Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.86 Billion |

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.11 Billion |

| Growth Rate (2026 - 2031) | 2.13% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Rice Seed Market Analysis by Mordor Intelligence

The China rice seed market size is expected to grow from USD 1.86 billion in 2025 to USD 1.9 billion in 2026 and is forecast to reach USD 2.11 billion by 2031 at 2.13% CAGR over 2026-2031. Demand is shifting from volume to value as growers balance government incentives with input-cost discipline. Hybrid adoption remains the primary growth engine, mechanization is lifting per-mu seed usage, and climate resilience traits are opening premium sub-segments. Counterfeit circulation, lingering hybrid inventory, and muted paddy prices temper momentum, but rising public–private R&D collaboration keeps the innovation pipeline active. Fragmented competition, coupled with stricter enforcement of variety protection, paves the way for consolidation and technology-driven differentiation. These forces collectively shape the medium-term trajectory of the China rice seed market.

Key Report Takeaways

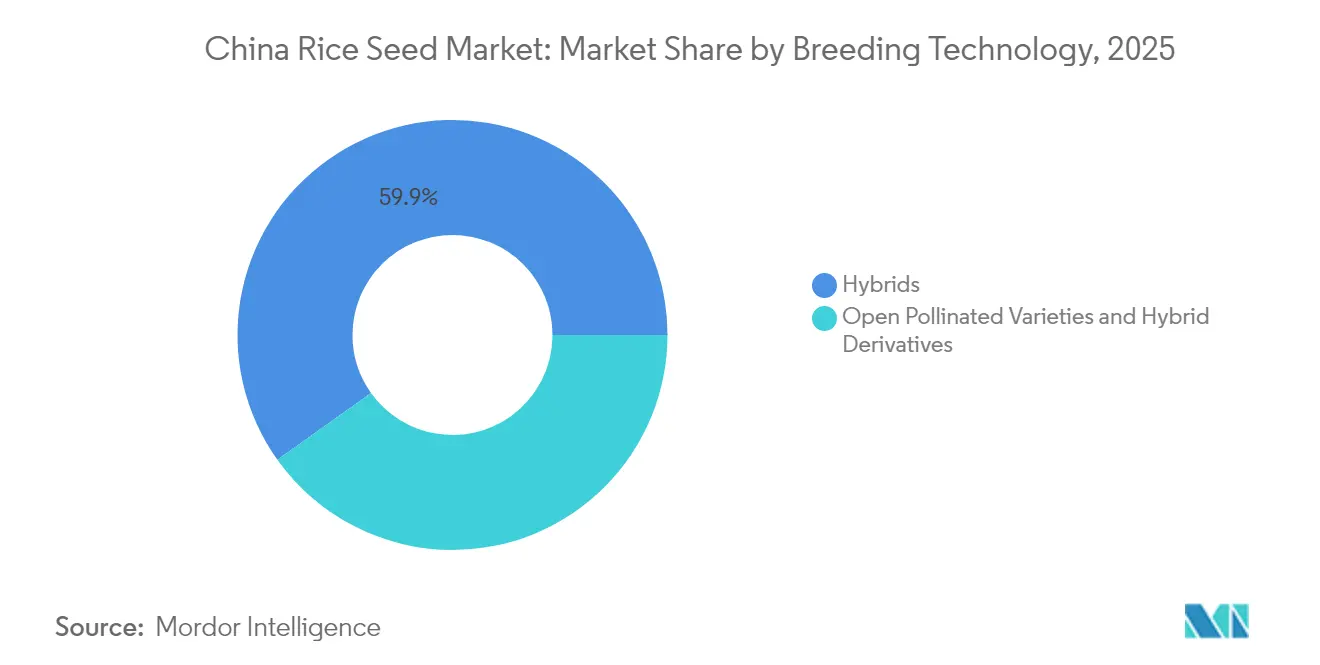

- By breeding technology, hybrids accounted for 59.85% of China rice seed market share in 2025 and are forecasted to expand at a 2.14% CAGR through 2031.

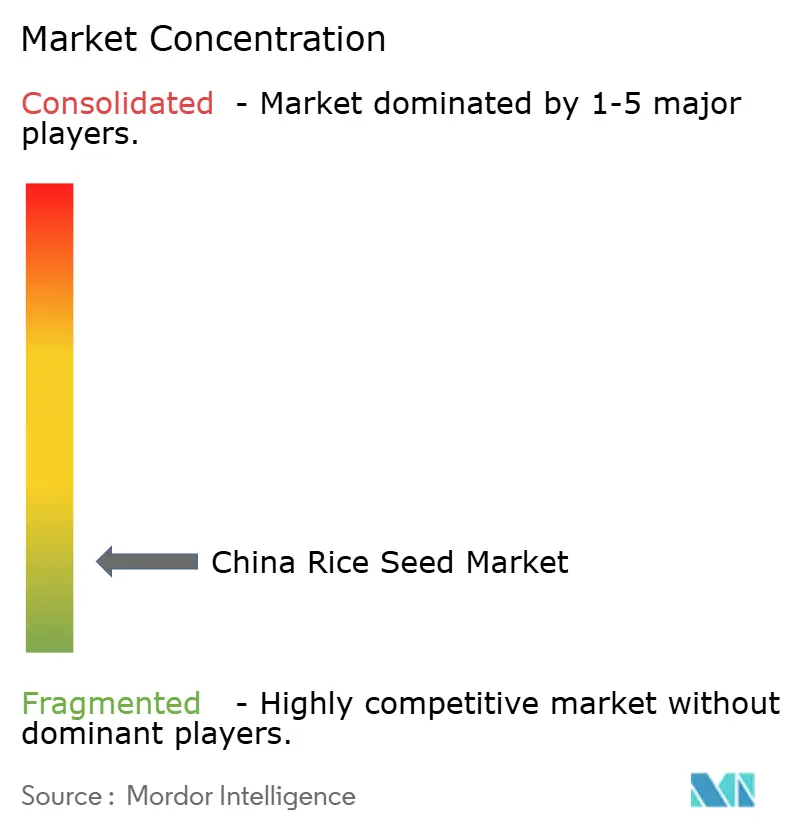

- The China rice seed market remains fragmented, with the top five companies collectively holding nearly 24% market share. The major players include Yuan Longping High-Tech Agriculture, Zhongnongfa Seed Industry Group, Anhui Tsuen Yin Hi-Tech Seed Industry Co. Ltd., Beidahuang Kenfeng Seed Co. Ltd., and Hefei Fengle Seed Industry Co. Ltd.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Rice Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing hybrid-rice acreage in central and southern provinces | +0.4% | Hunan, Jiangxi, Guangdong, and Sichuan | Medium term (2-4 years) |

| Government “Seed Industry Revitalization” subsidies for quality seed adoption | +0.3% | National focus in major rice regions | Short term (≤ 2 years) |

| Rapid mechanized transplanting raises per-mu seed usage rates | +0.2% | Central and southern provinces | Medium term (2-4 years) |

| Climate-change driven demand for drought- and heat-tolerant cultivars | +0.3% | National, water-stressed areas | Long term (≥ 4 years) |

| Rise of direct-seeded rice and coated seed technologies | +0.2% | Jiangsu, Zhejiang, expanding elsewhere | Medium term (2-4 years) |

| Private–public genomic platforms lowering breeding cycle time | +0.1% | National R&D hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing hybrid-rice acreage in central and southern provinces

Mechanization rates of 85.2% in Hunan and 82.1% in Jiangxi align with provincial subsidies that narrow price gaps between premium and conventional cultivars.[1]Source: Hunan Provincial Agricultural Department, “Rice Production Mechanization Report 2024,” nyt.hunan.gov.cn Uniform seedling traits preferred by transplanters reinforce hybrid appeal, while rising farm scale makes higher seed replacement financially viable. As Guangdong upgrades its field infrastructure, similar hybrid-mechanization collaborations are expected to accelerate. The resulting lift in per-mu usage feeds directly into volume growth for leading suppliers.

Government “Seed Industry Revitalization” subsidies for quality seed adoption

The 2024 No. 1 Central Document expanded certified-seed subsidies, covering testing fees and traceability labels.[2]Source: Ministry of Agriculture and Rural Affairs, “Seed Industry Policy Guidelines 2024,” moa.gov.cn Provincial add-ons in Sichuan and Hubei further stack incentives, trimming farmer out-of-pocket premiums by up to 30%. Mandatory certification displaces informal trade and nudges breeders toward higher-value traits, reinforcing the hybrid growth cycle within the China rice seed market. The subsidy structure particularly benefits hybrid seed adoption, as government programs prioritize varieties with documented yield advantages and quality certifications.

Rapid mechanized transplanting raises per-mu seed usage rates

Machine transplanting consumes 25–30 kg of seed per hectare compared with 15–20 kg under hand methods.[3]Source: China Agricultural Mechanization Association, “Mechanization Impact Study 2024,” came.org.cn The 40–50% volume lift magnifies seed demand even in flat acreage scenarios. Uniform spacing requirements amplify the need for treated, high-germination lots, favoring companies with robust quality-control systems and reinforcing market differentiation. Regional mechanization rates vary dramatically: northeastern provinces exceed 90% adoption while southern regions lag at 60-70%, indicating a substantial growth runway as infrastructure investment continues.

Climate-change driven demand for drought- and heat-tolerant cultivars

Twelve drought-tolerant lines released in 2024 delivered 15–20% yield gains under water stress. Yuan Longping High-Tech Agriculture allocated 18% of R&D outlays to climate adaptation, banking on expedited approvals that now take 2–3 years instead of 5 years. Premium pricing for stress-tolerant hybrids offsets slower acreage growth, sustaining revenue momentum in the china rice seed market. The regulatory framework supports this trend through expedited variety approval processes for climate-resilient traits, reducing time-to-market from 4-5 years to 2-3 years for qualifying varieties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent counterfeit seed circulation in informal channels | −0.3% | Remote rural areas nationwide | Short term (≤ 2 years) |

| Excess hybrid-seed inventories | −0.2% | Major production regions | Short term (≤ 2 years) |

| Farmer price resistance amid flattened paddy prices | −0.2% | Price-sensitive provinces | Medium term (2-4 years) |

| Regulatory uncertainty for commercial GM rice traits | −0.1% | National, R&D investment decisions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent counterfeit seed circulation in informal channels

In 2024, authorities prosecuted 847 violations and recovered RMB 156 million (USD 22 million) in damages, yet enforcement gaps persist. Counterfeiters target high-margin hybrids, mimicking packaging to bypass wary buyers. Erosion of brand trust and lower re-purchase rates drag on legitimate sales, trimming near-term growth for the china rice seed market. Rural distribution networks in remote areas remain vulnerable to counterfeit infiltration due to limited regulatory oversight and farmer price sensitivity. The problem intensifies during peak planting seasons when supply shortages create opportunities for counterfeit substitution.

Excess hybrid-seed inventories

Hybrid production hit 310 million kg in 2024 against demand ratios of 125%, pushing turnover to 12–15 months. Discounting to clear stock squeezes margins, disproportionately hurting smaller firms without diversified pipelines. The destocking phase particularly affects premium hybrid varieties where production volumes exceeded adoption rates, forcing companies to offer volume discounts that compress margins. Industry consolidation may accelerate as smaller producers struggle with inventory carrying costs and reduced cash flow during this adjustment period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrid Adoption Outpaces OPVs

Advanced breeding techniques position hybrids to capture 59.85% market share in 2025, expanding at 2.14% CAGR through 2031 as mechanization adoption creates structural demand advantages. Non-transgenic hybrids dominate current market dynamics, benefiting from established regulatory pathways and farmer acceptance, while transgenic hybrids await commercial approval despite promising field trial results. Insect-resistant hybrid development accelerates through public-private partnerships, with the Chinese Academy of Agricultural Sciences collaborating with Yuan Longping High-Tech Agriculture on Bt-trait integration projects. Open-pollinated varieties and hybrid derivatives maintain relevance in northeastern provinces where Beidahuang Kenfeng leverages government farm relationships to sustain market position.

The breeding technology landscape reflects China's agricultural modernization trajectory, where hybrid adoption correlates directly with mechanization rates and farm scale expansion. Provincial variation remains significant: Hunan achieves 78% hybrid adoption while Heilongjiang maintains 65% open-pollinated variety usage, indicating regional optimization strategies based on local conditions and farmer preferences. Genomic selection platforms reduce breeding cycle times from 8-10 years to 5-6 years, enabling faster trait integration and variety development responses to market demands. The Ministry of Agriculture and Rural Affairs streamlined variety approval processes for climate-resilient traits, creating regulatory advantages for breeding companies investing in stress-tolerance research and development programs.

Geography Analysis

Central and southern provinces jointly generate the largest portion of the China rice seed market, propelled by mechanization rates above 80% and layered subsidies that compress payback periods for certified hybrids. Jiangxi growers, for example, recoup premium seed costs within one cycle due to 8% yield lifts, reinforcing hybrid loyalty.

Northeastern provinces display a contrasting profile. Large contiguous farms in Heilongjiang and Jilin favor OPVs tailored to cooler climates. Beidahuang Kenfeng leverages vertically integrated operations to supply OPVs at scale, protecting share despite hybrid encroachment. Provincial policies prioritize grain security, channeling research funds into cold-tolerant genomic lines.

The south coast, notably Guangdong and Hainan, acts as a regulatory sandbox for new traits. Warm climates allow three crop cycles per year, accelerating field trials. Syngenta’s Hainan innovation center exploits this advantage, shortening breeding feedback loops. Climate-driven demand stratifies the market: drought-prone inland basins shift toward water-saving hybrids, while flood-susceptible delta zones seek submergence-tolerant OPVs. Such micro-segmentation sustains diversified growth across the China rice seed market.

Competitive Landscape

The China rice seed market remains fragmented, with the top five players holding around 24% combined share. Yuan Longping High-Tech Agriculture leads the market, leveraging nationwide extension teams and a deep hybrid portfolio. Zhongnongfa Seed Industry Group excels in dealer-centric distribution.

Global firms operate through technology licensing rather than direct marketing. Syngenta partners with provincial institutes to co-develop hybrids, avoiding the regulatory hurdles of foreign seed importation. Bayer channels CRISPR know-how into joint ventures, betting on eventual GM trait approvals.

Intellectual-property enforcement is tightening. Variety-protection lawsuits rose 18% in 2024, favoring companies with strong patent arsenals. Smaller regional firms, facing rising compliance costs and R&D demands, have become acquisition targets; Beidahuang Kenfeng’s 2024 buyout spree in Jilin and Liaoning exemplifies the consolidation trend. Climate-resilient traits and direct-seeding compatibility represent the next battlegrounds for differentiation within the China rice seed market.

China Rice Seed Industry Leaders

Yuan Longping High-Tech Agriculture Co. Ltd (CITIC Agriculture)

Hefei Fengle Seed Industry Co. Ltd

Beidahuang Kenfeng Seed Co. Ltd

Zhongnongfa Seed Industry Group Co. Ltd

Anhui Tsuen Yin Hi-Tech Seed Industry Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The South Asia & Southeast Asia Rice Molecular Design Breeding Network was officially launched in Kunming (Yunnan), aiming to leverage China’s breeding technologies and regional genetic resources to develop new rice varieties that are climate-resilient and suited to upland and marginal environments.

- December 2024: The Ministry of Agriculture and Rural Affairs approved 17 genetically modified crop varieties, including multiple gene-edited rice cultivars, marking the largest such approval to date.

- June 2024: Chinese scientists identified a gene that enables the mechanical production of hybrid rice seeds, marking the first successful automation of this process. This development has the potential to reduce manual labor requirements in rice farming operations while increasing seed production efficiency.

China Rice Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology.Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Insect Resistant Hybrids | |

| Open Pollinated Varieties & Hybrid Derivatives | ||

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Insect Resistant Hybrids | ||

| Open Pollinated Varieties & Hybrid Derivatives | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms