Self-service BI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

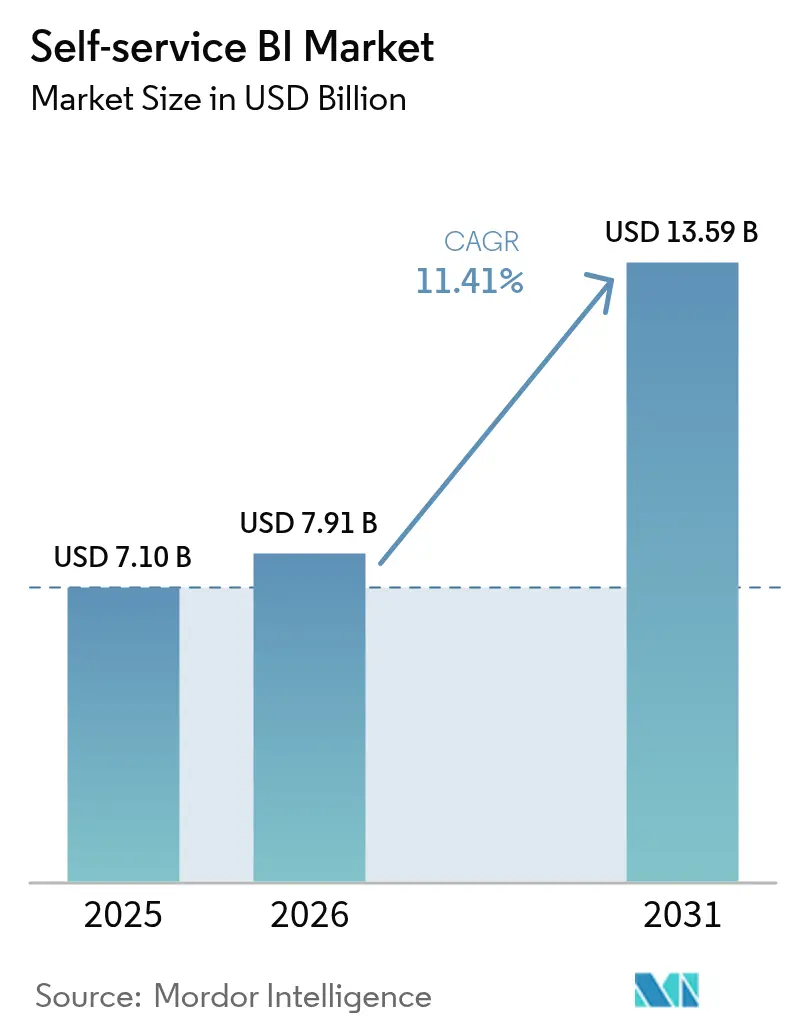

| Market Size (2026) | USD 7.91 Billion |

| Market Size (2031) | USD 13.59 Billion |

| Growth Rate (2026 - 2031) | 11.41% CAGR |

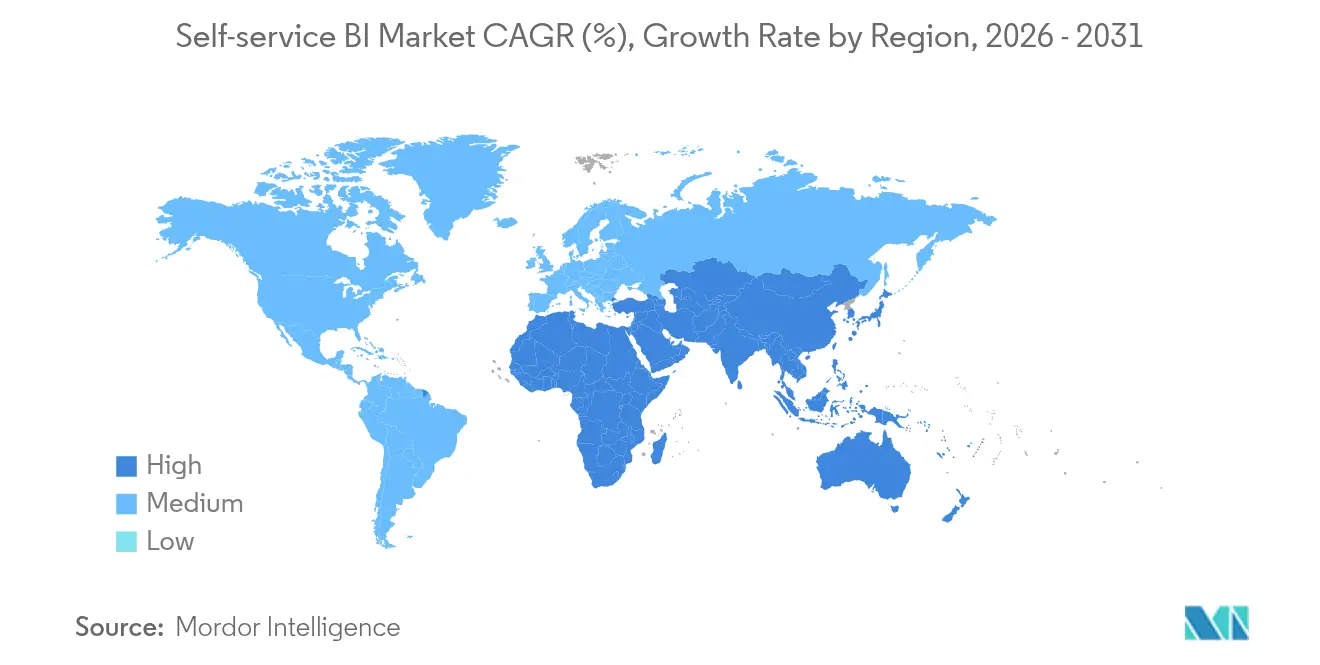

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

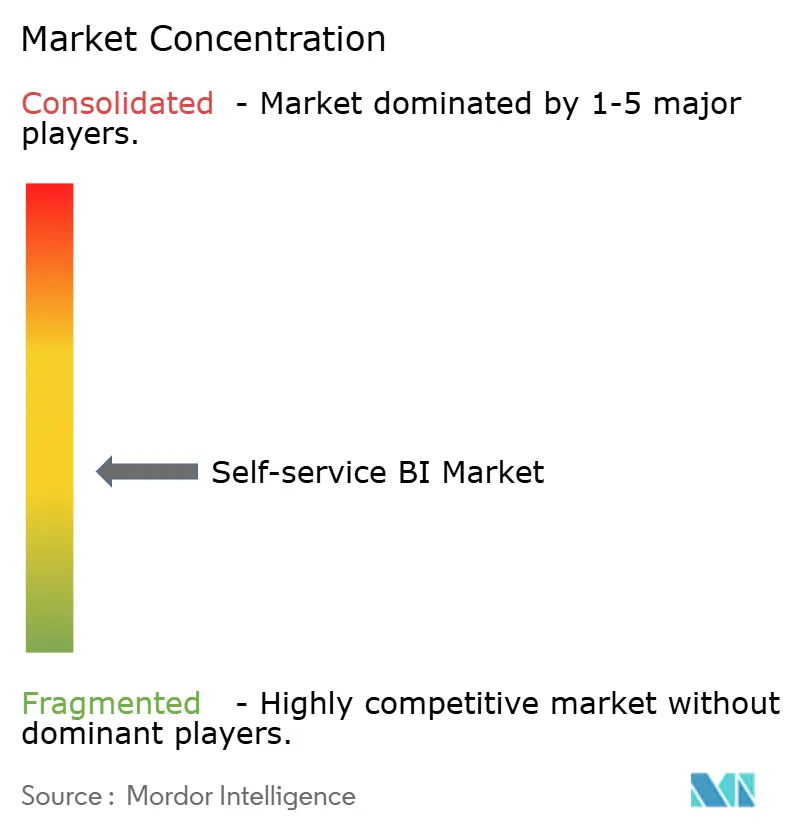

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-service BI Market Analysis by Mordor Intelligence

The self-service BI market size is expected to grow from USD 7.10 billion in 2025 to USD 7.91 billion in 2026 and is forecast to reach USD 13.59 billion by 2031 at 11.41% CAGR over 2026-2031. Firms are scaling low-code analytics, embedding generative AI, and shifting workloads to cloud data warehouses, which shortens insight cycles and frees IT staff for strategic work. North American organizations lead adoption after proving that intuitive tools can cut reporting backlogs by roughly one-third, while Asia-Pacific businesses are catching up fast as cloud infrastructure matures. Vendors are racing to integrate natural-language querying that supports multilingual environments, a capability already boosting engagement among European users. Meanwhile, heightened attention to governance, driven by regulatory pressure and shadow-IT incidents, is steering purchasing toward platforms that pair open architectures with automated control features. [1]Mallikarjun Bussa, “Emerging Trends in Self-Service BI Platforms: Democratizing Data Insights,” International Journal of Scientific Research in Computer Science Engineering and Information Technology, doi.org

Key Report Takeaways

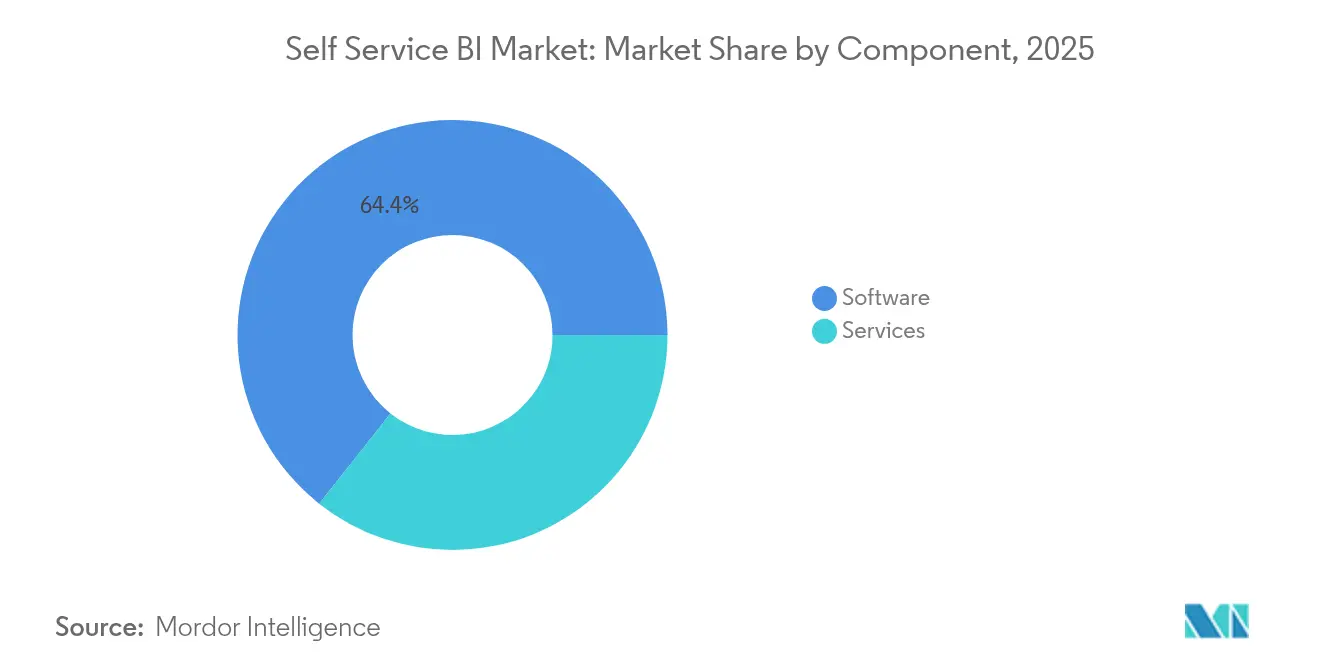

- By component, Software captured 64.35% of the self-service BI market share in 2025; the Services segment is advancing at a 14.92% CAGR to 2031.

- By deployment model, Cloud/On-Demand accounted for 72.40% of the self-service BI market size in 2025 and is growing at a 13.24% CAGR.

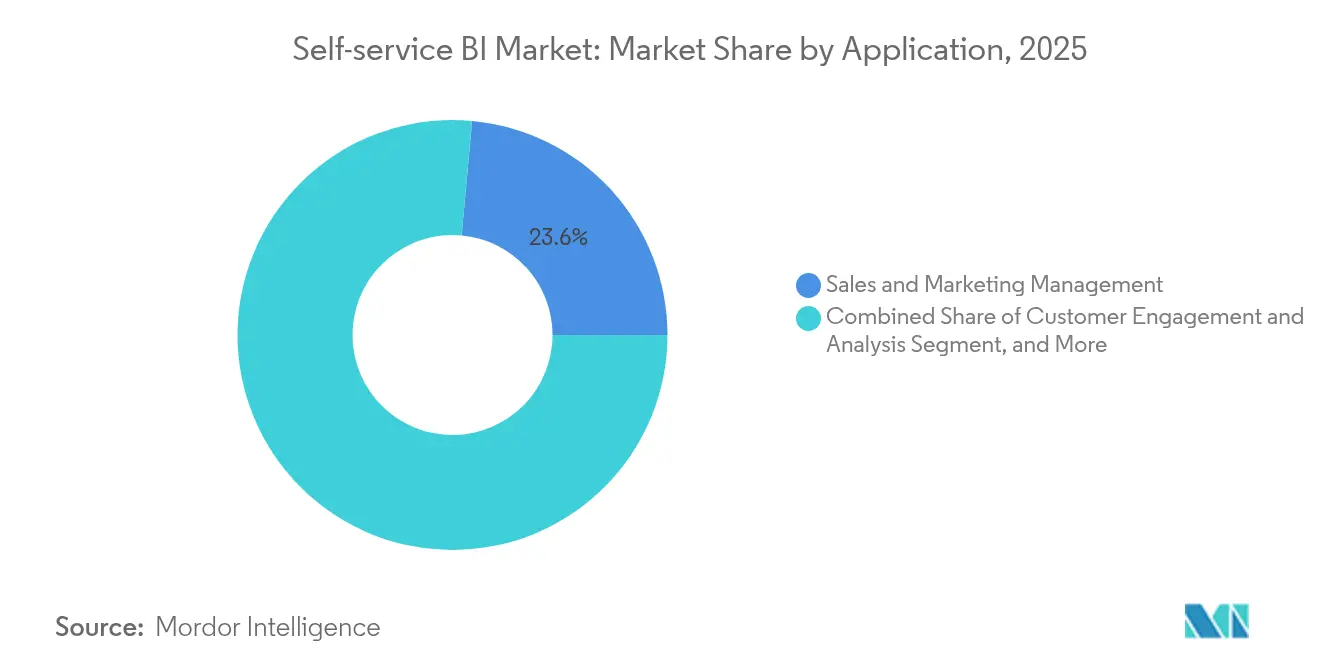

- By application, Sales & Marketing held 23.55% revenue share in 2025; Customer Engagement analytics is expanding at a 15.76% CAGR through 2031.

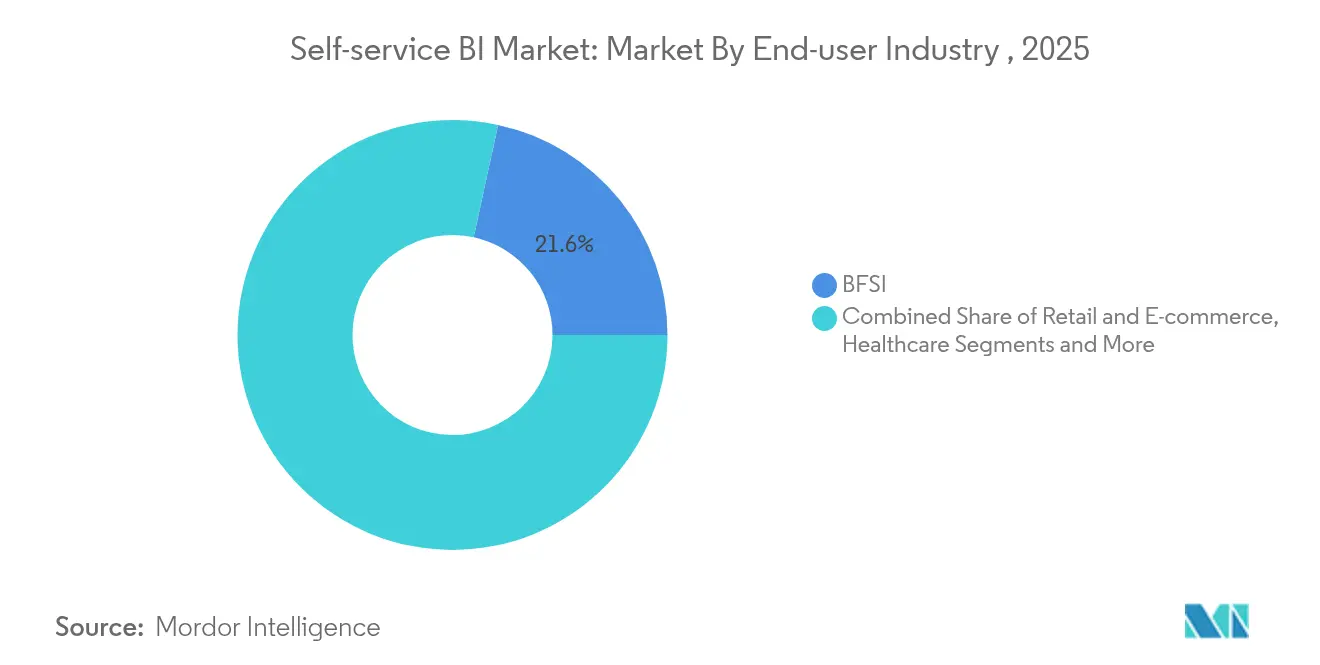

- By end-user industry, BFSI led with 21.60% of the self-service BI market size in 2025, while Healthcare is projected to expand at a 13.92% CAGR.

- By organization size, Large Enterprises commanded 67.25% of the self-service BI market share in 2025; Asia-Pacific is projected to grow at a 13.50% CAGR.

- By geography, North America commanded 41.50% of the self-service BI market share in 2025; SMEs are projected to grow at a 14.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Self-service BI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Democratization of Analytics via Low-code/No-code Tools | +3.2% | North America, Europe | Medium term (2-4 years) |

| Surge in Cloud-based Data Warehouses Accelerating Self-service Adoption | +2.7% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Integration of Generative AI for Natural-Language Querying | +2.5% | Europe, North America | Medium term (2-4 years) |

| Embedded Analytics Demand from SaaS Vendors | +1.4% | Global | Medium term (2-4 years) |

| Rising Data-Literacy Programs Among Mid-Sized Enterprises | +1.1% | Global | Long term (≥ 4 years) |

| Regulatory Push for Data-Residency Compliance Driving Localized BI Platforms | +0.5% | Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Democratization of analytics via low-code/no-code tools

Low-code interfaces let business professionals create dashboards without relying on developers, a shift most visible in North America where 80% of executives credit wider data access for faster decisions. Productivity for analytical tasks has risen 74% as citizen data scientists pair domain knowledge with simplified tooling, unearthing patterns traditional BI teams often overlook. Companies that married democratization with robust semantic layers cut backlog hand-offs and delivered insight within the operational window where actions still matter. This cultural change is expanding platform evaluation criteria from feature depth to the ease of onboarding non-technical staff, driving platform consolidation around intuitive drag-and-drop authoring and in-app guidance.

Surge in cloud-based data warehouses accelerating self-service adoption

Asia-Pacific organizations are leapfrogging legacy stacks by landing data in the cloud, eliminating bottlenecks that once restricted BI concurrency. With the cloud warehouse segment itself climbing at 27.64% CAGR, analytics teams now query fresh data without queuing jobs, shrinking report time by as much as 40%. Firms that align self-service rollouts with warehouse modernization gain triple-speed time-to-insight compared with siloed deployments. Centralized governance baked into these warehouses also raises data quality, enabling consistent metrics across departments. [2]Firebolt, “Cloud Data Warehouse Key Statistics & Industry Trends,” firebolt.io

Integration of generative AI for natural-language querying

Natural language search has become the final catalyst for truly self-served analytics. European organizations, long challenged by multilingual user bases, now see 50% more non-technical engagement after rolling out LLM-powered interfaces. Large language models turn conversational prompts into optimized SQL, then surface narrative explanations of trends, which shifts the perception of BI from a visualizer to an active advisor. Vendors highlight this capability as table stakes: buyers increasingly rank NLQ responsiveness above chart variety when scoring RFPs.

Embedded analytics demand from SaaS vendors

BFSI and retail software providers embed self-service dashboards directly into operational apps, which eliminates context-switching and drives a documented 35% lift in customer satisfaction. API-first BI platforms that allow white-label customization are therefore growing wallet share inside SaaS ecosystems. As this model matures, the distinction between transactional and analytical systems blurs, locking BI providers into long-term contracts and raising switching costs for end customers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shadow-IT Risks from Uncontrolled Data Visualization Tools | -1.2% | Global | Short term (≤ 2 years) |

| Shortage of Data Governance Talent in Emerging Economies | -0.9% | Asia-Pacific, Middle East & Africa | Medium term (2-4 years) |

| High Migration Cost from Legacy BI to Self-service Stacks | -0.8% | North America, Europe | Short term (≤ 2 years) |

| Vendor Lock-in Concerns with Proprietary Semantic Layers | -0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shadow-IT risks from uncontrolled visualization tools

Unvetted tool adoption has generated conflicting KPIs and exposed sensitive datasets, costing non-compliant firms USD 1.03 million on average per incident. Marketing and finance units are frequent offenders because rapid iterations tempt them to sidestep IT. Best-in-class enterprises deploy catalog-driven governance, automated lineage, and role-based access that preserve agility yet curb risk, yielding 45% higher adoption than blanket lockdown approaches.

Shortage of data-governance talent in emerging economies

Emerging markets face acute hiring gaps, with 57% of CIOs naming governance expertise their top AI-analytics bottleneck. Vendors that bundle automated policy enforcement and role-specific training gain a foothold by offsetting the skills deficit. Companies rolling out self-service BI in phased sprints—first standardizing metadata, then widening access—create durable data cultures while managing resource constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Advisory services narrow the adoption gap

The software segment continues to anchor revenue, yet services revenue is compounding faster at 14.92% CAGR. Organizations that pair platform purchases with training programs report adoption rates 45% higher than tool-only buyers. Demand is shifting toward continuous enablement subscriptions that cover data-literacy upskilling and governance audits. As a result, implementation specialists are packaging industry-specific playbooks, aligning dashboards with vertical KPIs, and expediting time-to-value. The self-service BI market size for services is projected to reach USD 5.83 billion by 2031, reflecting sustained appetite for human expertise alongside automation.

Software vendors, meanwhile, prioritize AI feature parity, adding NLQ, automated insights, and embedded modes to remain competitive. The relentless update cadence pushes enterprises to favor modular architectures that let them swap analytic engines without ripping out semantic layers. This posture mitigates vendor lock-in concerns and supports mixed-tool environments that evolve as AI capabilities mature.

By Deployment Model: Cloud preference becomes irreversible

Cloud deployments own both usage and momentum, commanding 72.40% of current revenue and adding users at a 13.24% CAGR. Economies of scale let mid-market firms implement enterprise-grade analytics without capital outlay, leveling the playing field with larger peers. Moreover, distributed teams can collaborate on shared workspaces in real time, accelerating feedback loops. Security postures have evolved; encryption-at-rest, private links, and regional data centers now satisfy most regulatory audits, tempering earlier reservations about public cloud.

On-premises solutions persist in heavily regulated verticals where data residency is mandatory. Yet even there, hybrid designs are common: sensitive tables stay onsite while aggregated models sync to the cloud for broad exploration. Over the forecast period, the self-service BI market share for cloud is expected to edge past 80.85% as hyperscalers integrate BI tightly with their storage and AI services.

By Application: Customer engagement analytics outpaces traditional reporting

Customer Engagement & Analysis is the fastest mover with a 15.76% CAGR, reflecting the shift from descriptive to predictive insight. Retailers and subscription businesses mine behavioral data to pre-empt churn and personalize offers, improving retention metrics by double digits. Generative models further enhance this segment by auto-summarizing sentiment from call transcripts and social mentions, bringing unstructured data into the analytics fold.

Sales & Marketing remains the biggest slice at 23.55% of 2025 revenue. Dashboards tracking funnel velocity, campaign ROI, and territory alignment remain foundational. Emerging use cases extend into cross-sell propensity scoring and ABM targeting, enriching account views for go-to-market teams. As embedded analytics spreads, front-line sellers gain direct access to these insights inside CRM systems, closing the gap between analysis and action.

By End-user Industry: Healthcare narrows the lead

BFSI still contributes the largest spend, driven by risk models, fraud analytics, and regulatory reporting. Yet Healthcare is growing faster at 13.92% CAGR as electronic health records and value-based care push providers toward data-driven operations. Hospitals deploying self-service scheduling tools cut appointment cancellations by 40%, freeing clinical capacity and improving outcomes. Insurance payers are merging claims and wearable-device streams to personalize wellness programs, underscoring how healthcare data variety fuels BI demand.

Manufacturing is exploiting predictive maintenance dashboards that harvest sensor output to avoid unplanned downtime, while Telecommunications leverages network analytics to enhance customer experience. Government agencies, though slower to procure, recognize BI as central to transparency mandates and stimulus program tracking, positioning the sector for steady expansion after 2026.

By Organization Size: SMEs become the growth engine

Large Enterprises held 67.25% revenue in 2025 thanks to mature data estates and larger budgets. The growth spotlight now shifts to SMEs, whose 14.78% CAGR exceeds the overall self-service BI market growth by more than three points. Subscription-based pricing, low administration overhead, and verticalized templates de-risk adoption for lean teams. SMEs using self-service dashboards report 30% better performance metrics once reliance on spreadsheet reporting fades.

Vendors courting this segment tailor onboarding to non-specialists and bundle bite-size learning paths. Community-led support, marketplace connectors, and pay-as-you-grow licensing form the core of SME-oriented value propositions. Over the forecast horizon, wider SME penetration will broaden the self-service BI industry’s customer base and diversify feature roadmaps toward simplicity and speed.

Geography Analysis

North America retains 41.50% of self-service BI market revenue, buoyed by early adoption of low-code platforms and the presence of leading vendors. Financial services and healthcare providers there embed natural-language querying in day-to-day workflows, keeping user sentiment high and shadow-IT incidents under control through mature governance programs. R&D investments focus on advanced AI explainability, preparing systems to justify recommendations in regulated settings. Cross-border data-sharing rules remain a watchpoint, yet the region’s sophisticated cloud infrastructure continues to attract innovative analytics startups that expand platform ecosystems.

Asia-Pacific is the fastest growing territory, advancing at a 13.50% CAGR. China, India, Japan, and Australia demonstrate vigorous demand as domestic cloud giants and hyperscalers alike pour capital into data centers. SMEs in the region use mobile-first analytics to overcome desktop scarcity, with smartphone dashboards becoming the primary interface for many field employees. Talent shortages in data governance persist, prompting governments and academia to launch certification programs that should ease constraints after 2027. Manufacturing adoption is strong in Japan and South Korea, where predictive maintenance aligns with Industry 4.0 roadmaps, while financial hubs like Singapore emphasize customer analytics to differentiate regional banking services.

Europe shows steady uptake shaped by strict privacy statutes. Organizations balance democratization with GDPR compliance by opting for platforms that support fine-grained consent management and local data processing. Multilingual natural-language interfaces are especially valued, lifting engagement among non-technical staff by 50% in pilot projects. Western European cloud migration is accelerating after regulators clarified that encryption and local failover meet sovereignty requirements. Eastern Europe is catching up quickly as digital transformation funding flows into Poland, Romania, and the Czech Republic. Retail and discrete manufacturing dominate demand, though open-source alternatives gain traction in institutions wary of proprietary lock-in.

South America, the Middle East, and Africa remain early-stage yet promising. Brazil and Mexico head Latin American adoption, with telecom operators and banks seeking real-time customer views. Gulf Cooperation Council governments anchor investment in the Middle East, leveraging BI to support diversification agendas and smart-city initiatives. African uptake is fragmented; South Africa leads enterprise deployments, while Nigeria and Kenya show momentum through fintech ecosystems. Across these regions, cloud solutions enjoy preference owing to limited legacy estates, and mobile dashboards bridge infrastructure gaps in areas where desktop penetration is low.

Regulatory Landscape

Regulation shaping self-service BI centers on data protection, data access, and the governance of AI-enabled analytics, especially as cloud/on-demand deployments represented 72.40% of market revenue in 2025. In the European Union, the Data Act (Regulation (EU) 2023/2854) entered its initial application phase in September 2025, which raises interoperability, data-sharing, and switching requirements. This, in turn, influences BI platform architectures and connector strategies. Separately, the EU AI Act (Regulation (EU) 2024/1689) introduces mandatory governance provisions for high-risk AI systems and transparency obligations for certain AI outputs, adding documentation and control expectations for BI features that use generative AI for natural-language querying and narrative insights.

In the United States, government and regulated deployments are anchored to security categorization and control frameworks such as FIPS 199 and NIST SP 800-53, which push vendors toward auditable access control, logging, and continuous monitoring for analytics workspaces. Federal agencies are also updating internal AI governance: the General Services Administration issued Directive CIO 2185.1C in March 2026 (posted June 2026), formalizing responsible AI adoption practices that reinforce tenant-level governance, model oversight, and policy-driven use of AI capabilities within analytics platforms. These policy signals steer procurement toward platforms that combine self-service agility with compliance-ready governance and data-residency options.

Value Chain Analysis

The self-service BI value chain spans data generation and operational systems (ERP, CRM, OSS/BSS, WMS/TMS), data platform layers (cloud data warehouses and lakehouse storage), semantic and governance layers, and end-user analytics experiences (dashboards, embedded analytics, and natural-language interfaces). Upstream, cloud providers and data-platform vendors supply scalable compute, storage, identity, and audit capabilities. Midstream, BI vendors package data preparation, modeling, visualization, and AI-assisted querying. Downstream, system integrators and advisory providers deliver implementation, training, and governance programs that raise adoption and reduce shadow-IT risk.

Ecosystem integration is increasingly defined by standardized connectors and shared semantic definitions, helping business users explore governed metrics without creating conflicting KPIs. Bottlenecks commonly arise from fragmented data silos, legacy migration complexity, and insufficient governance talent, which elevates the role of services and managed enablement. Recent platform moves reinforce the shift toward warehouse-native and agent-enabled workflows, including Google making Conversational Analytics in BigQuery generally available in July 2026. In parallel, vendors are aligning self-service experiences to enterprise access controls and auditability rather than treating visualization as a standalone layer.

Competitive Landscape

The self-service BI market displays moderate concentration. Microsoft Power BI, Salesforce Tableau, and Qlik retain lead positions due to embedded ecosystems and broad partner networks. Microsoft deepened its advantage by integrating GPT-4-Turbo for conversational analytics that shortens query build time dramatically. Tableau enhanced embedded options through new APIs, appealing to SaaS providers that view analytics as core product differentiators. Qlik invested in a lakehouse architecture on Apache Iceberg, signaling a pivot toward unified data management.

Cloud hyperscalers intensify competition. Google couples Looker with Vertex AI to deliver customizable AI insight tiles, while Amazon QuickSight leverages native data lake integration for cost-aware scaling. Specialist vendors ThoughtSpot and Sisense carve niches in search-based UX and white-label embedded BI, respectively. Open-source platforms gain mindshare among buyers wary of proprietary semantic layers that complicate multi-cloud strategies.

Strategic alliances and M&A shape the battlefield. BI vendors partner with data-catalog providers to fuse discovery and governance, while service integrators acquire niche consultancies to offer end-to-end modernization packages. Competitive success hinges less on charting features and more on ecosystem extensibility, AI breadth, and governance automation.

Self-service BI Industry Leaders

Microsoft Corporation

IBM

Oracle Corporation

SAP SE

SAS Institute

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity is the shift from dashboard-led self-service BI to agentic and conversational analytics operating inside governed data environments, narrowing the gap between questions, analysis, and actions. The opportunity is supported by vendor launches that productize this direction. In May 2026, Salesforce announced the Tableau Agentic Analytics Platform and an Agentic Analytics Command Center, aimed at governance and observability for autonomous analytics agents. In July 2026, Google Cloud announced general availability of Conversational Analytics in BigQuery, positioning natural-language, multi-step analysis to inherit BigQuery security and governance. These releases create space for enterprises to standardize how LLM-driven querying, narrative explanations, and automated investigative workflows are controlled, audited, and rolled out across business functions.

Another opportunity lies in interoperability and vendor lock-in mitigation across multi-cloud and heterogeneous data estates, where organizations want self-service experiences to remain consistent even as storage, catalogs, and semantic layers vary by domain. The EU Data Act application phase starting in September 2025 raises the importance of portability and switching, which aligns with demand for open architectures, standardized connectors, and semantic-layer governance that can move with the business. Services providers also have expansion room as governance talent shortages persist in emerging economies, supporting enablement subscriptions that bundle training, policy implementation, and ongoing governance audits alongside software adoption.

Recent Industry Developments

- July 2026: Oracle introduced an AI-native builder experience for Oracle AI Agent Studio within Fusion Cloud Applications, enabling customers to create and run agentic applications using native tooling. Bringing agent development closer to application data and workflows strengthens Oracle’s positioning for governed self-service analytics that feeds operational decisions rather than static reporting.

- May 2026: Salesforce announced the Tableau Agentic Analytics Platform, including an Agentic Analytics Command Center designed for governance and observability of autonomous analytics agents. The launch signals a product-level shift toward controlled, agent-driven self-service experiences, which supports enterprise rollouts where auditability and policy enforcement are procurement requirements.

- April 2025: Microsoft added GPT-4-Turbo natural-language querying and enhanced governance capabilities to Power BI. This expanded conversational access for non-technical users while reinforcing administrative controls that organizations use to curb shadow-IT risks and maintain consistent metrics at scale.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the self-service BI market is defined as software and related services that let business users build dashboards, run ad hoc analysis, and share insights, with limited day to day dependence on IT. Coverage includes both cloud and on-premise deployments.

Scope exclusions: We exclude generic spreadsheets and databases, traditional reporting tools without self-service features, and fully managed analytics outsourcing that is priced mainly as a services contract.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Model

- Cloud / On-Demand

- On-Premises

- By Application

- Sales and Marketing Management

- Customer Engagement and Analysis

- Fraud and Security Management

- Predictive Asset Maintenance

- Risk and Compliance Management

- Supply Chain and Procurement

- Operations Management

- By End-user Industry

- BFSI

- Retail and E-commerce

- Healthcare

- Manufacturing

- Telecommunications

- Media and Entertainment

- Transportation and Logistics

- Energy and Utilities

- Government and Defense

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what counts as self-service BI and to anchor the model with repeatable outside indicators. We relied on public sources such as the US Bureau of Labor Statistics for labor and productivity series, the US Census Bureau and Eurostat for business digitization signals, and IT and cloud adoption statistics from bodies such as the OECD and the International Telecommunication Union.

To keep the commercial view realistic, we also reviewed company filings, investor presentations, product documentation, and reputable press coverage for pricing moves, packaging changes, and deployment shifts. Patent databases and peer-reviewed journals were used selectively to understand product direction, for example natural language query and embedded analytics, which can influence adoption curves and renewal behavior. In addition, approved paid subscriptions for company financials and for news and financial screening were used to check revenue exposure and deal momentum. The sources listed here are illustrative, and many other public and paid references were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with software providers, channel and implementation partners, and enterprise buyers who run analytics programs, so we could validate adoption, packaging, and average selling price assumptions. Because this is a global market, inputs were checked across APAC, EMEA, and the Americas. We then used the feedback to close gaps left by public data and to confirm that the final totals match observed purchase patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 13% | APAC: 49% |

| Mid tier: 46% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 15% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where enterprise software spend and analytics modernization signals are translated into a self-service BI demand pool using adoption rates, deployment mix, and typical contract patterns. Once that structure is in place, we corroborate totals with selective bottom-up approximations, such as sampled vendor revenue exposure, channel checks, and a volume-times-ASP sense-check for user-based subscriptions, before adjustments are finalized.

Key inputs used in the model include cloud versus on-premise share, seat growth and usage intensity for self-serve authoring, average contract value progression, renewal and churn expectations, and the mix of services attached to deployments and governance rollouts. Because product packaging changes can move revenue between license and services lines, we normalize pricing to a common unit and then convert into USD using consistent currency timing for the base year.

Forecasting uses scenario analysis supported by trend lines for the main variables, which are stress-tested with primary feedback around budget cycles, data governance maturity, and the pace of AI enabled features entering standard editions. Where bottom-up visibility is thin in smaller regions or in long-tail industries, gap handling is done by applying penetration ranges tied to the local installed base of analytics users, then rechecking the outcome against independent spend and adoption signals.

Data Validation & Update Cycle

Outputs are validated in several passes so the final number stays tied to what buyers can actually spend and deploy. We compare the model totals against independent signals such as enterprise software spend direction, cloud migration pace, and vendor reported performance, and then investigate unusual jumps before sign-off.

Assumptions are reviewed by a second analyst, and follow-up calls are triggered when interview feedback conflicts with desk indicators, or when pricing and packaging shifts create discontinuities. The report is refreshed annually, with interim updates when material events occur, and a final pre-delivery sweep is completed so clients receive the latest updated view.

Mordor Intelligence's Self Service Bi Market Growth Trends and Forecast Market Size Measured Against Other Published Estimates

Published market sizes for self-service BI rarely match perfectly because the boundaries of the market are drawn differently and the revenue lines are counted in different ways. Differences also come from the year used as the anchor, how services are treated, and how quickly assumptions get refreshed when product bundles and cloud pricing change.

By tracking pricing-packaging changes and refreshing currency timing checks, Mordor Intelligence keeps the model aligned to self-service BI platforms and attached services, instead of letting adjacent analytics categories inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.91 B (2026) | |

| Industry Publisher A | USD 9.84 B (2024) | Uses an earlier anchor year and a broader revenue framing that emphasizes software plus services across many applications, which can pull in adjacent BI and analytics work that is not strictly self-service. |

| Data Aggregator B | USD 10.10 B (2024) | Anchors the market in 2024 and tends to report a wider component and vertical coverage, which can shift the total upward when traditional BI bundles and general analytics services are grouped under self-service. |

The spread in the table is mainly explained by anchor-year differences and by how closely each study separates true self-service functionality from nearby BI and analytics spend. Our approach stays traceable because the inputs are tied to adoption, deployment mix, and normalized pricing, which makes the final number easier to replicate and update when market conditions change.

Key Questions Answered in the Report

What is the current Self-service BI Market size?

The Self-service BI Market is projected to register a CAGR of 11.41% during the forecast period (2026-2031)

What is the current self-service BI market size?

The self-service BI market is valued at USD 7.91 billion in 2026.

How fast is the self-service BI market expected to grow?

The market is projected to expand at an 11.41% CAGR, reaching USD 13.59 billion by 2031.

Which deployment model is gaining the most traction?

Cloud/On-Demand deployment leads with 72.40% revenue share and is growing at a 13.24% CAGR as firms favor scalability and lower maintenance.

Which application segment is the fastest growing?

Customer Engagement & Analysis is advancing at a 15.76% CAGR due to rising demand for personalized customer insights.

Why are SMEs increasingly adopting self-service BI?

Subscription pricing, ease of use, and vertical templates enable SMEs to capture data-driven advantages once limited to large enterprises, driving a 14.78% CAGR in the segment.

What are the primary challenges to wider self-service BI adoption?

Shadow-IT risks and a global shortage of data governance talent remain the key hurdles; organizations counter them with stronger governance frameworks and targeted training.

Page last updated on: