Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

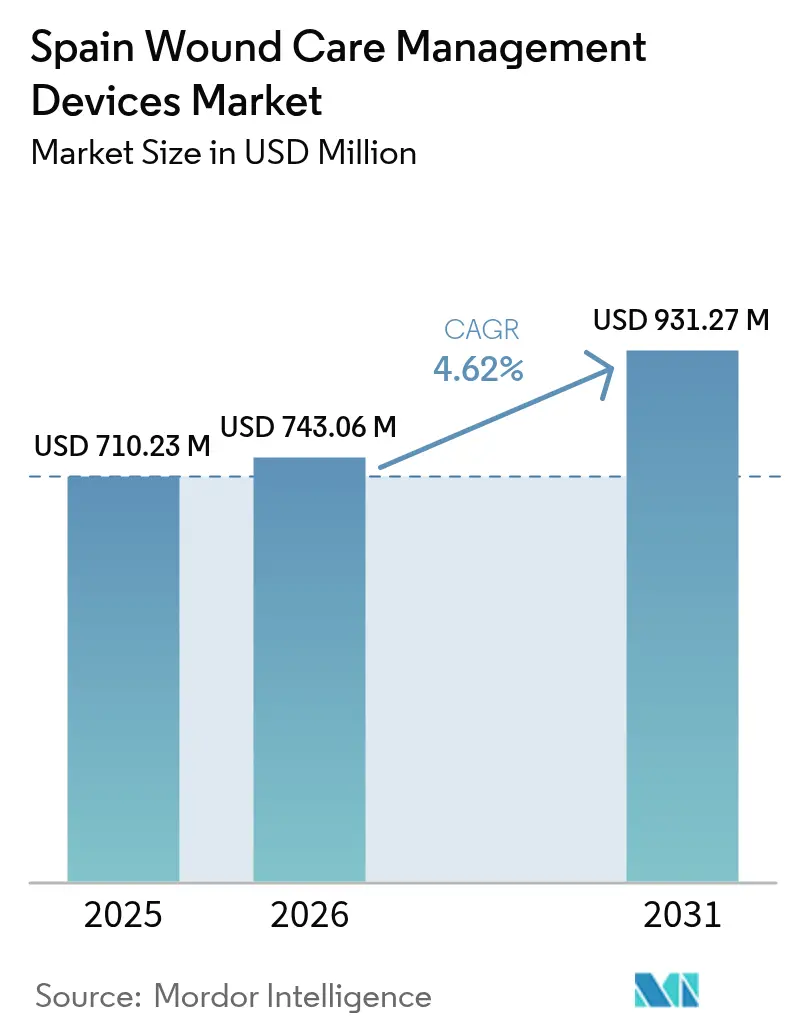

| Base Year Market Size (2025) | USD 710.23 Million |

| Market Size (2026) | USD 743.06 Million |

| Market Size (2031) | USD 931.27 Million |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Wound Care Management Devices Market Analysis by Mordor Intelligence

The Spain wound care management devices market size is expected to grow from USD 710.23 million in 2025 to USD 743.06 million in 2026 and is forecast to reach USD 931.27 million by 2031 at 4.62% CAGR over 2026-2031. Rising life expectancy, with 37.2% of residents expected to be over 65 by 2052, intensifies demand for chronic-wound therapies. A national type 2 diabetes prevalence of 14.7%, and 30.3% among people older than 70, further fuels the Spain wound care management devices market as diabetic foot ulcers require specialized care. Decentralized procurement across 17 Autonomous Communities drives cost variation yet stimulates adoption of advanced dressings and negative pressure wound therapy (NPWT) to lower per-patient costs. Chronic wounds account for 60.34% of revenue, while acute wounds are growing faster in tandem with recovering surgical procedures [1]Miguel Ángel Díaz-Herrera, "The financial burden of chronic wounds in primary care: A real-world data analysis on cost and prevalence," ScienceDirect, sciencedirect.com. Technology-enabled home care, including tele-monitoring and portable NPWT, underpins a rapid shift from hospital to community settings.

Key Report Takeaways

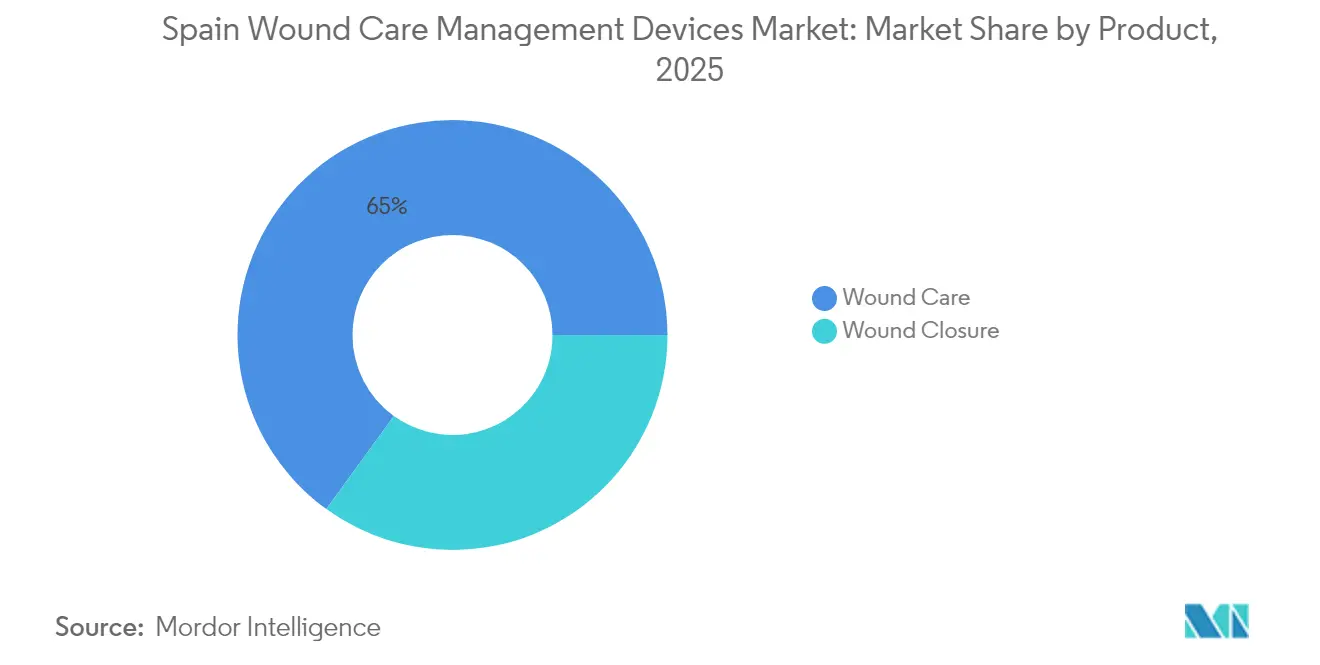

- By product category, wound care devices led with 65.02% revenue share of the Spain wound care management devices market in 2025; wound closure products post the fastest 5.05% CAGR through 2031.

- By wound type, chronic wounds held 60.05% of the Spain wound care management devices market share in 2025, while acute wounds record the highest 5.14% CAGR outlook to 2031.

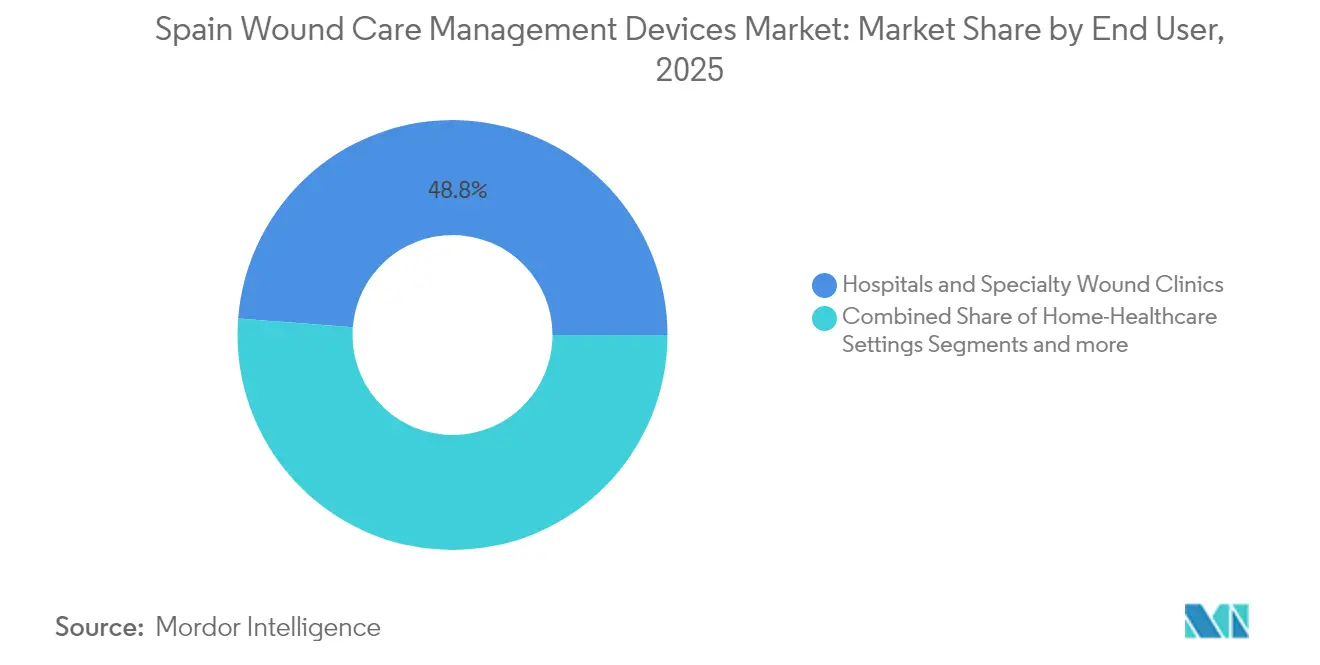

- By end user, hospitals and specialty clinics accounted for 48.78% of the Spain wound care management devices market size in 2025, whereas home healthcare is projected to expand at a 5.64% CAGR during 2026-2031.

- By mode of purchase, institutional procurement dominated with 64.02% share in 2025; retail/OTC channels are forecast to grow at 5.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of diabetic foot & pressure ulcers | +1.2% | National, higher in urban areas | Long term (≥ 4 years) |

| Rising volume of elective & trauma surgeries | +0.8% | Major metropolitan regions | Medium term (2-4 years) |

| Ageing population boosting chronic-wound incidence | +1.5% | Rural communities | Long term (≥ 4 years) |

| Hospital-to-home shift & home-based NPWT adoption | +0.9% | Catalonia, Madrid, Andalusia | Medium term (2-4 years) |

| Regional clinical-nurse-led wound units cutting recurrence | +0.4% | Andalusia, Valencia, Catalonia | Short term (≤ 2 years) |

| E-health tele-monitoring platforms reducing follow-up visits | +0.6% | Pilot programs nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Diabetic Foot & Pressure Ulcers

Diabetic foot ulcers are now the primary diagnosis in 90.5% of Spain’s specialized wound units, generating EUR 2.063 million per infected case when hospitalization is required [2]Roberto Da Ros, "Burden of Infected Diabetic Foot Ulcers on Hospital Admissions and Costs in a Third-Level Center," MDPI, mdpi.com. Hospital stays account for 88% of that expense and lengthen healing to 194 days versus 136 days for outpatient care. Advanced thermographic AI yields 95% diagnostic accuracy for peripheral neuropathy, prompting earlier interventions that lower ulcer incidence [3]Albert Siré Langa, "Advanced AI-Driven Thermographic Analysis for Diagnosing Diabetic Peripheral Neuropathy and Peripheral Arterial Disease," MDPI, mdpi.com. Health authorities view investment in advanced dressings and NPWT as a cost-saving strategy that curbs amputations and readmissions.

Rising Volume of Elective & Trauma Surgeries

Elective procedures rebounded in 2024-2025, sustaining demand for post-operative closure and infection-prevention devices. Vacuum-assisted closure therapy reduced healing time and length of stay in 41 complex cases at the University Clinic of Navarra. Polyurethane foam multilayer dressings cut dressing changes by 47.1% and weekly costs by 58.7%. Surgeons increasingly prescribe single-use NPWT systems that enable earlier discharge and support community-based follow-ups.

Ageing Population Boosting Chronic-Wound Incidence

Chronic diseases generate 80% of primary-care visits among older Spaniards, and structured nurse-training in Andalusia halved chronic-wound prevalence within two years. Pressure-ulcer treatment already absorbs EUR 600 million annually yet remains below US and UK levels due to protocol differences. Demographic pressure accelerates demand for smart mattresses, antimicrobial dressings, and sensor-enabled bandages that prevent ulcer formation.

Hospital-to-Home Shift & Home-Based NPWT Adoption

Portable NPWT delivers similar closure rates to inpatient systems yet saves EUR 4,155.98 per healed wound through fewer resources and faster discharge. Catalonia, Madrid, and Andalusia spearhead tele-monitoring pilots that connect community nurses with specialists, promoting continuity of care. Budget constraints delay nationwide roll-out, but expanding electronic prescription coverage builds the digital foundation for large-scale remote wound surveillance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited national reimbursement for advanced dressings | -0.7% | National, variable across regions | Medium term (2-4 years) |

| High per-patient cost of NPWT & bio-engineered grafts | -0.5% | Budget-constrained regions | Long term (≥ 4 years) |

| Fragmented procurement across 17 Autonomous Communities | -0.3% | Nationwide | Short term (≤ 2 years) |

| Shortage of certified wound-care specialists in primary care | -0.4% | Rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited National Reimbursement for Advanced Dressings

Advanced devices need CE marking through the Spanish Agency of Medicines and Medical Devices (AEMPS), yet decisions on funding rest with each region, creating a patchwork of coverage. Manufacturers negotiate multiple formularies, slowing time-to-market even when cost-effectiveness is proven via health technology assessments.

High Per-Patient Cost of NPWT & Bio-Engineered Grafts

NPWT capital requirements deter hospitals with tight budgets, although clinical data confirm lower total care costs once adopted. Spanish engineers are prototyping low-cost vacuum systems yielding comparable outcomes, but perception of high upfront cost persists among administrators focused on annual spending rather than lifetime savings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound Care Dominance Drives Innovation

Advanced wound care solutions held 65.02% of the Spain wound care management devices market in 2025, led by antimicrobial foam dressings that trimmed weekly treatment expenses by 58.6%. The Spain wound care management devices market size for wound closure products is growing at a 5.05% CAGR, driven by demand for tissue adhesives that lower infection risk and enable faster outpatient turnover. Smith+Nephew marked 12.2% sales growth within its local advanced wound unit following the release of the Red Dot-winning RENASYS EDGE NPWT platform, reinforcing brand momentum.

Sutures remain dominant in closure devices, yet smart sealants containing growth factors are entering operating rooms. Bio-engineered topical agents continue to capture niche demand for antimicrobial control, while enzymatic debridement gels receive attention in diabetic care pathways. Emerging Internet-of-Things-enabled dressings transmit temperature and exudate data, allowing clinicians to predict infection onset and adjust therapy without unnecessary dressing removal.

By Wound Type: Chronic Wounds Lead Despite Acute Growth

Chronic wounds accounted for 60.05% of the Spain wound care management devices market share in 2025 as diabetic foot, venous leg, and pressure ulcers prevail in an aging society. The Spain wound care management devices market size for acute wounds is projected to grow at 5.14% CAGR to 2031, reflecting surgical rebounds and trauma incidence.

Diabetic foot ulcers represent the largest chronic segment, correlating with 14.7% diabetes prevalence. Pressure ulcers pose significant resource burdens, yet structured prevention programs demonstrate a 50% reduction in prevalence when spearheaded by advanced practice nurses. Acute surgical wounds benefit from prophylactic NPWT and antimicrobial hydrofiber dressings that shorten closure times.

By End User: Home Healthcare Emerges as Growth Driver

Hospitals and specialist clinics captured 48.78% of revenue in 2025, underlining their role in complex wound treatment. Home-care settings, however, will expand by 5.64% CAGR as portable NPWT and tele-consultation solutions mature. Flexible reimbursement for home visits and the elderly's preference for domestic recovery underpin this growth.

Long-term care facilities maintain steady demand given Spain’s growing institutionalized elderly population. Community pharmacies broaden access by stocking advanced dressings vetted through clinical-nurse guidance, limiting unnecessary emergency consultations.

By Mode of Purchase: Retail Growth Challenges Institutional Dominance

Institutional tenders claimed 64.02% of sales in 2025, but patient self-care and direct-to-consumer channels are widening at 5.42% CAGR. Consumers value convenience and privacy when treating chronic wounds, turning to e-commerce sites integrated with pharmacist advice tools.

Regional value-based procurement pilots, such as Andalusia’s dressings framework, shift evaluation criteria from unit price to total care cost, favoring premium technologies with proven outcome savings.

Geography Analysis

Spain’s decentralized model shapes procurement and adoption patterns within the Spain wound care management devices market. Catalonia, Madrid, and Andalusia lead purchases owing to larger budgets, academic hospitals, and higher patient volumes. These regions host most of the nation’s 42 specialized wound units, 35.7% of which are hospital-based and 40.5% located in health centers, leaving rural areas to depend on primary-care nurses for wound management.

Northern regions such as the Basque Country leverage European innovation networks to pilot AI-enabled thermographic screening and remote-monitoring solutions. Early adopters report reduced clinic visits and lower recidivism through predictive analytics. Mediterranean coastal provinces face the highest burden of chronic ulcers due to demographic aging and lifestyle factors. Valencia’s La Fe University Hospital documented improved outcomes using vacuum therapy across pediatric and adult cohorts, demonstrating technology transfer potential to neighboring regions.

Andalusia’s advanced practice nursing model, credited with halving chronic-wound prevalence, is being replicated in Extremadura and Castilla-La Mancha. Despite progress, rural municipalities still contend with specialist shortages, highlighting demand for intuitive, low-maintenance devices that primary-care teams can deploy. Region-specific reimbursement differences oblige suppliers to tailor bids, yet national adoption of electronic medical records fosters data harmonization that supports wider tele-wound programs.

Regulatory Landscape

Medical devices commercialized in Spain, including wound dressings, NPWT systems, and closure products, operate under the EU Medical Device Regulation (EU) 2017/745 (MDR), with national implementation and oversight anchored by Real Decreto 192/2023. The Agencia Espanola de Medicamentos y Productos Sanitarios (AEMPS) serves as the competent authority for market oversight, vigilance, and national requirements tied to placing devices on the Spanish market.

In 2026, compliance requirements tightened around more formalized, digital-first registrations. Mandatory use of EUDAMED modules took effect on May 28, 2026, and AEMPS brought its RECOPS national registry platform into operation on June 15, 2026, to centralize device and IVD registrations. For manufacturers, importers, and distributors supplying Spain, these steps increase the need to keep device and economic-operator data current, since gaps can disrupt commercialization and affect tender timelines across the 17 Autonomous Communities.

Competitive Landscape

The Spain wound care management devices market shows moderate concentration with top multinationals and nimble domestic innovators vying for formulary placement. Smith+Nephew’s RENASYS EDGE launch strengthened its position by offering user-friendly controls and remote pressure monitoring.

Mölnlycke’s Mepilex Border Flex study in Spain confirmed fewer dressing changes and cost savings, bolstering tender competitiveness. Coloplast leverages intimate collaboration with stoma and continence care teams to cross-sell wound dressings in hospital and community settings. Domestic biotech players such as Histocell and Genia BioPharma target regenerative grafts tailored to local clinical preferences. These SMEs partner with university hospitals to validate efficacy and accelerate regional adoption.

Digital-health integration is now a key differentiator. Platforms that combine wound photography, measurement algorithms, and clinician dashboards provide real-time insights, helping vendors demonstrate outcome-based value. Procurement bodies increasingly demand proof of total-cost reduction, triggering alliances where manufacturers co-develop training modules, data analytics, and supply-chain services. Companies able to align commercial goals with cost containment and clinical outcomes gain strategic advantage in a fragmented yet performance-driven environment.

Spain Wound Care Management Devices Industry Leaders

-

Medtronic PLC

-

Smith & Nephew

-

ConvaTec Group PLC

-

Coloplast A/S

-

Solventum

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Fragmented procurement and uneven regional funding create whitespace for suppliers that combine advanced wound care products with service layers that reduce friction in adoption, particularly through community pathways. Portable NPWT and technology-enabled home care align with the hospital-to-home shift described in the market, and tele-monitoring pilots in Catalonia, Madrid, and Andalusia offer a practical route to scale devices that reduce follow-up visits, provided vendors also support training and remote follow-up. Vendors that standardize evidence submission and registry readiness for AEMPS processes, including EUDAMED and the newer RECOPS workflow, can reduce administrative delays that often slow multi-region rollouts.

Recent corporate actions also point to supply and go-to-market opportunities around advanced dressings and distribution footprint. In May 2026, Saesco Medical acquired the autonomous business unit of Sanguessa S.A. and Tramedic S.A., committing an initial investment of more than EUR 3 million to consolidate operations in Spain. This signals continued interest in strengthening local commercial coverage for hospital and institutional channels. On the manufacturing side, Molnlycke Health Care announced in June 2026 an approximately EUR 40 million combined investment across its Mikkeli (Finland) and Oldham (UK) manufacturing sites to expand wound care capacity and improve supply resilience, supporting steadier availability of advanced wound care products in markets such as Spain where tender continuity and on-time delivery influence formulary positioning.

Recent Industry Developments

- May 2026: Saesco Medical acquired the autonomous business unit of Sanguessa S.A. and Tramedic S.A., stating an initial investment of more than EUR 3 million to consolidate and drive its medical device operations in Spain. The acquisition strengthens local coverage and logistics for institutional procurement, where supplier service levels and continuity can shape tender outcomes in wound care.

- June 2025: Smith & Nephew inaugurated a 2,000 square meter medtech facility and Competence Center in Barcelona (Esplugues de Llobregat) to expand surgical training and digital lab capabilities. The site strengthens local clinical education and technology deployment infrastructure, supporting uptake of advanced wound management solutions through closer engagement with Spanish care teams.

- April 2024: Gradiant and IIS Galicia Sur launched ICAREWOUNDS, a European consortium focused on comprehensive chronic-wound care models. The collaboration supports standardized pathways and evidence generation that can accelerate adoption of advanced dressings and devices across hospital and community settings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers device-based products used in Spain to manage wounds, meaning items that clean, protect, close, or help healing for acute and chronic skin breaks, which are procured through medical channels.

Scope exclusions: Over-the-counter antiseptic creams and purely diagnostic imaging tools are not counted in the market value.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base and confirm that assumptions matched what is observable in Spain. We relied on public and official source types such as Spanish health system publications and procurement notices, Eurostat health and demographic tables, OECD health statistics, World Health Organization health indicators, and clinical guidance and papers indexed in peer-reviewed journals.

We also reviewed company annual reports, product literature, investor presentations, and trusted industry press to understand what products are being promoted in Spain, how portfolios are shifting, and how pricing is moving. For a few topics, we referenced paid subscriptions for company financials and news coverage, as well as patent databases, mainly to verify timelines and product activity rather than to replace market modeling. The sources listed above are illustrative only, and additional public references were used to collect data, cross-check numbers, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure-test the Spain-specific demand picture and the pricing logic across hospitals, outpatient settings, and home care where relevant. We spoke with a mix of manufacturers, distributors, clinical stakeholders, and procurement-focused respondents so that gaps from desk research could be closed, and assumptions could be checked from more than one angle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | |

| Mid tier: 48% | Functional/Unit leaders: 35% | |

| Smaller Players: 21% | Managers: 53% |

Market-Sizing & Forecasting

Sizing started with a top-down build where Spain health system utilization signals and treated-patient pools were translated into device demand, and then converted to value using observed price points from channel discussions. To keep the totals realistic, the output was corroborated with selective bottom-up checks, such as sampled supplier revenue splits, product mix patterns across care settings, and a few ASP times volume approximations for major categories.

Inputs used in the model included the estimated chronic wound burden tied to diabetes and aging, surgical procedure activity that shapes acute wound volumes, adoption rates for advanced dressings and NPWT in routine protocols, typical change frequency for dressings by wound type, and procurement behavior differences across Spain's autonomous communities. Where data was thin for smaller sub-categories, we filled gaps using proxy indicators such as clinical usage norms and validated share splits gathered from interviews.

For forecasting, scenario analysis was used so that faster or slower adoption of advanced therapies, price movement under tenders, and shifts to home care could be reflected without overfitting the data. Assumptions were reviewed with primary respondents, and only changes that could be tied back to clear drivers were carried into the final forecast.

Data Validation & Update Cycle

Validation was done through step-by-step checks that compare the model output against independent signals, and then flag any large variances for a second look. When something looked off, such as a pricing jump that did not align with procurement cycles or a volume swing that did not match procedure trends, the assumptions were revisited and, when needed, primary contacts were re-approached for clarification.

Before sign-off, the work is reviewed across analysts so the scope, math, and logic are consistent and traceable. The report is refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery review so clients receive the latest view.

Mordor Intelligence's Spain Wound Care Management Devices Market Estimate Compared With Other Published Estimates

Published market values for Spain wound care devices can vary, even when the topic sounds the same, because the product list, the care settings counted, and the way pricing is converted to revenue are not always aligned. Differences in base year choice and the refresh timing can also create spreads, especially when tender-driven prices move.

The main gap comes from what is counted as a device market, where Mordor Intelligence includes advanced dressings, NPWT kits, closure staples, sutures, tissue adhesives, hemostats, and low-frequency therapy units, but keeps out over-the-counter creams and non-therapy imaging, which some estimates blend into a broader wound care value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 710.23 M (2025) | |

| Industry Publisher A | USD 49.50 M (2025) | Uses a narrower product scope that appears to center on selected wound care products, which can exclude large device revenue pools like closure, hemostats, and therapy systems, thereby understating the total when compared on the same year. |

| Databook Publisher B | USD 373.80 M (2024) | Focuses on chronic wound care only and anchors the value to a different year, so acute and surgical wound volumes and the full hospital procurement mix are not fully represented in the total. |

The table shows that scope choices explain most of the spread, and the year used for quoting the number explains the rest. By keeping the product list tied to what is procured through medical channels and by checking totals against usage and pricing signals, the final value stays transparent and repeatable.

Key Questions Answered in the Report

What is the current value of the Spain wound care management devices market?

The market is valued at USD 743.06 million in 2026 and is projected to reach USD 931.27 million by 2031, reflecting a 4.62% CAGR outlook.

Which product category leads the Spain wound care management devices market?

Advanced wound care devices, including antimicrobial foam dressings and NPWT systems, held 65.02% share in 2025.

Why are home-care settings growing faster than hospitals?

Portable NPWT and tele-monitoring platforms enable safe wound management at home, delivering comparable clinical results while lowering costs and freeing hospital capacity.

How does Spain’s decentralized healthcare system affect device procurement?

Each of the 17 Autonomous Communities controls its own tenders and reimbursement lists, forcing suppliers to navigate varied criteria and timelines.

Which wound type drives the highest revenue?

Chronic wounds, especially diabetic foot and pressure ulcers, represented 60.05% of 2025 revenue due to an aging population and high diabetes prevalence.

What main barrier limits advanced dressing adoption?

Regional reimbursement gaps and the perceived high upfront cost of NPWT and bio-engineered grafts slow market penetration despite long-term savings evidence.

Page last updated on: