Biological Safety Cabinet Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

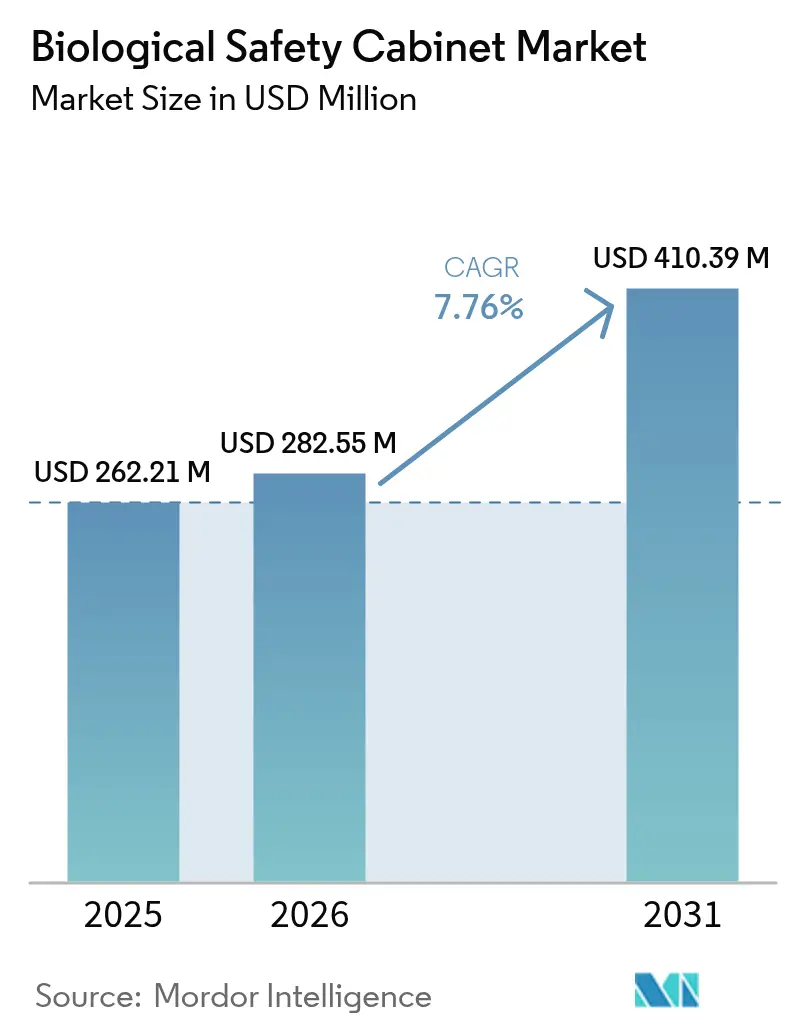

| Market Size (2026) | USD 282.55 Million |

| Market Size (2031) | USD 410.39 Million |

| Growth Rate (2026 - 2031) | 7.76% CAGR |

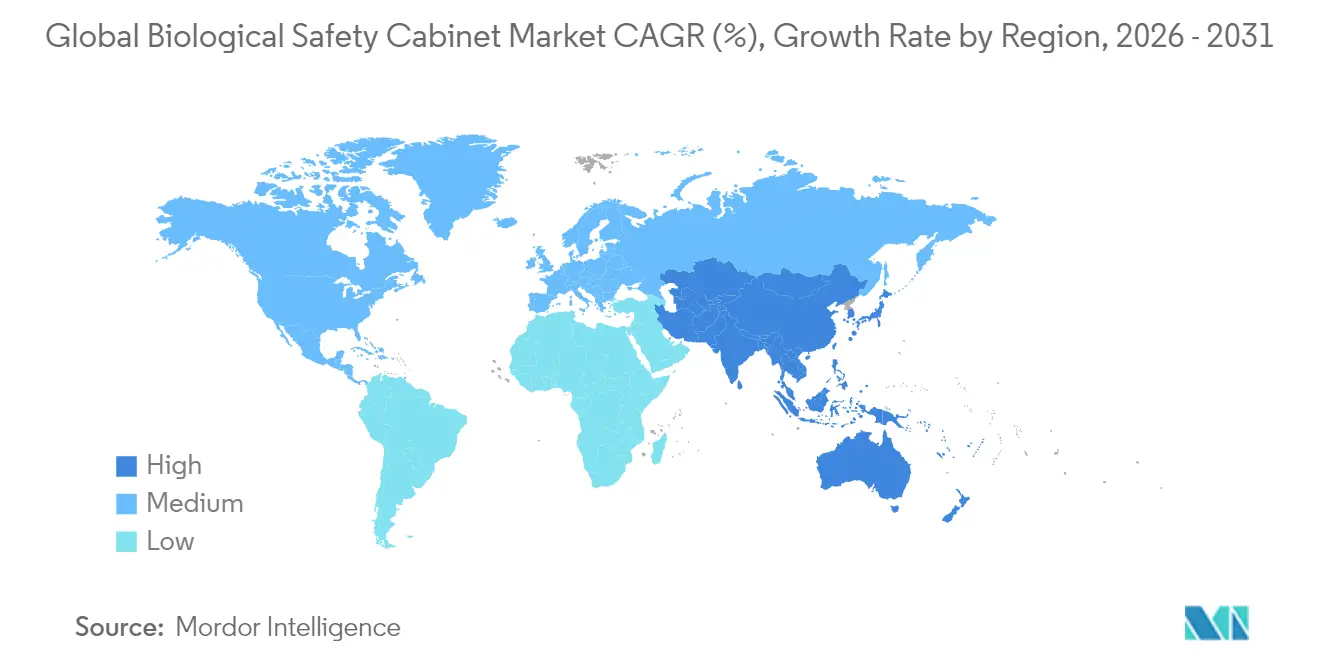

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

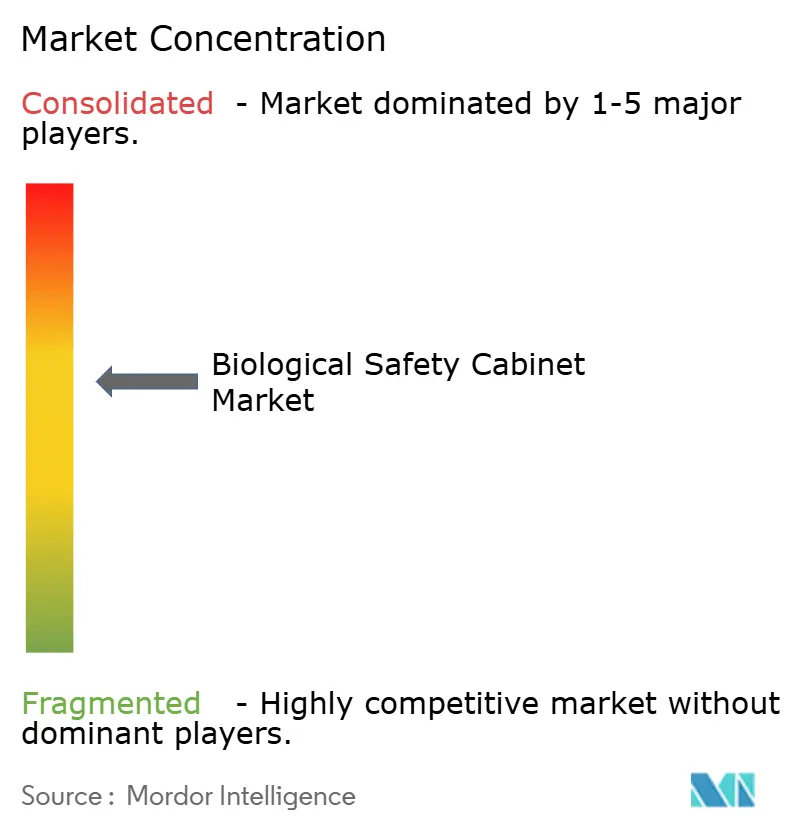

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biological Safety Cabinet Market Analysis by Mordor Intelligence

The biological safety cabinets market size was valued at USD 262.21 million in 2025 and estimated to grow from USD 282.55 million in 2026 to reach USD 410.39 million by 2031, at a CAGR of 7.76% during the forecast period (2026-2031). This expansion stems from record capital spending on cell and gene therapy infrastructure, large-scale aseptic manufacturing projects, and steady adoption of higher-containment technologies. Investment announcements such as Novo Nordisk’s USD 4.1 billion fill-finish campus and Thermo Fisher Scientific’s USD 2 billion U.S. capacity upgrade signal sustained equipment demand. Contract development and manufacturing organizations (CDMOs) now capture a growing share of cabinet purchases as outsourcing accelerates, while energy-efficient ductless designs win favor in retrofit laboratories. Regulatory convergence around ISO 14644-4 and the EU Machinery Regulation is eliminating regional specification gaps and rewarding suppliers with global compliance expertise. Asia-Pacific is set to overtake Europe in new installations as pharmaceutical supply chains rebalance away from China toward India and Southeast Asia.

Key Report Takeaways

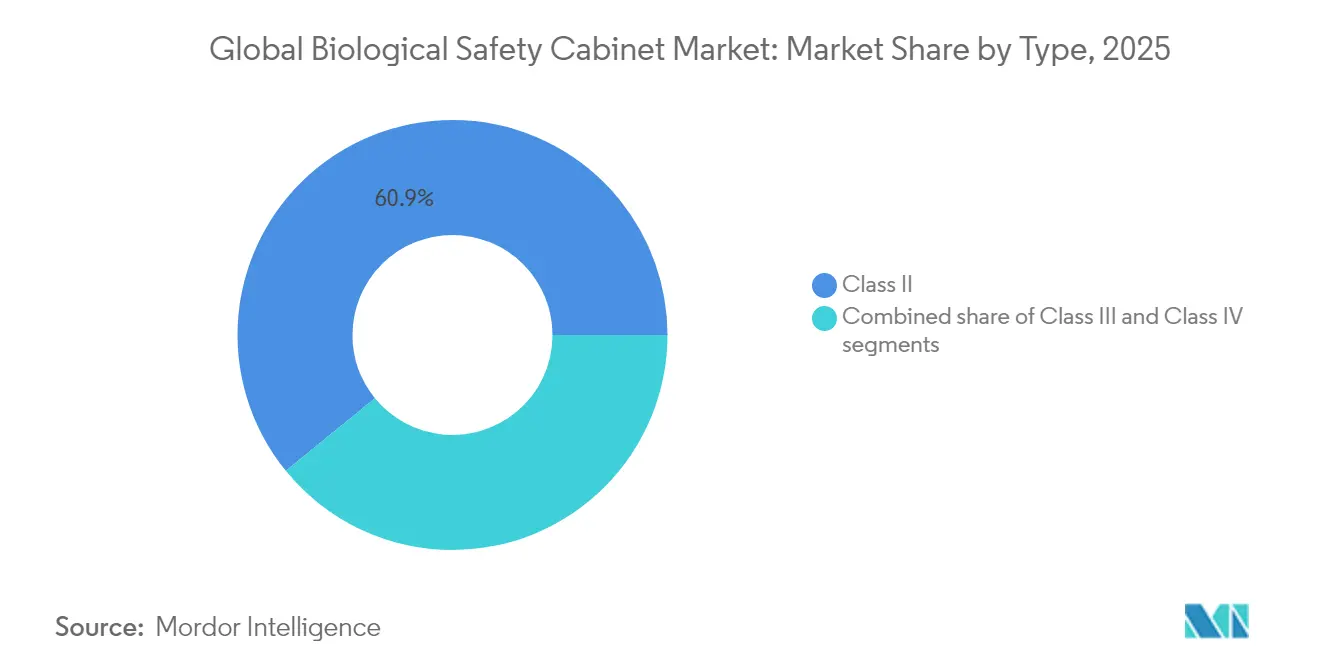

- By type, Class II equipment accounted for 60.88% share of the biological safety cabinets market size in 2025, whereas Class III systems are expanding at a 10.01% CAGR.

- By exhaust system, ducted models commanded 57.92% share of the biological safety cabinets market size in 2025, while ductless solutions are rising at a 10.28% CAGR.

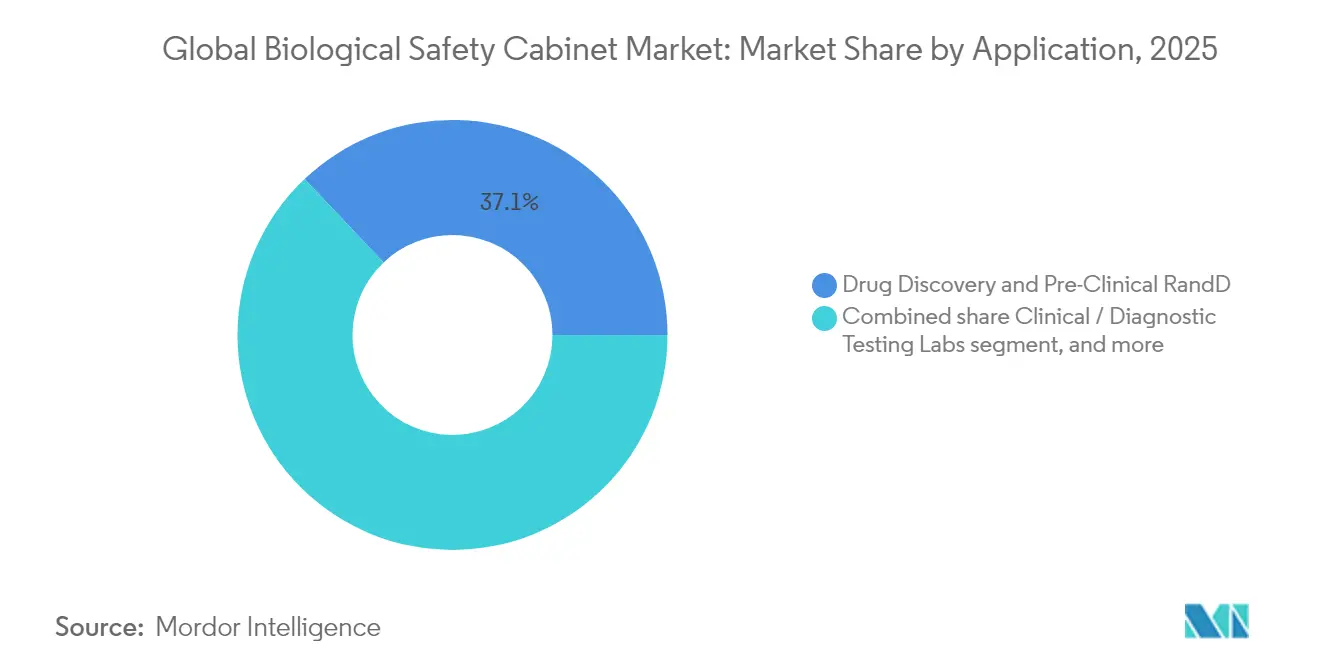

- By application, drug discovery and pre-clinical R&D held 37.08% of the biological safety cabinets market share in 2025; biopharmaceutical manufacturing and fill-finish is growing fastest at an 10.92% CAGR.

- By end-user, pharmaceutical and biotechnology companies held 48.02% of the biological safety cabinets market share in 2025, while CDMOs record the fastest growth at an 11.33% CAGR through 2031.

- By geography, North America led with 41.98% revenue share in 2025; Asia-Pacific is projected to advance at a 9.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biological Safety Cabinet Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding pharmaceutical and biotechnology research expenditure | +2.1% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Escalating global preparedness for emerging infectious diseases | +1.8% | Global, priority in Asia-Pacific & North America | Short term (≤2 years) |

| Stringent occupational health and safety regulations | +1.5% | North America & EU core, expanding to Asia-Pacific | Long term (≥4 years) |

| Accelerating cell and gene therapy manufacturing expansion | +2.3% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Rising adoption of smart energy-efficient cabinet technologies | +0.8% | Global, led by North America & Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expanding Pharmaceutical and Biotechnology Research Expenditure

Robust drug-development pipelines are prompting large companies to build redundant research hubs that need new containment suites. Thermo Fisher Scientific is allocating USD 1.5 billion of its four-year U.S. investment program to laboratory infrastructure that includes biological safety cabinets. Mergers that add late-stage assets further boost facility retrofits, and AI-enabled discovery platforms are re-configuring workspaces for automated, high-throughput assays that still require operator protection. As a result, the biological safety cabinets market gains additional pull-through from every newly equipped research laboratory. Universities benefit from expanded grant funding that covers biosafety upgrades, supporting steady public-sector demand. The trend is most visible in North America, but similar capacity builds are underway in Western Europe.

Escalating Global Preparedness for Emerging Infectious Diseases

Governments have prioritized resilient laboratory networks since 2024. The CDC’s sixth edition of the Biosafety in Microbiological and Biomedical Laboratories outlines tighter performance criteria for airflow and filter integrity, prompting cabinet replacement cycles. OSHA’s forthcoming infectious-disease rule will extend similar requirements to clinical laboratories, accelerating domestic orders[1]U.S. Department of Health & Human Services, “OSHA Infectious Disease Rulemaking Update,” hhs.gov. Defense programs that study bioaerosol threats also rely on HEPA-filtered workstations, underlining cross-sector demand. National stockpiles of rapid-response testing infrastructure now routinely include biosafety cabinets, ensuring immediate deployment during outbreaks. This focus on readiness sustains short-term growth, particularly in Asia-Pacific where public-health laboratories are scaling up.

Stringent Occupational Health and Safety Regulations

The FDA’s adoption of ISO 14644-4 for cleanroom construction sets new benchmarks for air-change efficiency and maintenance documentation, affecting cabinet selection after December 2026. The EU Machinery Regulation 2023/1230 adds mandatory conformity assessments that standardize performance claims across member states[2]European Parliament and Council, “Machinery Regulation 2023/1230,” eur-lex.europa.eu. OSHA’s revised Hazard Communication Standard elevates labeling and ventilation expectations for laboratories. Europe’s updated GMP Annex 1 stipulates 0.45 m/s unidirectional airflow, pressuring manufacturers to refine cabinet design[3]International Society for Pharmaceutical Engineering, “Impact of EU GMP Annex 1 on Airflow,” ispe.org. Global harmonization reduces regional model variants and favors suppliers with multi-jurisdiction certifications, thereby shaping procurement decisions within the biological safety cabinets market.

Accelerating Cell and Gene Therapy Manufacturing Expansion

Major biomanufacturing projects are reshaping the production footprint of advanced therapies. Fujifilm is investing USD 1.2 billion to add eight 20,000-liter bioreactors in North Carolina, each requiring multiple Class II and III workstations for seed train and fill-finish steps. Lonza’s agreement to make Vertex’s CRISPR-edited therapy uses dedicated containment suites in Portsmouth and the Netherlands, illustrating specialized cabinet requirements. GenScript’s 128,000-square-foot New Jersey site expands plasmid DNA output and relies on modular cabinets with automated decontamination. Canadian federal support for STEMCELL Technologies’ new plant demonstrates public-sector backing for advanced bioprocessing that includes biosafety investments. Each project translates directly into demand for high-containment, rapid-cycle equipment.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and certification costs | -1.2% | Global, particularly affecting smaller laboratories | Short term (≤2 years) |

| Emergence of alternative closed isolator systems | -0.8% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Supply chain vulnerabilities in HEPA / ULPA filtration components | -0.6% | Global, with acute impact in Asia-Pacific | Short term (≤2 years) |

| Intensifying energy-efficiency compliance pressure | -0.4% | EU core, expanding to North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital and Certification Costs

Total installed cost often doubles list price once validation, construction modifications, and GMP documentation are added. Academic laboratories struggle to fund upgrades because research grants rarely cover infrastructure. Uncertainty over future certification rules tied to ISO 14644-4 has prompted some buyers to postpone orders. Smaller biotech firms mitigate expense by leasing shared lab space, which delays direct equipment sales. Custom validation for potent-compound handling pushes expenses higher, particularly for first-time CDMOs.

Emergence of Alternative Closed Isolator Systems

Isolators deliver higher sterility assurance levels for cytotoxic or HPAPI production. Telstar’s Pura system achieves log-6 microbial reductions while reducing cleanroom classification needs. Restricted Access Barrier Systems lower HVAC loads yet offer limited operator protection for very toxic materials. Pharmaceutical contamination-control guidelines increasingly recommend isolators for cell therapy lines. Curis System’s rapid vaporized-hydrogen-peroxide decontamination unit completes validated cycles in under one hour, illustrating technical advantages. As isolators proliferate, the biological safety cabinets market faces substitution risk, especially in fill-finish suites.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Class III Systems Lead Innovation

Class II units retained 60.88% of the biological safety cabinets market share in 2025 because they meet the majority of routine research and diagnostic needs. However, Class III glove-box designs are on a 10.01% CAGR trajectory thanks to rising HPAPI and viral-vector handling requirements. Esco’s leak-tight Class III series supports chemotherapy compounding and vaccine formulation while ensuring zero operator exposure. The biological safety cabinets market size for Class III units is projected to grow rapidly as CRISPR and oncolytic-virus pipelines expand. Across all classes, manufacturers embed touch-screen airflow analytics and automatic pressure-decay tests that simplify annual recertification. Energy-optimization remains a cross-class design focus to satisfy ISO-driven lifecycle cost mandates.

Technological parity is narrowing, yet Class I equipment remains niche, serving teaching labs that require personnel and environmental protection without the product shielding offered by higher classes. Software integrations now push usage data to building-management systems, enabling laboratory managers to demonstrate ventilation compliance in real time. Global harmonization of airflow velocity targets is expected to drive retrofits, sustaining demand for all classes within the biological safety cabinets market.

By Exhaust System: Ductless Solutions Gain Momentum

Ducted configurations captured 57.92% of revenue in 2025 due to regulatory preference in GMP suites. They remain indispensable where direct hazardous-air removal is mandated, especially in large biopharmaceutical campuses. Even so, ductless units are advancing at a 10.28% CAGR because they avoid costly HVAC rework in space-constrained buildings. The biological safety cabinets market size for ductless models will accelerate in emerging economies where laboratory retrofits exceed new-build projects. Better Basics Laborbedarf’s SmartIntegrate module boosts workstation efficiency by 30% and allows tool-free filter swaps, illustrating innovation in this segment.

Energy codes pushing toward net-zero buildings give ductless units an advantage by minimizing conditioned-air losses. Suppliers now offer hybrid models that allow future conversion between ducted and recirculating modes, protecting customer capital as regulations evolve. Despite these gains, high-risk HPAPI suites still specify hard-ducted exhaust to guarantee negative pressure, so both systems will coexist in the biological safety cabinets market.

By Application: Manufacturing Applications Accelerate

Drug discovery and pre-clinical R&D accounted for 37.08% of 2025 revenue, yet the manufacturing and fill-finish segment is growing faster at 10.92% CAGR. Capacity expansions for monoclonal antibodies and mRNA vaccines require multiple high-throughput biosafety lines within a single plant, elevating demand. Monmouth Scientific’s Class II units support organoid production in Molecular Devices’ facility, indicating how specialized therapeutic platforms influence cabinet choice. The biological safety cabinets market size for manufacturing applications is projected to outstrip R&D spending as late-stage pipelines mature. Automation and robotics inside fill-finish suites are increasing cabinet footprint per line because each robotic enclosure still demands HEPA filtration and validated airflow integrity.

Clinical and diagnostic labs remain a stable buyer group, benefiting from syndicated testing programs and new molecular-assay launches. Growth in biosafety testing, projected to reach USD 15.07 billion by 2034, supplies a steady replacement cycle for cabinets handling endotoxin, sterility, and mycoplasma assays. Academic institutes continue to upgrade to energy-smart units, partly funded by government infrastructure grants.

By End-User: CDMOs Drive Market Evolution

Pharmaceutical and biotechnology companies held the largest 2025 share at 48.02%, but CDMOs are expanding faster at 11.33% CAGR. Fujifilm’s mammalian-cell expansion and Lonza’s CRISPR deal illustrate the rapid scaling that outsourcers undertake on behalf of sponsors. The biologics CDMO sector is forecast to quadruple its revenue by 2034, translating into sustained cabinet procurement. The biological safety cabinets market benefits as each greenfield CDMO campus installs dozens of units across seed train, media prep, and QC labs.

Academic and research centers occupy a third tier of demand, aided by public funding aimed at pandemic preparedness. Meanwhile, small biotech firms increasingly rely on shared lab incubators that centralize Class II workstations, indirectly boosting utilization rates and service revenues within the biological safety cabinets industry.

Geography Analysis

North America led the biological safety cabinets market at 41.98% revenue share in 2025. Large-scale projects such as Novo Nordisk’s 1.4-million-square-foot aseptic facility and Thermo Fisher Scientific’s multiyear capital program underscore sustained equipment pull. FDA adoption of ISO 14644-4 plus OSHA’s forthcoming infectious-disease rule create back-to-back compliance cycles that compel cabinet upgrades. Federal incentives for reshoring pharmaceutical supply chains also channel investment into U.S. CDMO campuses that specify high-containment designs.

Asia-Pacific is the fastest-growing region at a 9.22% CAGR through 2031. The US Biosecure Act is redirecting outsourcing toward India, where the CDMO market will climb from USD 15.63 billion in 2023 to USD 26.73 billion by 2028. Singapore’s USD 150 million Pall Corporation filtration plant demonstrates the region’s evolving ecosystem that integrates upstream consumables with cabinet manufacturing. China’s ongoing pharmaceutical build-out and Japan’s vaccine self-sufficiency plans further elevate demand. Harmonized standards simplify imports, encouraging multinational suppliers to locate final assembly closer to customers.

Europe shows steady expansion anchored by strict regulatory mandates and green-building directives. The Machinery Regulation and Ecodesign rules push laboratories to adopt energy-efficient units with digital passports. Rentschler Biopharma’s buffer-media complex and other biologics investments bolster replacement demand for high-performance cabinets. The region’s active-pharmaceutical-ingredient market growth supports modern GMP suites, lifting the biological safety cabinets market. Sustainability targets that require net-zero emissions by 2050 are tilting procurement toward ductless or low-pressure designs, reinforcing technology differentiation among suppliers.

Competitive Landscape

The biological safety cabinets market features a moderately concentrated vendor pool where innovation and compliance scope define leadership. Thermo Fisher Scientific deepened vertical integration by agreeing to acquire Solventum’s filtration unit for USD 4.1 billion, adding critical upstream capability in HEPA media and purification hardware. Kewaunee Scientific’s January 2025 alliance with NuAire merges furniture and containment portfolios, delivering turnkey laboratory packages that simplify procurement. These moves reflect a trend toward bundled offerings that include cabinets, casework, and facility monitoring software.

Suppliers differentiate through IoT analytics, automated decontamination, and ergonomic advances. The new Herasafe 2025 platform offers adaptive airflow control and voice prompts that guide safe work practice. Esco, NuAire, and Baker adopt similar digital dashboards that feed data to quality-management systems. Global certification breadth is another competitive lever as ISO, GMP Annex 1, and Machinery Regulation frameworks converge. Companies capable of rapid multi-jurisdiction validation gain share, especially among CDMOs with cross-border operations.

Smaller regional firms carve out niches in custom isolator retrofits or aftermarket service. They partner with HEPA cartridge specialists to secure supply, insulating customers from the filtration shortages seen in 2024. Overall, price competition remains balanced by high switching costs and the critical-safety function cabinets perform, keeping margins stable for top-tier producers inside the biological safety cabinets industry.

Biological Safety Cabinet Industry Leaders

Esco Micro

Labconco

The Baker Company

Kewaunee Scientific

Thermo Fisher Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’sPurification & Filtration business for USD 4.1 billion to strengthen bioproduction offerings.

- January 2025: Kewaunee Scientific and NuAire formed a strategic partnership to combine laboratory furniture and biosafety cabinet portfolios for global customers.

- January 2025: Thermo Fisher Scientific launched the Herasafe 2025 Biological Safety Cabinet featuring adaptive airflow control and improved ergonomics.

- January 2025: Thermo Fisher Scientific committed USD 2 billion over four years to expand U.S. manufacturing and R&D capacity, including laboratory infrastructure.

- June 2024: Novo Nordisk unveiled a USD 4.1 billion fill-finish facility in Clayton, North Carolina, with 1,000 new jobs and LEED Gold design targets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the biological safety cabinet market as the sale of newly manufactured, enclosed laboratory workstations with HEPA-filtered, directional airflow that protect operators, samples, and the environment while handling bio-hazardous material at biosafety levels one through three. Units covered include Class I, Class II, and Class III cabinets that conform to NSF/ANSI 49 or equivalent standards.

Scope Exclusions: Laminar flow clean benches, powder containment hoods, and refurbished or rental units are not included.

Segmentation Overview

- By Type

- Class I

- Class II

- Class III

- By Exhaust System

- Ducted (Hard-Connected)

- Recirculating / Ductless

- By Application

- Drug Discovery & Pre-Clinical R&D

- Clinical / Diagnostic Testing Labs

- Biopharmaceutical Manufacturing & Fill-Finish

- By End-User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research / CDMOs

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts interviewed safety officers in pharmaceutical plants, procurement leads at contract research organizations, certification engineers, and regional distributors across North America, Europe, and Asia Pacific. In these discussions, we clarified purchase criteria, average selling prices, and cabinet replacement cycles, filling gaps the desk work left open.

Desk Research

We began with tier-one public sources such as United States CDC laboratory capacity updates, European ECDC surveillance bulletins, OECD Science and Technology Indicators, UN Comtrade shipment records, and peer-reviewed biosafety studies on PubMed. Company filings accessed via D&B Hoovers, news archives from Dow Jones Factiva, and import volumes verified through Volza added commercial color.

These references illustrate, and do not exhaust, the wider pool of government, academic, and industry releases that informed the dataset.

Market-Sizing & Forecasting

A top-down model that rebuilds the global installed base from production and trade data is paired once with selective bottom-up supplier revenue roll-ups to sense-check totals and adjust for captive manufacturing. Key variables include announced cell and gene therapy facility investments, annual NSF/ANSI 49 revision adoption rates, pharmaceutical R&D spending, new BSL-3 lab construction permits, average selling price by cabinet class, and typical ten-year replacement intervals. Multivariate regression links these drivers to demand, while scenario analysis supplies low and high cases. Gaps in granular volumes are bridged through expert-validated utilization ratios.

Data Validation & Update Cycle

Cross checks compare model outputs with independent shipment signals, and certification backlogs and anomalies trigger senior review. Our report refreshes yearly, with interim revisions when material plant expansions, regulatory changes, or currency swings occur, ensuring clients receive the latest view.

Why Mordor's Biological Safety Cabinet Baseline Inspires Confidence

Published estimates often differ because each firm selects its own mix of products, regions, exchange rates, and refresh cadence.

Some studies merge clean benches with safety cabinets, others skip emerging markets, and a few freeze currency at survey-year averages that distort values when rates move sharply. Mordor chooses clear scope boundaries, updates exchange rates quarterly, and revisits assumptions whenever large manufacturing projects are announced, keeping our 2025 figure balanced.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 262.21 million (2025) | Mordor Intelligence | None |

| USD 226.79 million (2024) | Global Consultancy A | Omits 11 high-growth countries and service revenue streams |

| USD 240.78 million (2024) | Trade Journal B | Applies flat average selling price across all cabinet classes |

| USD 255.00 million (2024) | Industry Observatory C | Combines laminar flow benches with biosafety cabinets |

The comparison shows that, while other publishers offer useful snapshots, Mordor's disciplined scope selection, timely currency conversion, and mixed-method modeling deliver a dependable, decision-ready baseline for stakeholders.

Key Questions Answered in the Report

What is the current valuation of the biological safety cabinets market?

The market is valued at USD 282.55 million in 2026 and is projected to reach USD 410.39 million by 2031.

Which region leads the biological safety cabinets market?

North America leads with 41.98% revenue share, supported by major biopharmaceutical investments and rigorous regulatory standards.

Why are CDMOs important to future cabinet demand?

CDMOs are expanding at an 11.33% CAGR as drug sponsors outsource complex manufacturing, driving continuous installation of new containment suites.

How are regulations influencing cabinet design?

Adoption of ISO 14644-4, the EU Machinery Regulation, and revised GMP Annex 1 is pushing suppliers to deliver energy-efficient, globally certified models.

What technological trends are shaping new cabinet models?

IoT-enabled airflow monitoring, predictive maintenance, and low-pressure HEPA systems are reducing energy costs while improving safety and compliance.

Are ductless cabinets replacing ducted systems?

Ductless cabinets are growing faster due to retrofit flexibility, yet ducted units remain indispensable for high-risk GMP operations that require direct exhaust.

Page last updated on: