Saudi Arabia Luxury Residential Real Estate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

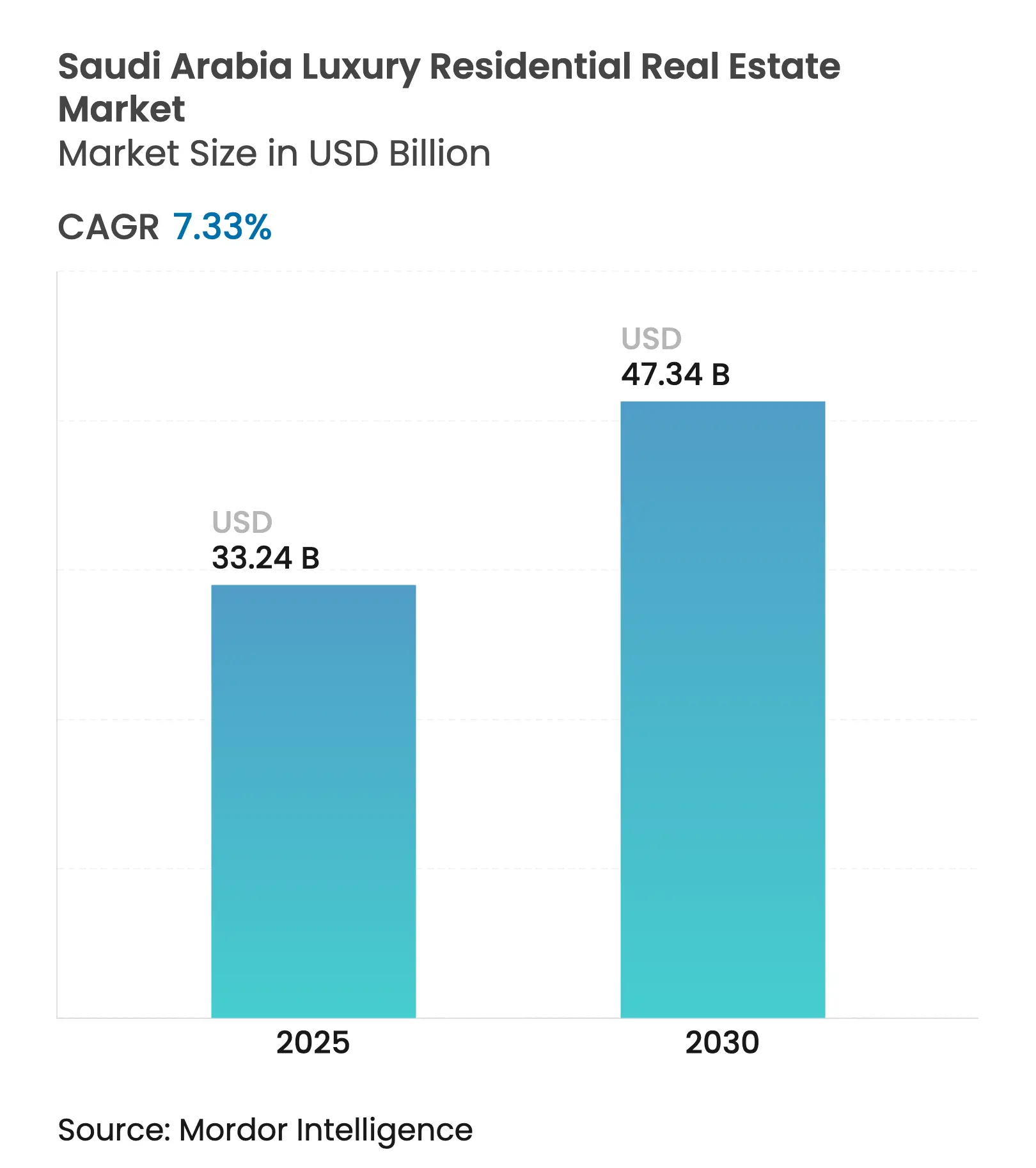

| Market Size (2025) | USD 33.24 Billion |

| Market Size (2030) | USD 47.34 Billion |

| Growth Rate (2025 - 2030) | 7.33 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Saudi Arabia Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Saudi Arabia luxury residential real estate market size stood at USD 33.24 billion in 2025 and is forecast to climb to USD 47.34 billion by 2030, registering a 7.33% CAGR over 2025-2030. This steady trajectory mirrors Vision 2030’s push to diversify income, embed advanced technology, and elevate environmental standards within premium housing. Mega-projects such as NEOM, New Murabba, and Red Sea Global expand the supply of high-specification units, while a 32% jump in the country’s high-net-worth population since 2013 maintains robust demand. Expatriate executives relocating regional headquarters to Riyadh and Jeddah add depth to the renter pool, as do new foreign-ownership rules scheduled for 2026 that remove residency requirements for select zones. Developers combat construction-cost inflation by adopting modular building and strategic sourcing, but sovereign wealth backing and stable oil receipts buffer the sector from macro volatility.

Key Report Takeaways

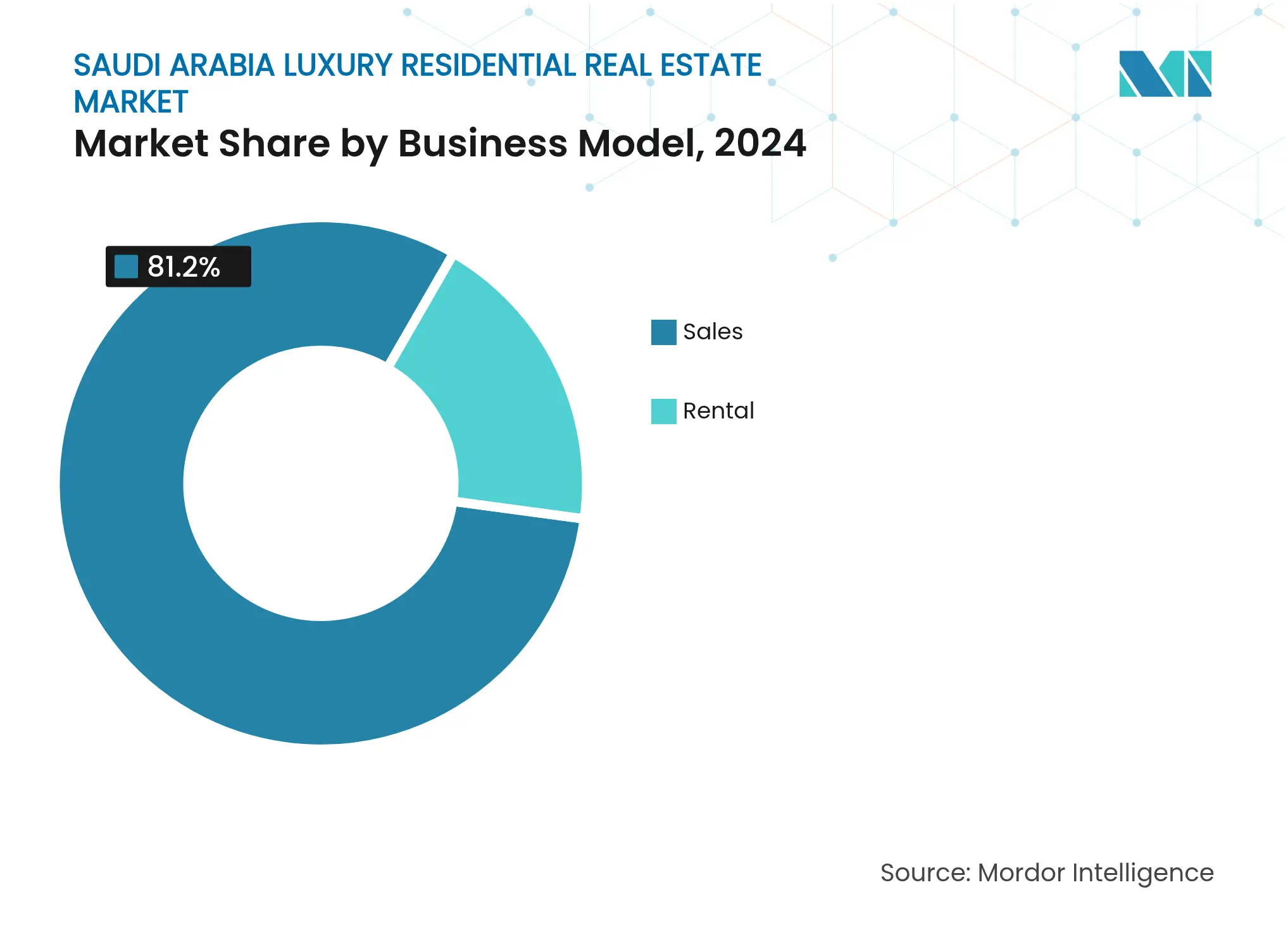

- By business model, sales commanded 81.2% revenue share in 2024; rentals are projected to advance at an 8.02% CAGR to 2030.

- By property type, villas and landed houses held 67.8% of the Saudi Arabia luxury residential real estate market share in 2024, while apartments and condominiums are set to grow at an 8.16% CAGR through 2030.

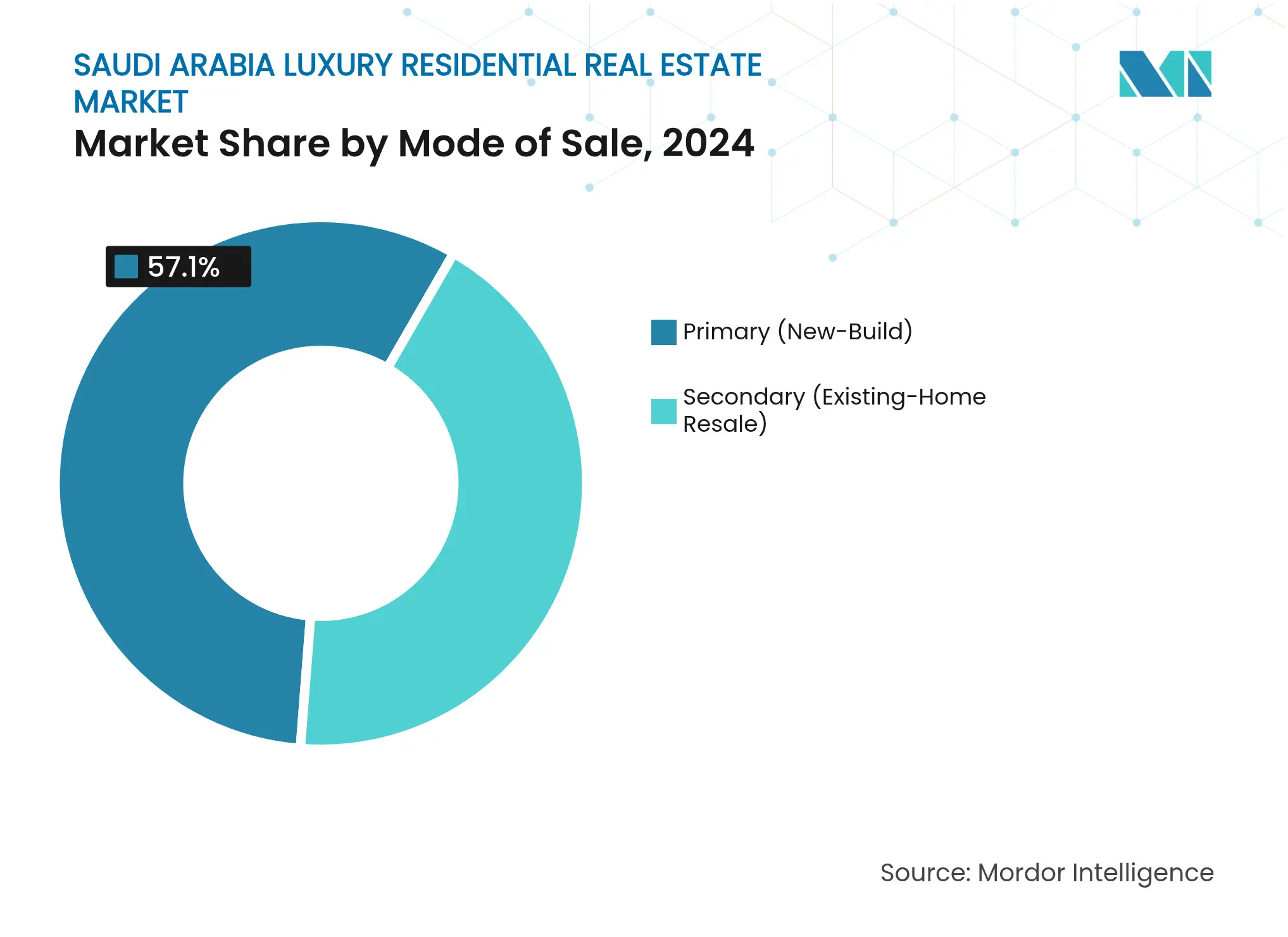

- By mode of sale, primary transactions accounted for 57.1% of the Saudi Arabia luxury residential real estate market size in 2024 and are poised for an 8.31% CAGR over the period.

- By city, Riyadh dominated with 46.9% share in 2024; the Dammam metropolitan area is on track for the fastest 8.56% CAGR through 2030.

Saudi Arabia Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Vision

2030 initiatives promoting luxury mixed-use and waterfront developments

Vision

2030 initiatives promoting luxury mixed-use and waterfront developments

| +2.1% | Riyadh, Jeddah, NEOM corridor | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+2.1%

|

Geographic

Relevance

:

Riyadh,

Jeddah, NEOM corridor

|

Impact

Timeline

:

Long

term (≥ 4 years)

|

Rising

HNWI population fueling demand for luxury villas and apartments

Rising

HNWI population fueling demand for luxury villas and apartments

| +1.8% | National, concentrated in Riyadh and Jeddah | Medium term (2-4 years) | |||

Growing

expatriate and executive population driving demand for premium gated

communities

Growing

expatriate and executive population driving demand for premium gated

communities

| +1.4% | Riyadh, Eastern Province, Jeddah | Medium term (2-4 years) | |||

Increased

foreign ownership allowances expanding buyer base

Increased

foreign ownership allowances expanding buyer base

| +1.2% | Designated zones in Riyadh and Jeddah | Short term (≤ 2 years) | |||

Preference

for branded residences integrating wellness and smart-home features

Preference

for branded residences integrating wellness and smart-home features

| +0.8% | National, premium developments | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Vision 2030 Mega-Projects Reshaping Supply

Saudi Arabia's Vision 2030 initiative is a cornerstone of the country's economic diversification strategy, driving significant changes in the construction and real estate sectors. NEOM's ambitious USD 500 billion project, New Murabba's downtown plan at USD 267 billion, and Red Sea Global's pipeline of 50 hotels are reshaping the product landscape. Starting late 2025, THE LINE will roll out 9 million residential units along a spine powered by renewables and devoid of cars, setting a new gold standard in sustainability. Mukaab in New Murabba is set to offer a retail and residential experience on par with the world's best, while Red Sea Global is merging hospitality with luxury branded residences, featuring names like Four Seasons and Ritz-Carlton Reserve. Together, these ventures boast a staggering construction value of USD 850 billion, with about a quarter allocated to upscale housing. Developers focusing on eco-friendly credentials and digital integration are poised to seize early advantages.

Rising HNWI Population Fueling Demand

The rising population of high-net-worth individuals (HNWIs) in Saudi Arabia is significantly influencing the luxury real estate market. In 2024, Saudi Arabia boasted a millionaire count of 58,300, with projections indicating a steady ascent. Historically, a 1% rise in the millionaire population has corresponded to a 2.3% increase in premium unit sales, providing developers with a reliable demand forecast. Riyadh, home to over 20,000 millionaires, stands as a prime target for ultra-luxury projects. Meanwhile, Jeddah, with its 10,400 affluent residents, continues to see launches along the Red Sea waterfront. Wealthy younger Saudis are gravitating towards lifestyle assets, such as wellness-focused communities, rather than traditional investments. The state's luxury market is further buoyed by the presence of 22 billionaires and 195 centi-millionaires, driving sales of exclusive trophy villas and branded penthouses. As wealth managers set up shop in Riyadh, an added layer of demand emerges from expatriate executives, amplifying the luxury market's momentum.

Expatriate Executive Housing Momentum

The demand for expatriate executive housing in Riyadh is witnessing significant momentum, driven by the city's growing population and economic development. By 2030, Riyadh's population is projected to hit 9.6 million, with expatriates making up a significant 5.5 million. This surge translates to a demand for 305,000 additional homes, many leaning towards the luxury spectrum. Premium gated communities, like ROSHN’s SEDRA, are setting the tone, rolling out over 30,000 homes in eight phases, echoing the integrated amenities that executives desire. With corporate housing allowances often surpassing USD 100,000 annually, the rental segment is witnessing a robust expansion, currently growing at an 8.02% CAGR. Expatriates typically pay a premium of 15-25% over local rents, ensuring attractive yields for purpose-built rental schemes. When selecting sites, factors like international schools, medical centers, and proximity to Grade-A office hubs play a pivotal role.

Foreign Ownership Liberalization

The Saudi Arabian real estate market is set to undergo significant changes with the introduction of foreign ownership liberalization. Starting January 2026, non-Saudis can buy property in select zones in Saudi Arabia without needing residency. This move could boost the buyer pool by 40-60%, drawing inspiration from Dubai's experience. Additionally, foreign investors can now take up to 49% stakes in listed real-estate firms with assets in Makkah and Madinah, paving the way for fresh capital-market opportunities. Initial signs suggest that Gulf Cooperation Council nationals and Qualified Foreign Investors are leading the charge, with annual transactions expected to hit USD 2-3 billion in just two years. The Real Estate General Authority's regulatory clarity bolsters confidence, and measures like escrow and Wafi off-plan safeguards further promote transparency.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High

construction and land costs increasing overall project pricing

High

construction and land costs increasing overall project pricing

| -1.5% | National, acute in prime urban areas | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-1.5%

|

Geographic

Relevance

:

National,

acute in prime urban areas

|

Impact

Timeline

:

Short

term (≤ 2 years)

|

Regulatory

and procedural complexities slowing approvals in luxury zones

Regulatory

and procedural complexities slowing approvals in luxury zones

| -0.9% | Riyadh, Jeddah, NEOM development areas | Medium term (2-4 years) | |||

Economic

dependence on oil revenues creating volatility in luxury cycles

Economic

dependence on oil revenues creating volatility in luxury cycles

| -0.7% | National, with regional variations | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Construction-Cost Inflation

Saudi Arabia's construction sector is experiencing significant cost pressures due to its ambitious development plans. Saudi Arabia's ambitious USD 1.5 trillion projects are putting a strain on material supplies and specialist labor, leading to a 20-30% inflation in costs compared to regional peers. The push for premium finishes, marble imports, and advanced MEP systems further squeezes luxury margins. Skilled trades are commanding a 15-25% wage premium, and localization mandates, which require additional training, are extending delivery schedules by over six months. While developers are turning to bulk procurement and modular construction to mitigate risks, smaller firms find the capital outlay challenging. Even with scale advantages, sovereign-backed entities are treading carefully on pricing strategies to maintain absorption rates.

Regulatory Complexity

Regulatory challenges significantly impact the real estate market, influencing project timelines and costs. The Real Estate General Authority's complex approval process—covering environmental assessments, cultural heritage clearances, and foreign investment reviews—extends project timelines by 18 to 24 months compared to regional norms. A newly implemented 5% Real Estate Transaction Tax increases compliance costs for high-value transactions. Additionally, luxury developments exceeding USD 50 million undergo stringent foreign-ownership evaluations. Environmental assessments for Red Sea coastline projects require detailed coral-reef studies, which involve additional consultants and delay groundbreaking activities. Although recent digital permit platforms have enhanced transparency, overlapping responsibilities between municipal and federal authorities continue to create bottlenecks[1]Real Estate General Authority, “Regulatory framework updates,” rega.gov.sa.

Segment Analysis

By Business Model: Sales Leadership with Rental Upside

The sales channel captured 81.2% of the Saudi Arabia luxury residential real estate market in 2024, underscoring entrenched ownership culture and wealth-building preferences. Developers leverage wide mortgage products and government subsidy programs to keep payment plans attractive, while off-plan escrow under the Wafi system de-risks early commitments. However, the rental segment’s 8.02% CAGR through 2030 signals evolving preferences. Expatriate executives, rotating project staff, and mobile Saudi professionals value flexibility, driving consistent lease demand in Riyadh’s Diplomatic Quarter and Jeddah’s waterfront towers. ROSHN’s pivot into serviced rentals points to growing institutional interest, and hotel-branded residences such as Vida Jeddah Gate blur hotel and multifamily lines, offering guaranteed yields for investors. Over time, the widening renter base is expected to narrow the share gap, though outright sales will stay dominant thanks to cultural norms favoring deed ownership.

Investors note that the Saudi Arabia luxury residential real estate market size for rentals is slated to expand significantly, yet absolute volume remains smaller than sales. Corporate tenancy agreements, often backed by multi-year contracts, provide predictable cash flow to developers stressed by material-cost inflation. Foreign-ownership liberalization further bolsters rental appetite, as overseas buyers may initially prefer income-generating assets before committing to personal residences. Sales activity remains buoyed by Vision 2030 mega-projects; primary handovers at THE LINE and New Murabba will add thousands of new-build options, reinforcing sales volume leadership through the decade.

By Property Type: Villas Dominate as Apartments Accelerate

Villas and landed houses controlled 67.8% of the Saudi Arabia luxury residential real estate market share in 2024, reflecting cultural emphasis on privacy, large majlis areas, and multi-generational living. Flagship communities such as SEDRA include smart-home controls, private gardens, and wellness domes to retain villa appeal. Yet, high urban land prices and densification strategies have propelled apartment demand, making high-rise units the fastest-growing segment at an 8.16% CAGR. Projects in NEOM’s Gidori district showcase luxury apartments with panoramic Gulf views, digital concierge, and shared clubs, proving vertical living can satisfy affluent tastes. Developers adapt floor plans to include private lifts and duplex formats, thereby bridging villa conveniences within towers.

The Saudi Arabia luxury residential real estate market size for top-tier apartments is forecast to expand notably as millennials and international buyers prioritize location over plot size. Riyadh’s New Murabba aims to deliver skyline residences with integrated retail and cultural attractions, while Jeddah’s canal-front MARAFY district adds yacht berths and beachfront lounges. Villa supply growth persists in outer Riyadh and Eastern Province where land remains comparatively affordable, but shifting demographics are rebalancing the product mix. Smart building codes issued in 2024 ensure apartments match villas on construction-quality metrics, fostering buyer confidence in vertical formats.

By Mode of Sale: Primary Pipeline Drives Growth

Primary transactions accounted for 57.1% of the Saudi Arabia luxury residential real estate market in 2024 and are forecast to log the swiftest 8.31% CAGR. Vision 2030’s giga-projects funnel thousands of off-plan villas and apartments into the market, supplying modern designs, ESG credentials, and developer payment plans unmatched in the secondary arena. Buyers gain from construction-linked installments and warranty coverage, while developers benefit from milestone cash flow that funds ambitious phases. Wafi regulations mandate escrow segregation and monthly progress disclosure, enhancing transparency for primary buyers.

Secondary deals still provide 42.9% of turnover, especially in established enclaves like Al-Khuzama where mature landscaping and embassy proximity command premiums. The Saudi Arabia luxury residential real estate market size for secondary trades should grow steadily, yet older stock faces renovation costs to compete with new-build amenities. Tax exemptions on select primary deals—contrasting with uniform 5% levies on resales—tilt economics toward fresh launches. With Knowledge Economic City funneling USD 1.067 billion in new homes by 2030, the primary channel’s dominance appears locked in through the forecast period[2]TradeArabia, “Vida Jeddah Gate launches serviced apartments,” tradearabia.com.

Geography Analysis

In 2024, Riyadh accounted for 46.9% of the nation's transaction value and had the most extensive pipeline in the country. The New Murabba project is expected to deliver over 104,000 residential units, including observation-deck penthouses within the Mukaab cube. Riyadh's strategy to attract 480 foreign company headquarters by 2030 is driving demand for high-end apartments, particularly near the King Abdullah Financial District. Public Infrastructure Fund initiatives, such as the USD 933 million Sports Boulevard, are enhancing the city's lifestyle appeal, supporting premium pricing despite increasing supply. Rental yields remain steady at approximately 5.5%, supported by strong occupancy from diplomatic staff, consultants, and professionals in the digital economy[3]Sports Boulevard Foundation, “Urban Wadi High Rises investment fund,” sportsboulevard.sa.

Jeddah's coastal location influences its distinct product offerings. The city combines urban living with resort-style amenities through developments like Red Sea Global's hospitality-branded homes, Vida Jeddah Gate's services, and the canal-front MARAFY. Annual pilgrim inflows contribute to a growing luxury short-stay market, while the city's 10,400 millionaires drive demand for larger beachfront villas. Infrastructure improvements at Jeddah Islamic Port and King Abdulaziz International Airport are enhancing connectivity, increasing the city's appeal to regional investors. Apartment towers in Jeddah yield 6% gross returns, slightly higher than Riyadh, reflecting consistent tourism demand and limited availability of beachfront land.

The Eastern Province, which includes the tri-city area of Dammam, Al-Khobar, and Dhahran, is undergoing significant transformation with USD 2.667 billion invested in mixed-use projects such as Banan City. The expansion of the petrochemical and logistics industries is prompting executive relocations, increasing demand for luxury gated communities with convenient highway access to industrial hubs. Upcoming cross-Gulf rail services are expected to reduce travel times to Manama, enhancing the appeal of dual-country living. NEOM's initial handovers, AlWadi at Abha, and other Vision 2030 projects are extending the luxury market to secondary cities, reducing concentration and strengthening nationwide resilience.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Saudi Arabia's luxury residential real estate market features over 20 developers, resulting in a moderately concentrated environment. ROSHN Group, supported by the Public Investment Fund, leads the market with large-scale communities such as SEDRA and WAREFAH. The company integrates retail, healthcare, and leisure assets into its developments. Emaar Middle East follows a brand-focused strategy by collaborating with Vida and Address Hotels, incorporating serviced apartments into mixed-use projects to ensure consistent income streams. Dar Al Arkan leverages international design partnerships, incorporating Italian interiors and high-jewelry collaborations to enhance unit premiums in its flagship Riyadh towers.

Government-affiliated entities like Red Sea Global and Qiddiya Investment Company are entering the residential market through hospitality-driven master plans. Red Sea Global’s Desert Rock resort, a USD 200 million regenerative project, incorporates branded villas into an ecologically sensitive canyon, emphasizing experience-based differentiation. Qiddiya focuses on sports and entertainment to attract younger demographics, positioning nearby residences as lifestyle extensions. Smaller domestic developers target niche segments such as golf estates, heritage-themed compounds, and waterfront properties, benefiting from faster design approval processes compared to larger competitors.

Technology and adherence to ESG principles are increasingly critical in determining competitive advantages. Oliver Wyman’s Riyadh blueprint highlights the importance of smart-city frameworks, including 5G connectivity, autonomous shuttle systems, and centralized district cooling. Developers who adopt these features early achieve higher absorption rates and command premium pricing. The upcoming foreign-ownership law is expected to increase global scrutiny, favoring companies with strong governance, transparent escrow management, and international valuation standards. Consolidation in the market may accelerate as mid-tier developers face cost pressures and struggle to secure long-term financing.

Saudi Arabia Luxury Residential Real Estate Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Red Sea Global broke ground on the USD 200 million Desert Rock mountain resort, integrating 48 cliff-side villas and 12 hotel suites into its regenerative tourism blueprint. The project, designed by Oppenheim Architecture, elevates the developer’s luxury sustainability portfolio within the broader Red Sea destination.

- February 2025: NEOM awarded main contracts for vertical construction on THE LINE, triggering a 100 km car-free city that will deliver 9 million high-tech residences. The milestone materially advances Saudi Arabia’s most ambitious urban-luxury concept toward its late-2025 build schedule.

- February 2025: Sports Boulevard Foundation activated a USD 933 million real-estate fund to finance Urban Wadi High Rises along Riyadh’s 83 km active-lifestyle corridor. The capital injection accelerates mixed-use towers that blend premium housing with sports and wellness amenities.

- November 2024: Knowledge Economic City enlisted contractors for its USD 2.667 billion Islamic World Avenue and Madinah Gate phases, adding 840 luxury homes and 5,140 hotel keys to Madinah’s pipeline. These builds strengthen the city’s position as a high-end religious-tourism hub.

Table of Contents for Saudi Arabia Luxury Residential Real Estate Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Insights and Dynamics

- 4.1Market Overview

- 4.2Residential Real Estate Buying Trends – Socio-economic & Demographic Insights

- 4.3Rental Yield Analysis

- 4.4Regulatory Outlook

- 4.5Technological Outlook

- 4.6Insights into Existing and Upcoming Projects

- 4.7Market Drivers

- 4.7.1Rising high-net-worth individual (HNWI) population fueling demand for luxury villas and apartments

- 4.7.2Vision 2030 initiatives promoting luxury mixed-use and waterfront developments in Riyadh, Jeddah, and NEOM

- 4.7.3Growing expatriate and executive population driving demand for premium gated communities

- 4.7.4Increased foreign ownership allowances in select zones expanding buyer base

- 4.7.5Preference for branded residences and lifestyle-driven projects integrating wellness and smart home features

- 4.8Market Restraints

- 4.8.1High construction and land costs increasing overall project pricing

- 4.8.2Regulatory and procedural complexities slowing approvals in luxury zones

- 4.8.3Economic dependence on oil revenues creating volatility in luxury demand cycles

- 4.9Value / Supply-Chain Analysis

- 4.9.1Overview

- 4.9.2Real Estate Developers and Contractors - Key Quantitative and Qualitative Insights

- 4.9.3Real Estate Brokers and Agents - Key Quantitative and Qualitative Insights

- 4.9.4Property Management Companies - Key Quantitative and Qualitative Insights

- 4.9.5Insights on Valuation Advisory and Other Real Estate Services

- 4.9.6State of the Building Materials Industry and Partnerships with Key Developers

- 4.9.7Insights on Key Strategic Real Estate Investors/Buyers in the Market

- 4.10Porter’s Five Forces

- 4.10.1Threat of New Entrants

- 4.10.2Bargaining Power of Buyers

- 4.10.3Bargaining Power of Suppliers

- 4.10.4Threat of Substitutes

- 4.10.5Competitive Rivalry Intensity

5. Residential Real Estate Market Size & Growth Forecasts (Value USD billion)

- 5.1By Business Model

- 5.1.1Sales

- 5.1.2Rental

6. Residential Real Estate Market (Sales Model) Size & Growth Forecasts (Value USD billion)

- 6.1By Property Type

- 6.1.1Apartments & Condominiums

- 6.1.2Villas & Landed Houses

- 6.2By Mode of Sale

- 6.2.1Primary (New-Build)

- 6.2.2Secondary (Existing-Home Resale)

- 6.3By City

- 6.3.1Riyadh

- 6.3.2Jeddah

- 6.3.3DMA (Dammam metropolitan area)

- 6.3.4Rest of Saudi Arabia

7. Competitive Landscape

- 7.1Market Concentration

- 7.2Strategic Moves (M&A, Joint Ventures, etc)

- 7.3Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)}

- 7.3.1Dar Al Arkan

- 7.3.2ROSHN (PIF)

- 7.3.3Emaar Middle East

- 7.3.4Jeddah Economic Co.

- 7.3.5Kingdom Holding – Real Estate

- 7.3.6Al Akaria

- 7.3.7Cayan Group

- 7.3.8Red Sea Global (residential)

- 7.3.9Qiddiya Investment Co.

- 7.3.10Omrania Development

- 7.3.11Al Rajhi Real Estate

- 7.3.12Tatweer Real Estate

- 7.3.13Al Tahaluf Real Estate

- 7.3.14Dallah Real Estate

- 7.3.15Al Balad Development Co.

- 7.3.16Sedco Development

- 7.3.17Hashem Contracting & Real Estate

- 7.3.18Rafal Real Estate

- 7.3.19Misk City Developers

- 7.3.20Retal Urban Development

8. Market Opportunities & Future Outlook

- 8.1White-Space & Unmet-Need Assessment

Saudi Arabia Luxury Residential Real Estate Market Report Scope

Luxury residential real estate encompasses properties crafted for human habitation, offering a blend of allure and resort-style living, complete with upscale amenities.

Saudi Arabia's luxury residential real estate market is segmented by type (apartments and condominiums and villas and landed houses) and by key cities (Riyadh, Jeddah, Makkah, Dammam Metropolitan Area (DMA), and Other Cities). The report offers market size and forecasts for the Saudi Arabian Luxury Residential Real Estate Market in value (USD) for all the above segments.