Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

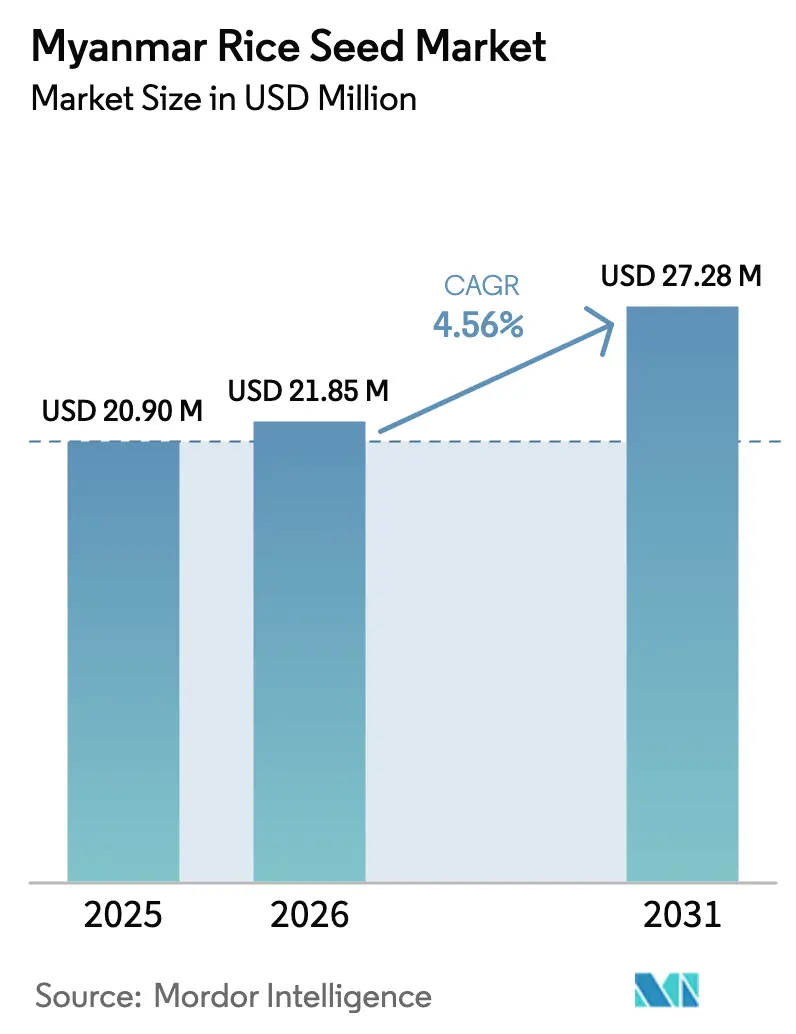

| Base Year Market Size (2025) | USD 20.90 Million |

| Market Size (2026) | USD 21.85 Million |

| Market Size (2031) | USD 27.28 Million |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Myanmar Rice Seed Market Analysis by Mordor Intelligence

Myanmar rice seed market size in 2026 is estimated at USD 21.85 million, growing from 2025 value of USD 20.90 million with 2031 projections showing USD 27.28 million, growing at 4.56% CAGR over 2026-2031. The expansion reflects steady demand for certified seed, a gradual pivot toward hybrid varieties, and state-led programs that favor quality-assured planting material. Rising farm-gate paddy prices, the spread of digital input-commerce tools, and donor-backed seed-system projects add further momentum. Yet political turbulence, fuel shortages, and the dominance of farmer-saved seed temper growth prospects. Multinational and domestic suppliers continue to test go-to-market models that blend traditional dealer networks with smartphone apps, while upstream breeding programs benefit from fresh genomic resources and streamlined import permitting.

Key Report Takeaways

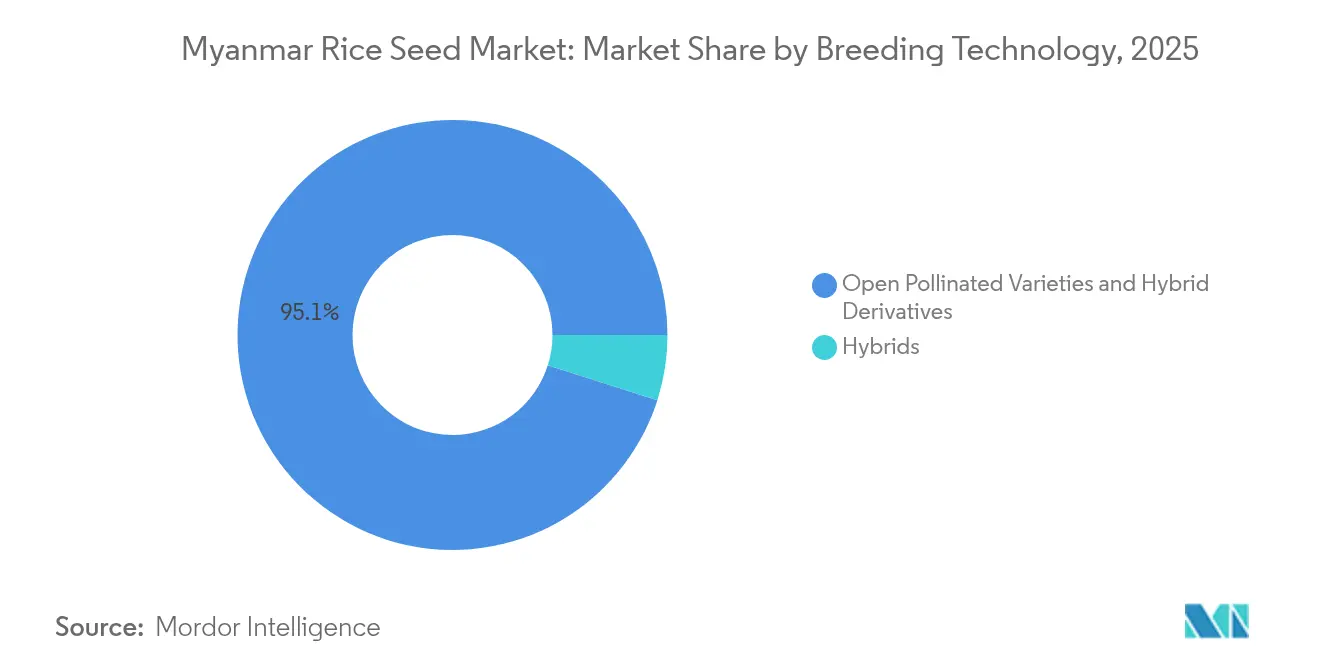

- By breeding technology, open-pollinated varieties and hybrid derivatives held 95.10% of the Myanmar rice seed market share in 2025; hybrids are projected to register the fastest 4.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Myanmar Rice Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government initiatives to scale certified seed production | +1.2% | National, with early gains in Naypyitaw and Yangon regions | Medium term (2-4 years) |

| Rising adoption of hybrid rice for yield gains | +0.8% | Ayeyarwady, Bago and Sagaing core regions | Long term (≥ 4 years) |

| International donor-funded seed-system projects | +0.6% | National, concentrated in rural development zones | Medium term (2-4 years) |

| Higher farm-gate paddy prices stimulating improved-seed demand | +0.5% | National, strongest in export-oriented regions | Short term (≤ 2 years) |

| Digital seed-trading platforms expanding rural access | +0.4% | National, accelerated in connected townships | Short term (≤ 2 years) |

| Contract-farming models offering input credit for quality seed | +0.3% | Regional, focused near processing facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Initiatives to Scale Certified Seed Production

In 2025, the Department of Agriculture accelerated seed-law reform and launched a fast-track import-permit window that clears planting-material certificates within three working days. The National Economic Promotion Fund is allocated for agricultural modernization, with seed sector development receiving priority attention[1]Source: Myanmar National Trade Portal, “Import Certificate (IC) for Plants and Plant Products,” myanmartradeportal.gov.mm. Prompting regional governments to co-finance cold-storage and seed-testing labs. Parallel registration mandates under the Myanmar Rice Online platform have improved traceability across 726 large warehouses, creating a transparent backbone for certified-seed distribution. These measures reduce transaction risk for private breeders and raise farmer confidence in formally labeled seed.

Rising Adoption of Hybrid Rice for Yield Gains

Recent evidence from Lewe Township showed certified seed adopters achieving 4.05 metric tons per hectare compared to 3.37 metric tons for non-adopters, with returns above total variable cost reaching USD 428 versus USD 136, respectively[2]Source: Asian-Pacific Forest Technology Center, “Knowledge and attitude of farmers towards adoption of certified rice seeds in Lewe Township,” ap.fftc.org.tw. Such performance data underpin farmer workshops organized by IRRI (International Rice Research Institute) and the Myanmar Rice Federation, while private breeders deploy demonstration plots bundled with buy-back guarantees. Genomic resource releases in 2024 now allow local breeders to shorten selection cycles and tailor hybrids to Myanmar’s delta ecology. As seed costs fall and yield premiums stabilize, adoption is projected to rise most quickly in irrigated pockets of Ayeyarwady.

International Donor-Funded Seed-System Projects

International development support has catalyzed seed system modernization through targeted capacity building and technology transfer initiatives. The Global Innovation Fund's grant to Proximity Designs in September 2024 supports "No-Burn Rice Farming" solutions that integrate improved seed varieties with sustainable agricultural practices, targeting 46,000 rice farmers[3]Source: Global Innovation Fund, “GIF makes its first investment in Myanmar,” globalinnovation.fund. United States Agency for International Development (USAID) Feed the Future initiatives and IFDC's Fertilizer Sector Improvement project have enhanced input supply chains that support certified seed adoption. These interventions address systemic constraints, including limited access to early-generation seed, inadequate storage facilities, and weak extension services that historically impeded seed system development.

Higher Farm-Gate Paddy Prices Stimulating Improved-Seed Demand

In 2024, farm-gate paddy prices climbed compared with 2023 levels, widening margins for growers who adopt productivity-enhancing inputs. Certified seed users captured a USD 48 premium per metric ton over conventional grain, reinforcing the economic case for annual seed purchase. The Myanmar Rice Federation’s strategic reserve, targeting 1 million bags of premium Pawsan rice, underscores rising commercial interest in premium varietal identity and quality assurance. Price signals, therefore, intersect with policy support to nudge farmers toward formal seed channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dominance of farmer-saved seed and informal channels | -1.1% | National, strongest in remote rural areas | Long term (≥ 4 years) |

| Political instability disrupting input logistics | -0.9% | National, concentrated in conflict-affected townships | Short term (≤ 2 years) |

| Chronic fuel shortages hampering mechanized seed production | -0.6% | National, severe in mechanization-dependent regions | Medium term (2-4 years) |

| Coastal soil salinity limiting varietal performance | -0.4% | Coastal regions, Ayeyarwady Delta, Tanintharyi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dominance of Farmer-Saved Seed and Informal Channels

Approximately 94% of Myanmar rice growers still source first seed from neighbors or grain harvests, reflecting long-standing social trust networks and limited purchasing power. Replacement cycles average nearly seven years, constraining genetic improvement and disease tolerance. The informal system's resilience stems from its accessibility, affordability, and social networks that provide quality assurance through farmer-to-farmer knowledge transfer. This dominance constrains genetic improvement and limits the introduction of disease-resistant or climate-adapted varieties essential for long-term productivity growth. Without intensified outreach, informal channels will continue to dampen the Myanmar rice seed market growth trajectory.

Political Instability Disrupting Input Logistics

Post-2021 unrest curtails mobility for extension staff and private distributors. Farmers in townships under martial law, representing 13% of all townships, use extension services significantly less due to internet access restrictions and mobility constraints. Input logistics face additional challenges from border checkpoint delays and transportation cost increases that particularly impact imported seed and breeding materials. The Myanmar Agricultural Inputs Registration System's implementation has been complicated by administrative capacity constraints and reduced coordination between central and regional authorities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

Open-pollinated varieties and hybrid derivatives commanded 95.10% of the Myanmar rice seed market size in 2025, mirroring entrenched farmer preferences for familiar cultivars that perform reliably under low-input management. Varieties such as Hnan Kar and Sin Thu Kha support mixed cropping and withstand erratic monsoon patterns. The large base of saved seed and granular local knowledge protects this segment’s volume, yet low seed turnover caps value capture for formal suppliers.

Hybrid seed, though representing only a small volume, posts the quickest expansion at a 4.95% CAGR. SL-series hybrids and the locally bred Pearl Thwe line deliver 15–20% yield improvements when combined with balanced nitrogen and timely drainage. Commercial acceptance hinges on annual repurchase and higher planting-material cost, yet field evidence of gross-margin gains drives uptake in irrigated delta tracts. As farmers integrate mechanical transplanters and higher fertilizer doses, hybrids can lift the Myanmar rice seed market size for the segment by 2031.

Geography Analysis

Myanmar's rice seed market exhibits significant regional variation driven by agroecological conditions, infrastructure development, and proximity to processing facilities. The Ayeyarwady region dominates rice production, with farmers deriving the majority of household income from rice, creating concentrated demand for seed improvements and productivity enhancements. This region's extensive irrigation infrastructure and favorable growing conditions make it the primary target for hybrid rice introduction and certified seed programs.

The Bago region presents diversified rotations where rice contributes a good share of farm income. Farmers allocate some dry-season land to pulses, motivating interest in short-duration rice varieties that free labor for alternative crops. Bago’s seed demand is forecast to grow annually, the fastest country-wide, aided by logistic corridors linking mills to Yangon port. Sagaing relies mainly on rain-fed systems; drought-tolerant open-pollinated seed remains the standard. Field days run by the Department of Agricultural Research highlight water-saving hybrids, yet limited irrigation constrains mass uptake. The region's remoteness and limited mechanization create additional barriers to seed access and adoption. Digital platform penetration varies significantly by region, with Green Way app coverage extending across 329 townships, but effectiveness is dependent on smartphone adoption and internet connectivity, which remains limited in remote areas.

Competitive Landscape

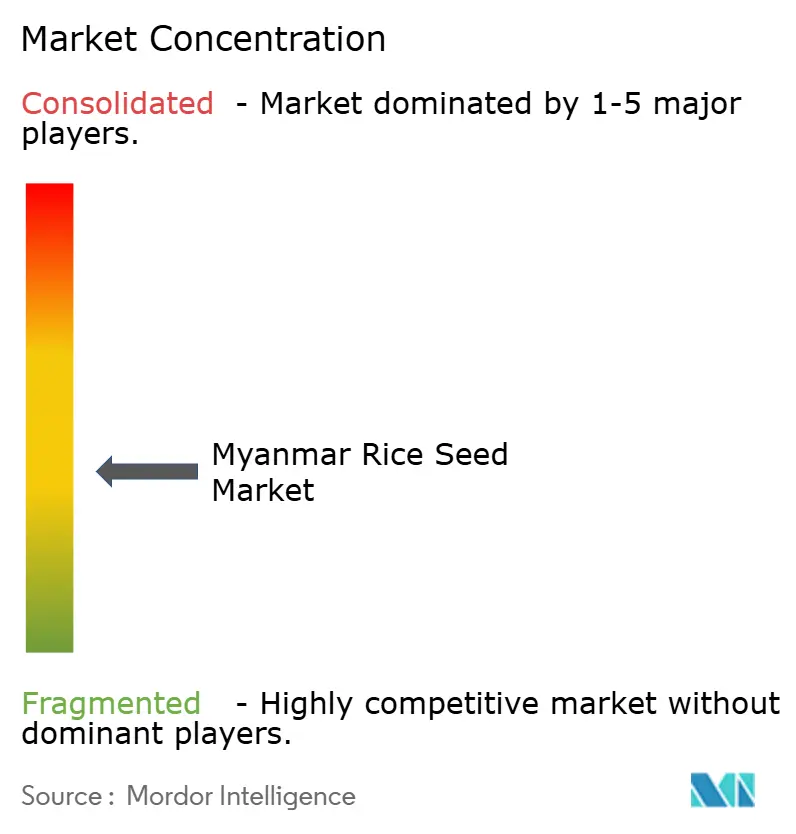

The Myanmar rice seed market remains moderately fragmented. The top five suppliers—Myanma Awba Group, SL Agritech Corporation (SLAC), Groupe Limagrain, Bayer AG, and Dagon Group of Companies collectively hold a good value share, while the rest is split among small domestic multipliers. Myanmar Agribusiness Public Corporation’s (MAPCO) integrated rice complex at Hinthada contracts growers on a seed-plus-mechanization package, boosting certified-seed use within its 20,000 ha catchment. Bayer and Syngenta operate through regional hubs in Bangkok, supplying foundation hybrid seed and conducting joint demonstration trials with the Ministry of Agriculture.

Corteva focuses on parental-line multiplication under greenhouse isolation to mitigate pollen contamination risks. Technology adoption represents a key competitive differentiator, with companies investing in digital tools, precision agriculture, and data analytics to enhance farmer engagement and service delivery. Myanma Awba Group's Htwet Toe digital platform achieved over 450,000 installations and resolved more than 40,000 farmer queries, demonstrating the potential for technology-enabled market expansion.

MAPCO's Integrated Rice Complex Project exemplifies vertical integration strategies that combine seed supply, mechanization services, processing, and marketing under unified management. The regulatory environment remains underdeveloped for genetically modified crops, with Myanmar lacking comprehensive biosafety legislation and GM food safety assessment capabilities, creating opportunities for companies focused on conventional breeding and hybrid development rather than biotechnology applications.

Myanmar Rice Seed Industry Leaders

Bayer AG

Dagon Group of Companies

Groupe Limagrain

Myanma Awba Group

SL Agritech Corporation (SLAC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: The Myanmar Rice Federation expanded strategic storage to 1 million bags of premium Pawsan rice to stabilize domestic prices and underpin quality-seed demand.

- March 2024: The Department of Agricultural Research published a genomic resource set covering under-utilized Myanmar germplasm to accelerate marker-assisted breeding.

Myanmar Rice Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology.Breeding Technology

| Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties & Hybrid Derivatives |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties & Hybrid Derivatives |

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms