Saudi Arabia Tiles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

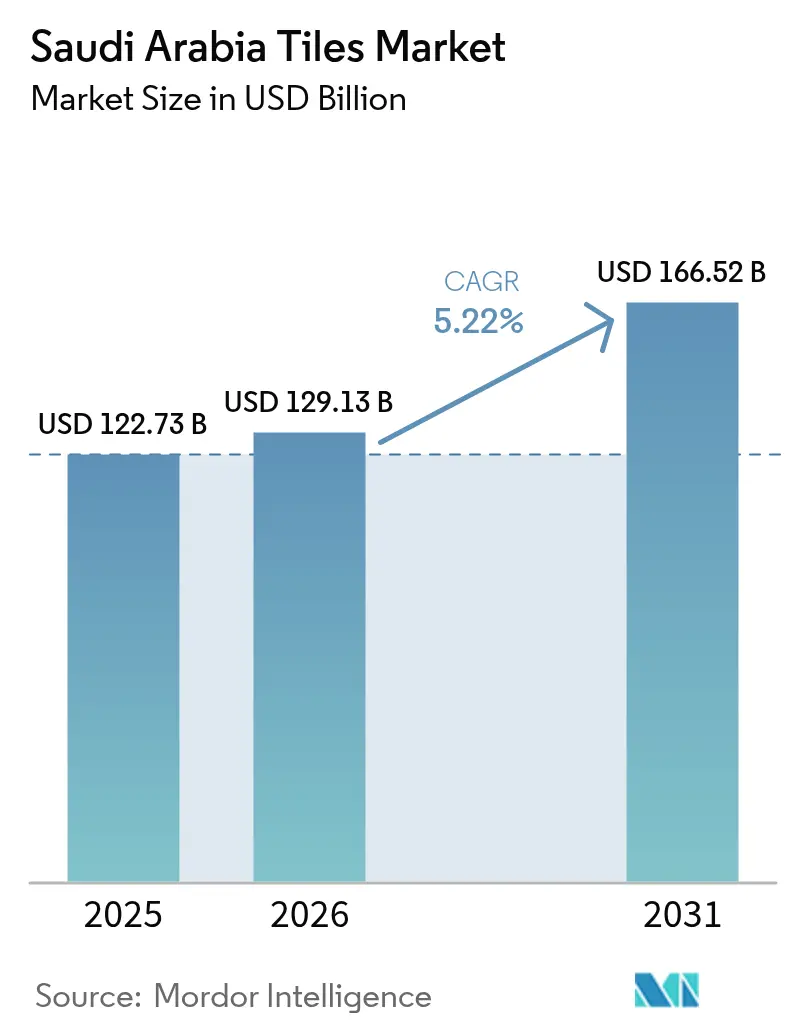

| Base Year Market Size (2025) | USD 122.73 Billion |

| Market Size (2026) | USD 129.13 Billion |

| Market Size (2031) | USD 166.52 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

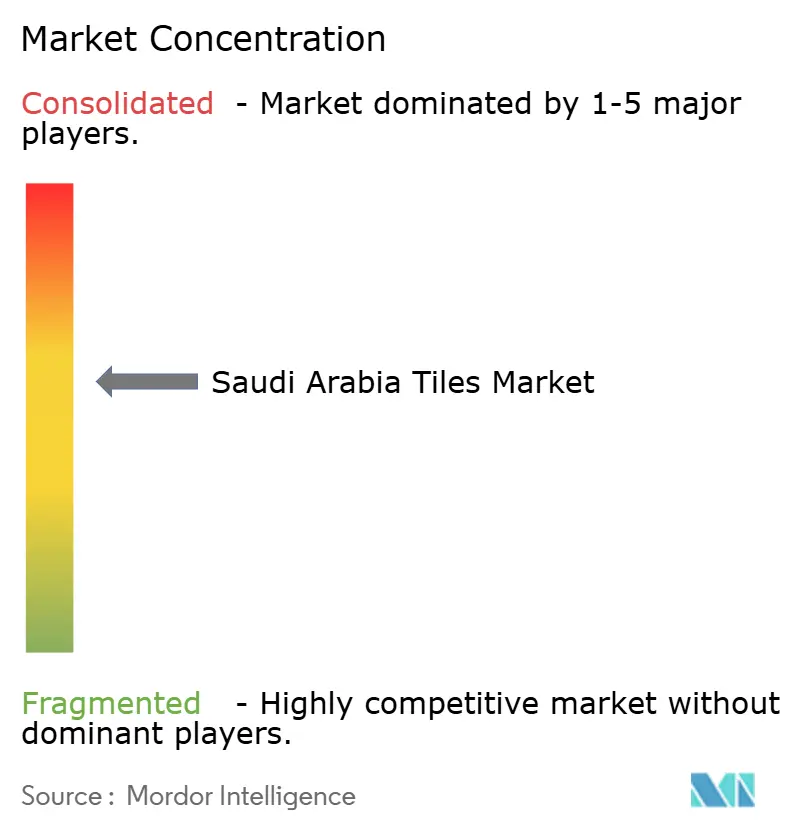

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Tiles Market Analysis by Mordor Intelligence

Saudi Arabia Tiles Market size in 2026 is estimated at USD 129.13 billion, growing from 2025 value of USD 122.73 billion with 2031 projections showing USD 166.52 billion, growing at 5.22% CAGR over 2026-2031. The trajectory mirrors the construction momentum unleashed by Vision 2030 housing targets, a surge of giga-projects, and mortgage reforms that widened home-ownership access across the Kingdom. Demand tilts decisively toward ceramic and porcelain categories because durable surfaces meet Saudi Building Code performance requirements and aesthetic expectations for premium residential and commercial projects. Logistics upgrades—new rail corridors, automated warehouses, and multimodal freight hubs—shorten delivery lead times and reduce breakage, thereby strengthening domestic and import-driven supply chains. Competitive intensity stays moderate as the top five suppliers hold about 65% of total sales, yet more than 30 smaller brands retain price-sensitive niches, fueling product innovation and segmented marketing strategies[1]Saudi Industrial Development Fund, “Manufacturing Sector Analysis,” sidf.gov.sa..

Key Report Takeaways

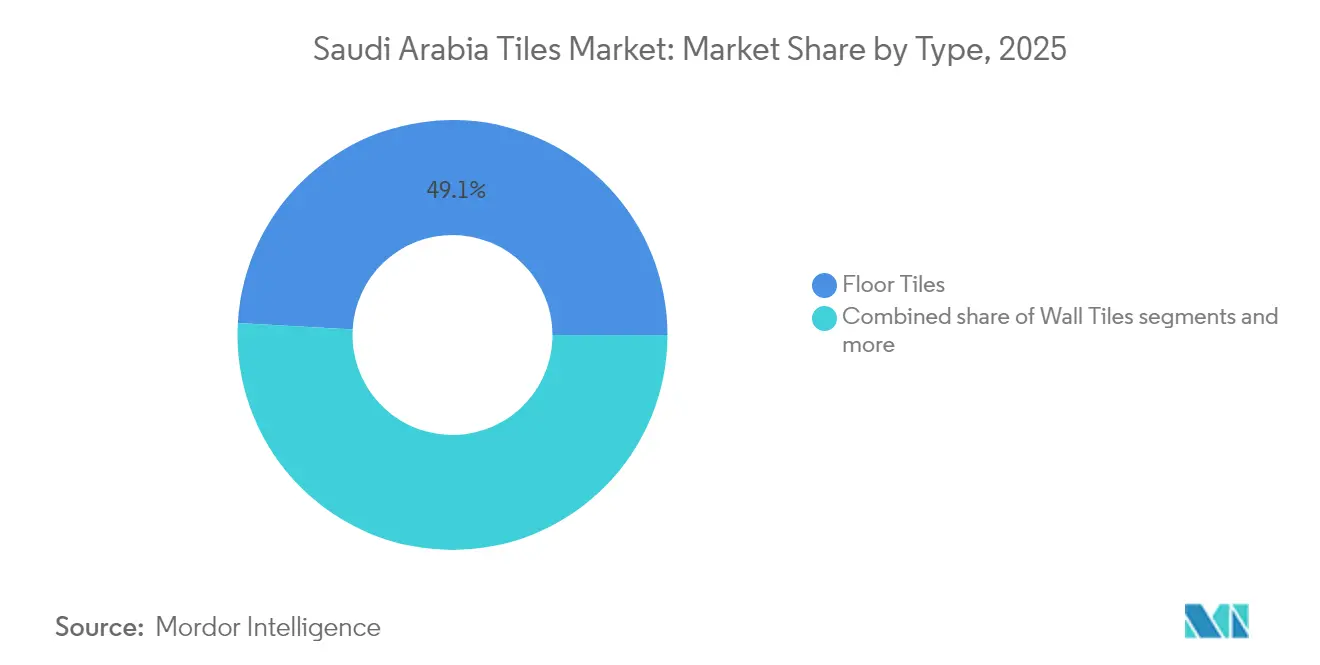

- By type, floor tiles led with 49.12% of the Saudi Arabia Tiles Market share in 2025, whereas roof tiles are expanding at the fastest 8.54% CAGR to 2031.

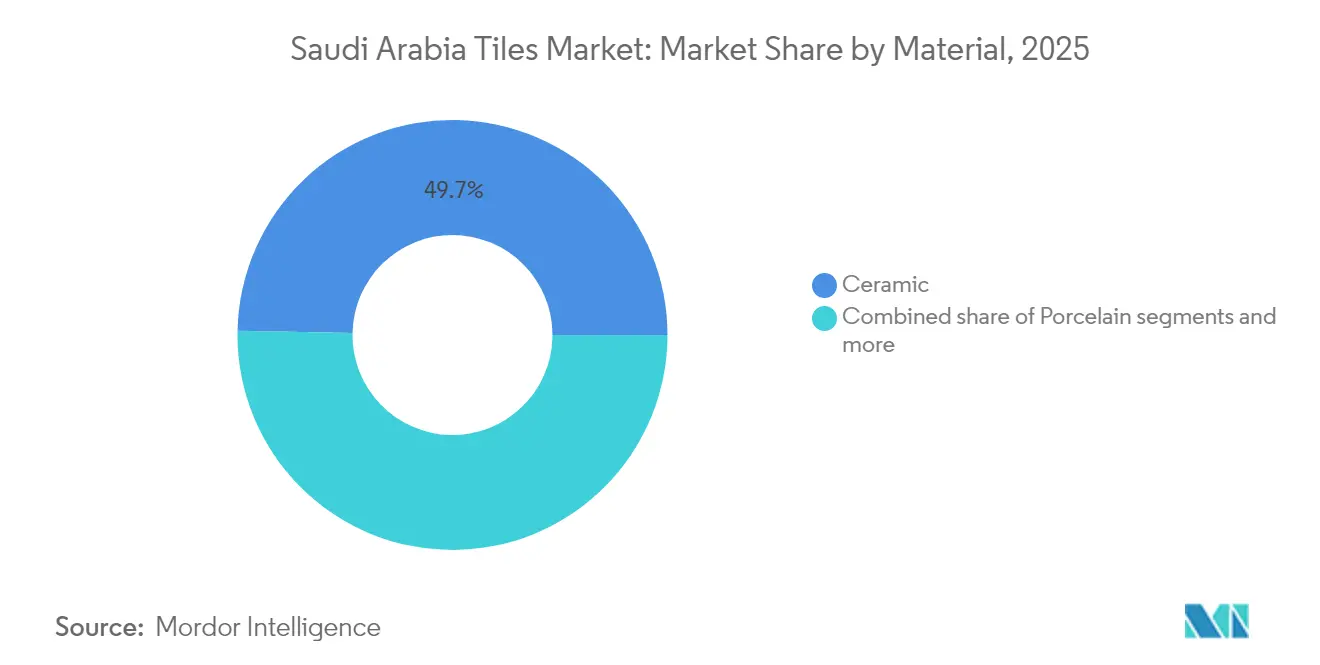

- By material, ceramic occupied 49.68% of the Saudi Arabia Tiles Market size in 2025, while porcelain shows a 7.61% CAGR through 2031.

- By end user, the residential segment accounted for a 57.05% share of the Saudi Arabia Tiles Market size in 2025, yet commercial applications are accelerating at an 8.42% CAGR toward 2031.

- By geography, the Central Region captured 33.10% of Saudi Arabia's tile market share in 2025, and the Northern Region is projected to surge at a 10.52% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging residential construction under Vision 2030 | +1.8% | National, highest in Central & Western regions | Medium term (2-4 years) |

| Government-backed giga-projects (NEOM, Red Sea, Diriyah, Qiddiya) | +1.5% | Northern & Western regions | Long term (≥ 4 years) |

| Preference shift toward ceramic & porcelain tiles | +1.2% | National, premium cities | Short term (≤ 2 years) |

| Improved retail & logistics infrastructure | +0.8% | Nationwide, early gains in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Localization incentives (“Made in Saudi”) boosting domestic output | +1.0% | Nationwide, strong uptake in industrial zones | Medium term (2–4 years) |

| Growing demand for high-albedo tiles that reduce cooling loads | +0.9% | Central & Western regions with high solar exposure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Residential Construction Under Vision 2030

Vision 2030’s Sakani program delivered 374,000 housing units in 2024, each averaging 120 m² of tile-covered areas across kitchens, bathrooms, and living spaces. Mortgage rules that broadened borrower eligibility raised the home-ownership rate by 47% compared with 2024, injecting sustained demand into the Saudi Arabia Tiles Market[2]Saudi Central Bank, “Housing Program Annual Report 2024,” sama.gov.sa. . Developers specify material lifespans of at least 25 years, favoring ceramic and porcelain formats that demonstrate low water absorption and thermal-shock resistance. Riyadh, Jeddah, and King Abdullah Economic City account for most approved building permits, concentrating distribution flows into these zones. Suppliers leverage localized warehousing to maintain just-in-time inventory levels, mitigating stock-outs on fast-moving SKUs.

Government-Backed Giga-Projects Pipeline

NEOM’s USD 500 billion megacity is slated to consume more than 15 million m² of tiles across residential, commercial, and infrastructural footprints by 2030 [3]NEOM Company, “Development Updates,” neom.com. . The Red Sea Project’s hospitality cluster requires slip-resistant and high-albedo roof tiles that cut cooling loads by up to 30% versus conventional materials. Qiddiya and Diriyah Gate enlarge premium demand pools for decorative porcelain mosaics, while remote project sites prioritize suppliers with agile logistics and on-site storage capabilities. Tile makers respond by adding capacity for large-format slabs and photovoltaic-integrated roof systems, aligning with Saudi green-building mandates. This multi-regional pipeline locks in long-range order books and stabilizes factory utilization rates.

Preference Shift Toward Ceramic & Porcelain Tiles

Porcelain’s moisture-absorption rate below 0.5% delivers durability in Saudi Arabia’s heat and sandstorm conditions. Digital printing enables ceramic tiles to mimic marble or wood at 40–60% lower installed cost, accelerating adoption among middle-income homeowners. Large-format sizes such as 600×600 mm reduce grout lines, boosting aesthetic appeal and ease of cleaning. Premium buyers increasingly select rectified edges and 3D textures, reinforcing the migration away from vinyl and carpet. Local manufacturers scale up porcelain kilns to reclaim import share, while importers reposition as specification partners on luxury projects.

Improved Retail & Logistics Infrastructure

Saudi Arabia invested USD 147 billion in logistics upgrades that now include specialized tile distribution centers equipped with automated stacking cranes and climate-controlled storage. Freight rail links connecting Dammam, Riyadh, and Jeddah cut transit time by 35%, trimming breakage rates by 22% and lowering landed costs on imported products. Regional distributors integrate e-commerce platforms that allow contractors to schedule just-in-time deliveries to urban job sites, minimizing project delays. Smaller producers leverage third-party warehousing to expand geographic reach without heavy capital outlays. The Saudi Railway Company's freight services now handle 2.3 million tons of construction materials annually, including tiles, compared to 800,000 tons in 2023. Collectively, these enhancements elevate service levels, widen product variety, and underpin the Saudi Arabia Tiles Market growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas & raw-material prices | −0.9% | National manufacturing hubs | Short term (≤ 2 years) |

| Rising competition from resilient flooring (LVT, SPC) | −0.6% | Urban commercial areas | Medium term (2-4 years) |

| Water-scarcity constraints on ceramic production processes | -0.5% | Drought-prone industrial regions | Medium term (2–4 years) |

| Import dependence for specialty glazes & pigments | -0.4% | National, with concentration in design-centric segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Gas & Raw-Material Prices

Ceramic kilns account for the majority of manufacturing energy use, exposing producers to significant cost swings when natural gas prices fluctuate sharply each quarter. Key raw materials like feldspar, clay, and silica sand saw notable price increases in 2024 due to export limits and global shipping disruptions. Larger tile manufacturers have mitigated some of this volatility by hedging energy inputs and installing regenerative burners to improve efficiency. In contrast, smaller firms struggle to absorb rising costs, facing tighter margins and limited flexibility. Some facilities are experimenting with solar-assisted kiln pre-heating, which can reduce gas usage by up to one-fifth. Although many companies rely on price pass-through to maintain revenue, extended procurement timelines and higher interest rates are creating added pressure on working capital.

Rising Competition from Resilient Flooring

Luxury vinyl tile (LVT) and stone plastic composite (SPC) have gained significant traction in commercial interiors, especially among developers seeking faster project turnaround due to their shorter installation times. Advancements in digital printing and surface embossing have enhanced their appearance, allowing these materials to closely mimic natural stone and wood finishes. This has positioned them as viable alternatives to entry-level ceramic tiles in design-driven projects. However, ceramic still holds a strong advantage in areas with high moisture exposure and where Class A fire-rating compliance is essential. To stay competitive, tile manufacturers are introducing thin-body porcelain slabs that reduce installation time significantly. Additionally, industry-led installer training and warranty programs are helping to reinforce confidence in ceramic solutions, limiting market share loss to resilient flooring options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Performance Gap Drives Roof-Tile Upswing

The roof-tile sub-segment is the Saudi Arabia Tiles Market’s fastest riser, posting an 8.54% CAGR to 2031 as cool-roof mandates set solar-reflectance index (SRI) benchmarks above 78. Floor tiles occupy 49.12% of the Saudi Arabia Tiles Market share thanks to sustained residential construction, while wall tiles secure decorative equity in bathrooms and feature walls. Large-format flooring slabs (≥1200×600 mm) enhance installation speed and create open-plan aesthetics valued in modern villas. Roof-tile makers integrate reflective pigments and photovoltaic laminates, turning rooftops into passive energy assets. Distributors profile SKUs by climate zone, recognizing coastal versus inland thermal loads that influence product mix. Contractors adopt mechanized hoisting rigs to install lighter concrete-based roof tiles that cut structural loads. Insurance providers endorse high-albedo roofs because they lower cooling costs and extend membrane life, creating an ecosystem pull for the sub-segment.

The floor-tile category continues to dominate absolute volume yet faces price pressures from import-heavy SKUs. Market leaders use digital glazing lines to personalize patterns without delaying cycle times, maintaining margins. Wall-tile demand benefits from hospitality fit-outs in Makkah and Madinah, where decorative mosaics support premium room rates. Simultaneously, emerging DIY channels in Riyadh’s retail corridors introduce click-system ceramic planks that allow homeowner installation with minimal tools. Cross-promotion campaigns pair grout additives with antibacterial properties, elevating customer lifetime value. Episodic buying cycles for renovation projects create opportunity windows for promotions tied to Islamic holidays and marriage seasons.

By Material: Porcelain’s Premium Proposition

Ceramic slots 49.68% of the Saudi Arabia Tiles Market size in 2025, yet porcelain accelerates at a 7.61% CAGR courtesy of its sub-0.5% porosity and color-body composition that masks surface wear. Digital roll-printing facilitates hyper-realistic Carrara marble and travertine visuals, capturing the luxury segment without marble’s maintenance liabilities. Producers advocate porcelain for exterior cladding in coastal cities, emphasizing salt-spray resistance. Retailers consolidate merchandising displays around “performance zones,” enabling consumers to compare scratch, stain, and slip metrics across materials. Natural stone and mosaic tiles pivot toward niche spa resorts and palace restorations, preserving heritage aesthetics. Bio-based composite tiles—made from rice husk ash and recycled glass—enter pilot projects that aim for LEED and Mostadam certifications.

Investments in vertical kilns and fast-fire technology reduce porcelain firing times to under 40 minutes, boosting capacity utilization and mitigating energy cost exposure. Color-through porcelain formats command 20–30% price premiums, improving revenue mix even during cyclical slowdowns. Importers from Spain and Italy deepen Saudi distribution partnerships, but local porcelain output climbs as players secure low-interest SIDF loans. Glaze suppliers localize production of metallic and pearlescent finishes, cutting lead times by 45%. Product education campaigns teach contractors optimal thinset usage, lessening callbacks linked to hollow-sound tile debonding.

By End User: Commercial Schemes Gain Velocity

Residential customers accounted for 57.05% share of the Saudi Arabia Tiles Market in 2025, primarily driven by mortgage incentives and government-funded housing clusters. Yet commercial demand is projected to outpace at 8.42% CAGR through 2031 as hospitality, retail, and mixed-use hubs proliferate under economic diversification blueprints. Hotels and resorts alone will require an estimated 8 million m² of tiles each year, specifying large-format porcelain for lobby grandeur and anti-slip ceramic for wet areas. Shopping-mall developers favor high-traffic-rated porcelain and matte textures that minimize glare. Corporate campuses, anchored by international tenants, choose ventilated façade tile systems that raise energy efficiency by 11%.

Residential renovation cycles shorten as young households upgrade starter units within five years, underpinning repeat demand for mid-price ceramic SKUs. E-commerce platforms deliver visualization apps that allow homeowners to preview tile layouts in augmented reality, lifting conversion rates. Commercial project owners negotiate performance guarantees that bundle tiles with installation and maintenance services, shifting the supply chain toward turnkey models. Facility managers document total-cost-of-ownership savings from porcelain’s scratch resistance, reinforcing material preference over resilient flooring in heavy-traffic zones.

Geography Analysis

Riyadh-anchored Central Region held a 33.10% Saudi Arabia Tiles Market share in 2025 on the back of robust public-sector spending, New Murabba’s cultural district, and administrative expansions. Construction permits in the region climbed 28% year on year, supporting sustained demand across floor, wall, and roof tiles. Contractors benefit from proximity to large factories and distribution centers that maintain buffer inventory, shortening procurement cycles. Retail showrooms in Riyadh display augmented reality booths, improving consumer engagement and raising upselling potential. Western Region followed closely at 32.25%, leveraging Jeddah’s port logistics, religious tourism inflows into Makkah and Madinah, and premium coastal developments along the Red Sea. Developers in the Red Sea Project specify enhanced slip resistance and color stability to withstand saline air and UV exposure. Tile import volumes through Jeddah Islamic Port hit 1.8 million tons in 2024, positioning the region as the primary entry point for European and Asian products. Retailers enjoy short lead times on exotic designs, widening style selection for upscale villas.

Eastern Region captured 18.05% share, driven by industrial city expansions in Jubail and Dammam that demand chemical-resistant floor tiles for petrochemical and logistics facilities. The area benefits from abundant silica deposits, lowering raw-material transport costs for nearby tile plants. Heavy-duty thickness formats (≥20 mm) find traction in outdoor pedestrian areas subject to forklift traffic and oil spills. Manufacturers co-locate glaze mills near Qatif clay quarries, securing stable feedstock supply. Northern Region projects the fastest 10.52% CAGR as NEOM’s entirely new urban footprint necessitates mass procurement of façade, pavement, and interior tiles. Supply chains undergo transformation, with modular warehouses and inland container depots mitigating the long haul from Jeddah. Southern Region keeps a modest 5.80% share, yet infrastructure rollouts along the Yemen border and agriculture hub investments sustain baseline demand.

Competitive Landscape

The Saudi Arabia tiles market is moderately concentrated, with a few dominant players accounting for the majority of national sales, while a long tail of over 30 local and import-driven competitors adds pricing complexity and innovation pressure. Saudi Ceramic Company maintains market leadership, benefiting from end-to-end manufacturing integration and a widespread distribution footprint. RAK Ceramics follows, leveraging its strong presence in large-scale construction projects and its ability to meet strict specification standards. These top players emphasize vertical integration, ensuring control over raw material sourcing, production, and final delivery to strengthen margins and improve reliability. This approach helps mitigate supply chain risks and enhances responsiveness to large-scale demand. However, fragmentation among smaller players continues to shape the competitive landscape.

Technology adoption is becoming a key competitive differentiator across the market. Leading manufacturers are investing in advanced digital printing, automation, and energy-efficient kiln technologies to reduce costs and improve consistency. These upgrades support faster product innovation cycles and allow for greater customization. Efficiency in production also enables companies to handle more complex orders and meet evolving design trends. Additionally, there's growing interest in smart production systems that support sustainable operations and quality tracking. These advancements are helping major players stay ahead in a market facing increased import competition[4]General Authority for Statistics, “Construction Permits,” stats.gov.sa..

Market opportunities are emerging in niche and high-performance segments. Specialized categories like photovoltaic roof tiles and heavy-duty commercial flooring are creating new growth paths that require technical capabilities and R&D investment. Smaller players are disrupting the luxury residential segment by offering eco-friendly materials and tailored design options. These offerings appeal to environmentally conscious consumers and premium developments. Meanwhile, established players are under pressure to manage costs amid volatile raw material prices and aggressive imports. As a result, innovation, differentiation, and supply chain agility are becoming critical to long-term market positioning.

Saudi Arabia Tiles Industry Leaders

Saudi Ceramic Company

RAK Ceramics (KSA operations)

Future Ceramics

Arabian Tile Co. (ARTIC)

Alfanar Ceramics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Saudi Ceramic Company announced a USD 85 million capacity expansion at its Riyadh facility, adding 15 million square meters of annual production capacity focused on large-format porcelain tiles. The expansion includes advanced digital printing technology and automated handling systems to serve Vision 2030 project requirements.

- August 2024: RAK Ceramics secured a USD 45 million supply contract for NEOM's residential phase, covering 3.2 million square meters of specialized tiles with enhanced durability specifications for extreme weather conditions. The contract includes on-site technical support and customized logistics solutions.

- July 2024: Future Ceramics completed its USD 120 million automated manufacturing plant in Jubail, featuring energy-efficient kiln technology that reduces natural gas consumption by 25% compared to conventional systems. The facility targets premium porcelain production for commercial and hospitality applications.

- June 2024: Arabian Tile Company (ARTIC) launched its high-albedo roof tile line meeting Saudi Building Code SRI requirements above 78, targeting the growing cool-roof market segment. The product line includes integrated solar reflective coatings and 25-year performance warranties.

Saudi Arabia Tiles Market Report Scope

A complete background analysis of the Saudi Arabia tiles market, which includes an assessment of the National accounts, economy, and the emerging market trends by segments, significant changes in the market dynamics, and the market overview is covered in the report.

| Floor Tiles |

| Wall Tiles |

| Roof Tiles |

| Ceramic |

| Porcelain |

| Natural Stone & Mosaic |

| Others |

| Residential |

| Commercial |

| Central Region (Riyadh) |

| Western Region (Makkah & Madinah) |

| Eastern Region (Dammam & Al-Khobar) |

| Northern Region |

| Southern Region |

| By Type | Floor Tiles |

| Wall Tiles | |

| Roof Tiles | |

| By Material | Ceramic |

| Porcelain | |

| Natural Stone & Mosaic | |

| Others | |

| By End User | Residential |

| Commercial | |

| By Geography | Central Region (Riyadh) |

| Western Region (Makkah & Madinah) | |

| Eastern Region (Dammam & Al-Khobar) | |

| Northern Region | |

| Southern Region |

Key Questions Answered in the Report

How large is the Saudi Arabia Tiles Market in 2026?

The market is valued at USD 129.13 billion in 2026 and is forecast to reach USD 166.52 billion by 2031.

Which tile type is growing the fastest?

Roof tiles post the highest 8.54% CAGR thanks to energy-efficient cool-roof mandates.

Why is porcelain gaining share over ceramic?

Porcelain delivers sub-0.5% water-absorption, superior durability, and premium aesthetics, pushing its 7.61% CAGR.

Which region leads in tile demand?

Riyadh-anchored Central Region commands 33.10% market share due to active public-sector construction.

Who are the leading manufacturers?

Saudi Ceramic Company, RAK Ceramics, Future Ceramics, Alfanar Ceramics, and Arabian Tile Company are the leading manufacturers.

Page last updated on: