Scandium Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2026 - 2031) | 14.53% CAGR |

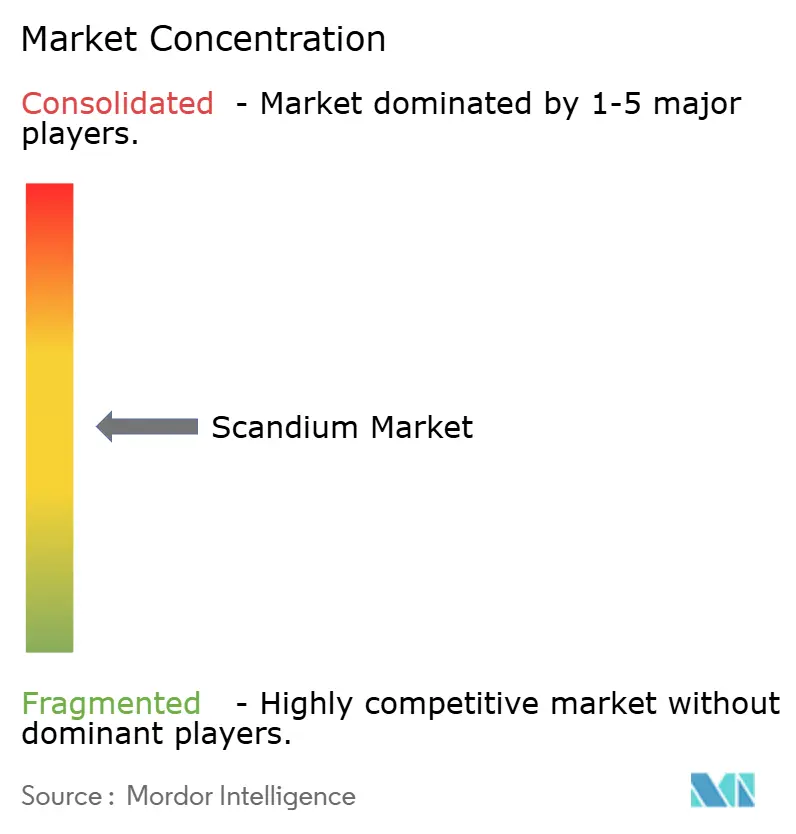

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scandium Market Analysis by Mordor Intelligence

The Scandium Market size is projected to be USD 0.89 billion in 2025, USD 1.02 billion in 2026, and reach USD 2.01 billion by 2031, growing at a CAGR of 14.53% from 2026 to 2031. Robust demand from solid-oxide fuel cells (SOFCs), aerospace lightweighting, and critical-mineral policy incentives is widening both civilian and defense use cases. A tightening supply base after China’s April 2025 export controls and October 2025 Foreign Direct Product Rule (FDPR) is forcing Western buyers to accelerate off-take agreements with non-Chinese suppliers, notably Rio Tinto in Canada and emerging mines in Australia and the United States. Vertically integrated strategies that capture oxide, master-alloy, and powder margins are raising capital efficiency, while industrial-symbiosis projects such as the EU-funded ScaVanger initiative promise secondary feedstocks at lower carbon intensity. Price volatility - USD 1,200 per kg for oxide versus up to USD 210,000 per kg for 99.99% metal—keeps the global market focused on premium applications where modest loading rates deliver high value-to-weight benefits.

Key Report Takeaways

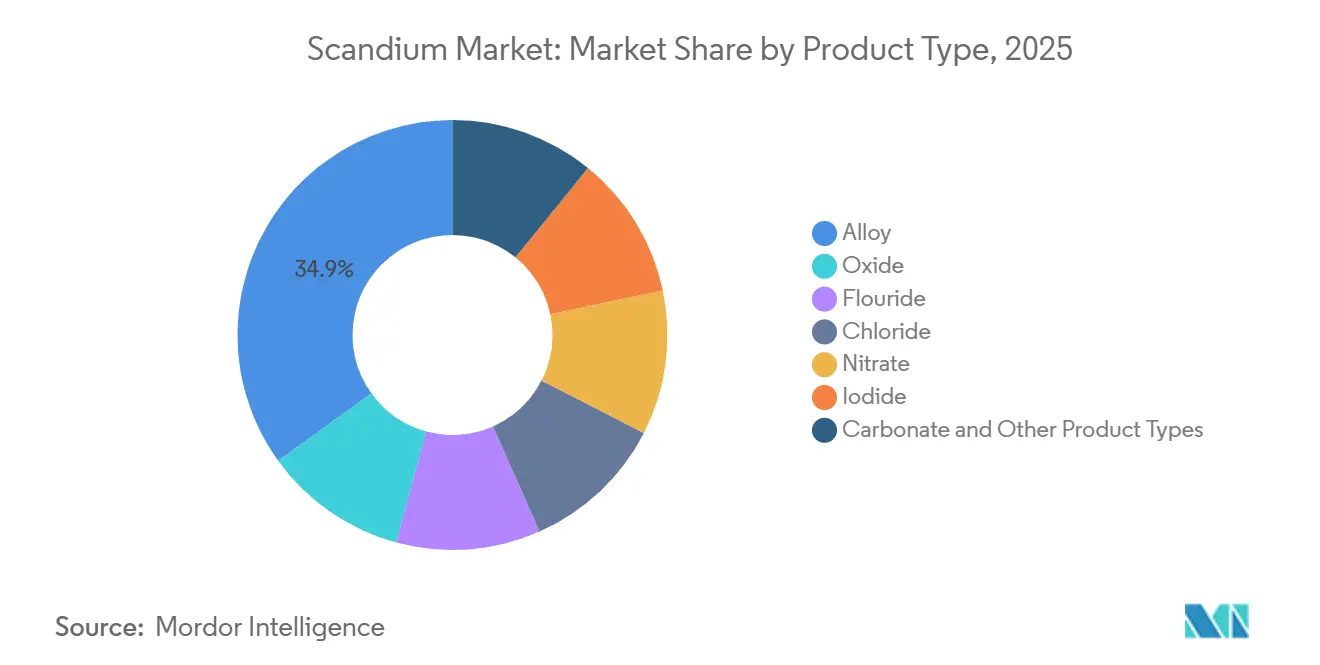

- By product type, alloys led with 34.94% of the scandium market share in 2025, while oxide is advancing at a 15.81% CAGR through 2031.

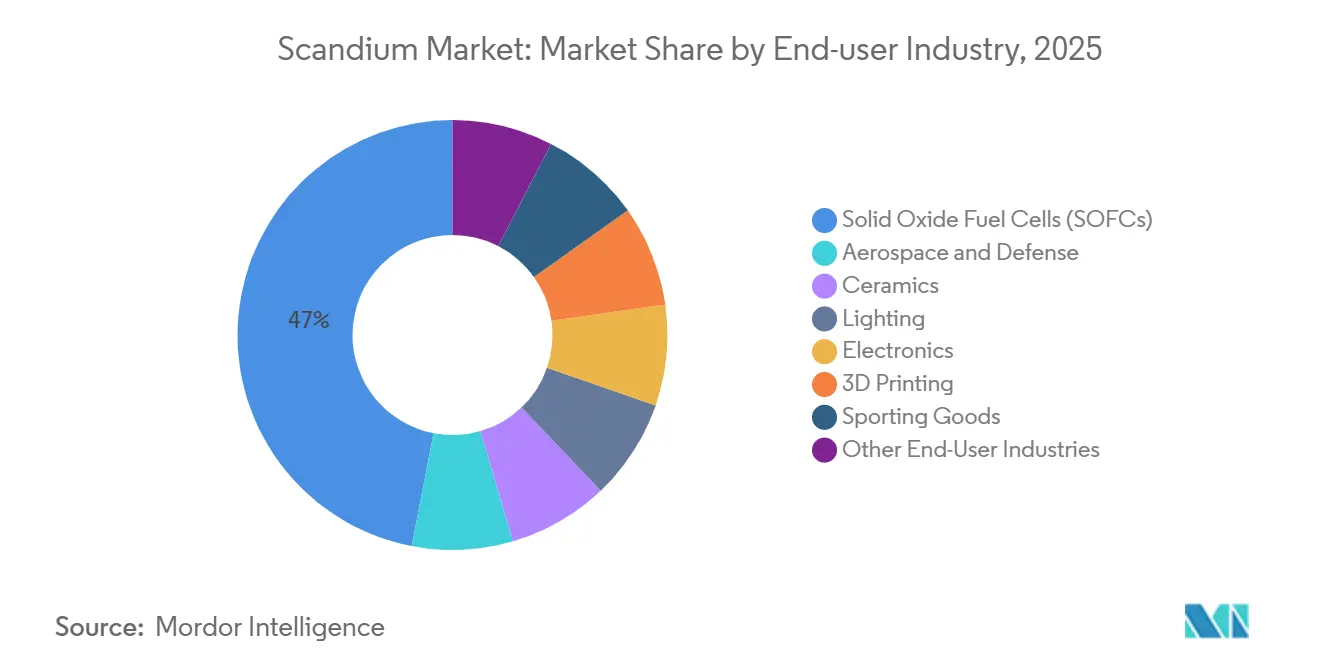

- By end-user industry, Solid Oxide Fuel Cells (SOFCs) accounted for 46.97% of demand in 2025, whereas aerospace and defense is expanding at a 15.12% CAGR to 2031.

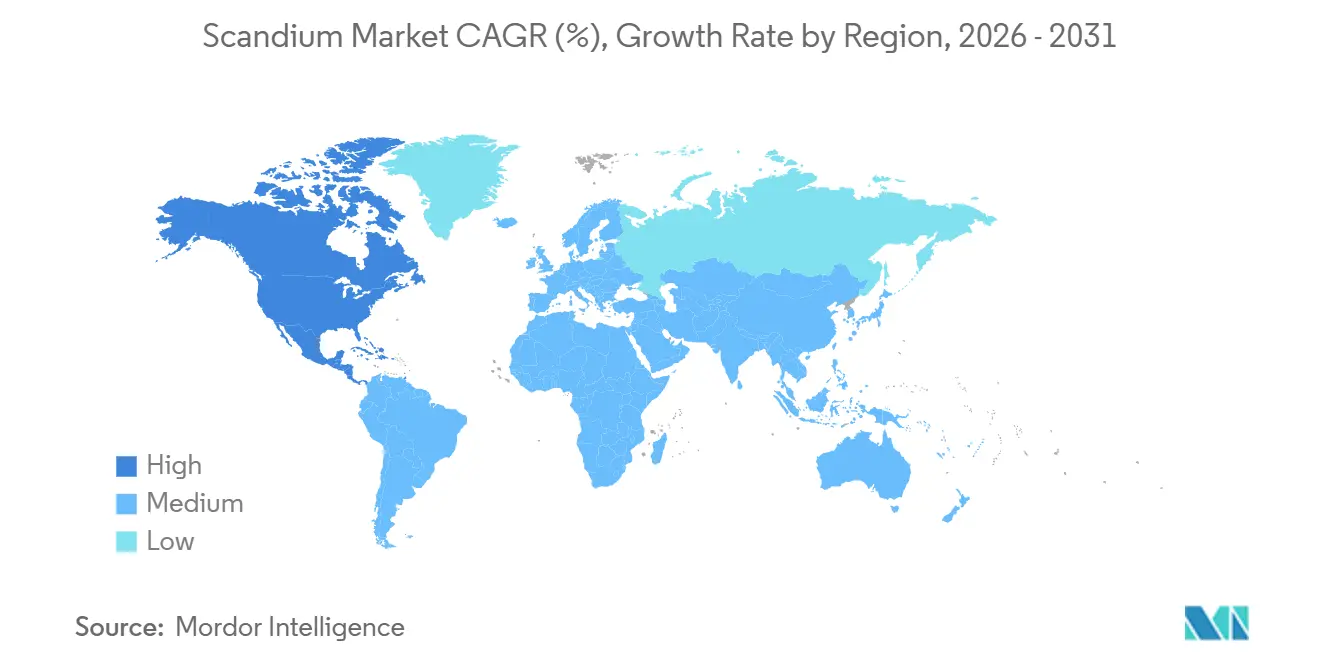

- By geography, China held 39.48% of 2025 consumption, and the United States is progressing at a 15.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Scandium Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption in Solid-Oxide Fuel Cells | +4.2% | Global, with early deployments in EU, Japan, US | Medium term (2–4 years) |

| Rising Demand for Al-Sc Alloys in Aerospace and Defence | +3.8% | North America, EU | Long term (≥4 years) |

| Critical-Mineral Policy Incentives and Funding | +2.9% | US, EU, Australia | Short term (≤2 years) |

| Expansion of Sc-Enabled Additive Manufacturing | +1.7% | North America, EU, APAC | Medium term (2–4 years) |

| EU TiO₂-Waste Scavenger Capacity Boost | +1.4% | European Union | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption in Solid-Oxide Fuel Cells

Scandium-stabilized zirconia lowers SOFC stack temperature to 700-800 °C, extending life and enabling cheaper metallic interconnects. Production, near 40 t oxide equivalent in 2025, is insufficient for both SOFC and aerospace demand. The EU-backed ScaVanger project targets 21 t oxide annually by 2026 from TiO₂ waste. Japan and Germany are piloting residential micro-CHP units but require long-term oxide pricing below USD 1,500 per kg to reach commercial parity. If secondary recovery scales on schedule, the scandium market will unlock new distributed power opportunities across data centers and commercial buildings.

Rising Demand for Al-Sc Alloys in Aerospace and Defense

Al-Sc alloys deliver 15-30% weight savings and superior weldability over 7xxx-series aluminum, attributes vital to hypersonic and next-generation airframes[1]U.S. Government Accountability Office, “Defense Critical Minerals Supply Chain Risks,” gao.gov . A USD 10 million Department of Defense grant to NioCorp in August 2025 created the first U.S. mine-to-master-alloy pathway. Additive-manufacturing powders further spur demand, reducing hot-cracking during laser fusion. Qualification cycles run three to five years, so each specification locks multi-tonne oxide offtake, deepening long-run scandium market visibility. Aerospace’s sustained 15.12% CAGR implies alloys will soon rival SOFCs in tonnage terms.

Critical-Mineral Policy Incentives and Funding

The U.S. Defense Logistics Agency plans to purchase up to USD 40 million of oxide for the National Defense Stockpile, anchoring domestic contracts. The EU Critical Raw Materials Act caps single-country dependence at 65%, pressuring firms to diversify away from China. Australia’s AUD 2 billion Critical Minerals Facility offers concessional loans, accelerating Nyngan and other projects. Rio Tinto expanded Sorel-Tracy from 3 t to 12 t oxide in 18 months, thanks to Canadian grants. Collectively, these moves shorten time-to-production for new scandium market entrants.

Expansion of Sc-Enabled Additive Manufacturing

Al-Sc powders refine grain structure, allowing high-precision lattice and heat-exchanger parts for aerospace. The same 36 wt % Al₃Sc powder now feeds semiconductor sputtering targets, as Al-Sc-N films offer 5× piezoelectric response over Al-N for 5 G filters. Higher semiconductor volumes improve powder economies of scale, lowering costs for aerospace buyers. Scandium Canada partnered with Productique Québec in August 2025 to qualify patent-pending alloys, cutting powder lead times to eight weeks. Additive manufacturing therefore multiplies use cases while decoupling buyers from traditional alloy supply chains, broadening the scandium market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Material Cost and Price Volatility | -2.1% | Global | Short term (≤2 years) |

| Supply Concentration in a Few Countries | -1.6% | Global | Medium term (2–4 years) |

| Uncertain Sc Precipitation Yields from HPAL Tailings | -0.9% | APAC (Philippines) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Material Cost and Price Volatility

Scandium oxide transacted around USD 1,200 per kg in 5 kg lots in 2025 while 99.99% metal reached USD 185,000-210,000 per kg within the scandium market, annual supply near 40 t, allowing a single aerospace contract can swing prices 30% in a quarter. Large buyers secure multi-year offtake from Rio Tinto and Scandium Canada, but small additive-manufacturing shops lack this leverage. Price spikes confine usage to premium goods such as F-35 landing-gear forgings and Louisville Slugger bats. The planned USD 40 million U.S. stockpile may stabilize a floor price yet signals scarcity through 2027.

Supply Concentration in a Few Countries

China controls ~60% of rare-earth mining and 90% of refining capacity, setting tone for scandium too. Russia and the Philippines add volume but face sanctions or nickel price swings. The GAO confirmed zero U.S. scandium suppliers in 2025, extending aerospace lead times up to six months. The FDPR now demands a Chinese license for foreign products containing ≥0.1% Chinese scandium, extending Beijing’s leverage. Projects at Elk Creek (95 t oxide) and Nyngan (38.5 t oxide) will not fully produce before 2027, leaving the scandium market vulnerable for the next two to three years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Alloys Lead, Oxide Accelerates for Dual-Use Demand

Alloys generated 34.94% of revenue in 2025 due to aerospace adoption of Al-Sc formulations that shave 15-30% weight yet maintain weldability. Oxide is registering the fastest 15.81% CAGR because both SOFC electrolytes and in-house master-alloy blending pull from the same feedstock. Fluoride, chloride, iodide, and carbonate variants remain research-grade at more than 500 kg annual global demand. Metalysis blurs lines by offering 36 wt % Al₃Sc powder that bypasses oxide traders and sells straight to semiconductor fabricators.

End-users shifting to internal alloy formulation shorten qualification from 12 months to 8 weeks, redistributing margin inside OEMs and tilting the scandium market toward oxide spot contracting. Should petrochemical catalysts based on scandium fluoride reach pilots, niche salt demand could rise, though commercialization is still exploratory.

By End-user Industry: SOFCs Dominate, Aerospace Surges on Defense Procurement

Solid Oxide Fuel Cells (SOFCs) commanded 46.97% of 2025 demand, underpinned by residential micro-CHP rollouts in Japan and Germany. Aerospace and defense is expanding at 15.12% CAGR, implying its scandium market share could approach 40% by 2029 if next-generation airframes adopt Al-Sc stringers.

Ceramics absorb modest volumes in dental and thermal-barrier uses, while lighting stagnates as LEDs replace metal-halide lamps. Electronics is the fastest emerging niche thanks to Al-Sc-N thin films for 5 G filters, now supplied by Metalysis powder. Sporting goods remain premium only, limited by high oxide pricing.

Geography Analysis

China accounted for 39.48% consumption in 2025, reflecting its dominant rare-earth refining and domestic SOFC pilots. The scandium market in United States is growing at 15.28% CAGR, driven by Defense Logistics Agency stockpiling and a USD 10 million DoD grant to NioCorp that targets a full mine-to-alloy chain. Russia’s RUSAL added 1.5 t oxide pilot capacity in 2025 but faces export hurdles under sanctions[2]RUSAL, “Bogoslovsky Pilot Plant Press Release,” rusal.ru .

The European Union mobilized EUR 3 billion under RESourceEU, with ScaVanger aiming at 21 t oxide from TiO₂ waste by 2026. Canada’s Sorel-Tracy expansion now yields 12 t oxide annually, offering North American primes a non-Chinese option. Australia’s Nyngan lease secures 38.5 t oxide from 2027, reinforcing diversified supply.

Philippine HPAL output remains volatile; utilization hangs around 33% of capacity, tied to nickel economics. Japan consumes oxide for SOFCs and electronics, while Brazil’s uptake is small and research-oriented. The scandium market continues to face supply-chain risk as FDPR license reviews of two to six months inject supply-chain risk, pushing Western aerospace primes to dual-source from Canada and Australia despite higher landed costs, a trend likely to persist through 2028.

Competitive Landscape

Moderate concentration defines the scandium market, with Rio Tinto, RUSAL, and Sumitomo integrating mining through refining. Rio Tinto secures long-term offtake with aerospace customers after tripling Sorel-Tracy capacity. The U.S. stockpile tender underwrites demand, encouraging miners such as NioCorp and Scandium International to finalize project finance.

Metalysis disrupts traditional alloy flow by selling 36 wt % Al₃Sc directly to semiconductor and additive-manufacturing markets, bypassing master-alloy houses. Secondary recovery projects, including EU ScaVanger and RUSAL’s red-mud pilot, illustrate a low-capex model that may double non-Chinese supply within five years. Players offering 99.99% oxide or ultra-low-impurity alloys command 20-30% price premiums, a margin supporting investment in advanced solvent-extraction or zone-melting systems.

White-space remains in additive manufacturing service bureaus that can atomize alloy on demand, in catalyst developers exploring scandium fluoride, and in medical-implant innovators piloting scandium-doped titanium. Technology differentiation based on extraction yield and purity will decide winners as new capacity arrives between 2026 and 2029, potentially reshaping the scandium market hierarchy.

Scandium Industry Leaders

Rio Tinto

RusAL

Sunrise Energy Metals

Guangxi Maoxin Technology Co., Ltd

Scandium International Mining Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Australian Mines Limited reported notable drilling results from its Flemington Project. The aircore drilling program has identified high-grade scandium mineralisation near the surface, surpassing the current resource estimate. The program consisted of 30 aircore drill holes, covering a total of 604 metres, and confirmed extensive scandium mineralisation from surface level.

- November 2025: Department of War awarded USD 29.9 million to ElementUS Minerals, LLC (ElementUSA) to establish a U.S. domestic supply of gallium and scandiu. ElementUSA will utilize this funding to develop a demonstration facility in Gramercy, Louisiana, aimed at separating and purifying gallium and scandium from existing industrial waste.

Global Scandium Market Report Scope

Scandium, with the chemical symbol Sc and atomic number 21, is a silver-white transitional metal categorized as a rare-earth element. It possesses distinctive traits such as lightness, a high melting point, and a small ionic radius. Due to its small ion size, it seldom forms concentrations exceeding 100 ppm naturally, as it doesn't readily bond with common ore-forming anions. Notably, its main applications include solid oxide fuel cells (SOFCs) and aluminum-scandium alloys, enhancing strength and performance, particularly due to its fine grain refinement, which reduces hot cracking in welds and improves fatigue behavior.

The scandium market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into oxide, fluoride, chloride, nitrate, iodide, alloy, carbonate, and other product types. By end-user industry, the market is segmented into aerospace and defense, solid oxide fuel cells, ceramics, lighting, electronics, 3D printing, sporting goods, and other end-user industries. The report also covers the market size and forecasts for scandium in 6 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of value (USD).

| Alloy |

| Oxide |

| Flouride |

| Chloride |

| Nitrate |

| Iodide |

| Carbonate and Other Product Types |

| Solid Oxide Fuel Cells (SOFCs) |

| Aerospace and Defense |

| Ceramics |

| Lighting |

| Electronics |

| 3D Printing |

| Sporting Goods |

| Other End-User Industries |

| Production Analysis | China |

| Russia | |

| Philippines | |

| Rest of the World | |

| Consumption Analysis | United States |

| China | |

| Russia | |

| Japan | |

| Brazil | |

| European Union | |

| Rest of the World |

| By Product Type | Alloy | |

| Oxide | ||

| Flouride | ||

| Chloride | ||

| Nitrate | ||

| Iodide | ||

| Carbonate and Other Product Types | ||

| By End-user Industry | Solid Oxide Fuel Cells (SOFCs) | |

| Aerospace and Defense | ||

| Ceramics | ||

| Lighting | ||

| Electronics | ||

| 3D Printing | ||

| Sporting Goods | ||

| Other End-User Industries | ||

| By Geography | Production Analysis | China |

| Russia | ||

| Philippines | ||

| Rest of the World | ||

| Consumption Analysis | United States | |

| China | ||

| Russia | ||

| Japan | ||

| Brazil | ||

| European Union | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large will global demand be for scandium by 2031?

The scandium market size is forecast to reach USD 2.01 billion by 2031, reflecting a 14.53% CAGR from 2026.

Which segment is expanding fastest?

Aerospace and defense demand is advancing at a 15.12% CAGR due to Al-Sc alloy adoption in future airframes and hypersonic vehicles.

Why are oxide prices so volatile?

Annual output is only about 40 t, so a single multi-tonne aerospace or SOFC contract can shift spot prices by 30% within a quarter.

What policy actions support new scandium supply?

The EU’s RESourceEU plan, the U.S. Defense Logistics Agency stockpile purchase, and Australia’s Critical Minerals Facility all provide funding and offtake guarantees for new projects.

How will secondary recovery affect supply security?

Projects such as the EU ScaVanger initiative could displace up to 40% of primary mined scandium by 2030, reducing reliance on China.

Page last updated on: