spectrum analytics start-ups and by opening their proprietary interfaces to third-party apps.

White-space opportunities lie in protective cybersecurity for satellite ground networks, AI-driven RF anomaly detection, and data-standard toolkits that ease NATO STANAG compliance. NGA’s successful rollout of AI-generated intelligence feeds underscores the commercial potential of autonomous exploitation software. Overall, competition pivots on time-to-field and cyber resilience as end-users demand validated security accreditation along with high collection sensitivity.

Signals Intelligence (SIGINT) Industry Leaders

General Dynamics Mission Systems, Inc.

BAE Systems plc

Parsons Corporation

Rohde and Schwarz GmbH and Co KG

ThinkRF Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Leidos won a USD 390 million NSA contract covering engineering, analysis, and reporting for global SIGINT operations.

- March 2025: General Atomics acquired North Point Defense, adding AI/ML signal-processing IP for real-time ISR.

- January 2025: U.S. State Department finalized ITAR revisions that add new controls on uncrewed vessels and exoskeletons, effective September 2025.

- August 2024: Parsons completed its acquisition of BlackSignal to deepen SIGINT offerings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study from Mordor Intelligence defines the Signals Intelligence (SIGINT) market as the worldwide spending on equipment, software, and sustainment services that capture, decode, and analyze electromagnetic emissions, namely Communications Intelligence (COMINT), Electronic Intelligence (ELINT), and Foreign Instrumentation Signals (FISINT), deployed on land, naval, airborne, and space platforms for defense, homeland security, and selected critical infrastructure missions. The value chain covers sensors, antennas, on-board mission systems, signal processing suites, analytics middleware, and associated logistics support.

Scope exclusion: We intentionally exclude stand-alone cyber threat intelligence tools that mine network logs without any radio frequency collection capability.

Segmentation Overview

- By Application

- Cyber Intelligence (CYBINT)

- Ground-based Intelligence

- Naval Intelligence

- Space Intelligence

- Airborne Intelligence

- Lawful Interception and Telecom Monitoring

- By Type

- Electronic Intelligence (ELINT)

- Communications Intelligence (COMINT)

- Foreign Instrumentation Signals (FISINT)

- By Platform

- Airborne

- Ground

- Naval

- Space

- Unmanned Systems (UAV/UGV/USV)

- Portable/Man-pack

- By Component

- Hardware (Antennas, Receivers, SDRs)

- Software and Analytics

- Services (Integration, Training, MRO)

- By End-user

- Defense Forces

- Homeland Security and Law Enforcement

- Critical Infrastructure Operators

- Commercial Space and Telecom Providers

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Turkey

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured interviews with acquisition managers in the US and NATO, airborne ISR integrators in India, retired SIGINT officers in Israel, and spectrum policy officials in Japan. Feedback on sensor mixes, average selling prices, and upgrade cycles helped us refine model assumptions and close secondary data gaps.

Desk Research

Our analysts began by mapping open-source defense appropriation bills, Stockholm International Peace Research Institute military expenditure datasets, United States Federal Procurement Data System releases, European Defense Agency registers, and UN Comtrade import-export codes for surveillance radios to size the primary demand pool. Trade association briefs such as those from the Global Counter-UAS Council and ITU spectrum statistics added contextual volume indicators.

We then extracted company revenue splits from D&B Hoovers, scanned global news on Dow Jones Factiva, and reviewed SIGINT patent families through Questel to spot upcoming design wins. These sources are illustrative, and many other publications were reviewed for data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts with national defense electronics outlays, fleet counts of ISR aircraft, SIGINT satellites, man portable receivers, and related lifecycle budgets. Select bottom-up checks, for example, supplier roll-ups and sampled ASP × volume deliveries, validate and, where needed, calibrate totals. Key variables include regional defense budget trends, annual ISR aircraft deliveries, number of 5G base stations (proxy for signal density), software defined radio adoption, and conflict intensity indices. Multivariate regression supported by scenario analysis projects every driver to 2030, while logical constraints cap extreme outliers.

Data Validation & Update Cycle

Model outputs pass variance checks against historic contract tallies and inventory registries before senior analyst sign-off. Reports refresh annually, and interim updates are triggered by material events, while a last-minute sweep ensures clients receive the freshest view.

Why Our Signals Intelligence Baseline Commands Reliability

Published estimates often diverge because firms vary platform coverage, price bases, refresh cadence, and currency fixes. By anchoring values to verifiable defense spending and cross-checking with real procurement activity, Mordor Intelligence delivers a balanced benchmark.

Key gap drivers include whether commercial cyber tooling is blended into totals, the treatment of long-term service contracts, and the inflation factors applied to multi-year programs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.51 B (2025) | Mordor Intelligence | - |

| USD 17.20 B (2025) | Global Consultancy A | Excludes sustainment services, uses constant 2020 prices |

| USD 17.44 B (2024) | Industry Analysis B | Blends cyber threat intel software, limited primary validation |

The comparison shows that our disciplined scope selection, annual refresh cadence, and dual validation steps keep Mordor's baseline transparent and dependable for strategy teams that cannot afford mis-sized opportunity pools.

Key Questions Answered in the Report

How big is the signals intelligence market in 2026?

The signals intelligence market stands at USD 19.63 billion in 2026 and is on track for a 6.05% CAGR to 2031.

Which application area is growing fastest?

Space Intelligence leads growth at 7.09% CAGR owing to LEO constellation proliferation and large sovereign investments.

Why is Asia Pacific the fastest-growing region?

Rising defense budgets in Japan, India, Australia, and China’s expanding satellite fleets propel an 8.15% regional CAGR.

What technologies are reshaping SIGINT procurement?

AI-driven analytics, software-defined radios, and proliferated LEO constellations are now core requirements.

How is encryption affecting SIGINT operations?

End-to-end encryption on mainstream platforms reduces COMINT yields, pushing agencies toward cyber intrusion and technical ELINT/FISINT methods.

Page last updated on: