Dunnage Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

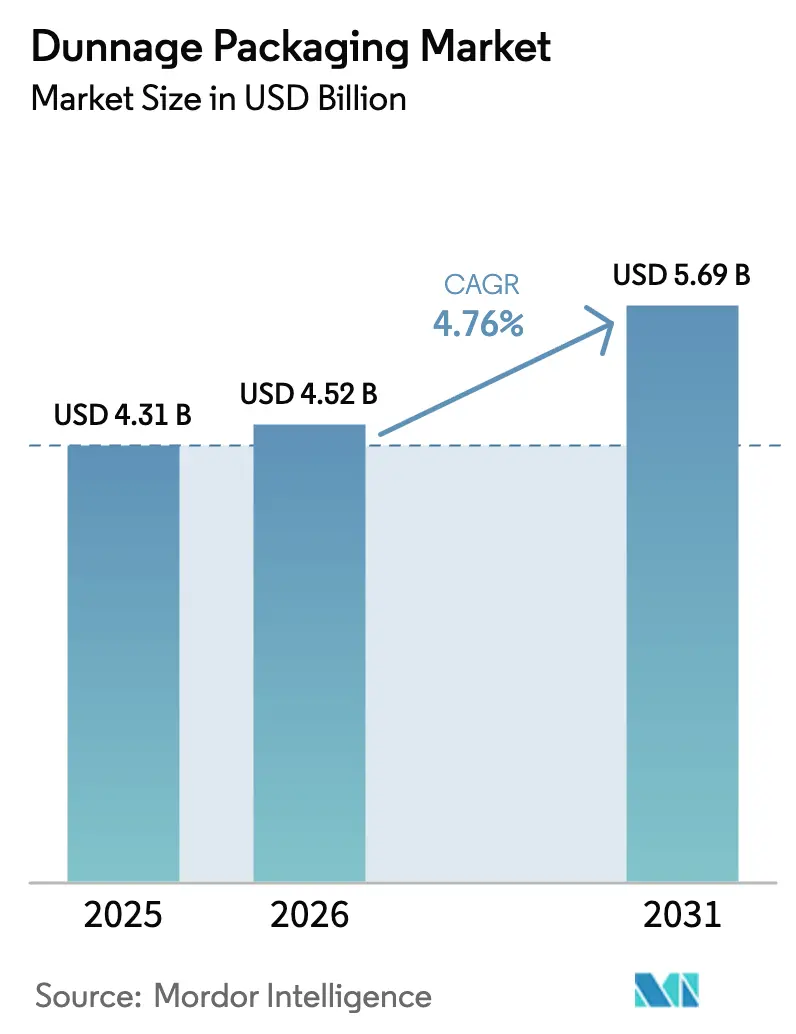

| Market Size (2026) | USD 4.52 Billion |

| Market Size (2031) | USD 5.69 Billion |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dunnage Packaging Market Analysis by Mordor Intelligence

The dunnage packaging market size was valued at USD 4.31 billion in 2025 and estimated to grow from USD 4.52 billion in 2026 to reach USD 5.69 billion by 2031, at a CAGR of 4.76% during the forecast period (2026-2031).[1]European Commission, “Regulation 2025/40,” eur-lex.europa.euContinued acceleration of e-commerce parcel volumes, the automotive industry’s pivot to electric vehicle (EV) battery logistics, and EU-wide recyclability mandates are shaping product innovation and procurement strategies. Plastic dunnage retains leadership because of durability and ease of cleaning, yet fiber-based materials are posting the fastest expansion as brand owners pursue circular-economy credentials. Reusable formats deliver the strongest value proposition by lowering total cost per trip, a metric that resonates with manufacturers looking to curb packaging taxes and landfill fees. Asia-Pacific is both the largest producing region and the fastest growing sales destination, fueled by Chinese and Indian infrastructure build-outs and electronics exports. Supply-side headwinds—chiefly polypropylene and paper-pulp price swings—are encouraging investment in mono-material designs and advanced recycling, reinforcing the long-term resilience of the dunnage packaging market.

Key Report Takeaways

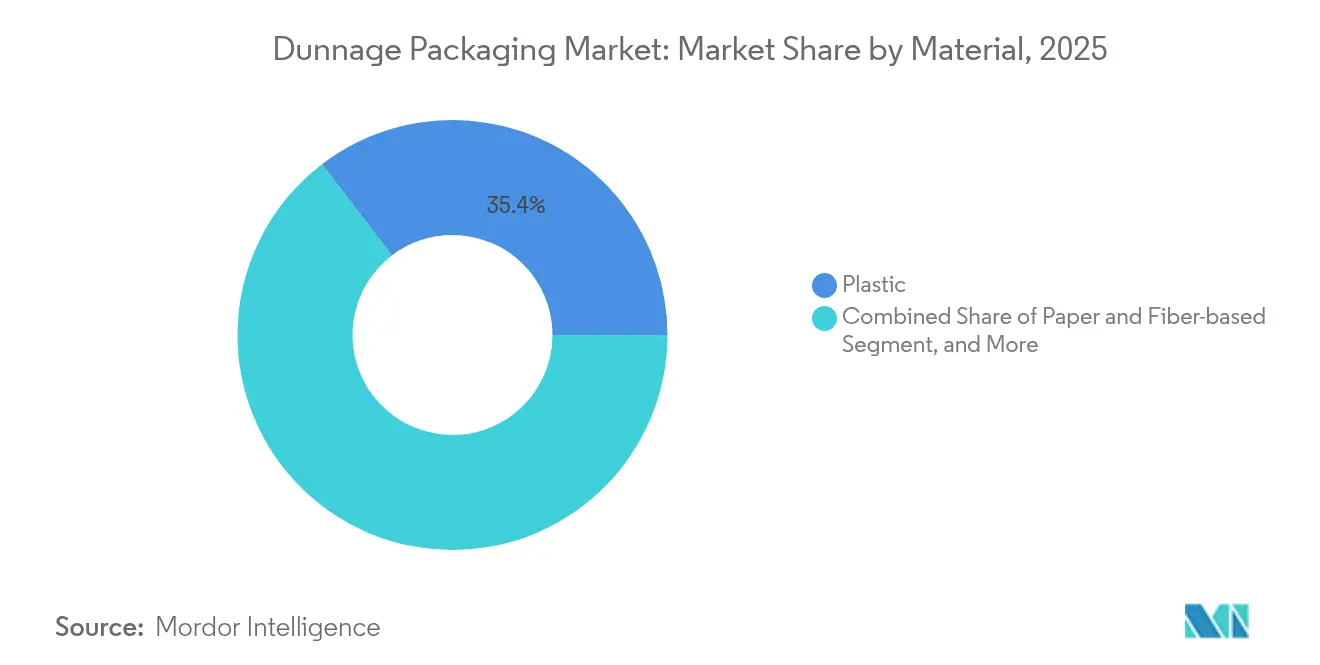

- By material, plastic captured 35.38% dunnage packaging market share in 2025; paper and fiber-based solutions are forecast to expand at an 8.36% CAGR to 2031.

- By packaging format, returnable/reusable systems held 57.93% of the dunnage packaging market size in 2025 and are growing at 5.55% CAGR through 2031.

- By product type, trays and inserts led with 30.15% revenue share in 2025, while inflatable air-bags record the highest projected CAGR at 7.18% to 2031.

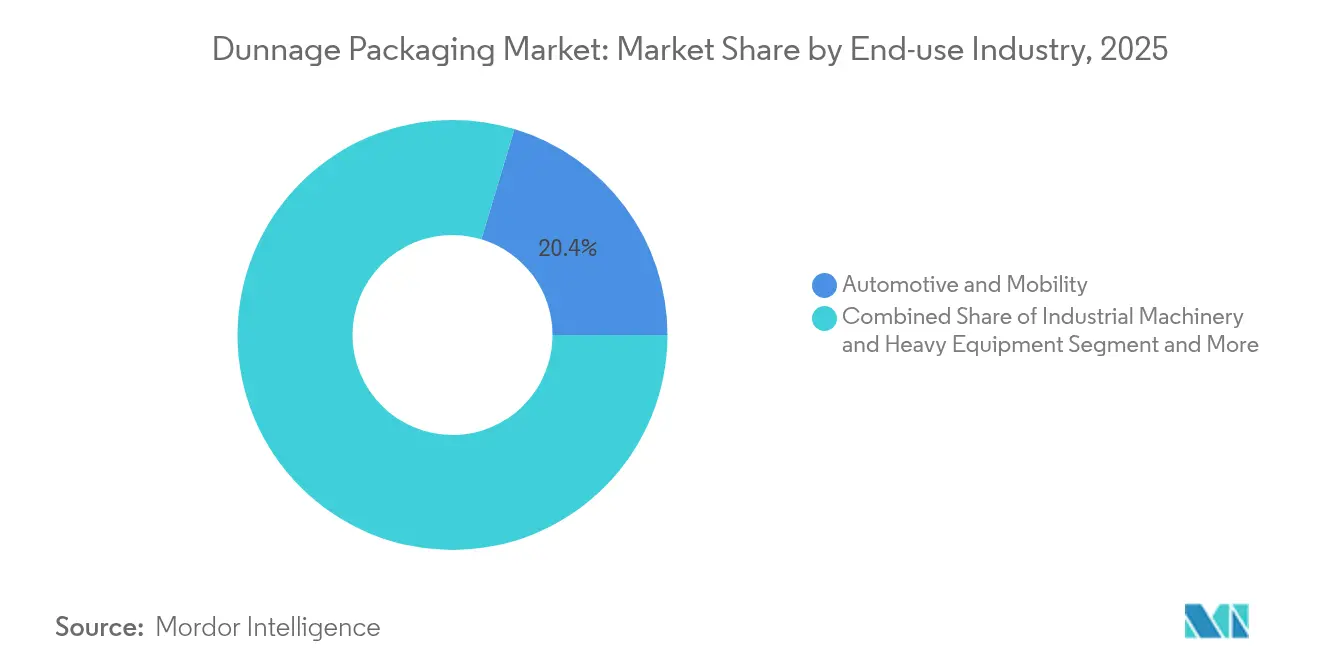

- By end-use industry, automotive and mobility accounted for a 20.35% slice of the dunnage packaging market size in 2025; electronics and semiconductors advance at an 7.88% CAGR through 2031.

- By geography, Asia-Pacific dominated with 38.10% share of the dunnage packaging market in 2025 and is set to grow fastest at 7.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Dunnage Packaging Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce parcel volumes | +1.2% | Global; strongest in North America & Asia-Pacific | Medium term (2-4 years) |

| OEM shift to lightweight reusable packaging | +0.8% | Global; led by Germany, US, China | Long term (≥ 4 years) |

| EU recycled-content mandates | +0.6% | Europe; spillover to North America | Short term (≤ 2 years) |

| Vision-guided robotics need dimensionally-consistent trays | +0.4% | Asia-Pacific core; expanding to North America & Europe | Medium term (2-4 years) |

| EV battery logistics demand ESD-safe dunnage | +0.3% | EV manufacturing regions worldwide | Long term (≥ 4 years) |

| Micro-fulfilment dark stores need compact inflatable dunnage | +0.2% | Urban centers globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Parcel Volumes

Dimensional-weight pricing and urban delivery constraints push retailers to right-size every shipment, prompting rapid adoption of automated on-demand box making and inflatable void-fill that matches each order’s footprint. Micro-fulfilment centers equipped with AI route-planning process up to 1,000 orders per hour, translating into strong pull for lightweight airbags that store flat and inflate instantly at pack stations. New Jersey legislation mandating cartons be at least 50% full catalyzes broader US compliance efforts, and Europe’s forthcoming PPWR heightens similar optimization imperatives. Suppliers such as Packsize claim 26% corrugated savings and 40% smaller box sizes for clients deploying their X5 line, outcomes that reinforce investment paybacks.

OEM Shift to Lightweight Reusable Packaging

Automotive and aerospace OEMs validate 50-cycle life targets for returnable containers, with flame-retardant polypropylene solutions enabling 30-50% weight savings versus steel racks while preserving part safety.[2]SABIC, “Thermoplastic Solutions for EV Batteries,” sabic.com Total cost of ownership models consistently favor reusable designs once shipment lanes exceed 100 km and component cost tops USD 50, encouraging global platforms to specify returnable dunnage at program launch. Rapid consolidation—exemplified by the Schoeller Allibert-IPL merger—expands geographic footprints so suppliers can backhaul empties economically.

EU Recycled-Content Mandates

The PPWR 2025/40 regulation compels 30% recycled content in PET food packaging by 2030 and applies equivalent targets to transport packaging, accelerating mono-material tray development and closing the door on hard-to-recycle multilayer laminates. Multinational brands streamline specifications to one global standard to avoid dual tooling, sending ripple effects into North America and Asia. Innovators such as DS Smith’s fiber-based TailorTemp® demonstrate how recyclability benchmarks can coexist with performance requirements in temperature-controlled logistics.

Vision-Guided Robotics Need Dimensionally-Consistent Trays

Machine-vision algorithms demand tolerance bands below 0.3 mm to guarantee accurate pick-and-place, pushing suppliers to adopt precision tooling, anti-warp resins, and metrology audits. The SASI 4.0 range illustrates next-generation load carriers engineered for low-vibration automated lines and validated in European appliance plants. Electronics assemblers, handling miniature chips, prioritize ESD shielding, creating a lucrative niche for conductive polypropylene trays.

Restraints Impact Analysis of Dunnage Packaging Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polypropylene and paper-pulp price volatility | −0.7% | Europe & North America | Short term (≤ 2 years) |

| Disposal hurdles for multi-material composites | −0.4% | Europe; expanding globally | Medium term (2-4 years) |

| Urban warehouse space constraints | −0.3% | Global urban centers | Medium term (2-4 years) |

| Product-integrated primary packs curbing secondary dunnage | −0.2% | Consumer goods & electronics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Polypropylene and Paper-Pulp Price Volatility

Energy shocks and Old Corrugated Container shortages lifted European paperboard prices by EUR 60/t in April 2025, with converters passing through costs that test customer loyalty. Hardwood-softwood pulp price spreads tripled against historical norms, prompting substitution debates and intermittently slowing fiber-based dunnage conversion plans. Equivalent volatility in polypropylene resin, aggravated by refinery outages, complicates budgeting for reusable plastics and can delay tooling investments.

Disposal Hurdles for Multi-Material Composites

Multilayer films account for 17% of flexible output, yet recycling rates remain marginal because shredders cannot separate adhesives, polymers, and barrier layers. Lack of global design-for-recycling standards hampers scaling of compatible sortation lines, while ongoing greenwashing probes foster consumer skepticism. As regulators tighten extended producer responsibility fees, brands hesitate to specify hybrid dunnage, stalling wider adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Dunnage Packaging Market Segment Analysis

By Material:

Plastic Dominance Faces Fiber ChallengePlastic solutions generated 35.38% of the dunnage packaging market in 2025, anchored by corrugated plastic totes, EPP foam, and conductive trays preferred by automakers and electronics assemblers. The segment continues to benefit from repeat-use life cycles and parts-per-container optimization, but tightening PP supply and end-of-life scrutiny spur customers to trial molded pulp and honeycomb fiber inserts. Fiber-based dunnage posts an 8.36% CAGR to 2031, leveraging retail pressure for recyclable packaging and rapid advances in thermoformed pulp that now achieves +/-0.5 mm tolerances suitable for consumer electronics.

Demand for metal, wood, and textile dunnage remains niche. Metal frames endure where 1-ton loads and forklift abuse favor steel; wood loses share as deforestation rules drive up compliance costs; textile wraps occupy luxury goods shipments where scuff prevention takes priority. Throughout the forecast window, resin additive packages and high-clarity cellulose fibers will shape competitive dynamics as brand owners weigh protection, cost, and sustainability in selecting future dunnage packaging market options.

By Packaging Format:

Reusable Solutions Drive Circular EconomyReturnable containers accounted for 57.93% of the dunnage packaging market size in 2025, underpinned by automotive loops that cover 600-1,000 km round-trip distances between component plants and final assembly. GPS sensors and IoT dashboards now trace asset utilization, shrinking idle time by 18% and validating 30-month payback periods. Reusable bins made from HDPE and polypropylene resist oils, solvents, and temperature swings, a benefit that secures long-term adoption in metal-stamping and EV battery lines.

Single-use formats retain relevance in frozen food and pharmaceutical exports that mandate pristine packouts and tamper evidence. Right-sizing algorithms and bio-based adhesives cut corrugated use by 94%, aligning expendable dunnage with tightening landfill levies. Looking ahead, the dunnage packaging industry is expected to witness hybrid models where fleets of pooled reusable crates coexist with compostable pads for last-mile segments, creating layered revenue streams for suppliers.

By Product Type:

Inflatable Solutions Gain MomentumTrays/inserts generated 30.15% of global revenue in 2025 because OEMs favor organized kitting that feeds robotic assembly lines without manual sorting. They underpin defect-free delivery of electronic boards, turbochargers, and precision optics. Inflatable air-bags, accelerating at 7.18% CAGR, thrive in e-commerce where void volume varies order-to-order and warehouse footprints are constrained. Their low deflated cube enables a 10:1 storage efficiency compared with foam peanuts, while on-site inflation slashes inbound freight.

Foam, void-fill paper, and custom racks round out the landscape. Foam’s shock-absorption matches high-value medical instruments; void-fill fibers cushion apparel without static build-up; racks serve aerospace castings too heavy for corrugated. Pallets, although mature, leverage RFID tags to support closed-loop logistics. Innovations such as sensor-equipped platforms that log shock events are gaining traction among semiconductor exporters wary of microfracture risk.

By End-use Industry:

Electronics Overtakes Automotive GrowthAutomotive and mobility held the largest revenue share at 20.35% in 2025, propelled by complex part geometries, rising EV battery exports, and safety regulations that demand flame-retardant, ESD-safe packaging. However, electronics and semiconductors is the fastest climbing sector at 7.88% CAGR, a trajectory sparked by chip miniaturization and the boom in consumer wearables. Cleanroom-compliant, static-dissipative trays safeguard delicate dies from contamination and electrical discharge, making this vertical a flashpoint for future dunnage packaging market expansion.

Aerospace and defense buyers specify ATA 300 and MIL-SPEC rated cases capable of resisting 1,000 cycles on vibration platforms, positioning ruggedized solutions as an enduring niche. Healthcare device makers lean heavily on polymer foams that deliver gamma-sterilizability, matching the single-use nature of 90% of med-device kits. Food and beverage, industrial machinery, and retail fulfillment complete the picture, each blending hygiene, load stability, and brand-experience requirements.

By Distribution Channel:

Direct Sales Maintain AdvantageDirect contracts accounted for 64.65% of global spend in 2025, reflecting the engineering complexity and custom tooling associated with many automotive, aerospace, and medical projects. The International Paper-DS Smith combination amplifies this model, coupling technical consultative selling with expanded North American and EMEA footprints. Suppliers leverage dedicated account teams and in-house design centers to integrate dunnage early in product-development cycles, boosting lock-in and margin capture.

Indirect channels grow at 5.68% CAGR as standardized SKUs, fold-flat crates, bubble mailers, and inflatable tabs, scale via distributors and e-commerce catalogs. Veritiv’s USD 1.19 billion acquisition of Orora Packaging Solutions reveals how distributors pursue critical mass to secure supplier rebates and private-label opportunities. Long term, digital marketplaces could commoditize simple dunnage forms, while intricate reusable programs remain tethered to direct sales.

Geography Analysis

APAC Dunnage Packaging Market

Asia-Pacific generated 38.10% of dunnage packaging market revenue in 2025 and is expanding at an 7.98% CAGR, fueled by China’s EV battery exports and India’s growing electronics contract-manufacturing base. Chinese tier-one automakers back-spec reusable polypropylene totes for gigafactory supply lines, while Indian smartphone assemblers demand ESD-grade trays to protect microprocessors during humid monsoon conditions. Government incentives for make-in-India programs widen the runway for local converters investing in precision thermoforming capacity. Simultaneously, Southeast Asian electronics clusters in Vietnam and Thailand outsource dunnage design to regional hubs, intensifying cross-border flows of both new crates and recovered void-fill paper.

North America Dunnage Packaging Market

North America represents a mature yet technologically progressive arena where robotics, micro-fulfilment, and e-commerce optimization set benchmarks adopted globally. New Jersey’s fullness law and the wave of curbside recyclability labeling guide procurement toward dim-weight-compliant, high-recycled-content packs. Manufacturers optimize reverse-logistics corridors, tying reusable pool rotations to third-party logistics nodes. Resin price volatility has nonetheless prompted packaging teams to maintain contingency designs in molded pulp, a hedge that restrains multi-year plastic tooling commitments. Future growth leans on automation investment as US distribution centers confront sustained labor scarcity.

Europe Dunnage Packaging Market

Europe balances stringent sustainability regulations with advanced manufacturing needs. The PPWR sets the stage for mono-material transformations that ripple through the dunnage packaging industry. German automotive hubs deploy pooled foldable large containers equipped with telematics, delivering visibility from Tier-2 stamping to final assembly. French aerospace exporters integrate shock-indicator sensors in wood-free pallets to satisfy strict insurance clauses. Energy cost inflation complicates fiber-based dunnage economics, but surging renewable capacity could moderate price pressures by 2027 if forecasts hold.

MEA and South America Dunnage Packaging Market

The Middle East and Africa, though under 5% of global revenue, illustrate rising prospects tied to pharmaceutical cold-chain corridors linking Gulf Cooperation Council states to African vaccine programs. Temperature-controlled fiber mailers introduced in 2024 position suppliers to capture value as regional biotech ecosystems mature. South America’s opportunity revolves around agritech equipment exports and the Brazilian automotive rebound, but currency volatility periodically weakens capital-intensive reusable transitions.

Competitive Landscape

Competition remains moderately fragmented, with regional converters and material specialists vying alongside diversified packaging conglomerates. Consolidation quickened in 2024-2025 as International Paper absorbed DS Smith, elevating combined sales to USD 5.9 billion in Q1 2025 and deepening integration across corrugated, molded fiber, and protective solutions. Schoeller Allibert’s union with IPL formed a USD 1.4 billion revenue player specializing in injection-molded reusable containers, granting automotive OEMs a one-stop global pool asset.

Technology differentiation intensifies. Sealed Air’s fan-folded cellular cushioning patent underpins lighter, faster dispensed padding suited to high-velocity fulfillment lines. Meta’s work on ultrahigh molecular weight polyethylene thin films hints at next-gen conductive liners for electronics that could disrupt incumbent EPP foam use. Vertically integrated resin-to-recycling models proliferate as converters hedge feedstock risks and demonstrate closed-loop credibility to brand owners.

Sustainability positioning increasingly guides RFP outcomes. Companies able to validate 36-hour temperature control in fully fiber packs, such as DS Smith’s TailorTemp®, win pharma bids even where unit cost is 12-15% higher than EPS boxes. Meanwhile, price hikes—Sonoco’s EUR 60/t increase—signal persistent margin defense tactics as energy expenses remain elevated. White-space niches include smart pallets that log shock profiles, low-carbon ESD foams, and depot-agnostic container pools that flex across industries.

In sum, suppliers that broaden material portfolios, embed automation-ready designs, and secure feedstock via recycling partnerships are best placed to capture incremental dunnage packaging market demand through 2030.

Dunnage Packaging Industry Leaders

DS Smith

Dunnage Engineering Limited

Orbis Corporation

UFP Industries Inc.

Amatech Inc.

- *Disclaimer: Major Players sorted in no particular order

Dunnage Packaging Market Companies Covered in this Report

- DS Smith ( International Paper)

- Orbis (Menasha Corp.)

- Schoeller Allibert

- UFP Industries

- Sonoco Products

- Sealed Air

- Pregis LLC

- Smurfit Westrock

- Nefab Group

- Rehrig Pacific

- Dunnage Engineering Ltd.

- Amatech Inc.

- RPP Containers

- Flexpak LLC

- Cascades Inc.

- Mondi plc

- Inteplast Group

- Placon Corp.

- Engineered Plastic Products

- MJSolpac Ltd.

Recent Industry Developments in Dunnage Packaging Market

- May 2025: International Paper reported first-quarter 2025 net sales of USD 5.9 billion, reflecting DS Smith integration and price gains.

- April 2025: UFP Industries opened its third corrugated packaging facility to meet rising demand for sustainable dunnage solutions.

- March 2025: Sonoco announced a EUR 60/t price hike for European core board and paperboard, citing OCC shortages and energy costs.

- February 2025: Sealed Air reorganized into Food and Protective segments and forecast 2025 net sales of USD 5.1-5.5 billion.

Global Dunnage Packaging Market Report Scope

Dunnage packaging refers to materials or structures used to protect goods during transportation or storage. The primary purpose of dunnage is to prevent damage, provide cushioning, and secure products in place, ensuring they remain stable and safe throughout handling, shipping, and storage. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

Dunnage packaging market is segmented by material (Corrugated Plastic, Molded Plastic, Steel, Aluminum, Corrugated Paper, Wood and Other Materials), by end-use industry (Automotive, Aerospace, Electronics, Healthcare, Food & Beverage and Other End-Use Industries) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

Segmentation Overview

| Plastic | Corrugated Plastic |

| Molded Plastic | |

| Expanded PP Foam | |

| Other Plastics | |

| Paper and Fiber-based | Corrugated Paper/Board |

| Kraft Paper | |

| Molded Pulp | |

| Other Paper and Fiber-based | |

| Metals | Steel |

| Aluminum | |

| Wood and Composite | |

| Fabric and Textile |

| Returnable / Reusable Dunnage |

| Expendable / Single-use Dunnage |

| Trays and Inserts |

| Void-Fill Materials |

| Inflatable Air-bags |

| Pallets and Separators |

| Custom Racks and Dividers |

| Other Product Type |

| Automotive and Mobility |

| Aerospace and Defense |

| Electronics and Semiconductors |

| Healthcare and Medical Devices |

| Food and Beverage |

| Industrial Machinery and Heavy Equipment |

| Retail and E-commerce Fulfilment |

| Other End-use Industry |

| Direct Sales |

| Indirect Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material | Plastic | Corrugated Plastic | |

| Molded Plastic | |||

| Expanded PP Foam | |||

| Other Plastics | |||

| Paper and Fiber-based | Corrugated Paper/Board | ||

| Kraft Paper | |||

| Molded Pulp | |||

| Other Paper and Fiber-based | |||

| Metals | Steel | ||

| Aluminum | |||

| Wood and Composite | |||

| Fabric and Textile | |||

| By Packaging Format | Returnable / Reusable Dunnage | ||

| Expendable / Single-use Dunnage | |||

| By Product Type | Trays and Inserts | ||

| Void-Fill Materials | |||

| Inflatable Air-bags | |||

| Pallets and Separators | |||

| Custom Racks and Dividers | |||

| Other Product Type | |||

| By End-use Industry | Automotive and Mobility | ||

| Aerospace and Defense | |||

| Electronics and Semiconductors | |||

| Healthcare and Medical Devices | |||

| Food and Beverage | |||

| Industrial Machinery and Heavy Equipment | |||

| Retail and E-commerce Fulfilment | |||

| Other End-use Industry | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the dunnage packaging market?

The market is valued at USD 4.52 billion in 2026 and is forecast to reach USD 5.69 billion by 2031.

Which region leads the dunnage packaging market growth?

Asia-Pacific holds 38.10% share and is advancing at an 7.98% CAGR through 2031, driven by Chinese and Indian manufacturing expansion.

Why are reusable dunnage solutions gaining traction?

Reusable formats lower total cost per trip, comply with circular-economy mandates, and now command 57.93% of the dunnage packaging market size.

Which end-use sector is growing fastest in dunnage demand?

Electronics and semiconductors are expanding at an 7.88% CAGR because miniaturized components need precision, ESD-safe packaging.

How do EU recycled-content rules affect dunnage packaging?

The PPWR requires transport packaging to be recyclable and include specific recycled content, prompting rapid innovation in mono-material designs.

What are the main restraints on dunnage packaging market growth?

Raw material price volatility and limited recycling pathways for multi-material composites are currently the strongest growth headwinds.

Page last updated on: