Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

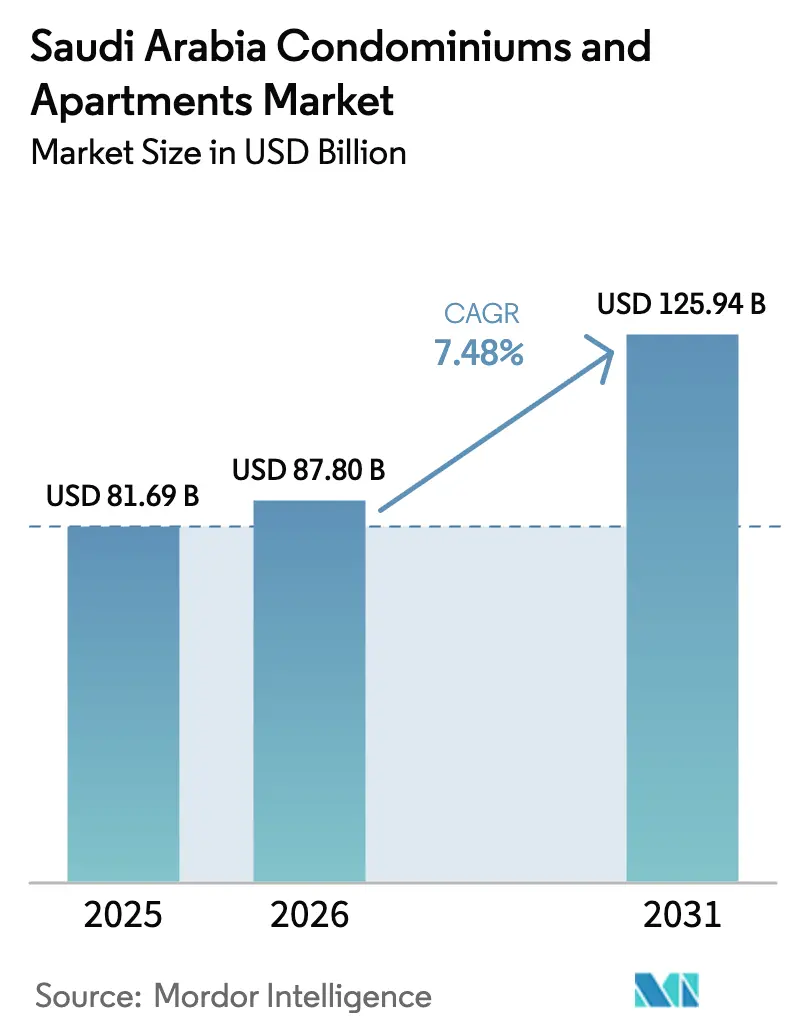

| Base Year Market Size (2025) | USD 81.69 Billion |

| Market Size (2026) | USD 87.8 Billion |

| Market Size (2031) | USD 125.94 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

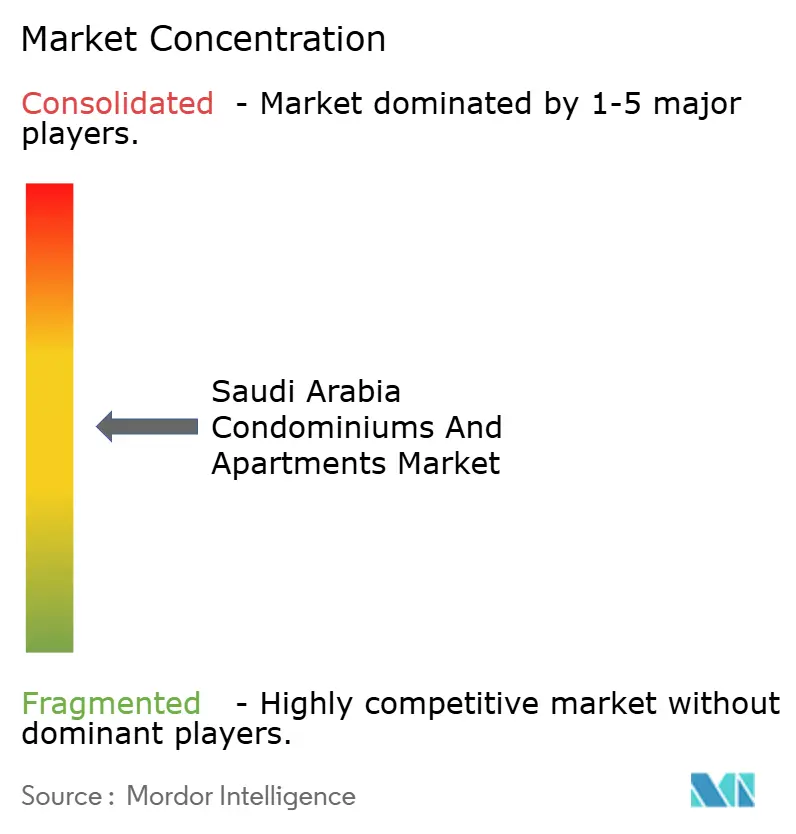

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Condominiums And Apartments Market Analysis by Mordor Intelligence

The Saudi Arabia condominiums and apartments market size is expected to grow from USD 81.69 billion in 2025 to USD 87.8 billion in 2026 and is forecast to reach USD 125.94 billion by 2031 at 7.48% CAGR over 2026-2031. Growing urbanization tied to Vision 2030 megaprojects, the Kingdom’s young demographic profile, and government-subsidized mortgages are enlarging the pool of potential buyers. Developers are accelerating launches of smart, amenity-rich buildings to capture shifting lifestyle preferences, while new foreign-ownership rules are expected to deepen the demand base from 2026. At the same time, construction-cost inflation and nascent rent-control discussions create cost-management and policy-monitoring imperatives for market participants. Overall, the Saudi Arabia condominiums and apartments market continues to attract both public and private capital keen on long-run residential yields.

Key Report Takeaways

- By business model, Sales led with 65.40% of the Saudi Arabia condominiums and apartments market share in 2025; Rental is projected to grow at 7.98% CAGR through 2031.

- By price band, Mid-Market captured 49.02% of the Saudi Arabia condominiums and apartments market in 2025, while Affordable is set to expand at 8.11% CAGR to 2031.

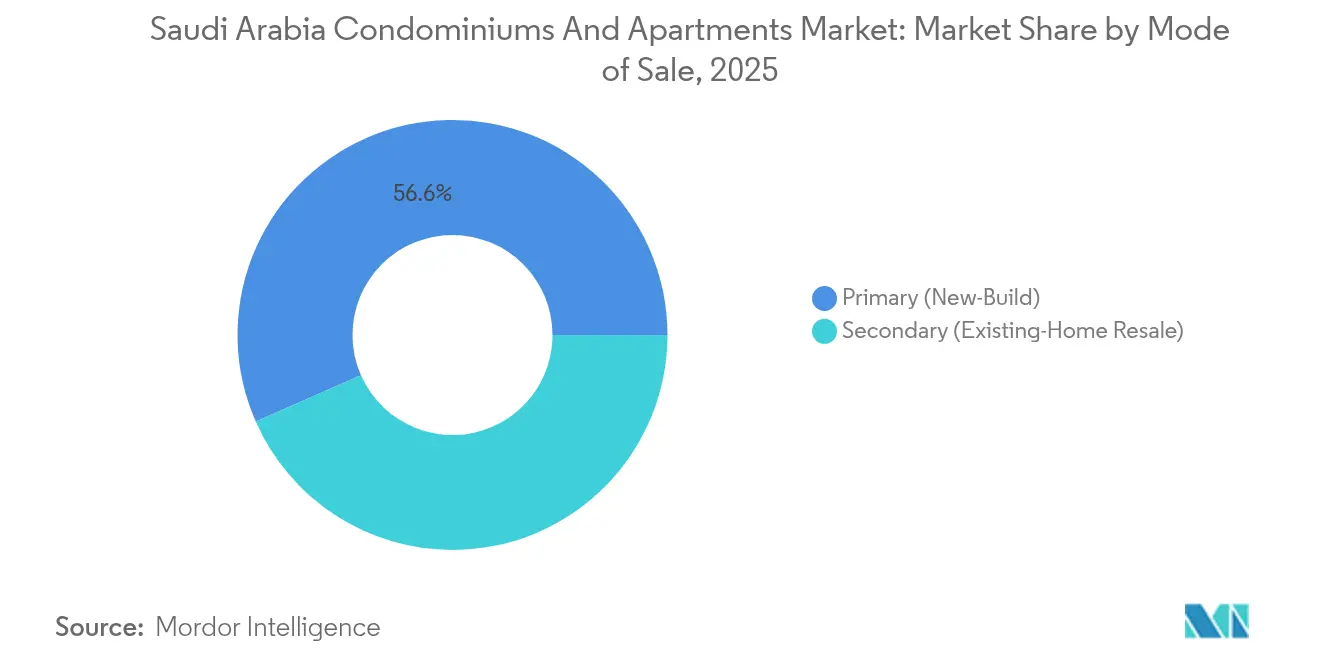

- By mode of sale, Primary accounted for 56.60% of the Saudi Arabia condominiums and apartments market in 2025 and is advancing at an 8.43% CAGR through 2031.

- By geography, Riyadh held 46.20% revenue share in 2025; the Dammam Metropolitan Area is forecast to post the fastest 8.75% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Condominiums And Apartments Market Trends and Insights

Drivers Impact Analysis*

| Drivers | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 urban development driving demand for high-density residential formats | +2.1% | National, with concentrated gains in Riyadh, Jeddah, NEOM | Long term (≥ 4 years) |

| Rising young population and smaller household sizes boosting apartment demand | +1.8% | National, with stronger influence in urban centers | Medium term (2-4 years) |

| Increased expatriate housing needs in Riyadh, Jeddah, and Dammam | +1.4% | Riyadh, Jeddah, DMA core markets | Short term (≤ 2 years) |

| Government-backed mortgage and homeownership programs supporting affordability | +1.2% | National, with emphasis on first-time buyers | Medium term (2-4 years) |

| Growing preference for modern amenities, smart homes, and gated apartment communities | +0.9% | Premium segments in Riyadh, Jeddah, emerging in secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Urban Developments

Vision 2030 giga-projects such as NEOM and the Mukaab are redefining the Saudi residential ecosystem by creating employment hubs anchored by high-density housing. These projects channel over USD 3332.5 million into mixed-use residential assets that normalize vertical living concepts previously uncommon in the Kingdom. Planned capacity for millions of new residents near high-value job centers sustains long-run demand for condominiums, encouraging developers to prioritize apartment-led communities over low-rise villas. Public-sector backing mitigates infrastructure risk and sends a strong signal to private investors seeking stable pipelines. As construction phases overlap through 2030 and beyond, the Saudi Arabia condominiums and apartments market is poised to absorb continuous supply without derailing price stability.

Rising Young Population and Smaller Households

Seventy-one percent of Saudis are under 35, and average household size has narrowed to 5.2 persons, trends that tilt preferences toward compact, well-located apartments. The demographic dividend boosts the pool of mortgage-ready buyers who favor proximity to workplaces over suburban living. Increasing numbers of single-person and dual-income households gravitate toward serviced apartments with shared amenities that reduce running costs. Developers offering integrated gyms, co-working lounges, and community retail report higher pre-sales velocity, underscoring the segment’s pull. The resulting uplift spreads across primary and secondary cities, solidifying the growth runway for the Saudi Arabia condominiums and apartments market[1]Fahad al-Dosari, “Household Housing Survey 2024,” General Authority for Statistics, stats.gov.sa.

Increasing Expatriate Housing Needs

More than 200 multinational corporations have secured licenses for regional headquarters in Riyadh, accelerating expatriate inflows that require immediate apartment leasing options. Monthly rents for one-bedroom units in the capital average USD 1,333, and premium compounds command annual leases above USD 133,300, sustaining attractive landlord yields. Managed apartment complexes gain traction by offering language-friendly leasing platforms and bundled services that match expatriate expectations. In Jeddah and Dammam, rapid petrochemical and logistics expansion mirrors the trend, prompting landlords to refurbish stock into turnkey apartments. Combined, these inflows add momentum to the near-term leasing arm of the Saudi Arabia condominiums and apartments market.

Government-Backed Mortgage Programs

The Sakani platform has facilitated more than 800,000 subsidized housing contracts, driving home-ownership to 63.74% by 2024 and feeding sustained demand for mid-market apartments. Mortgage-to-value caps at 70% keep systemic risk in check while generous interest-rate support lowers entry barriers for first-time buyers. Islamic finance products widen eligibility, attracting religiously compliant borrowers into the formal housing finance system. The program’s target of 355,000 additional contracts by 2025 equates to roughly USD 41.8 billion in new credit flowing into residential real estate. Consequently, developers calibrate launch pipelines toward price points aligned with subsidy thresholds, supporting volume growth across the Saudi Arabia condominiums and apartments market.

Restraints Impact Analysis*

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural preference for villas in certain segments slowing condo adoption | -1.6% | Traditional segments nationwide, stronger in suburban areas | Long term (≥ 4 years) |

| High construction costs impacting project feasibility | -1.1% | National, with acute pressure in premium developments | Short term (≤ 2 years) |

| Regulatory and approval delays affecting large-scale urban projects | -0.8% | National, with concentrated impact in Riyadh and Jeddah mega-projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cultural Villa Preference

Deep-rooted affinity for standalone villas tempers condominium demand in many family-oriented segments. Villa transactions still form more than half of residential deals in Riyadh, signaling latent resistance to vertical living among larger households. Developers counter by embedding villa-level amenity packages, private gardens, family recreation courts, and generous parking into apartment master-plans. Over time, younger Saudis show a a willingness to trade private land for on-site facilities and shorter commutes, gradually eroding the cultural barrier. Still, the villa mindset remains a structural drag on the Saudi Arabia condominiums and apartments market’s ultimate penetration ceiling.

High Construction Costs

Material price volatility and supply-chain bottlenecks push Saudi construction outlays to USD 141.5 billion, squeezing developer margins, especially for price-sensitive mid-market projects. Steel, cement, and labor costs rise faster than unit selling prices, challenging feasibility calculations. Government fast-track programs like Etmam shorten approval cycles, but payment lags in public projects can create cash-flow strain. Developers respond with modular building techniques and long-term procurement contracts to lock in prices. Despite mitigation measures, sustained cost inflation can delay groundbreaking and slow supply additions within the Saudi Arabia condominiums and apartments market[2]Saad al-Harbi, “Construction Cost Trends 2025,” Saudi Building Code National Committee, sbc.gov.sa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Sales Dominance and Rental Momentum

The Sales segment occupied 65.40% of the Saudi Arabia condominiums and apartments market in 2025, underpinned by pervasive home-ownership aspirations and broad mortgage support. Rental activity, although smaller, is projected to expand at an 7.98% CAGR, outpacing ownership growth as expatriate arrivals intensify. Developers reliant on off-plan sales through the Wafi system enjoy early cash inflows, reinforcing project liquidity. Conversely, institutional landlords accumulate portfolios to capture rising rental yields of 5%-8%, diversifying revenue across the Saudi Arabia condominiums and apartments market.

Rental pressure is most visible in central Riyadh, where a one-bedroom apartment exceeds USD 1,333 per month, nudging young professionals toward ownership once mortgage subsidies become accessible. Lack of rent-increase caps amplifies this shift, although regulators are studying ceiling mechanisms to curb inflation. In Jeddah, premium districts post 11.7% gross yields, cementing the city’s appeal for income-focused investors. Across both models, transparent digital platforms such as Ejar safeguard tenancy contracts, fortifying market confidence and fostering balanced growth in the Saudi Arabia condominiums and apartments market.

By Price Band: Mid-Market Leadership and Affordable Upswing

Mid-Market units controlled 49.02% of 2025 transaction value, aligning with the spending power of middle-income Saudis and skilled expatriates. Units in this bracket often list between USD 270,000-USD 400,000 and feature smart-home readiness plus shared leisure amenities. Because mortgage subsidies partly offset monthly installments, absorption rates remain healthy even as interest rates fluctuate. Accordingly, the Saudi Arabia condominiums and apartments market size for Mid-Market properties stays resilient during macro-shifts.

Affordable housing, though smaller today, is projected to grow at an 8.11% CAGR through 2031 as Vision 2030 targets 70% national homeownership. Policies such as the White Land Tax release serviced plots at no more than USD 400 per square meter, obliging developers to add stock priced within subsidy thresholds. ROSHN’s mixed-income communities illustrate the model: apartments start near USD 160,000 yet still include landscaped courtyards and proximity to public transit. This supply pipeline directly enlarges the Saudi Arabia condominiums and apartments market, ensuring lower-income households gain formal housing access.

By Mode of Sale: Primary Innovation Outpaces Secondary Activity

Primary (new-build) transactions represented 56.60% of 2025 turnover and are forecast to increase at an 8.43% CAGR through 2031. Warranty coverage, green-building credentials, and flexible payment plans bolster buyer confidence in new stock. Developers leverage the Etmam fast-track to compress licensing timelines, while off-plan rules under Wafi unlock earlier revenue recognition. In turn, the Saudi Arabia condominiums and apartments market size for primary sales benefits from accelerated inventory churn.

The Secondary market remains relevant for buyers seeking mature neighborhoods or immediate occupancy. Yet the 5% Real Estate Transaction Tax introduced in 2025 raises all-in acquisition costs, prompting some households to favor presales where the levy is embedded in launch pricing. As foreign-ownership zones open in 2026, secondary units in designated areas may regain momentum, but fresh supply equipped with smart infrastructure is likely to capture a larger share of international demand within the Saudi Arabia condominiums and apartments market.

Geography Analysis

Riyadh captured 46.20% of the national condominium and apartment value in 2025 on the back of public-sector employment, multinational headquarters inflows, and the headline-grabbing Mukaab project. The city’s population is on track to hit 9.6 million by 2030, adding pressure for at least 305,000 more housing units. ROSHN’s SEDRA alone will supply 30,000 homes, while average apartment rents command USD 1,333 monthly, sustaining developer margins. As a result, Riyadh remains the anchor of the Saudi Arabia condominiums and apartments market, even as land-price appreciation nudges development outward to planned satellite cities.

Jeddah combines Red Sea trade, pilgrimage traffic, and lifestyle appeal to rank as the second-largest urban market. The USD 3.33 billion Jeddah Central Project will add 17,000 units set around cultural landmarks, elevating the city’s waterfront profile. Premium districts return gross rental yields above 11%, attracting investors aiming for income diversification. ROSHN’s ALAROUS community layers in 18,000 homes across 4 million m², underscoring scale and reinforcing the Saudi Arabia condominiums and apartments market expansion on the west coast.

The Dammam Metropolitan Area is forecast to log the fastest 8.75% CAGR through 2031 as energy majors and downstream clusters enlarge the expatriate workforce. ROSHN’s ALFULWA near Hofuf, spanning 10.8 million m² with 18,000 homes, signals institutional confidence in Eastern Province growth. Nearby, NEOM’s coastal enclaves and Madinah’s Knowledge Economic City indicate that secondary cities are integrating residential infill into wider economic strategies. Collectively, these zones enlarge the geographic footprint of the Saudi Arabia condominiums and apartments market beyond the traditional tri-city corridor.

Competitive Landscape

Government-linked ROSHN commands prime land access and capital, positioning it as the pace-setter in large-scale communities that blend residential, retail, and green space. Brand Finance ranks ROSHN among the world’s 25 most powerful real-estate brands, crediting its 200 million-m² pipeline and consistent smart-city themes. Private players such as Dar Global focus on premium offerings, including a recent USD 234.6 million project aimed at investors seeking Premium Residency visas. Meanwhile, domestic developers strike partnerships, for example, the Talaat Moustafa-Al Muhaidib joint venture behind Banan City’s planned 27,000 units, to share risk and accelerate delivery.

Technology is a primary differentiator. Projects like Banan City integrate 20,000 IoT-enabled homes that monitor energy, security, and community logistics in real time, elevating resident experience and lowering operating costs. Compliance with the 2024 Saudi Building Code update and international LEED benchmarks adds another layer of competitive sorting; firms with established engineering capacity and long procurement cycles move faster through certification gates. Anticipated 2026 foreign-ownership liberalization will likely intensify competition from global developers with luxury branding, but incumbents with local approvals expertise remain well-placed to defend share within the Saudi Arabia condominiums and apartments market.

White-space opportunities persist in affordable housing across secondary cities, where demand often overshoots supply even after policy incentives. Developers able to blend modular construction, green finance, and mixed-income master-planning are expected to capture untapped pools of first-time buyers. Given rising land values in core markets, land-banking strategies in peripheral zones, and public-private partnerships, will shape the next wave of growth in the Saudi Arabian condominiums and apartments market.

Saudi Arabia Condominiums And Apartments Industry Leaders

Kingdom Holding Company

Ewaan Global Residential

Al Ra’idah Investment Co.

SEDCO Development

Rafal Real Estate Dev.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Saudi Council of Ministers approved Resolution No. M/14 permitting non-Saudis to own residential property in zoned areas from Jan 2026, subject to transaction fees up to 5%.

- March 2025: Zakat, Tax & Customs Authority enforced a 5% Real Estate Transaction Tax on disposals and off-plan sales, outlining exemptions and refund procedures.

- March 2025: Dar Global disclosed land acquisitions worth USD 234.6 million to scale luxury residential launches across Riyadh and Jeddah.

- March 2024: Talaat Moustafa Group and Al Muhaidib Group formed a joint venture to develop Banan City’s 27,000 residential units in Riyadh.

Saudi Arabia Condominiums And Apartments Market Report Scope

Condominiums and apartments are residential units within multi-unit buildings or complexes. Condominiums are individually owned units within a building, while apartments are rented or leased from a property owner or management company. The Saudi Arabian condominiums and apartments market is segmented by type and city. By type, the market is segmented into condominiums and apartments. By city, the market is segmented into Riyadh, Jeddah, Makkah, Dammam Metropolitan Area (DMA), and the Rest of Saudi Arabia. The report offers market size and forecasts for the Saudi Arabian condominiums and apartments market in value (USD) for all the above segments.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

What is the 2026 value of the Saudi Arabia condominiums and apartments market?

The market is valued at USD 87.8 billion in 2026 and is forecast to reach USD 125.94 billion by 2031.

How fast is the sector growing?

The market is expanding at a 7.48% CAGR during 2026-2031, supported by Vision 2030 urban programs and mortgage subsidies.

Which city holds the largest share of condominium and apartment transactions?

Riyadh leads with 46.20% of national transaction value, buoyed by population growth and mega-project pipelines.

What segment is expanding the quickest?

Affordable apartments are projected to grow at an 8.11% CAGR thanks to land-release policies and housing subsidies.

Page last updated on: