Saudi Arabia Refrigerated Trailer Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

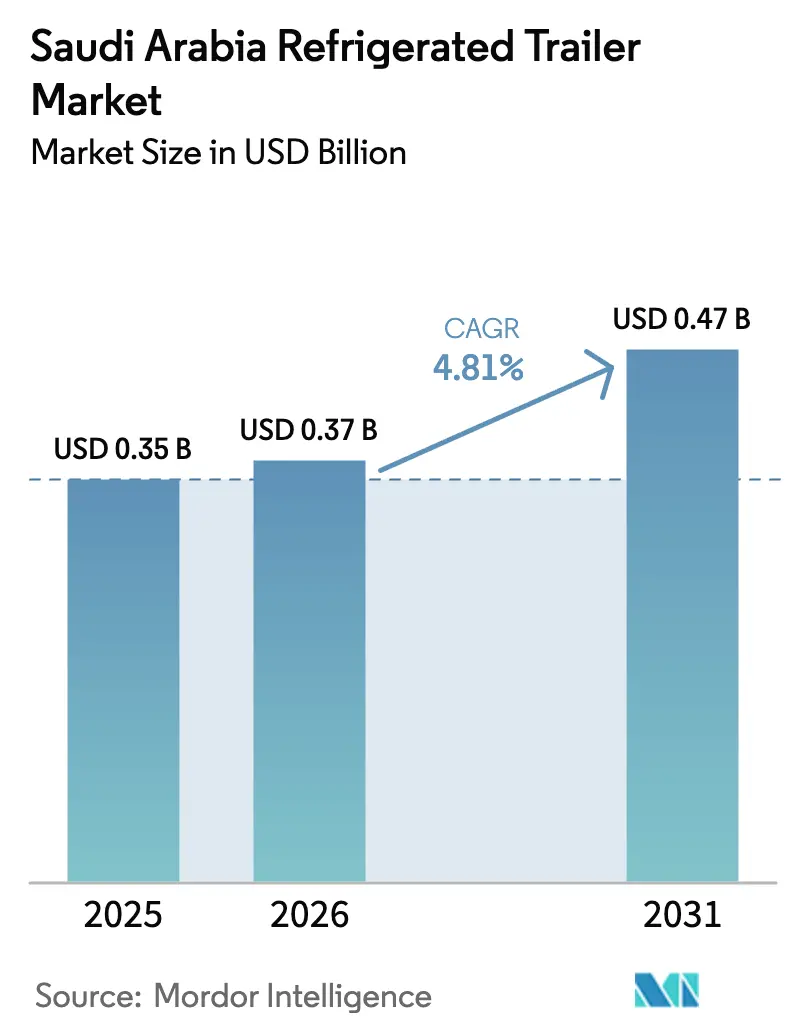

| Base Year Market Size (2025) | USD 0.35 Billion |

| Market Size (2026) | USD 0.37 Billion |

| Market Size (2031) | USD 0.47 Billion |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Refrigerated Trailer Market Analysis by Mordor Intelligence

The Saudi Arabia refrigerated trailer market was valued at USD 0.35 billion in 2025 and estimated to grow from USD 0.37 billion in 2026 to reach USD 0.47 billion by 2031, at a CAGR of 4.81% during the forecast period (2026-2031). This measured trajectory sits against Vision 2030’s National Transport & Logistics Strategy, which will create 59 logistics centers covering more than 100 million m² to accelerate just-in-time cold-chain flows[1]“National Transport & Logistics Strategy,” Saudi Ministry of Transport, mot.gov.sa. Saudi Arabia relies on food imports for a notable share of consumption, generating persistent demand for temperature-controlled transport despite a maturing fleet and high replacement costs. Modern retail expansion, the surge of e-grocery platforms, and stringent Saudi Food & Drug Authority (SFDA) regulations favor higher-specification units with continuous monitoring systems. Meanwhile, Coldstores Group’s significant hold on the Saudi Arabia refrigerated trailer market underscores an asymmetrical competitive field where global brands compete mainly on technology differentiation.

Key Report Takeaways

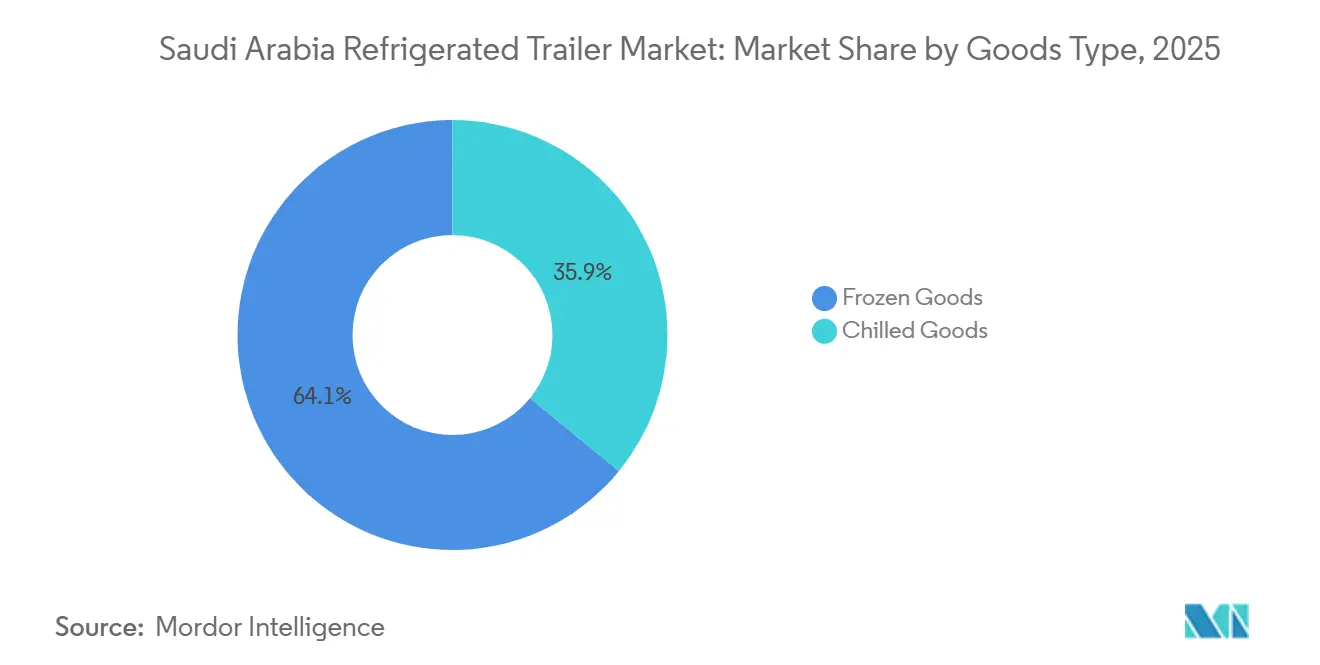

- By goods type, frozen goods led with a 64.11% share of the Saudi Arabian refrigerated trailer market in 2025, while chilled goods are forecast to expand at a 5.61% CAGR through 2031.

- By application, meat and seafood accounted for 40.22% of the Saudi Arabian refrigerated trailer market size in 2025, whereas healthcare and medicines are projected to grow at a 7.64% CAGR through 2031.

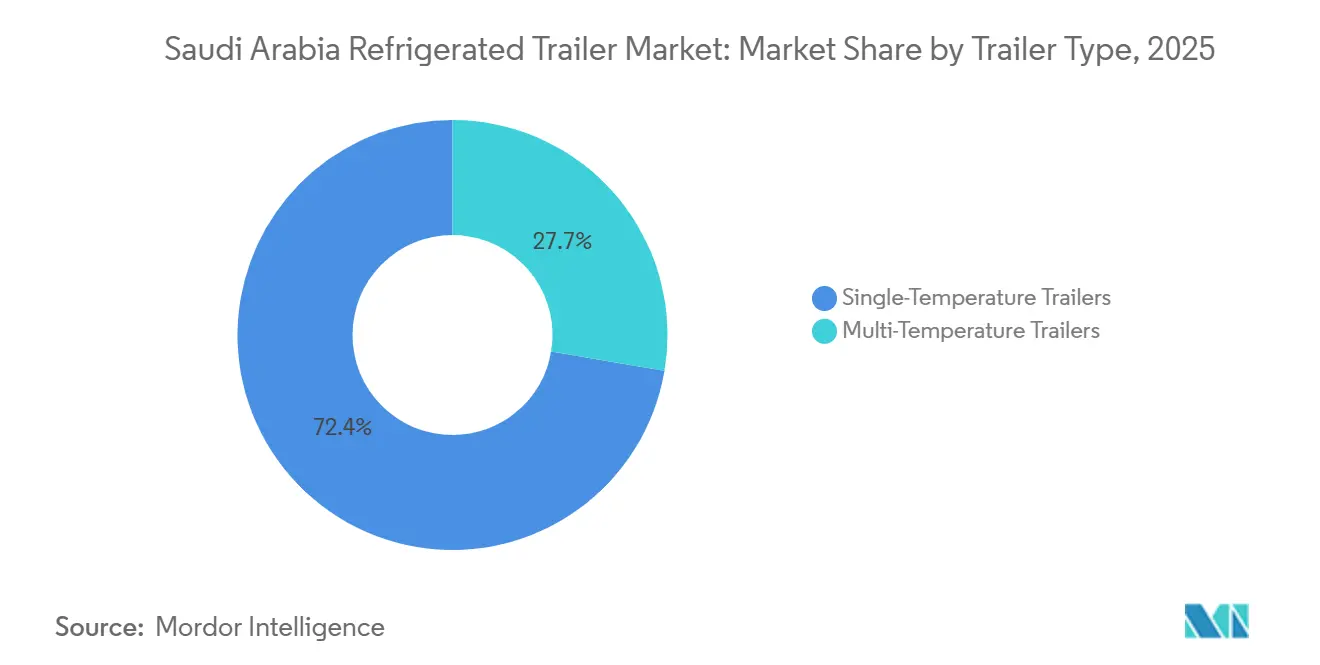

- By trailer type, single-temperature units dominated the Saudi Arabian refrigerated trailer market with 72.35% of the market share in 2025; multi-temperature designs are anticipated to grow at an 8.05% CAGR through 2031.

- By end-user industry, food & beverage accounted for 48.13% of the Saudi Arabian refrigerated trailer market in 2025, yet healthcare is set to post a 7.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi arabia contributes to a system defined not by any single country or region but by the interaction of many. The global refrigerated trailer market data by Mordor Intelligence represents that combined structure.

Saudi Arabia Refrigerated Trailer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Logistics Investment | +1.4% | King Abdullah Economic City, NEOM, Dammam zones | Long term (≥ 4 years) |

| Rising Frozen Food Import | +1.2% | Jeddah, Dammam, Riyadh corridors | Medium term (2-4 years) |

| Retail and Distribution Center Expansion | +0.9% | Riyadh, Jeddah, Eastern Province | Short term (≤ 2 years) |

| E-Grocery Quick Commerce Surge | +0.8% | Riyadh, Jeddah, Dammam, Mecca, Medina | Short term (≤ 2 years) |

| HACCP SFDA Cold-Chain Enforcement | +0.7% | National | Medium term (2-4 years) |

| Solar Hybrid TRU Deployment | +0.5% | Solar-rich regions nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Logistics-Hub Investments

By 2030, Vision 2030 aims to significantly improve the Logistics Performance Index ranking, with steady progress already underway. 59 planned logistics centers exceed 100 million m², each allocating space for 40-ft reefer traffic. Maersk’s 13,300 m² Dammam site, opened in 2023, provides 168,000 pallet positions and a 600 kWp solar array. Port throughput is expected to grow significantly by 2030, with efforts underway to minimize refrigerated-container dwell time. These advancements are driving just-in-time trailer operations and strengthening the refrigerated trailer market in Saudi Arabia.

Growing Frozen-Meat and Seafood Import Volumes

In recent years, Saudi Arabia has strengthened its reliance on protein imports, with significant volumes of frozen poultry and seafood being brought into the country. While frozen goods have traditionally dominated utilization, a growing trend is for chilled goods to expand faster as warehouses strategically position inventory closer to urban centers. The SFDA mandates strict temperature controls during transit, a requirement that most tier-one fleets have already incorporated into their operations. During peak periods, such as Ramadan, surges in poultry imports have placed pressure on reefer capacity at key ports. This volatility has created opportunities for asset-light firms, which prefer renting trailers on demand rather than maintaining dedicated frozen fleets.

Expansion of Modern Retail Chains and Distribution Centers

In 2024, Carrefour expanded its Riyadh hub with additional refrigerated trucks, significantly enhancing its same-day order capabilities. Lulu, with a strong presence across Saudi Arabia, plans further expansion in the coming years, which is expected to increase fleet demands. Retailers are increasingly adopting multi-temperature trailers capable of co-loading frozen, chilled, and ambient stocks, improving operational efficiency by reducing unnecessary mileage. Amazon, through its collaboration with Al Othaim Markets, is leveraging AI routing to optimize reefer operations and reduce inefficiencies. Meanwhile, smaller grocers, lacking advanced telematics systems, face challenges in achieving similar efficiencies, driving consolidation within Saudi Arabia's refrigerated trailer market.

Surge in E-Grocery/Quick-Commerce Last-Mile Demand

In 2024, e-grocery sales demonstrated significant growth potential, with market penetration remaining low. Platforms like Rabbit, promising rapid deliveries, are limiting their logistics to chilled vehicles set at specific temperature points. As a result, chilled goods are growing at a faster pace compared to frozen ones. Amazon has introduced its Prime grocery delivery in key cities, embedding cold-chain services into its subscription model. In the competitive landscape of Saudi Arabia's refrigerated trailer market, traditional wholesalers face a pivotal choice: retrofit their fleets or risk obsolescence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Maintenance Costs | -0.6% | Nationwide, acute need for small and mid-size fleets | Medium term (2-4 years) |

| Dependence on Imported Trailer Bodies | -0.4% | Jeddah and Dammam supply chains | Short term (≤ 2 years) |

| Shortage of Reefer Technicians | -0.3% | Regional cities and rural corridors | Long term (≥ 4 years) |

| Insulation Degradation in Desert | -0.2% | Central and northern desert zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex and Specialized Maintenance Costs

In Saudi Arabia, a 13.6 m refrigerated trailer equipped with a Carrier Transicold unit is considered a significant investment. TRU services, required at regular intervals, substantially increase maintenance costs compared to dry freight. Additionally, sand infiltration reduces condenser efficiency, increasing fuel consumption. Neglecting maintenance can disrupt operations and result in regulatory fines and delays from the SFDA. These operational challenges are driving smaller firms to prefer leasing, which is contributing to the consolidation of fleet ownership in the Saudi refrigerated trailer market.

Dependence on Imported Trailer Bodies/Reefer Units

Saudi Arabia's imports of air-conditioning parts have been significant, with a substantial portion sourced from China. In 2024, disruptions in the Red Sea have led to extended TRU lead times. While CIMC's plant in Bahrain supplies products to Saudi Arabia, it still relies on components manufactured in China. Additionally, potential tariffs could increase landed costs, contributing to price volatility in the refrigerated trailer market within the country.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Goods Type: Chilled Goods Accelerate on Fresh-Produce Delivery

Chilled cargo accounted for a notable share of the Saudi Arabia refrigerated trailer market in 2025 and is projected to grow at a 5.61% CAGR through 2031. This advance contrasts with the larger frozen segment, which held a 64.11% share in 2025 but grows more slowly as protein inventory shifts to near-city warehouses.

Quick-commerce platforms, Amazon Prime grocery, and Carrefour’s high-velocity fulfillment all depend on ≤ 5 °C setpoints, spurring demand for smaller loads but higher trip frequency. Continuous SFDA monitoring rules increase compliance costs, favoring branded fleets. As a result, chilled loads will close the gap with frozen, reshaping routing patterns across the Saudi Arabian refrigerated trailer market.

By Application: Healthcare Logistics Gains Momentum

Meat and seafood maintained the most significant share at 40.22% in 2025, but face price-driven margin pressure. Vision 2030’s push to localize biologics production with firms such as Sanofi and Novo Nordisk amplifies healthcare’s pull on the Saudi Arabia refrigerated trailer market, while seasonal protein import spikes keep meat and seafood volumes stable.

Healthcare and medicines represented the highest CAGR potential at 7.64% through 2031, the fastest among applications—GDP-compliant containers enforcing ±0.5 °C tolerance command significant price premiums, encouraging specialized providers to expand capacity.

By Trailer Type: Multi-Temperature Units Gain Share

Single-temperature designs dominated the Saudi Arabian refrigerated trailer market with 72.35% share in 2025, yet are forecast to lose share to multi-zone builds, which are growing at 8.05% through 2031. Dual-evaporator rigs cost more but cut fuel and improve load consolidation.

Retail giants co-load frozen meals, dairy, and pantry staples to reduce empty miles, and Coldstores Group supplies ATP-approved multi-temperature units with significant conductivity. Rising demand signals a structural mix shift in the Saudi Arabian refrigerated trailer market.

By End-User Industry: Healthcare Outpaces Food & Beverage

Food & beverage accounted for 48.13% of the Saudi Arabian refrigerated trailer market share in 2025, owing to a significant food import bill. However, healthcare is projected to expand at a 7.13% CAGR to 2031 as NUPCO builds four new pharma DCs [2]“Pharmaceutical Logistics Centers,” NUPCO, nupco.com.

Biologics, vaccines, and insulin pens require tighter controls than frozen protein, lifting fleet-specification levels. Industrial chemicals remain niche due to SASO conformity rules, leaving healthcare as the clear growth engine in the Saudi Arabia refrigerated trailer industry.

Geography Analysis

Riyadh, Jeddah, and Dammam, benefiting from their proximity to ports and dense consumer bases, dominate the national reefer utilization [3]“Container Dwell Time Report,” Saudi Ports Authority, mawani.gov.sa. These cities play a critical role in supporting the refrigerated trailer market due to their strategic locations and high demand for cold-chain logistics. Meanwhile, the Eastern Province also contributes significantly to utilization but faces challenges related to elevated maintenance costs driven by environmental factors such as humidity.

In 2024, Saudi Arabia achieved notable progress in its Logistics Performance Index, reflecting improvements in the efficiency of its logistics infrastructure. The reduction in clearance times for refrigerated containers has streamlined operations, enabling faster movement of goods and reducing the need for excessive inventory storage. These developments have positively impacted the refrigerated trailer market by enhancing operational efficiency and supporting quicker turnaround times.

While urban centers have made significant advancements, rural areas continue to face challenges in cold-chain infrastructure. A limited presence of modern cold storage facilities in distribution centers has led to inefficiencies, including longer transportation routes that affect profitability. However, with planned developments such as NEOM and King Abdullah Economic City expected to introduce dedicated cold-chain zones later in the decade, the refrigerated trailer industry in Saudi Arabia is poised for a more balanced and geographically inclusive growth trajectory.

The refrigerated trailer market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for Indonesia and Malaysia, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Coldstores Group holds a significant share of Saudi Arabia's refrigerated trailer market, supported by its strategic initiatives, including a forthcoming IPO and the establishment of a new factory in Al-Kharj. The company employs an advanced open-pour sandwich-panel process that ensures superior insulation capable of meeting stringent ATP and SASO standards, even under extreme heat.

Globally, competitors such as Schmitz Cargobull, Great Dane, and CIMC Vehicles focus on innovation in telematics and electric-reefer technologies to strengthen their market positions. CIMC, leveraging its regional hub in Bahrain, has been actively expanding its presence in the electric trailer segment, showcasing its commitment to technological advancements in the industry.

Local manufacturers, including Alshehili and Sharaf Din, primarily target cost-conscious fleet operators. However, they face challenges in research and development, particularly in solar-hybrid transport refrigeration units (TRUs). Additionally, concerns about subscription costs and data privacy have slowed the adoption of predictive maintenance solutions, resulting in uneven technological integration across Saudi Arabia's refrigerated-trailer sector.

Saudi Arabia Refrigerated Trailer Industry Leaders

Schmitz Cargobull

Utility Trailer Manufacturing Company, LLC

Coldstores Group of Saudi Arabia (CGS)

TSSC Group

Alshehili Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Alshehili Metal Industries won a SAR 3.56 million (~USD 0.95 million) contract to build and deliver 10 refrigerated trailers within 11 weeks.

- August 2025: Alshehili Metal Industries received a SAR 17.97 million (~USD 4.79 million) purchase order from Almarai to supply 73 refrigerated trailers over a three-month period.

Saudi Arabia Refrigerated Trailer Market Report Scope

The scope includes segmentation by goods type (frozen goods and chilled goods), application (dairy, meat and seafood, fruits and vegetables, healthcare/medicines, and others), trailer type (single-temperature trailers and multi-temperature trailers), and end-user industry (food and beverage, retail and distribution, healthcare, and industrial). Market size and growth forecasts are presented by value in USD.

| Frozen Goods |

| Chilled Goods |

| Dairy |

| Meat and Seafood |

| Fruits and Vegetables |

| Healthcare / Medicines |

| Others |

| Single-Temperature Trailers |

| Multi-Temperature Trailers |

| Food and Beverage |

| Retail and Distribution |

| Healthcare |

| Industrial |

| By Goods Type | Frozen Goods |

| Chilled Goods | |

| By Application | Dairy |

| Meat and Seafood | |

| Fruits and Vegetables | |

| Healthcare / Medicines | |

| Others | |

| By Trailer Type | Single-Temperature Trailers |

| Multi-Temperature Trailers | |

| By End-User Industry | Food and Beverage |

| Retail and Distribution | |

| Healthcare | |

| Industrial |

Key Questions Answered in the Report

What will be the market value of refrigerated trailers in Saudi Arabia in 2026?

The market stands at USD 0.37 billion in 2026 and is forecast to hit USD 0.47 billion by 2031.

How fast will chilled-goods transport grow?

Chilled cargo is set to expand at a 5.61% CAGR through 2031 as e-grocery and fresh-produce demand rises.

Which segment is growing quickest by application?

Healthcare logistics leads with a 7.64% CAGR driven by new pharma distribution centers and biologics handling.

What technology trends shape fleet upgrades?

Multi-temperature trailers, solar-hybrid TRUs, and telematics for predictive maintenance are the key upgrades.

Page last updated on: