Robotics and ADAS Vehicles Sensor Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

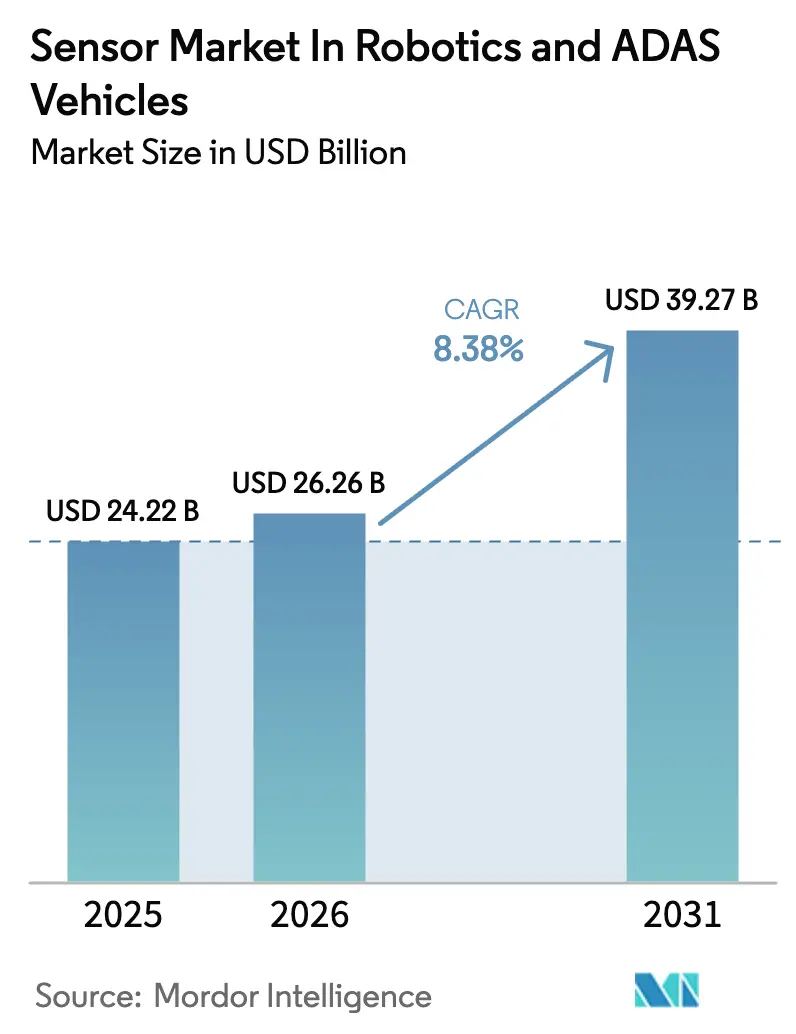

| Market Size (2026) | USD 26.26 Billion |

| Market Size (2031) | USD 39.27 Billion |

| Growth Rate (2026 - 2031) | 8.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotics and ADAS Vehicles Sensor Market Analysis by Mordor Intelligence

The Robotics and ADAS Vehicles Sensor Market was valued at USD 24.22 billion in 2025 and is estimated to grow from USD 26.26 billion in 2026 to reach USD 39.27 billion by 2031, at a CAGR of 8.38% during the forecast period (2026-2031). Rising integration of cameras, radar, LiDAR, and inertial sensors in both autonomous robots and passenger-car ADAS stacks is elevating hardware content per platform while shortening design cycles as OEMs migrate toward centralized, software-defined architectures. A regulatory pivot that positions perception hardware as the gating item for functional-safety compliance is tightening the link between sensor capability and vehicle homologation timelines. Edge-AI compute advances are enabling real-time fusion of multi-modal data, which in turn spurs demand for higher-resolution imagers and 4D imaging radar. Suppliers with in-house semiconductor capacity - particularly in China and the European Union - are achieving cost and supply-chain resilience advantages that translate into faster design wins and higher gross margins.

Key Report Takeaways

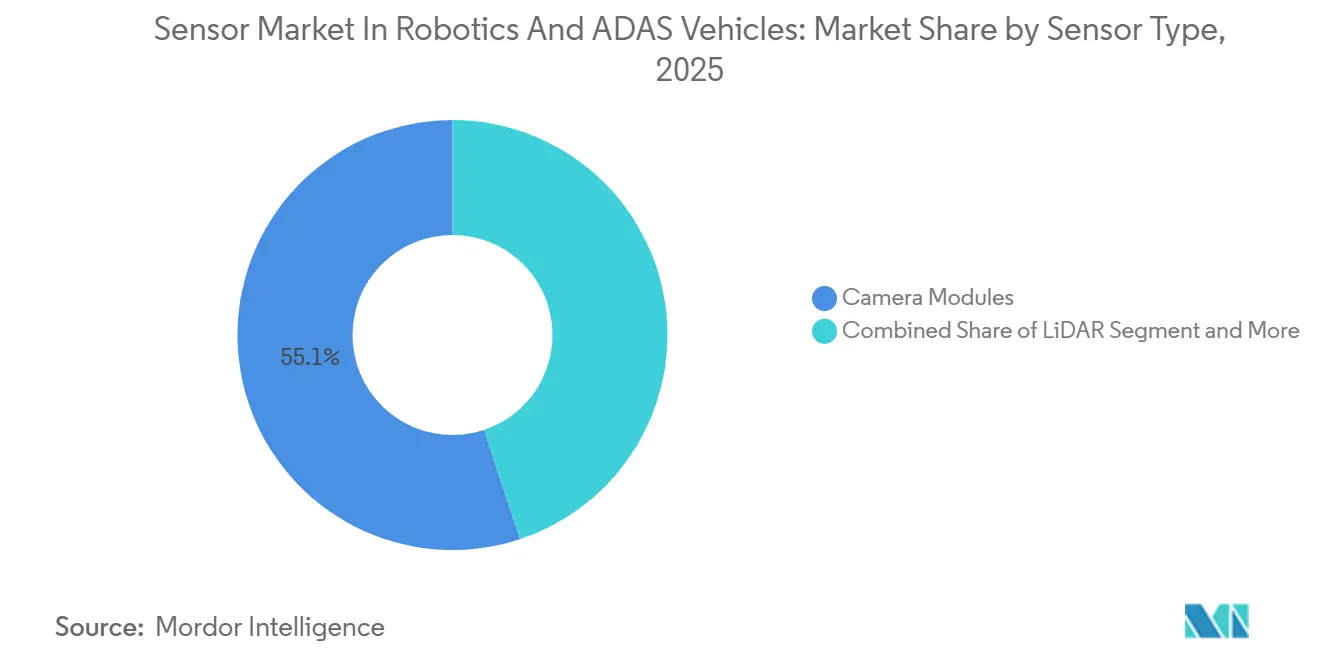

- By sensor type, camera modules commanded 55.13% of the Robotics and ADAS Vehicles Sensor Market share in 2025, while LiDAR is advancing at a 10.62% CAGR through 2031.

- By vehicle/automation level, ADAS L1-L2 platforms captured 57.25% share in 2025, while highly automated L4-L5 platforms are projected to record the fastest CAGR of 9.81%, underscoring the sensor intensity of robotaxis and autonomous trucks.

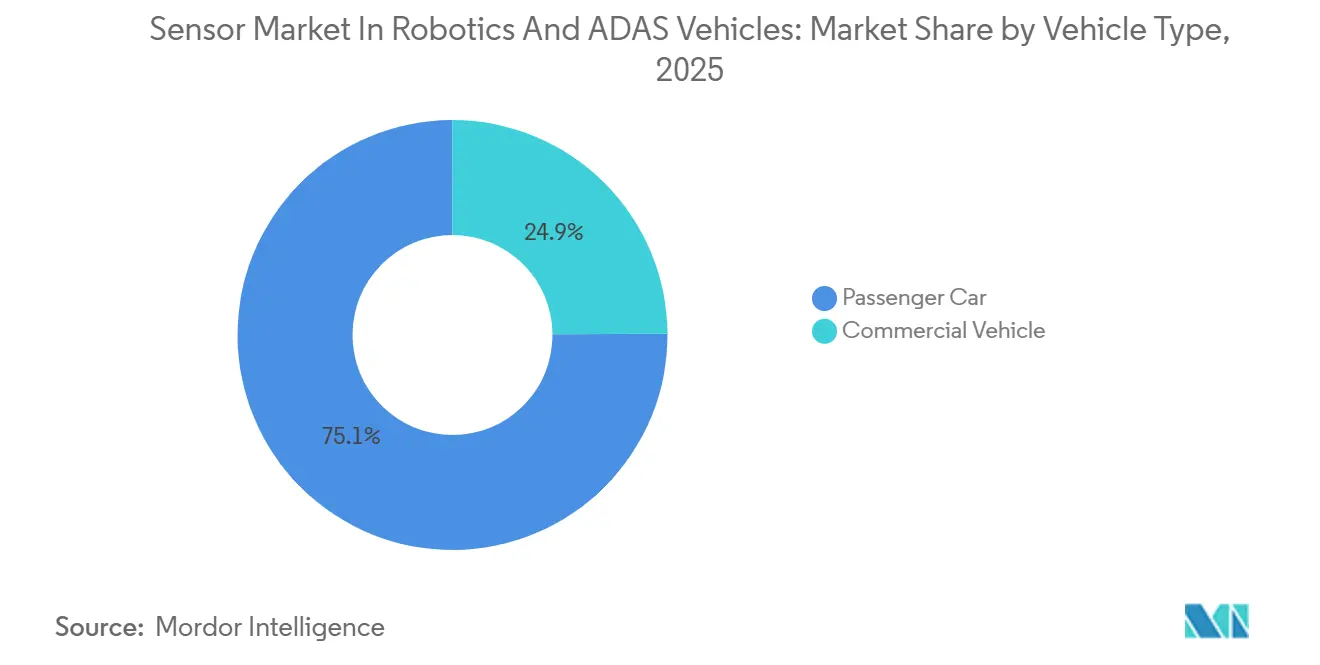

- By vehicle type, passenger cars captured 75.10% of the Robotics and ADAS Vehicles Sensor Market in 2025, while commercial vehicles are on track for an 8.91% CAGR through 2031.

- By propulsion type, internal combustion engine vehicles controlled 79.12% share in 2025, while electric vehicles are forecast to grow with a 10.21% CAGR through 2031.

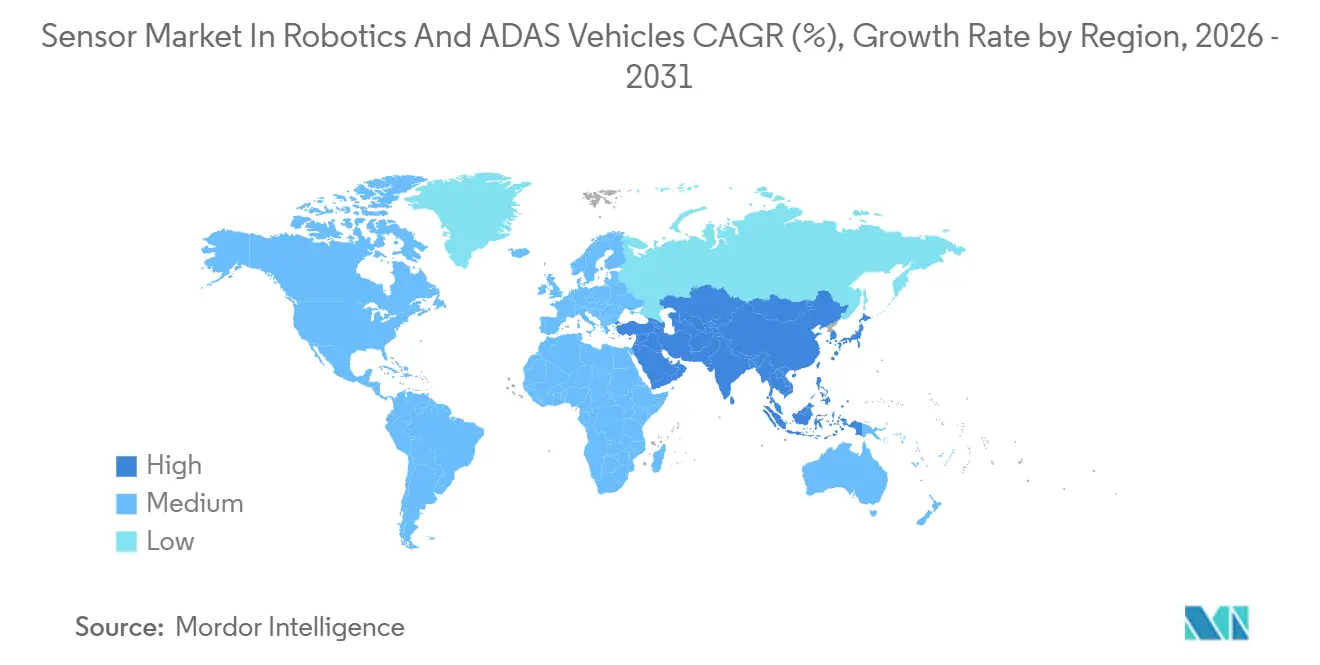

- By geography, Asia-Pacific held 36.12% of the Robotics and ADAS Vehicles Sensor Market share in 2025, and will expand at a 9.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Robotics and ADAS Vehicles Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for ADAS Features | +2.1% | Global, led by North America, Europe, and the Asia-Pacific | Short term (≤ 2 years) |

| Awareness of Road and Worker Safety | +1.8% | Global, Europe, and China are leading | Medium term (2-4 years) |

| Sensor Fusion and Software-Defined Perception | +1.5% | Global, early adoption in premium segments | Medium term (2-4 years) |

| Falling Costs in Cameras, Radar, and IMUs | +1.4% | Global, China is driving cost leadership | Short term (≤ 2 years) |

| Expansion of Service Robotics | +1.2% | North America, Asia-Pacific spillover to Europe | Long term (≥ 4 years) |

| Smart City and Intelligent Transport Initiatives | +0.9% | Asia-Pacific core, North America pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for ADAS Features in Passenger and Commercial Vehicles

Feature democratization is decoupling ADAS from luxury positioning. Volkswagen embedded Travel Assist as standard on the 2026-model ID.7, employing a radar-camera-ultrasonic trio that lowers lane-centering activation thresholds to 18 mph, thereby broadening urban-use applicability. Ford’s Pro Intelligence suite integrates 360-degree cameras and corner radar into the F-150 Lightning base trim, aligning fleet total-cost-of-ownership calculators with safety-driven insurance discounts. Penetration at Level 1-Level 2 reached a notable share of global vehicle builds in 2025; however, Level 2+ subscriptions are converting at higher attach rates because over-the-air feature unlocks monetize dormant hardware. This behavioral inflection is reinforcing upfront sensor fitment even where software activation is deferred, sustaining annual volume growth for the Robotics and ADAS Vehicles Sensor Market.

Rising Awareness of Road and Worker Safety and Stringent Regulations

Euro NCAP’s 2025 protocols made pedestrian and cyclist detection mandatory for a five-star rating, prompting Tier-1 suppliers to migrate from 1.2-megapixel to 8-megapixel imagers that double data throughput yet satisfy low-light detection thresholds[1]“2025 Protocols,” Euro NCAP, euroncap.com. NHTSA’s January 2025 Standing General Order obliges OEMs to log and report Level 2 ADAS crashes, turning sensor reliability into an actuarial risk variable that insurers now price in. China’s upgraded GB 7258-2017 standard requires forward-collision and lane-departure warning on heavy trucks, creating baseline demand for radar and camera modules in freight fleets. Industrial regulators are mirroring these moves; OSHA’s 2025 guideline update for collaborative robots mandates LiDAR-based workspace safeguarding in warehousing, aligning worker-safety policy with automotive norms. Collectively, these rules transform safety from a discretionary feature to a procurement trigger, directly expanding the Robotics and ADAS Vehicles Sensor Market.

Shift Toward Sensor Fusion and Software-Defined Perception Stacks

Real-time edge inference is moving fusion complexity off the cloud and into vehicle ECUs. NVIDIA’s DRIVE Orin delivers 254 TOPS, fusing up to 26 heterogeneous sensor streams within a few milliseconds for Level 4 perception [2]“DRIVE Orin Product Brief,” Nvidia Corporation, nvidia.com. Qualcomm’s Snapdragon Ride Flex scales compute from 10 TOPS to 60 TOPS on a shared board, allowing OEMs to homogenize hardware across trims and gate features in software. Mobileye’s EyeQ Ultra processes 176 TOPS and ships with a middleware layer that allows camera-only, camera-plus-radar, and camera-plus-LiDAR profiles to coexist, enabling regional tailoring without board redesign. The ability to mix sensors modularly reduces BOM volatility, incentivizing automakers to pre-install higher-end imagers and radars that can be monetized later, thus reinforcing volume growth in the Robotics and ADAS Vehicles Sensor Market.

Falling Unit Costs in Cameras, Radar, IMUs, and Gradual LiDAR Cost Decline

ON Semiconductor has reduced the die size on its 8-megapixel Hyperlux LP imagers, significantly lowering unit prices in 2025 compared to the previous generation. Infineon's integrated 77/79 GHz radar transceiver has made radar modules more affordable, enabling their inclusion in entry-level compact vehicles and motorcycles. Solid-state LiDARs from Hesai and RoboSense have become more cost-effective, while mechanical units remain priced higher, maintaining a performance stratification aligned with sensor-redundancy tiers. As commodity prices approach marginal costs, suppliers are shifting their focus to value-added software, ensuring profitability while simultaneously increasing unit shipments in the sensor market for robotics and ADAS vehicles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced LiDAR and Imaging Sensor Costs | -1.3% | Global, acute in India and Southeast Asia | Medium term (2-4 years) |

| Compute, Software, and Data-Handling | -1.1% | Global, steeper in talent-scarce regions | Long term (≥ 4 years) |

| Regulatory and Liability Uncertainty | -0.8% | North America and Europe | Medium term (2-4 years) |

| Semiconductor Supply-Chain Volatility | -0.7% | Global, analog and power bottlenecks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced LiDAR and Imaging Sensor Suites

Volvo's EX90 features Luminar's Iris LiDAR, highlighting its premium positioning in a high-end vehicle segment [3]“Iris Cost Structure,” Luminar Technologies, luminartech.com. Meanwhile, BMW's iX incorporates InnovizTwo, which confines its use to luxury trims despite a significant cost reduction from its predecessor, InnovizOne. However, original equipment manufacturers (OEMs) exhibit hesitation, leading to sluggish volume commitments. This, in turn, stifles cost-learning curves, creating a chicken-and-egg dilemma. While imaging radar presents a partial alternative, it falls short of LiDAR's point-cloud density, especially in bustling urban environments. This performance disparity remains unaddressed for mid-priced vehicles. Unless unit costs decrease significantly, widespread adoption will remain elusive, consequently tempering the growth rate for sensors in robotics and Advanced Driver-Assistance Systems (ADAS) vehicles.

Compute, Software, and Data-Handling Complexity

Every hour of operation, a Level 3 car produces an immense amount of sensor data. This data deluge compels original equipment manufacturers (OEMs) to embed advanced edge processors. Additionally, these manufacturers are channeling investments into sophisticated thermal management systems. While Tesla capitalizes on its extensive fleet data reservoir to refine its camera-centric networks, emerging players find it a daunting challenge to match that magnitude in a short span. This engineering challenge not only escalates R&D expenditures but also extends validation timelines. Consequently, these delays hinder vehicle program rollouts and temper the growth trajectory of the sensor market, particularly in robotics and Advanced Driver-Assistance Systems (ADAS) vehicles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: LiDAR Gains Despite Camera Dominance

Camera modules delivered 55.13% of the Robotics and ADAS Vehicles Sensor Market share in 2025, buoyed by regulatory mandates for forward-facing vision systems. Valeo’s SCALA 3 LiDAR entered production on Stellantis and Renault models at a sub-USD 600 price, a pivotal step toward volume broadening. Imaging radar evolves in parallel; Continental’s ARS540 detects at 300 meters with elevation classification, giving OEMs flexibility to reduce LiDAR count while preserving function. Ultrasonic sensors remain in commercial vehicles for close-range tasks despite Tesla’s 2024 vision-only pivot. Bosch’s sixth-generation units integrate on-chip signal processing that halves wiring harness weight, keeping them relevant for low-speed maneuvering. Absent a step-change in LiDAR cost, cameras will keep numerical dominance, yet LiDAR’s 10.62% CAGR signals accelerative uptake where redundancy is non-negotiable, sustaining multi-modal architectures across the Robotics and ADAS Vehicles Sensor Market.

Cameras benefit from economies of scale and silicon-node migration, but they confront physics limits in poor lighting and adverse weather. Radar excels under such conditions but historically lacked vertical resolution; the shift to 4D arrays now bridges that gap. LiDAR, once confined to mechanical architectures, is moving to solid-state, trimming moving parts and enhancing automotive-grade reliability. Collectively, tri-modal sensor stacks establish a baseline in Level 3 homologations, preserving demand diversification within the broader Robotics and ADAS Vehicles Sensor Market industry.

By Vehicle/Automation Level: L4-L5 Drives Sensor Intensity

Level 1-Level 2 vehicles formed 57.25% of global deployments in 2025, each carrying USD 200-400 in sensor content. Level 2+ systems double that spend, leveraging dual radar and backup camera channels for functional-safety redundancy. The Robotics and ADAS Vehicles Sensor Market for Level 3 is projected to expand at a notable CAGR because regulatory clarity in Germany, Japan, and California unlocks premium upsell opportunities. Mercedes Drive Pilot exemplifies the redundancy step-function: 2 LiDAR, 5 radars, 6 cameras, and 12 ultrasonics elevate BOM to USD 3,000 while granting conditional-automation liability shifts.

Highly Automated L4-L5 Platforms are set to expand at a 9.81% CAGR through 2031. Level 4 robotaxis and autonomous trucks intensify hardware content further. Aurora Driver fields 4 LiDAR, 7 radars, and 12 cameras, costing highly per unit yet justifying payback within 18 months via labor substitution. Waymo’s 5th-generation suite halves prior-gen cost by internalizing radar production, revealing that vertical integration can whittle premium hardware to near-passenger-car affordability. As pilot fleets scale, learnings cascade into future consumer releases, bolstering shipment outlook for the Robotics and ADAS Vehicles Sensor Market.

By Vehicle Type: Commercial Fleets Accelerate Adoption

Passenger cars accounted for 75.10% of sensor-equipped builds in 2025, while commercial vehicles are growing at an 8.91% CAGR through 2031. Daimler Truck’s Detroit Assurance 6.0 suite cuts collision frequency by 30% and parlayed that metric into 15-20% insurance savings for U.S. fleets. Volvo Trucks meets Europe’s 2024 GSR with radar-camera brake assist on every unit, setting a compliance baseline that scales sensor volumes. High asset utilization in trucking accelerates ROI on premium sensor suites, rendering BOM uplift palatable.

Urban logistics vans adopt 360-degree vision and corner radar for last-mile maneuvering, expanding sensor addressability beyond long-haul Class 8 tractors. Navistar’s International LT integrates side radar for blind-spot monitoring, catering to fleet demand for driver retention through safety technology. These factors elevate commercial-vehicle wallet share within the broader sensor market in the robotics and ADAS vehicles industry.

By Propulsion Type: EVs Enable Sensor Integration Advantages

Internal combustion engine vehicles represented 79.12% of sensor-equipped platforms in 2025, yet electric vehicles (EVs) are logging a 10.21% CAGR through 2031. Absence of engine vibration and heat enables precise sensor calibration and extended uptime for LiDAR units. Tesla’s cabin-facing cameras operate continuously without a range penalty, exploiting stable EV voltage rails. BYD’s Han EV leverages a central compute that simultaneously manages battery and perception functions, mitigating the need for discrete ADAS ECUs and trimming weight.

NIO's ET7 packages InnovizTwo LiDAR plus NVIDIA Orin compute, retailing under a high price point - a feat challenging for ICE rivals due to added power-management complexity. As charging networks expand, EV design cycles shorten, allowing faster sensor refresh than ICE platforms. These dynamics nudge sensor suppliers to prioritize high-voltage-ready designs, enriching the Robotics and ADAS Vehicles Sensor Market' opportunity pool.

Geography Analysis

Asia-Pacific’s 36.12% market share in 2025 and 9.25% CAGR mirror China’s C-NCAP and dual-credit mandates that bake camera and radar into sub-USD 25,000 vehicles. XPeng’s USD 28,000 P5, equipped with dual Hesai LiDAR units, exemplifies mid-tier sensor saturation difficult for Western brands to replicate. Japan’s 2025 subsidy for pedal-misapplication prevention drives ultrasonic and radar demand among elderly drivers, while South Korea’s compulsory ADAS for commercial trucks stimulates domestic supply chains, reinforcing Asia-Pacific leadership in the Robotics and ADAS Vehicles Sensor Market.

Europe’s July 2024 GSR makes AEBS, LKA, ISA, and DMS mandatory; compliance costs challenge smaller OEMs but guarantee baseline sensor volumes. Germany’s Level 3 approval anchored by Mercedes Drive Pilot sets a liability precedent that other EU states may mimic, eventually enlarging the sensor attachment rate. However, slower EV uptake and fragmented supplier networks temper Europe’s CAGR, marginally under the global pace but still additive to the Robotics and ADAS Vehicles Sensor Market' trajectory.

North America splits between permissive states—Texas, Arizona—where autonomous trucking pilots proliferate, and cautious regulators such as California that cap commercial Level 4 robotaxis. Still, NHTSA’s crash-reporting mandate incentivizes high-reliability sensor suites because insurers translate failure data into policy premiums. Fleet operators in logistics corridors now spec ADAS as standard, lifting commercial-vehicle sensor content and sustaining overall demand within the regional Robotics and ADAS Vehicles Sensor Market.

Competitive Landscape

Competition remains moderately fragmented: the top Tier-1s hold a significant share, producing radar, camera, and ultrasonic bundles that lower OEM integration cost. In 2026, Bosch integrated its in-house radar SoC with a multipurpose 8-megapixel camera, highlighting the benefits of owning silicon. Continental's 4D imaging radar, supplied to Stellantis and Renault in 2026, positions radar as a cost-effective substitute for LiDAR in highway-pilot programs. Valeo is advancing to third-generation LiDAR at a competitive cost, challenging competitors still reliant on pricier mechanical solutions.

In the upstream semiconductor layer, Infineon is making substantial investments in capacity to strengthen European radar-sensor sovereignty. Concurrently, ON Semiconductor is transitioning imagers to advanced nodes, achieving significant reductions in die area and bolstering its cost leadership. Chinese innovators, Hesai and RoboSense, are vertically integrating photonics to produce automotive LiDARs at competitive price points, a benchmark not yet reached by Western players. Startups like Apex.AI and Applied Intuition are capitalizing on sensor-agnostic middleware, enabling OEMs to switch hardware with minimal code alterations, thus shifting bargaining power from hardware to software licenses.

M&A and strategic alliances are on the rise. Aurora integrated Blackmore’s FMCW LiDAR into its trucking suite, enhancing range and immunity to cross-talk, vital for convoy operations. Mobileye has clinched an imaging-radar supply deal with a leading automaker, gearing up for 2028's Level 3 launches, underscoring radar's resurgence as a vital component. While ISO/TS 5083 functional-safety validation solidifies the position of established players, it also opens doors for newcomers who can demonstrate equivalence through simulation, keeping the Robotics and ADAS Vehicles Sensor Market vibrant.

Robotics and ADAS Vehicles Sensor Industry Leaders

NXP Semiconductor N.V.

Infineon Technologies AG

ST Microelectronics NV

Continental AG

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Bosch unveiled an in-house radar SoC bundled with an 8-megapixel camera and inertial unit, creating a modular ADAS family aimed at entry to luxury vehicles.

- December 2025: Innoviz launched InnovizThree, a compact automotive-grade LiDAR designed for behind-windshield integration, simplifying OEM packaging.

- October 2025: Aptiv introduced Gen 8 antenna-on-silicon radar for AI-driven ADAS, improving resolution without footprint growth.

- October 2025: A global automaker chose Mobileye Imaging Radar for 2028 highway Level 3 deployments after head-to-head evaluations.

Global Robotics and ADAS Vehicles Sensor Market Report Scope

The scope includes segmentation by sensor type (camera modules, lidar, radar, and ultrasonic and other sensors), vehicle/automation level (ADAS L1-L2, ADAS L2+/L3, and highly automated L4-L5), vehicle type (passenger car and commercial vehicle), and propulsion type (ICE vehicles and electric vehicles). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD.

| Camera Modules |

| LiDAR |

| Radar |

| Ultrasonic and Other Sensors |

| ADAS L1-L2 Platforms |

| ADAS L2+/L3 Platforms |

| Highly Automated L4-L5 Platforms |

| Passenger Car |

| Commercial Vehicle |

| Internal Combustion Engine Vehicles |

| Electric Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of the Middle East and Africa |

| By Sensor Type | Camera Modules | |

| LiDAR | ||

| Radar | ||

| Ultrasonic and Other Sensors | ||

| By Vehicle / Automation Level | ADAS L1-L2 Platforms | |

| ADAS L2+/L3 Platforms | ||

| Highly Automated L4-L5 Platforms | ||

| By Vehicle Type | Passenger Car | |

| Commercial Vehicle | ||

| By Propulsion Type | Internal Combustion Engine Vehicles | |

| Electric Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

Which sensor category shows the fastest growth trajectory through 2031?

LiDAR is forecast to expand at a 10.62% CAGR, outpacing cameras, radar, and ultrasonic sensors as OEMs add redundancy for Level 3 and higher automation.

How quickly are commercial fleets adopting advanced perception hardware?

Commercial vehicles are registering an 8.91% CAGR to 2031 because lower collision rates translate into 15-20% insurance savings, compelling fleet managers to spec ADAS as standard.

How large is the Asia-Pacific opportunity compared with Europe?

Asia-Pacific held 36.12% share in 2025 and is advancing at a 9.25% CAGR, whereas Europe is growing at a comparatively low CAGR as stricter regulations meet slower EV uptake.

What is the typical hardware cost for a hands-free Level 3 driving system?

A fully redundant Level 3 suite—such as Mercedes Drive Pilot—carries roughly USD 3,000 in sensor content, including dual LiDAR, five radars, six cameras, and twelve ultrasonics.

Page last updated on: