Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

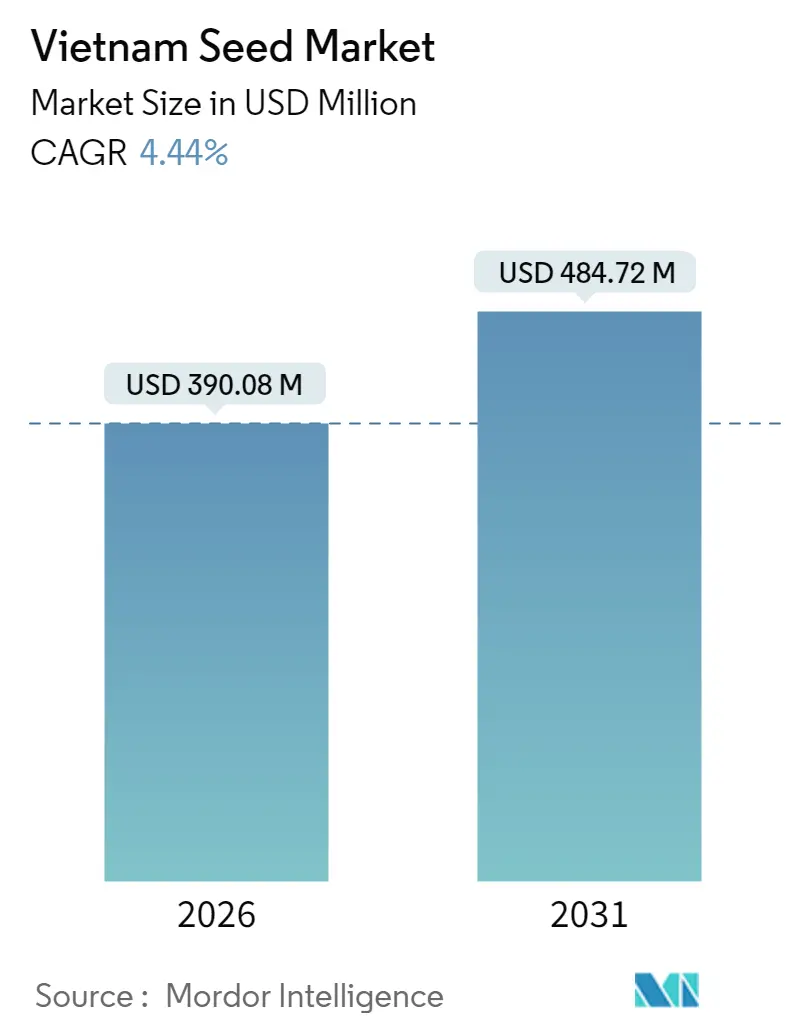

| Market Size (2026) | USD 390.08 Million |

| Market Size (2031) | USD 484.72 Million |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Seed Market Analysis by Mordor Intelligence

The Vietnam seed market is expected to grow from USD 373.5 million in 2025 to USD 390.08 million in 2026 and is forecast to reach USD 484.72 million by 2031 at 4.44% CAGR over 2026-2031. Continued momentum in rice exports, vegetable demand, and climate-smart cultivation keeps the Vietnam seed market on a moderate expansion path.[1]Source: CGIAR Communications, “IRRI joins forces with Vietnam Seed Corporation to develop premium rice varieties,” CGIAR.org At the same time, technology alliances accelerate varietal innovation and data-centric farm management. Private capital inflows, digital certification platforms, and government incentives for certified seed adoption propel formal market channels, yet counterfeits, R&D cost burdens, and fragmented smallholder structures temper growth prospects. Companies respond by widening hybrid portfolios, tightening quality control, and forging research pacts with global institutes to tailor high-performing seeds for domestic ecologies and strict export specifications.

Key Report Takeaways

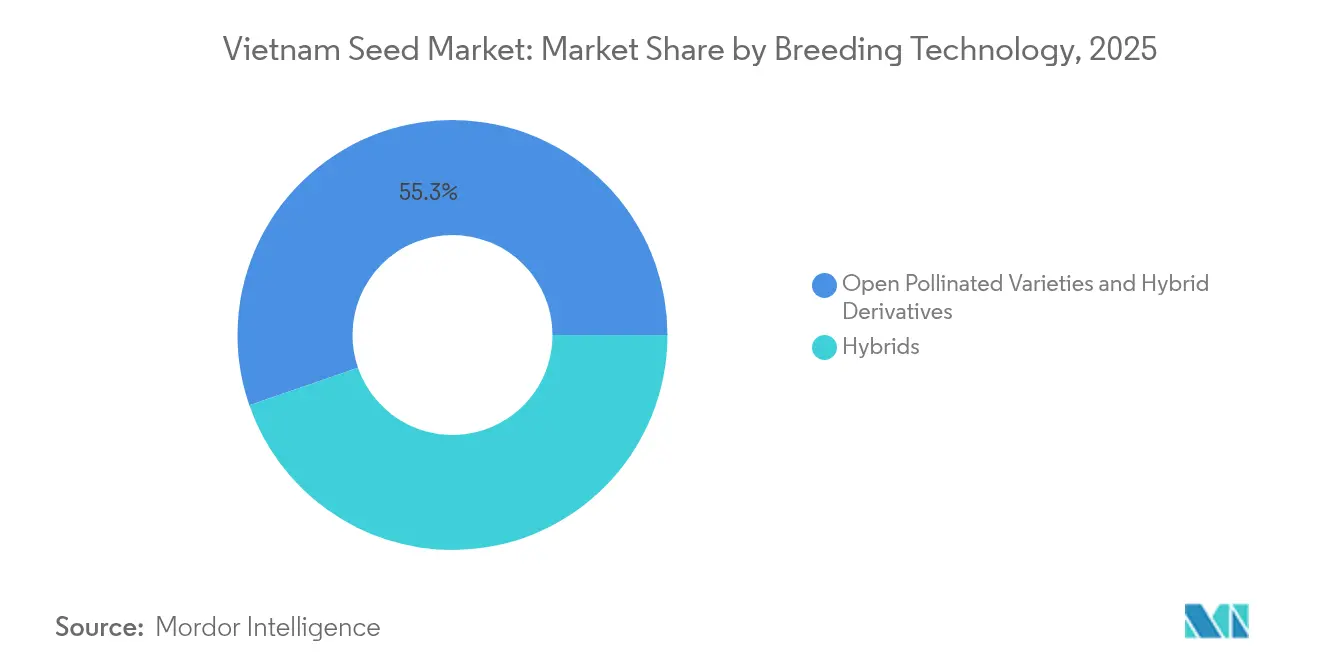

- By breeding technology, open-pollinated varieties and hybrid derivatives held 55.30% of the Vietnam seed market share in 2025, while hybrid seeds are projected to expand at a 4.38% CAGR through 2031.

- By cultivation mechanism, open-field production accounted for 99.86% of the Vietnam seed market size in 2025, and protected cultivation is advancing at a 12.55% CAGR to 2031.

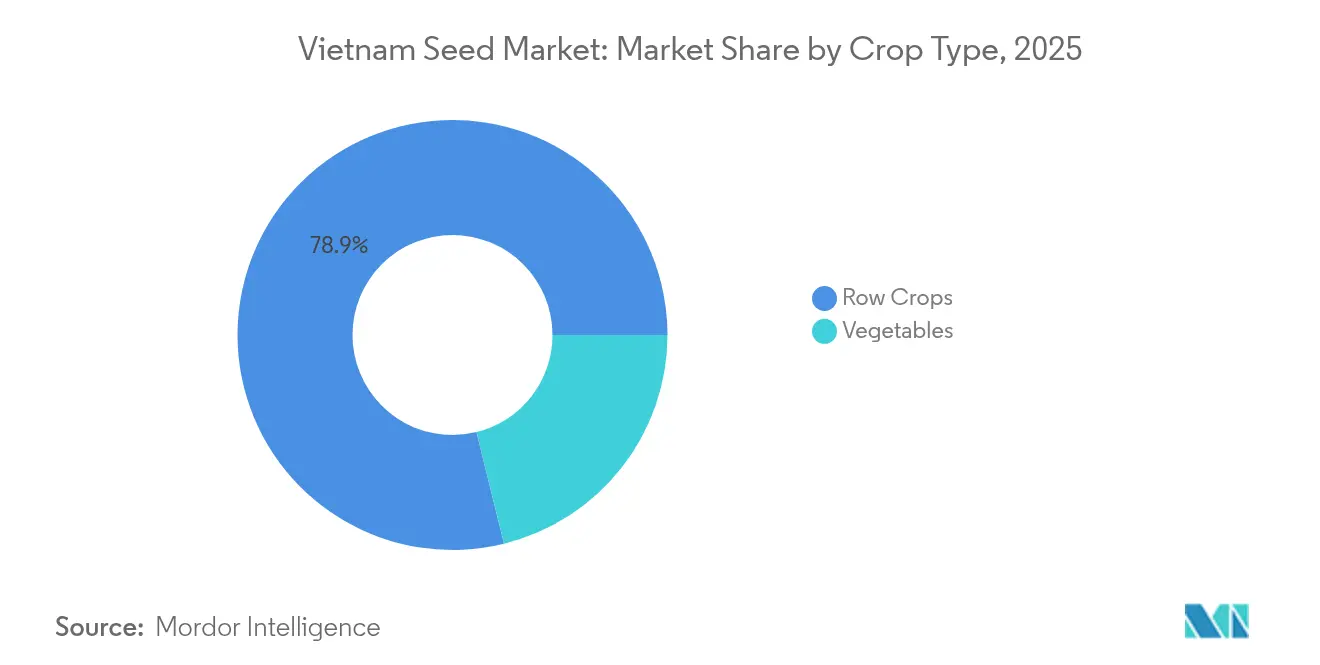

- By crop type, row crops contributed 78.85% share of the Vietnam seed market size in 2025, while vegetables are moving at a 6.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Seed Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for certified seeds | +1.2% | Mekong Delta and Red River Delta | Medium term (2-4 years) |

| Export-led demand growth for vegetables and rice | +1.8% | Southern rice belt and northern vegetable zones | Long term (≥ 4 years) |

| Hybrid and GM seed adoption for yield gains | +1.1% | Commercial farming clusters | Long term (≥ 4 years) |

| Expansion of protected cultivation acreage | +0.9% | Northern peri-urban areas | Medium term (2-4 years) |

| Foreign equity inflows after seed-sector liberalization | +0.8% | Ho Chi Minh City and Hanoi | Short term (≤ 2 years) |

| Climate-resilient rice varieties for Mekong Delta salinity | +1.4% | Mekong Delta | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Certified Seeds

Targeted incentives under Decision 2151/QĐ-BNN-VP and the “One Million Hectares” low-emission rice program reimburse part of seed costs and fund traceability platforms that enhance farmer trust in certified lots.[2]Source: Vietnam Agriculture News Desk, “Building digital data for rice production management,” Vietnamagriculture.nongnghiep.vn Subsidies cover up to 50% of premium seed prices for smallholders, lifting certified seed penetration in northern provinces above 70% while the Mekong Delta still trails near 40%. Digital tagging via quick response codes lets inspectors verify origin and germination data in real time, reducing loopholes that once enabled counterfeit trade. Vinaseed cites 45% higher farmer incomes from protected rice varieties compared with conventional lines, reinforcing willingness to purchase newer seeds.

Export-led Demand Growth for Vegetables and Rice

Agricultural exports generated USD 62.5 billion in 2024, including a historical 9 million metric tons rice shipment that motivates seed selection for milling yield, uniformity, and residue compliance.[3]Source: The PAN Group Communications Office, “Enterprises and scientists join forces to take Vietnamese crop varieties global,” Thepangroup.vn Vegetable seed orders soar for tomato, cucumber, and sweet pepper hybrids suited to climate-controlled tunnels that guarantee consistent color and size demanded by supermarkets in Japan and the European Union. Upcoming EU Deforestation Regulation further nudges exporters toward traceable seed sources that enable end-to-end carbon reporting.

Hybrid and GM Seed Adoption for Yield Gains

Hybrid rice and maize deliver 30-60% yield uplift over landraces, modern F1 rice now matures in 110 days and produces up to 10 metric tons per hectare, triple older cultivars. Gene-editing using clustered regularly interspaced short palindromic repeats (CRISPR) and homology-directed repair (HDR) cuts breeding cycles and introduces salt-tolerance without foreign DNA, aligning with consumer acceptance. Regulatory draft Circular 03/2025/TT-BNNMT outlines fast-track dossiers for gene-edited seed evaluation, easing commercialization by 2027.

Expansion of Protected Cultivation Acreage

Greenhouse acreage climbs 12.7% each year, concentrating near Hanoi, Hai Phong, and Da Lat, where land scarcity and high produce prices justify capital-intensive hydroponics. Farmers cite 20% pesticide reduction and 25% profit gain inside passive-ventilated polyhouses equipped with Internet of Things (IoT) sensors that monitor humidity, nutrient solution, and canopy temperature. Seeds for protected systems emphasize short internodes, virus resistance, and predictable fruit set.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit seeds and informal distribution networks | −0.8% | Remote rural districts | Long term (≥ 4 years) |

| High R&D cost and GMO approval delays | −0.6% | National | Medium term (2-4 years) |

| Farmer reliance on farm-saved seeds in upland areas | −0.9% | Northern mountains and Central Highlands | Long term (≥ 4 years) |

| Poor cold-chain logistics for vegetable seeds | −0.4% | Southern provinces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit Seeds and Informal Distribution Networks

Unofficial trading channels distribute mislabeled paddy and maize seeds, often with germination rates falling significantly below acceptable standards, which undermines farmer confidence and reduces the likelihood of repeat purchases. While blockchain tagging pilots have shown potential to address these issues by ensuring traceability and authenticity, their success largely depends on the widespread adoption of smartphones among farmers and the willingness of dealers to comply with the new system.

High R&D Cost and GMO Approval Delays

ThaiBinh Seed outlay to commercialize a single variety, tying up capital in long test cycles that include extensive field trials and regulatory approvals. GMO dossiers further complicate the process by adding biosafety trials, public consultations, and compliance requirements, which significantly extend timelines and stretch returns, making it challenging for smaller firms to compete effectively in the market. As a result, the commercialization process becomes resource-intensive and time-consuming. This highlights the need for streamlined procedures to support smaller firms in navigating these challenges effectively.

Segment Analysis

By Breeding Technology: Hybrid Seeds Advance Yield and Consistency

Open-pollinated varieties and hybrid derivatives held 55.30% of the Vietnam seed market share in 2025, while hybrid seeds are projected to expand at a 4.38% CAGR through 2031, signaling a gradual pivot away from traditional open-pollinated cultivars. The Vietnam seed market size for hybrids is poised to scale alongside rising export quality thresholds. Rice hybrids with cytoplasmic male sterility and two-line systems gain traction due to labor savings in seed multiplication, while triple-stacked corn hybrids integrate insect resistance and herbicide tolerance traits suited for mechanized Red River Delta farms.

Breeders leverage doubled haploid acceleration and genomic selection to trim development time from eight seasons to four, allowing quicker response to climate shocks. Vinaseed targets a 37% gross profit contribution from hybrid rice, corn, and vegetable seeds by 2027, aided by BAAS (Banking as a Service) germplasm exchange. Meanwhile, non-transgenic hybrids dominate adoption because they slot into existing regulatory pathways and consumer acceptance thresholds, yet precision-bred gene-edited variants are queued for release once biosafety guidelines clarify commercialization routes.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Cultivation Mechanism: Protected Cultivation Generates Premium Demand

Open-field systems still generate 99.86% revenue for the Vietnam seed market size, but the tiny protected cultivation slice grows fastest at 12.55% CAGR. Polycarbonate houses of 1,000-3,000 square meters near Hanoi and Ho Chi Minh City allow farmers to rotate tomato, cucumber, and commercial chrysanthemum using drip fertigation and ultraviolet-blocking films that extend seed vigor.

Protected cultivation requires high-germination lots (>95%), uniform emergence, and determinate architecture that simplifies trellising. Seed houses now offer pre-coated capsules with micronutrients and polymer film that extends shelf life under 25 °C for six months, mitigating Vietnam’s humid logistics chain. IoT-based climate control helps collect crop performance data, which feeds back to breeders to refine next-generation cultivars. Open-field remains essential for rice and maize, employing broadcast sowing and direct seeding machinery introduced under mechanization subsidies.

By Crop Type: Vegetables Outpace Staple-Crop Growth

Row crops, rice, corn, soybean, commanded 78.85% share of the Vietnam seed market in 2025, but vegetable seeds are growing at 6.62% CAGR through 2031. Consumer income gains and urban supermarkets push year-round demand for fresh produce with traceability stamps. Protected tomato F1 hybrids deliver 10% yield gain and 18-day shelf life that meets Japanese import standards.

Fiber and forage seeds rest at low bases yet attract dairy and textile investors searching for domestic feed and cotton sources. Official registries list 455 rice and 206 corn varieties, but only 52 vegetable entries hold Plant Variety Protection, hinting at room for proprietary breed expansion. Export-minded cooperatives in Lam Dong and Quang Nam run contract seed production for European firms, adding royalty revenues to rural economies.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Vietnam’s seed demand clusters around region-specific crop portfolios. The Mekong Delta supports 1.77 million hectares of irrigated rice that absorbs 54% of certified paddy seeds, including salt-tolerant lines with sub-1.5 parts-per-thousand yield drop. Red River Delta provinces plant two rice crops and a winter maize, requiring short-duration seeds to slot between harvest windows. Northern mountain zones prefer sticky rice and temperate vegetables, yet rely heavily on farm-saved lots due to market distance and varied microclimates.

Protected cultivation centers in Ha Nam, Hai Duong, and Da Lat, where altitude and cool nights suit high-value lettuce and strawberries. Ho Chi Minh City acts as the largest distribution hub, funneling imported vegetable seeds from the Netherlands and Japan via bonded warehouses and repack centers. Cross-border seed flow with Cambodia and Laos enlarges the regional market size, supported by ASEAN (Association of Southeast Asian Nations) trade facilitation and harmonized phytosanitary certificates.

Government policy implementation reflects regional priorities: the Mekong Delta receives digital extension tablets under RiceMoRe, northern provinces secure greenhouse subsidies. Central Highlands secures coffee seed research grants. Logistics upgrades, four-lane expressways and cold storage at seaports, enhance seed throughput to both farmgate and export docks.

Competitive Landscape

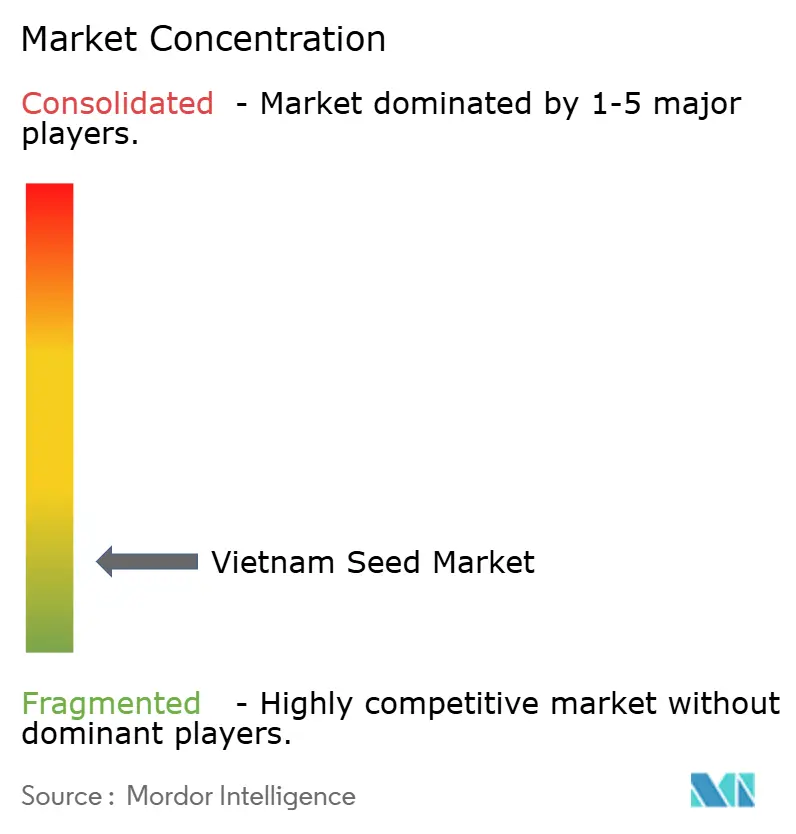

The Vietnam seed market is characterized by a low level of concentration, as the top five companies collectively account for only a small portion of the overall market share. Vietnam National Seed Group (Vinaseed) stands as the leading domestic player in the market, with an annual processing capacity of 75,000 metric tons distributed across 13 processing plants. The company's product portfolio encompasses a diverse range of seeds, including rice, corn, and vegetables.

PAN Group participates in the seed market through its vertically integrated grain business, leveraging its operational structure to supply seeds. ThaiBinh Seed focuses on the production and distribution of premium rice seeds and holds an estimated 20% share of the rice segment. Foreign companies, including Enza Zaden, Known-You Seed, Bayer, and Groupe Limagrain, actively compete in the market by offering advanced products such as protected vegetable hybrids and corn trait stacks.

Strategic moves in 2024–2025 include Vinaseed’s memorandum with the Mekong Delta Rice Research Institute to co-develop shorter-duration aromatic varieties, and PAN Group’s technology swap with the Vietnam Academy of Agricultural Sciences to fast-track field phenotyping. Digital transformation is underway as firms roll out dealer apps that display live germination tests, expiry alerts, and loyalty coupons, aiming to counteract counterfeit trade.

Vietnam Seed Industry Leaders

Bayer AG

Enza Zaden

Groupe Limagrain

Known You Seed Co. Ltd

Vietnam National Seed Group (VINASEED)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Agroviet 2025, Vietnam’s premier agricultural trade fair, will be held in Hanoi next week (November 12-16), showcasing innovations in farming, seeds, and agri-tech. The event aims to promote domestic agricultural products and foster international cooperation in the sector.

- October 2025: Vietnam will supply rice seeds to Cuba for its 2026 crop, strengthening agricultural cooperation between the two countries. This agreement reflects Vietnam’s growing role in the international seed trade and support for food security initiatives in allied nations.

- June 2025: Vinaseed has expanded its international partnerships in plant breeding to enhance seed quality and agricultural innovation. The collaboration aims to integrate advanced global technologies into Vietnam’s crop development programs.

Vietnam Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Open Field, Protected Cultivation are covered as segments by Cultivation Mechanism. Row Crops, Vegetables are covered as segments by Crop Type.Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Insect Resistant Hybrids | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

Cultivation Mechanism

| Open Field |

| Protected Cultivation |

Crop Type

| Row Crops | Fiber Crops | Cotton |

| Other Fiber Crops | ||

| Forage Crops | Alfalfa | |

| Forage Corn | ||

| Other Forage Crops | ||

| Grains and Cereals | Corn | |

| Rice | ||

| Other Grains and Cereals | ||

| Oilseeds | Canola, Rapeseed and Mustard | |

| Soybean | ||

| Other Oilseeds | ||

| Pulses | ||

| Vegetables | Brassicas | Cabbage |

| Carrot | ||

| Cauliflower and Broccoli | ||

| Other Brassicas | ||

| Cucurbits | Cucumber and Gherkin | |

| Pumpkin and Squash | ||

| Other Cucurbits | ||

| Roots and Bulbs | Garlic | |

| Onion | ||

| Potato | ||

| Other Roots and Bulbs | ||

| Solanaceae | Chilli | |

| Eggplant | ||

| Tomato | ||

| Other Solanaceae | ||

| Unclassified Vegetables | Asparagus | |

| Spinach | ||

| Other Unclassified Vegetables | ||

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Insect Resistant Hybrids | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Cultivation Mechanism | Open Field | ||

| Protected Cultivation | |||

| Crop Type | Row Crops | Fiber Crops | Cotton |

| Other Fiber Crops | |||

| Forage Crops | Alfalfa | ||

| Forage Corn | |||

| Other Forage Crops | |||

| Grains and Cereals | Corn | ||

| Rice | |||

| Other Grains and Cereals | |||

| Oilseeds | Canola, Rapeseed and Mustard | ||

| Soybean | |||

| Other Oilseeds | |||

| Pulses | |||

| Vegetables | Brassicas | Cabbage | |

| Carrot | |||

| Cauliflower and Broccoli | |||

| Other Brassicas | |||

| Cucurbits | Cucumber and Gherkin | ||

| Pumpkin and Squash | |||

| Other Cucurbits | |||

| Roots and Bulbs | Garlic | ||

| Onion | |||

| Potato | |||

| Other Roots and Bulbs | |||

| Solanaceae | Chilli | ||

| Eggplant | |||

| Tomato | |||

| Other Solanaceae | |||

| Unclassified Vegetables | Asparagus | ||

| Spinach | |||

| Other Unclassified Vegetables | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms

Get More Details On Research Methodology

Download PDF